SDI Productions

Investment thesis

MultiPlan (NYSE:MPLN) is a provider of data analytics and cost management solutions to the U.S. healthcare industry. The demand for these solutions is likely to be strong due to rising healthcare costs and a focus on finding ways to lower those costs and enhance the reliability of payments. However, while the business has compelling value proposition, I am staying away from the stock due to very bad near-term outlook and lack of visible upsides.

Business overview

MultiPlan is a provider of data analytics and cost management solutions to the U.S. healthcare industry. The company uses technology to offer end-to-end solutions that add value for its clients.

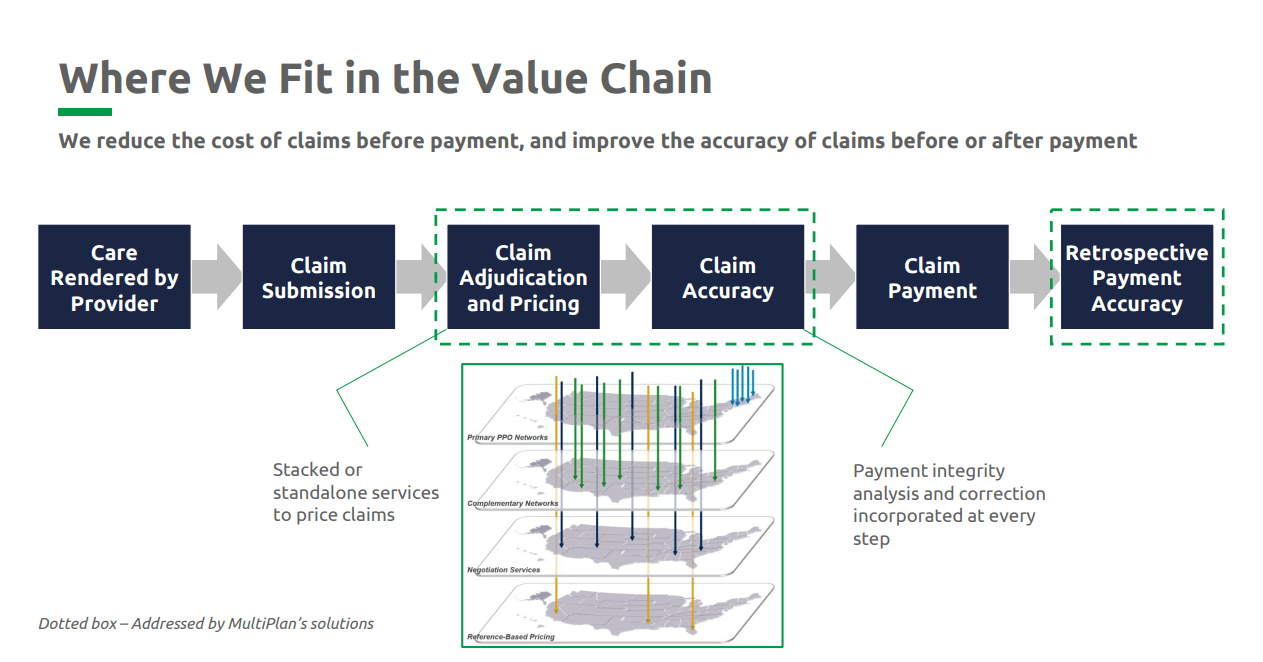

June 22 presentation

Healthcare industry would benefit a lot from cost management solutions

As reported by CMS, national healthcare spending in 2021 was $4.3 trillion, or $13,000 per person, or 18.3% of GDP. By the year 2030, CMS predicts this number will have risen to $6.8 trillion. I attribute this to multiple factors, not the least of which is the long-term trend of an aging population, which is influencing both the expansion of healthcare coverage and the rise in healthcare consumption. Having access to cutting-edge medical technology also drives up healthcare costs even further. As healthcare costs continue to rise, I believe that stakeholders, especially payors, will place a greater emphasis on finding ways to lower those costs and enhance the reliability of their payments.

Therefore, I anticipate that solutions provided by MPLN will remain highly valued by payors. In my opinion, there are two main factors that will cause the demand for these services to rise:

- A rise in claim expenses caused by rising medical inflation and improved medical technology

- An aging population and a rise in the number of people who are covered by health insurance have contributed to a rise in the overall volume of patients seeking treatment.

The combination of an aging population, sustained attention to primary and preventive care, and developing medical technologies bodes well for future healthcare activity. Consequently, I expect there to be a rise in interest in and use of MPLN solutions as the volume and value of medical claims continue to grow. Since MPLN’s access fee is predominately based on a percentage of the savings realized, it stands to gain from the general upward trend in medical costs. Eventually, I think MPL will be able to help slow down the rising tide of healthcare prices, which will bring about even greater cost savings for their clients.

Proprietary IT platform

After the recent upgrade, I think MPLN’s IT platform is a major competitive advantage. Because of this improvement, MPLN can now automatically process and store a vastly greater volume of transactions, greatly expanding its ability to cater to its user base. It is designed for high throughput and can return almost every claim within one day. This quickness is enhanced by the MPLN’s connectivity with electronic data interchange [EDI] and direct web service integration [DWSI]. I believe that the increased use of EDI and DWSI for claims processing at MPLN will lead to greater back-office interconnectivity as a result of the company’s electronic integration with customers. This results in a dramatic decrease in complexity and processing errors, which translates to substantial savings over time.

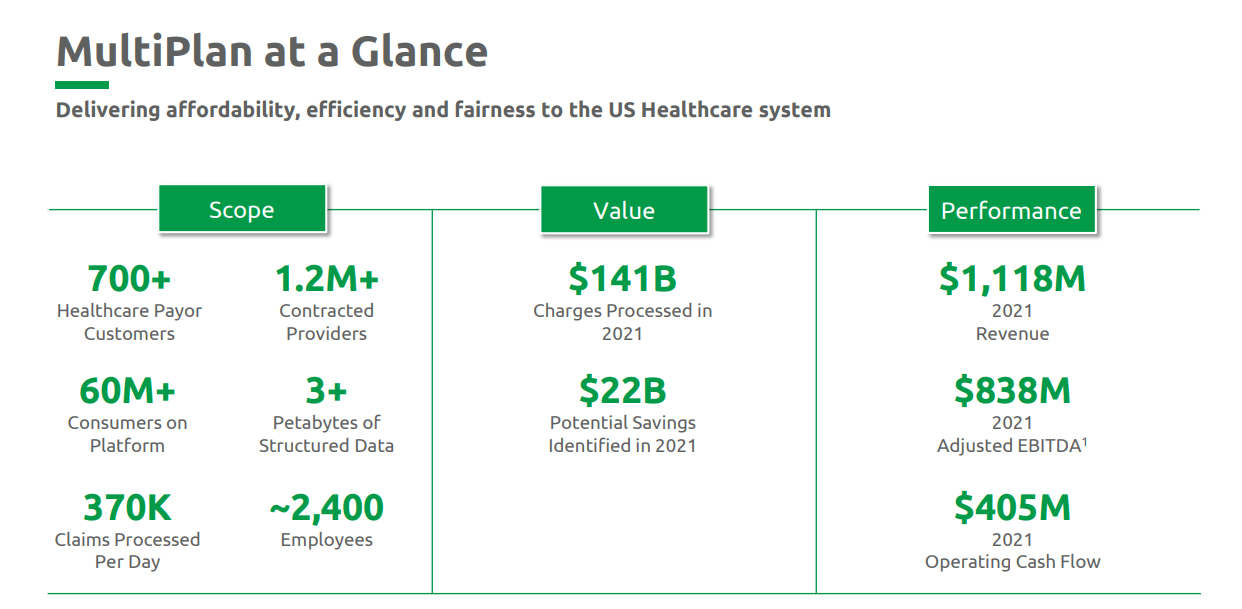

The MPLN IT platform is also extensible. Large increases in volume are easily accommodated with negligible additional expenses. For context, consider that the MPLN platform handles 370,000 daily claims and has access to 3 petabytes of structured data in the form of claim history.

Jun 22 presentation

Long-standing relationships highly recurring revenue base

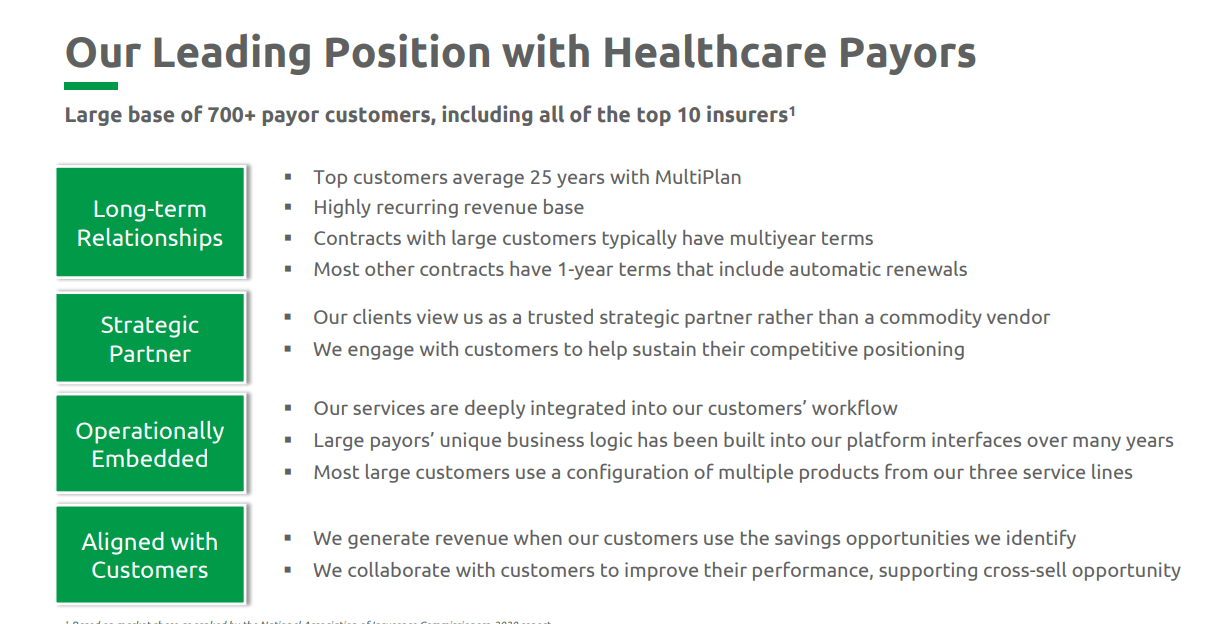

MPLN has been doing business with almost all of the major health plans for years. Customers are less likely to leave these partnerships due to the high switching costs involved because MultiPlan’s logo appears on many commercial customers’ membership cards. More importantly, company is electronically embedded to clients’ claims processing functions.

The majority of MPLN’s annual revenue comes from a small number of customers who have been with the company for an average of 25 years and who have signed multiyear contracts. MPLN has a strong track record of maintaining long-term relationships with payors following the signing of contracts, and the volume of claims repriced has a tendency to rise in tandem with the introduction of new services and/or the accumulation of new claims.

Jun 22 presentation

Competition

Given that the industry is extremely fragmented with many other prominent players, I think it is worth discussing more about the competition.

The markets for MLTPLN are splintered because many different companies offer various options for dealing with the problem. Its size, experience, and prominence as a leading independent PPO give it a significant leg up on the competition, especially when it comes to handling out-of-network [OON] claims. Large carriers offering fully insured and self-funded plans who are searching for a turn-key solution for OON claims will find the services it provides to be beneficial because they will be able to do the following more quickly and easily thanks to its offering.

MultiPlan competes with other regionally focused independent preferred provider organization [PPO] networks and PPO network aggregators in the market for network-based services. And to the extent that it can improve its contracting, the company also competes with primary networks. First Health, Three Rivers Provider Network, and Zelis are some of its main rivals in this market. It’s worth noting that Aetna owns First Health, so the offering from MultiPlan may be more appealing to other large carriers on the lookout for an independent PPO. In addition, MultiPlan may be simpler to use than PPO aggregators because it contracts with providers directly instead of pooling together regional networks to form a national one.

MPLN competes with other analytics-based repricing service providers. Such firms comprise Zelis, AMPS, ELAP, PayerCompass, 6Degrees, and ClearHealth Strategies. Most of these focus on medicare-plus solutions, and MPLN is already incorporated into the largest healthcare providers’ systems. Cotiviti, Optum, Discovery Health Partners, HMS, and The Rawlings Group are just a few of MPLN’s competitors in the Payment Integrity Services market. In order to deal with all of their payment integrity needs, health plans frequently employ the services of several different companies. Although MPLN’s service is still in its infancy in comparison to the market as a whole, it has proven to be successful. Since MPLN’s solution also provides an advantage for processing claims on complex prospective edits, I think it could move up the stack for OON repricing. In addition, I think the health plan can benefit from increased volume to negotiate better prices.

In my opinion, MPLN faces a greater threat of losing new business from smaller health plans to competitors who may be able to offer more tailored solutions at a lower price over time. Still, I think there’s some “stickiness” among repeat customers. Plan documents, which outline MPLN’s involvement, are typically renewed once a year and require regulatory approval. Implementing a new EDI with a new third-party vendor also creates administrative work for a large carrier. These companies have expanded significantly through acquisitions over the years and use a wide variety of different legacy systems. Because of the potential difficulty and expense of adopting a new EDI system, the company risks seeing a decline in both customer savings and revenue from service fees.

Ultimately, I think MPLN has a competitive advantage due to its comprehensive claims database and single-point-of-contact service.

Near-term uncertainties

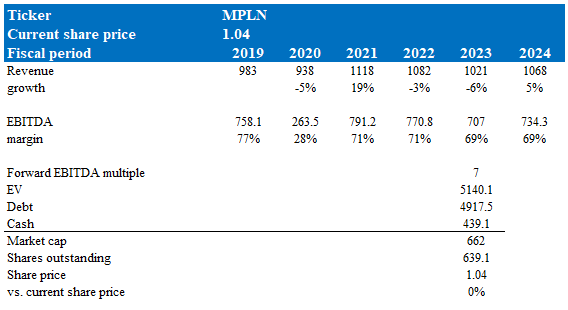

There are a lot of bad things in the most recent report for 3Q22. The company’s 3Q22 revenue and EBITDA guidance for MPLN was missed by 12% and 16%, respectively, compared to the company’s midpoint projections. In addition, the company’s outlook for FY22 and the implied guidance for 4Q22 were both lowered as a result of volume declines. Reductions in patient utilization are the primary cause of the gloomy outlook, but an unfavorable mix shift in identified potential savings is also to blame. Due to this, I anticipate a decline in the run-rate trend in the year 2023. (which management has acknowledged).

Lower EBITDA projections point to the other problem, which is margin compression that appears to be more severe than the company had anticipated. As an added complication, the outcomes of pending litigation, contract renewals, and the prevalence of repeat customers all remain unknown. The combination of these factors creates a great deal of short-term uncertainty, which may be a contributing factor to the stock market’s precipitous decline in recent weeks.

Valuation

My model suggests MPLN is worth what it is priced at today, if it trades at 7x forward EBITDA multiple in FY23.

Model walkthrough:

- Revenue to follow management full year guidance in FY23 and recovers to GDP-like levels of growth (i.e., mid-single digit)

- EBITDA margin to face a dip in FY23 as guided and remain pressured due to weaker contract unit economic s

- MPLN to trade at a forward EBITDA multiple of 7x earnings in FY23. It is unlikely to see any re-inflection in MPLN EBITDA multiple given the huge leverage sitting on the balance sheet and a very weak near-term outlook.

Own calculations

Risk

Contract renewal

As I mentioned before, it’s a mixed blessing to have long-term contracts with your most valuable customers because they may use that leverage to negotiate for lower prices. In today’s rate-hiking climate, I think this benefit is quickly becoming a drawback.

Revenue concentration risk

The concentration of customers is crucial. At the end of FY21, MPLN’s top three customers accounted for 63% of total revenue, with the largest customer contributing 34% of total revenue. The loss of even one of these clients could have a significant impact on earnings and share price.

Leverage

Since MPLN’s leverage is already quite high in comparison to its industry peers, any breach of covenant or additional indebtedness could have a negative impact on the stock price.

Conclusion

Due to the rising cost of healthcare and the subsequent emphasis on finding ways to reduce costs and improve the dependability of payments, I expect demand for MPLN to be high. That said, I’m not investing in the stock because the near-term outlook is so poor and there are no clear upsides.

Be the first to comment