It’s time to talk about one of my favorite companies for the next economic upswing: the Arconic Corporation (NYSE:ARNC). On June 1, I wrote an article titled: Despite Headwinds, Arconic Is too Cheap.

In this article, I am going to update my bull case and focus on the last sentence of my June article:

For now, the biggest problem is demand uncertainty as economic growth indicators in major economic areas are weakening. In other words, do not expect a sudden and steep uptrend but use weakness to accumulate shares if this stock fits your trading strategy.

While input costs have come down crashing, which was the company’s biggest issue earlier this year, it is now suffering from slowing demand expectations, which are making it unlikely that the company will reach its full-year targets.

However, as we will discuss in this article, investors are pricing in too much weakness. That’s usually the case when panic selling hits the market. The company has a fantastic balance sheet, the ability to generate a lot of free cash flow, and a valuation that will make the ARNC ticker one of the winners of the next economic upswing.

Now, let’s look at the details!

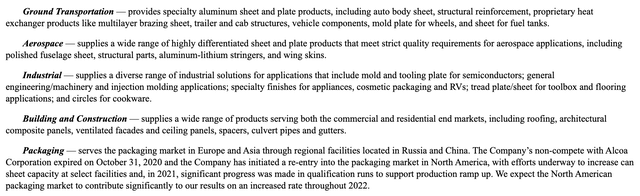

What’s Arconic?

Arconic is a company that is flying under the radar, and that’s not just because of its $2.0 billion market cap. I would argue that the vast majority of traders are not aware of this company. As I discussed in my last article, the company is the result of two spin-offs since 2016:

Arconic used to be part of the mighty aluminum producer Alcoa (AA) until Alcoa was spun off in 2016 to create a business focused on aluminum metals and engineering and an industry focused on aluminum and alumina production. The goal was to create shareholder value as businesses like Arconic have higher valuation multiples compared to basic material companies – in general.

Then, on February 8, 2019, Arconic announced that it would split into two separate businesses (again). Arconic would be renamed Howmet Aerospace Inc. (HWM) and a new company, Arconic Corporation, would be set up and spun out tax-free from Arconic. The new Arconic Corporation is focused on rolled aluminum products and Howmet Aerospace on engineered products. The separation was completed effective April 1, 2020.

Basically, rolled products are used in the production of finished goods ranging from automotive body panels and airframes to industrial plates and brazing sheets. Sheet and plates are used extensively in the transportation industries as well as in building and construction and packaging. They are also used for industrial applications such as tooling plates for the production of plastic products.

The company sells its products to 5 industries:

Arconic Corp.

From Supply To Demand Headwinds

Because the company does not have its own raw material production facilities, it is dependent on suppliers. The company mainly buys primary aluminum for remelting, aluminum alloys, aluminum scrap, and alloying materials, including magnesium, copper, and zinc. In addition to that, it buys natural gas, oils, packaging materials, and pretty much everything it needs to produce finished products.

