Feverpitched

Rental properties are some of the most popular investments of individual investors.

It makes sense.

The idea of buying a property with the bank’s money and then having a tenant reimburse your mortgage for you, and owning the property free and clear in a few decades, is a very compelling idea.

If you structure things well, you may even earn cash flow along the way and enjoy tax benefits.

Finally, it will also diversify your portfolio and protect a portion of it from the high stock market volatility.

So on the surface, it sounds like a no-brainer…

Relatively low risk… High returns… And lots of income.

I have invested in rental properties in the past and thought that this idea was so compelling that I eventually went to work in private equity real estate.

Even then, I think that rental properties are today some of the worst investments that you could make.

Let me explain why…

There are 5 main reasons:

Reason #1: The Returns Are Not As High As You Think

When you first start to learn about the idea of investing in rental properties, you will likely end up on some blog or YouTube channel where a real estate guru will teach about real estate investing, but will also likely try to sell you on some course or something else.

Naturally, they will want to make it sound as compelling as possible to catch your attention and will greatly overstate the returns, claiming you will earn 20, 25, or even 30% annual returns.

But these numbers aren’t remotely close to reality in most cases.

Warren Buffett became the richest man on earth by compounding the returns of Berkshire Hathaway (BRK.B) at 20% per year, so I can assure you that part-time amateur rental investors are not compounding at more than him. We would have many more real estate billionaires otherwise!

Instead, these people are simply miscalculating their returns.

The two most common mistakes are the following:

1) They understate their real expenses: The expenses of owning a property are very significant and they are commonly underestimated because many of these expenses only occur once in a while when something major breaks down. To give you an example, if your roof has a leak, and it isn’t caught early on, your house could suffer water damage that costs $30,000 to fix. That could be 3 years’ worth of net operating income. You need to account for an average annual cost for major repair items like this and it materially lowers your returns. A good rule of thumb is that your net operating income is about 50% of your gross rental income and even that may not cover all these repair items over time.

2) They forget to account for the value of their own time/work: This is the biggest misconception when it comes to rental properties. People will put a huge amount of work/hours into finding their rental property, negotiating it, financing it, renovating it, marketing it, managing it, etc. but they will assume that their work is worth 0 when calculating returns when in reality, each hour has a cost since you could use this time to do something else that’s productive. You could have just as well worked extra hours at your main job or worked a second job and earned $30 per hour of work. If you deduct all of that from your rental income, you will often find that you didn’t buy an investment, you just bought a second job. The returns from the investment are very low and you are just earning a “salary” on your work/time.

Once you properly calculate returns, you will typically end up with 8-15% annual returns. That’s still very good, but it is nowhere near the 20-30% returns that are commonly touted to new investors. Real estate is a relatively easy, low-margin business, with a lot of competition.

Reason #2: The Risks Are a Lot Greater Than You Think

People will commonly imagine that rental properties are safe investments because they are immune to the volatility of the stock market. In comparison to stocks, they feel like safe and defensive investments and this is particularly true when the stock market is as volatile as today. Moreover, everyone will always need a roof over their head, whether we go into a recession or not.

But this is very short-sighted.

The risks are actually very significant and in fact, a lot greater than those of investments in the stock market.

When you buy a rental property, you need to understand that you are making a private, illiquid, concentrated investment with high leverage, social risks, and unlimited liability in many cases.

Even if you use an LLC or insurance, you will still typically need to sign personally on the loans, and if things go wrong, the tenant will also sue you personally, not just your LLC. It is not just your returns that could be ruined, but also your personal life because these things could lead to significant stress and sleepless nights, which is probably the biggest risk of all.

Besides, even the belief of “low volatility” is a myth. Just because you aren’t getting a daily quote does not mean that your home value isn’t volatile.

If you tried to sell your property, you would get different offers every day, which proves my point that its value would be very volatile. And since rental investors commonly use high leverage, the value of your equity (which is what’s traded on the stock market), would be extremely volatile.

If you are 80% leveraged, and you received an offer at a 10% lower price, that’s a 50% drop in your equity value. So the real “hidden” volatility is actually huge, but you just don’t know about it. Any setback that could happen could cause a significant drop in your equity value.

Reason #3: It Handicaps Your Primary Source of Income

Your primary source of income is your career. This should be your main focus.

You want to advance in your career and increase your income so that you can invest more and eventually set yourself free.

But if you buy a rental property, let alone many of them, this will significantly handicap your ability to advance in your career.

It will take a lot of your time and energy, and will also tie you to a specific location because you will be more reluctant to move elsewhere since you would leave back all your properties and the local market knowledge that you have developed.

This could lead to significant indirect costs since you may not get the pay raise that you would have gotten if you had the time, energy, and freedom to focus on your primary source of income.

This is particularly true for higher earners because investing time and energy in rental properties (a low margin business) is time taken away from your highly rewarding activities. Think about a lawyer taking his time that’s worth $100s each hour to work on rental properties… It is not logical.

Reason #4: It Also Handicaps Your Lifestyle

Life isn’t just about money.

