Drazen Zigic/iStock via Getty Images

The highly anticipated Consumer Price Index report is becoming a market fixation. Speculators could use the CPI rising by 6.4% before seasonal adjustment, higher than the consensus increase of 6.2%, as an excuse to sell. Optimistic investors might point to the Federal Reserve’s reaction to the report as a reason to keep buying stocks.

The Fed’s rate policy decisions using CPI as one data point drives the market, not the CPI report alone.

Instead of getting caught up to the market’s fall, rise, and fall again within the first two hours after the market opened, what does the CPI really say?

Disinflation is Slower Inflation

Fed Chair Jerome Powell stressed “disinflation” at the Fed meeting. Disinflation means enduring higher prices for a longer period. The higher cost of shelter is by far the largest contributor to the monthly all items increase, according to the BLS. The report added that shelter accounted for almost half of the monthly all items increase. Food, gasoline, and natural gas also added to inflation in January.

Investors should brace for higher gas costs for two reasons. First, the Russian/Ukraine war is out of the Fed’s control. Russia will cut oil output next month by 500,000 barrels a day. The 5% reduction in world production will pressure Brent prices. Consider setting $100 per barrel as a target price for crude this year.

Second, China’s reopening is widely anticipated to cause an increase in demand for energy. The caveat is that after three years of a brutal lockdown, the Chinese consumer is not rushing to spend more on goods. Small business owners have high debt or are bankrupt. This will limit the China catalyst in the energy sector.

Despite the government’s scrutiny of oil companies buying back shares, investors should watch Exxon Mobil (XOM), ConocoPhillips (COP), and Chevron (CVX).

ConocoPhillips has a mixed quant score. Its valuation improved after the company posted earnings of $2.71 a share. In addition, it will pay a variable return of cash of 60 cents a share on April 14, 2023.

COP Stock (Seeking Alpha Premium)

Exxon stock has nearly identical quant scores as that of COP stock. It scores a D on growth. However, shareholder returns are rising after Exxon announced an up to $35 billion stock buyback in 2023-2024.

BP p.l.c. (BP) is now a consideration after it pulled back from green commitments. BP stock gained nearly 20% after the strategic change. The company realizes that after the war started last year, a fossil fuel alternative is years, if not decades, away.

Chevron bucked the energy rally trend when it missed Q4 expectations. The firm is forecasting a production increase of up to 3% at $80 per barrel Brent.

Price Decreases

The BLS report highlighted a decline in used cars and trucks, medical care, and airline fares. Investors do not have a clear buy or sell signal in those sectors. In the airline sector, United Airlines (UAL) already rallied after posting revenue rising by 51.4% Y/Y to $12.4 billion.

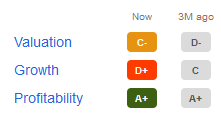

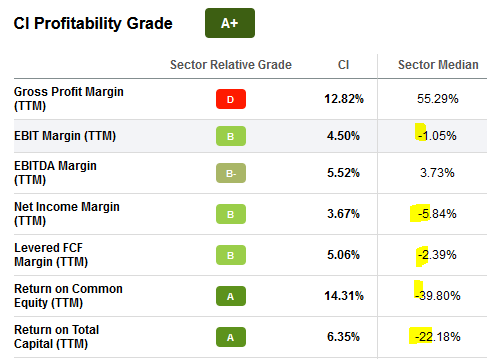

In the medical care segment, companies like Cigna (CI) and UnitedHealth Group (UNH) peaked in Dec. 2022. Markets are concerned about the Centers for Medicare & Medicaid Services (“CMS”) of Medicare Advantage (“MA”) payment rates for 2024. Investors are overly worried about the small price increase.

Plan providers will raise their premiums and deductible and provide less coverage to offset the lower reimbursement rates. Companies like Cigna will sustain profit margins while the sector operates in negative territory:

Seeking Alpha Premium

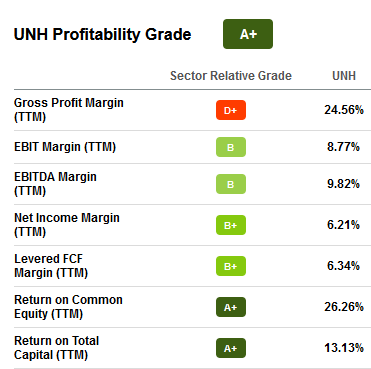

UnitedHealth has similar grades:

UNH Grade (Seeking Alpha Premium)

Investors should anticipate lower medical care costs lifting the profitability of the above-mentioned firms.

Automotive Sector Mixed

Magna International’s (MGA) weak Q4/2022 earnings miss is another example of company-specific fundamentals mattering more than the CPI report. The stock lost 15% in value after posting profits falling from $1.54 a share last year to 33 cents a share. Magna is Fisker’s (FSR) electric vehicle builder.

In the used automobile market, CarMax (KMX) stock has recovered since posting weak results.

The diverging stock action of those firms is disconnected from January’s CPI report for now. In the long term, disinflation and elevated interest rates will continue. This keeps auto financing rates at high levels. As long as that happens, people will delay buying new or used vehicles.

The Bottom Line

Markets acted like economists by pointing to the hot job market, the Fed’s small 25 bps rate hike, and this CPI report to arrive at today’s equity valuation. Bullish, long-term investors are accumulating stocks, believing the S&P 500 (NYSEARCA:SPY) forward price-to-earnings ratio of 20.43 is a bargain. They believe the multiple will fall if earnings improve. However, earnings might rise on job cuts (especially in the tech sector) but revenue could fall.

Bears keep pointing to an S&P 500 Index (SP500) target of 3,400 to 3,800. By waiting for the Oct. 2022 low of 3,500 to return, they missed the rally to 4,089.

The “cash gang” will earn at least 4.26% from money funds. Those investing a minimum of $1 million will earn 4.41%. This rate could rise to around 5.0% when the Fed raises rates again in 2023.

Among all the sectors, energy looks the most promising. Demand is rising and supply is falling. The high energy cost will show up in future CPI reports. Energy investors will benefit the most from this demand/supply dynamic.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment