ablokhin

The year was 1994 and Swedish pop group Ace of Base had come out with a chart topping The Sign, the Federal fund rates would peak at 6.50%, and the North American Free Trade Agreement went into operation for the first time. Macerich (NYSE:MAC) would go public this year, marking a milestone in a history that would come to be punctuated by tragedy, lost dreams, and a constant fight for survival. Co-founded in the 1960s by Mace Siegel and Richard Cohen whose first names combine to form Macerich, the company would quickly go on to build 18 strip centres which all counted a well-established discount store as an anchor tenant. The anchors would act as magnets for customers to form a symbiotic relationship with Macerich.

The company’s fate has always been tied to the financial viability of its anchors. Of the initial 18 strip centres owned by the first iteration of Macerich, 16 were anchored by Arlan’s. A discount chain that began to suffer towards the end of the decade and would file for bankruptcy in 1973 and then for eventual liquidation in 1975. Even during its foundational years, Macerich was plagued by the wheels of capitalism. A type of creative destruction that would see the old swept aside after being disrupted by the new.

Arlan’s would be the first in a long list of subsequent anchors from J.C. Penney to Sears that would go bankrupt in the decades after. Indeed, the new millennium would usher in the internet and a world speeding faster into a new creative destruction force posed by the development and proliferation of the internet. This did not prevent all-time highs from being reached just before the global financial crisis in 2008, highs that Macerich would flirt with again in 2016. But this year saw record retail bankruptcies. Aeropostale, Vestis Group, Sports Authority. This was an era of great change on par with the very same disruption that saw malls proliferate and move commerce out of urban centers in the years following the end of the second world war.

Retail Bankruptcies, A Blessing In Disguise?

Macerich’s earnings for its fiscal 2022 third quarter saw revenue come in at $210.7 million, a small decline of 0.7% over the year-ago quarter but a beat of $6.97 million on consensus estimates. This was driven by a sequential 30 basis point rise in portfolio occupancy to 92.1% from 91.8%. The portfolio saw average sales for tenants under 10,000 feet of $877 per foot, a new record with footfall recovering to about 95% of the pre-pandemic level. Macerich’s tenants continued to realize healthy customer demand even against the bleak macroeconomic backdrop, with comparable year-to-date tenant sales up 5% versus the year-ago period and up more than 13% compared to pre-pandemic fiscal 2019.

Leasing activity was strong with 219 leases for 1.1 million square feet executed during the quarter. This saw same-centre NOI growth of 2.1% over the year-ago period as FFO came in at $0.46 per share, broadly flat sequentially but a small increase from $0.45 in the year-ago quarter. This supported a quarterly cash dividend payout of $0.17 per share, an 13.3% increase over the prior dividend. There is more room for this to move up with the company’s overall performance against pre-pandemic numbers generally quite healthy. The current quarterly payout still sits more than 70% below the pre-pandemic averages.

During the earnings call for its fiscal 2017 first quarter, ex-CEO Arthur Coppola stated that retail bankruptcies were a blessing in disguise as it allows Macerich to redevelop a space currently being occupied by a company swept away by creative destruction. Hence, the company continued to focus intensely on redevelopment during the quarter with a number of projects underway including the transformation of around 150,000 square foot of space formerly occupied by Bloomingdale’s in Santa Monica Place to a new destination with a high-end fitness club and co-working space. The company anticipates this costing between $35 million to $40 million with an estimated yield of 22% to 24%.

For the full-year 2022, Macerich lowered FFO guidance to between $1.93 to $1.99, versus its previous range of $1.92 to $2.04. This represents a $0.02 per share decline in FFO guidance at the midpoint and reflects broad economic uncertainty as we close out the year.

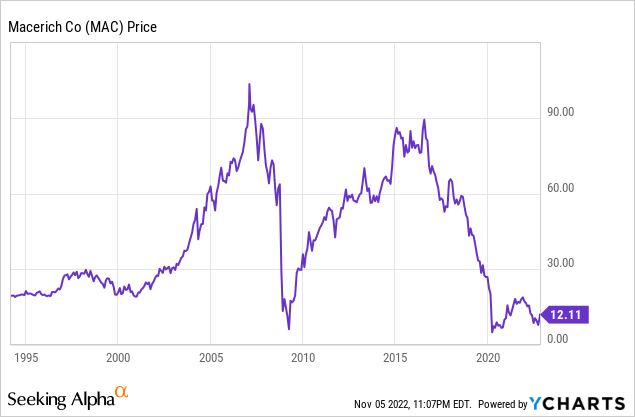

Will Shares Ever Go Back To 2016 Again?

Mark Twain, a famous American writer and humorist, in response to a British journalist who contacted him to ask whether the rumours that he was dead were true, replied stating that such reports of his death were an exaggeration. How else would one be able to respond to a journalist seeking comments on one’s own death? Macerich has faced and will continue to face a similar conundrum. This tale of creative destruction has formed part of its life since its creation, sped up by the pandemic, but one that Macerich has seized to reinvest itself time and time again.

The company currently trades at just over a 10% discount to its $13.48 tangible book value per share as of the end of the quarter. The dividend raise and continued strength in leasing would have supported this gap being closed. But the strong likelihood of the US falling into a recession next year likely warrants a level of discounting. Macerich continues to be a company that will survive in the face of change but shares are unlikely to see 2016 again until sentiment evolves and the company redevelopments feed into growth.

Be the first to comment