I would much rather earn stress and work-free 10% return which gives me total freedom than a work-intensive 12% that ties me to a specific place and results in occasional sleepless nights.

Owning rental properties will hurt your lifestyle because it is time-consuming, and energy-draining, reduces your freedom of movement, and will eventually also lead to social issues as well.

You will doubt taking long trips. You will get calls from your tenant or property manager about issues when you wish that you could just relax. And worst of all, you might get threats from your tenant, causing you to lose sleep at night or worse. It could literally affect your health!

Reason #5: There’s a Much Simpler and Better Alternative: REITs

Even despite all of what I mentioned earlier, real estate can still be a great investment if you find the right property at the right price.

But why bother when you could just invest in publicly listed real estate investment trusts (“REITs”) (VNQ) instead?

REITs allow you to invest in real estate with the added benefits of:

-

Diversification

-

Professional management

-

Limited liability

-

Liquidity

-

Total freedom.

They allow you to keep focusing on your primary source of income, which is your career, and they won’t hurt your lifestyle. On the contrary, they give you total freedom since you have professional management teams that work for you, and the management is far more efficient because REITs enjoy significant economies of scale.

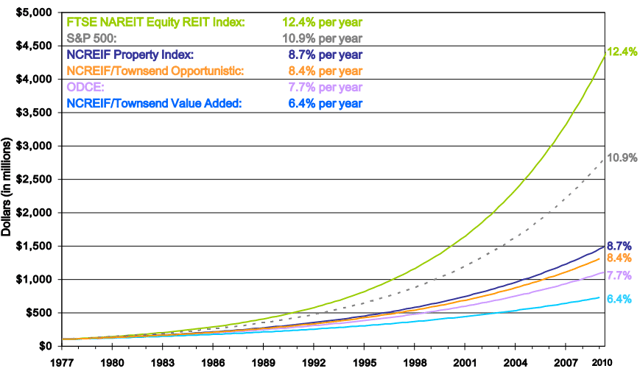

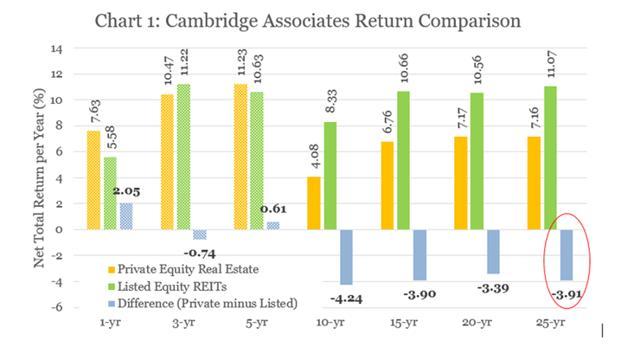

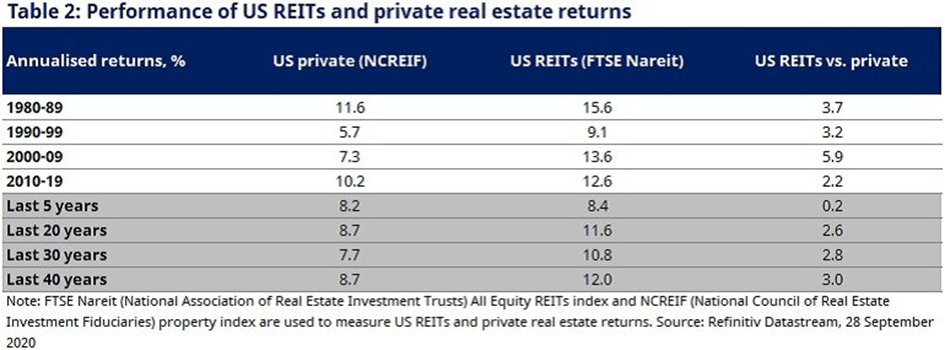

This is one of the reasons why REITs have historically outperformed private real estate investments by 2-4% per year. Their scale gives them a significant cost advantage in not just management, but also all other expenses.

Here are three studies that compare the returns of REITs to private real estate investments:

EPRA Cambridge NAREIT

So, why would you invest in rental properties when you could invest in REITs, and earn higher returns with lower risk and less effort?

This is especially true today since REITs are heavily discounted relative to the value of the real estate they own.

To give you an example: BSR REIT (OTCPK:BSRTF) owns a portfolio of apartment communities in Texas, and its net asset value per share is $22.35, but its share price is just $12.50. So, you get to invest in its real estate at 60 cents on the dollar.

The low valuation provides a significant margin of safety and future upside potential as REIT valuations eventually recover.

I would prefer to buy REITs over rental properties even if the valuations were equivalent, but at today’s discount, I just can’t make any sense of buying rental properties.

Bottom Line

I was once a rental investor, but I am now a converted REIT investor.

I think that rental properties are poor investments in most cases because investors overstate returns, understate risks, and fail to take into account the negative impact that it will have on their careers and lifestyle.

Besides, REITs offer better returns with lower risk and less effort, so why bother?

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment