VioletaStoimenova

Dear subscribers,

To say that I’ve been investing in insurance prolifically would be an understatement. Over the past few years, I’ve almost made a career out of covering quality insurance (and sometimes not so much quality). I’ve made profitable trades and investments in every insurance company I have ever invested in. This includes early ones like Prudential (PRU) and Principal (PFG), but later expanded to companies like Unum (UNM), and the European giants in the industry.

Overall, I feel like I have a decent grasp on how these companies move and what underlying trends drive their valuations. I’ve seen how, despite solid fundamentals, these companies can remain in disfavor for years, or at least 12-15 months, before slowly reversing and reaching price levels where I would say “stop”.

That’s what happened to Unum. And if you haven’t yet invested in Lincoln National (NYSE:LNC), it might be the last chance you get before it goes up above $30/share, when the next set of results come in and the upside becomes confirmed.

Lincoln National – Ripe for investing

As you know, I invest through a multitude of approaches. I use straight common share investments. I use cash-secured puts, I even use buy-write covered calls. What dictates my approach is the company’s circumstances and valuation, and how interested I am in holding the company long-term, and at what price. Usually, as long as it’s priced right, I’m interested in holding it long-term or until it goes up enough.

When it comes to Lincoln, I’ve done a bit of both. I’ve both invested in the common shares, but I’ve also, at times, done some conservative CSPs to try and get an even better price, or just take home the options premium.

I haven’t used buy-writes because the simple fact is that at this price, I believe the company is bound to rise high enough to make the strategy less appealing than other options.

My target is always at least 15% annualized, conservative RoR. This has been harder to find on the options side of things for the last 8 months. Put premiums have declined significantly, and even buy-write annualized RoRs aren’t as good as they were 3-4 months ago, on a broad basis.

The basic thesis for LNC hasn’t changed. It’s an insurance business that went through a fairly substantial re-evaluation primarily for assumptions for universal life insurance lapse assumptions, this company crashed in a manner not dissimilar to Unum and other finance companies I’ve invested in over the years. The primary difference between Unum and Lincoln was that I can honestly say that this was not something I expected out of LNC – nor did most of the analysts I follow, discuss with or collaborate with, or the industry experts I speak to.

It’s a good example that even if you believe that you own one of the safest companies and the best things since sliced bread, the market and the overall ups and downs can still surprise you, and nothing is really 100% safe. It’s a good argument for the practice of diversification, which I of course, as you might know, adhere to.

These sorts of insurance block/policy re-evaluations are a thing in insurance companies – it doesn’t matter if it’s life/health or property. I recently wrote a lengthy article about insurance companies in property pulling out of California and other states due to their re-evaluations no longer making sense in terms of selling policies there.

When it comes to insurance companies, you can bet your damndest that it’s always about the math. Insurance companies, as much as banks and often even more than banks, are unlikely to be flighty in their assumptions.

Unum is a great example of this, and one I honestly did not expect to see replicated, and worse, in another business. Yet that is what happened. It was a trip starting at below $20/share, to where it now trades at over $44/share. The difference there was that my overall initial cost basis in my personal portfolio was better – which means it took less time, about 2 years or so, for the investment to generate outsized returns

LNC is in a similar position, and part of the market clearly expects the company to not recover, or not to recover in full. I’m obviously of the stance that the company will eventually not do just that, but even come through stronger on the other side.

The company saw a 22-point RBC impact as the result of its re-evaluation, which is nothing to underestimate. However, LNC never cut its dividend, and its credit rating never dropped below BBB+.

My primary concern was that this was indicative of larger, fundamental problems in LNC’s shop where policyholder assumptions and expectations might have been not as conservative as assumed across the board – but I’ve not found this to be the case.

As a result of this, I have been very careful in adjusting my price targets for LNC – because under the Hood is still the superb insurer that we invested in a year ago. That’s why despite some analysts having PTs around $30/share or even below, my own targets stand at around twice that level – and I’ll show you just how conservatively estimated this is in the larger picture in a bit here.

The company reported 2Q23 less than a month ago. Those results came in with a net income just below $3/share, and adjusted operating income on a per share (diluted) basis of just above $2/share.

The company is shifting to a more capital-efficient mix, which it has been doing anyway, but has been accelerated as of these latest trends. 2Q23 was absolutely no worry here in any respect. Quite the opposite. The company saw solid progress, and the declines in annuities and Life insurance saw less severity. Life insurance, which is the segment taking the DAC and reserve assumption hit, is still income-positive at $33M for the quarter. A substantial majority of the company’s in-force has not been affected at all, and the average here for LNC is over $1.1T. That’s the company some are expecting to fail.

Furthermore, the group protection business saw almost a doubling of the operating income on a YoY, with improved disability and life underwriting results, with a less than 72% loss ratio compared to almost 80% YoY. This also meant an improved operating margin, up 4.5%, with insurance premiums up 6% compared to YoY.

It bears remembering that insurance companies, on the whole of it, are net beneficiaries of rising interest rates. The way that market risk benefit-related impacts and gains work means that LNC is seeing advantages here – an $1.6B gain associated with such trends in 2Q23 alone.

The big set of news to keep an eye on is the Fortitude RE transaction. The company took a $493M impact here, related to fixed-maturity securities. More complex than that of course – there’s also a $375M gain related to fixed maturity securities in an investment portfolio to be sold in conjunction with this transaction.

Pursuant to the applicable accounting guidance, the company impaired the securities in a loss position down to fair market value upon entry into the agreement in the second quarter and will recognize a gain for any securities in an unrealized gain position at the time when the transaction closes.

(Source: LNC 2Q23 Press release)

So, we can expect an unrealized gain position in the next few quarters related to this. Lincoln remains, and probably will remain a recovery play for the foreseeable future. By that, I mean that I don’t expect a massive amount of overall turnaround this or maybe even next year.

However, remember that Lincoln, like any company in headwinds, is at the mercy of market trends. This means that even if the results themselves don’t necessarily change for the better, it’s a perception that needs to change for the short-term share price to change.

I saw that with Unum. There was no groundbreaking turnaround during most of the higher climb days. It was simply the market “realizing” the cheapness of the stock.

The same thing, I believe, will happen to Lincoln National – and I have the valuation to give you a substantially positive upside here.

Let’s take a look.

Lincoln’s Upside – is still one of the 100%+ RoR stocks I invest in.

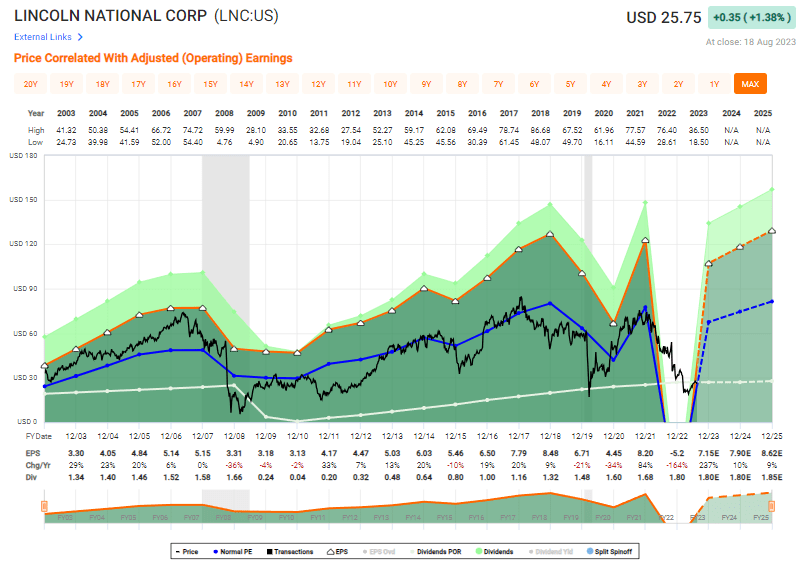

So, when I say that the company is a 100%+ RoR stock, I want to present you, to begin with, with this graph which very much illustrates the upside potential of Lincoln National in the medium to long term.

It also, perfectly, encapsulates why I have invested substantial amounts of capital in the company, averaging a current yield of above 6.7% on the entirety of my position.

LNC Upside (F.A.S.T Graphs)

I did not expect Lincoln National to “drop” this low. But nor did I expect the company’s adjusted or GAAP EPS to actually turn negative, which it has. But this also presents what could be the insurance opportunity of a lifetime.

As you can see, this company has a strong, long-term tendency to trade at around 9-10x P/E over time. While it experiences drawdowns, it usually goes up again fairly quickly – within a year or two. I expect the only reason that would not be the case would be something fundamental – and despite what we’ve seen here, I don’t view this as fundamental enough to change the company’s thesis. The market and the credit ratings are in agreement here – a small bump down to BBB+ doesn’t warrant a change here.

When it comes to what you can expect, the limit would be what you’d value the company at in terms of forward multiples. I wouldn’t expect dividend growth. Not for a very long time. But I also expect the company to continue paying its dividend. Let’s be clear. For 2023 analysts expect the company to generate $7.15 in adjusted earnings per share – that’s next to a $1.8/share dividend yield.

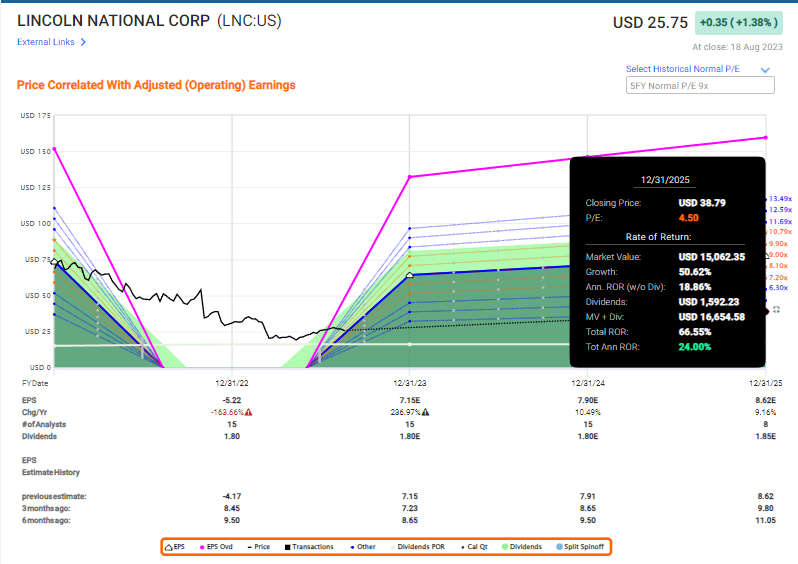

Even if you were to forecast this business on the basis of less than half of its historical P/E, at 4.5x, you’d still get this sort of upside right here.

Lincoln Upside (F.A.S.T Graphs)

That’s 24% per year based on expecting a BBB+ rated insurance business with hundreds of billions in policies, trading at a 4.5x forward P/E. Anything above that, and things get very interesting.

Full reversal to 9.8x P/E would entail 69% RoR per year, or 247% until 2025E. And I don’t see any reason why, over time, the company shouldn’t go back to such multiples.

So your upside is between 24% and 69% per year, of which almost 7% is in a dividend yield that’s covered with a less than 30% payout ratio – even on a 2023E basis.

That, dear subscribers, is why I’m so positive about Lincoln, and why I keep buying shares. Above $30/share it’ll still be good – but I can almost guarantee you’ll be kicking yourself if you think Lincoln is attractive now, but end up waiting till over $30/share before investing in the company.

So be careful – and don’t let fear rule you.

My own investing is methodical and slow, but decisive. I’ve added more and more shares to my portfolio, and Lincoln is currently 3.7% of my commercial portfolio.

I view it as a “BUY” with the following, positive thesis.

Thesis

-

Lincoln National has taken a harsh hit in terms of valuation after issues with its GUL/VUL block assumptions, resulting in an RBC hit that has temporarily pushed it below 400%. However, I expect the company to be able to be to push this above 400% in 2023-2024E, and through a combined block sale/transaction and improved business returns, recover its valuation and trajectory.

-

This makes LNC, even on a conservative basis, a potential investment that could return over 100% even on a 5-6x P/E in the next few years. That is why I continue to invest here, lowering my cost basis in my personal portfolio, and establishing a very already-profitable position in my corporate investment portfolio.

-

I view LNC as a “BUY” – and my PT is at least $55/share. This price target remains at this particular time.

Remember, I’m all about:

-

Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

-

This company is overall qualitative.

-

This company is fundamentally safe/conservative & well-run.

-

This company pays a well-covered dividend.

-

This company is currently cheap.

-

This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

LNC still fulfills all of my fundamental criteria for investment.

Questions? Let me know!

Be the first to comment