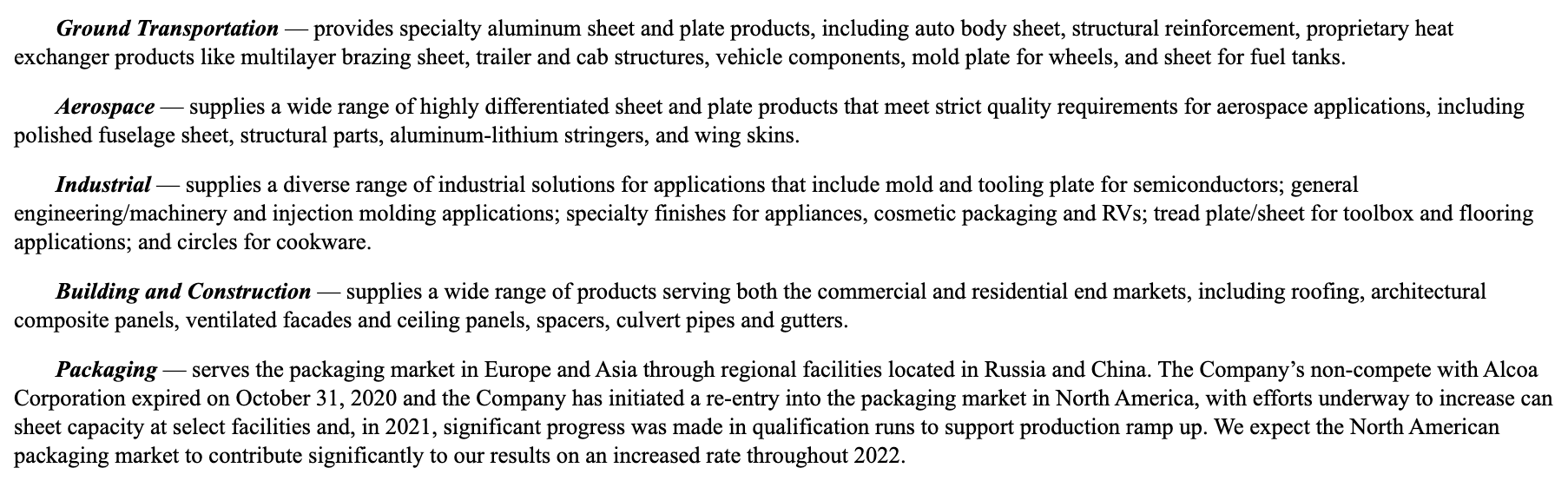

In 2021, and earlier this year, the company suffered from high material prices and supply chain issues – demand was quite good. In 1Q22, the company paid 65% more for aluminum as Midwest aluminum was trading north of $4,400 per ton.

Currently, COMEX aluminum futures are trading 40% below their 2022 highs.

TradingView (COMEX Aluminum)

The problem is that this downtrend is caused by demand fears, which are also pressuring the ARNC stock price.

In the second quarter, the ARNC attempted an uptrend, adding roughly 30% to its market cap when aluminum prices started to come down. But then again, demand fears started to do a number on the company, and the market in general.

As I wrote in a recent market outlook article, the Fed is eager to pressure inflation. That makes sense. However, it is risking financial instability and related economic weakness.

The worst part is that the economy needs to get worse before markets can expect the Fed to refrain from hiking any further.

However, we’re not out of the woods yet. Economic conditions need to become much worse for the Fed to pivot. That could end up pushing stocks lower than current levels again before we get dovish comments.

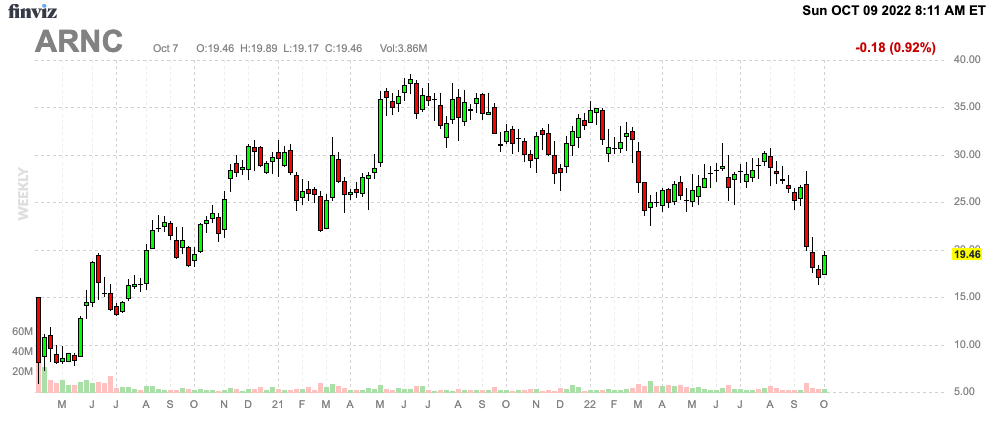

Hence, ARNC shares are now down 41% year to date. Hence, it is confirming the worries I had in June. In 2Q22, the company still saw high demand:

Demand across our end markets remained strong, and our operations generated $162 million in cash in the quarter, which will be fundamental to growing — as growing free cash flow is supporting high-return organic investments and substantial returns to our shareholders.

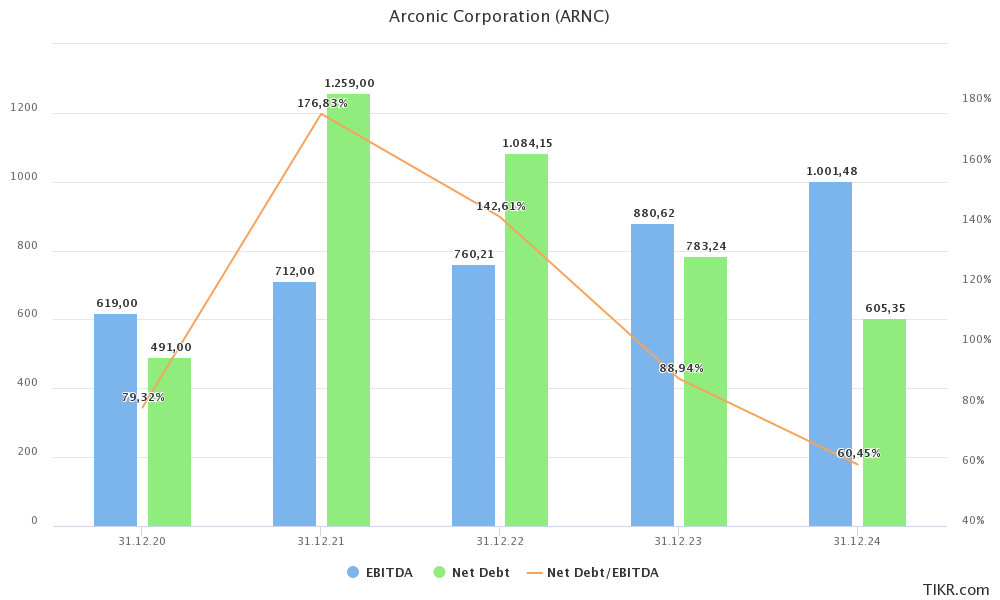

Unfortunately, that has now changed. Due to the high demand, ARNC expected positive organic revenue growth in every single segment. On a full-year basis, it expected adjusted EBITDA to come in between $820 million and $870 million, which would imply between 15% and 22% growth versus 2021. While doing so, the company expected $300 million in free cash flow.

If we look at current estimates, we see that analysts have made significant adjustments that are well below the company’s own guidance. Bear in mind that the guidance is a few months old. ARNC will (almost certainly) present its own update in a few weeks. What we are looking at now is $260 million in expected 2022 free cash flow and $760 million in EBITDA. That’s still an improvement versus 2021.

TIKR

The good news is that $260 million in free cash flow still implies a 12.5% free cash flow yield, using the aforementioned $2.0 billion market cap.

It’s Not *That* Bad

It is so important to mention that the company itself is not in bad shape. Yes, demand will come down. The market is pricing that in. However, ARNC is still in a good spot.

In September, Fitch affirmed Arconic’s BB+ credit rating. However, it boosted the outlook to “positive”.

The rating upgrade matters because it’s based on a lot of things that will benefit ARNC and its shareholders in the future. The company is seeing an improved financial situation, including lower pension liabilities. Pension contributions and other post-employment benefit payments are expected to decline to around $50 million per year.

Ignoring pensions, net debt is set to fall to less than 1x EBITDA in 2023. Even if EBITDA remains subdued, the company is in an incredible position to deal with financial and macroeconomic risks. The company’s borrowing conditions reflect this. The company’s ABL Credit Agreement is based on SOFR (this replaces LIBOR-based floating rates) plus a credit spread adjustment equal to 0.10% to 0.25% per year, depending on the borrowing duration.

TIKR

Moreover, ARNC is set to benefit from a longer-term recovery in aerospace. Even though demand is being pressured, the post-pandemic recovery is a much-needed tailwind.

Although aerospace accounted for just 11% of organic revenue in 2Q22, organic revenue growth was 50%, and I expect much more growth as major manufacturers and tier 1 suppliers start refilling their inventories after the first wave of new demand since the pandemic.

Moreover, with regard to a recession, Fitch highlights an extremely important point. Most of its supplies come from the US, which is much better positioned than i.e., Europe, which is now seeing a steep decline in metal production as I discussed in this article (among many others). Moreover, its diversification and specialization in secular growth markets are helping:

[…] Fitch believes ARNC would remain somewhat resilient during a potential recessionary environment due in part to its advantaged access to commodity supply with the majority of facilities located in the U.S. The company would also benefit from its relatively diversified end markets, as they have a wide array of products across industries that are shifting toward lighter-weight materials, which ARNC specializes in.

Despite recession fears, aerospace will see outperforming growth over the next five years as airline customers are ramping up demand. Especially as long-haul demand comes back, delivery rates will boost.

The same goes for packaging:

Meanwhile, packaging has several positive tailwinds that should support substantial growth beginning in 2022, including the ramp-up of ARNC’s U.S. facility following a non-compete agreement roll-off with Alcoa, in addition to broader market pressures to shift to more environmentally friendly products such as aluminum.

So, what does this mean in terms of valuation?

Valuation

Bear markets aren’t a lot of fun – for most people. However, bear markets come with opportunities. Just like bull markets result in a lot of stocks reaching valuations that are way too high, bear markets often see valuations that are too low.

Despite the decline in EBITDA estimates, ARNC is now trading at 4.3x 2023E EBITDA of $880 million. That’s based on a $3.8 billion enterprise value consisting of its $2.0 billion market cap, $780 million in 2023E net debt, and $1.0 billion in pension-related liabilities.

In June, the company was trading at 5.2x EBITDA, which was already way too low.

ARNC is now trading like a steel company in times of subdued economic growth.

Back then, I made the case that the fair value was roughly $40 to $45 per share, which is slightly above the $40 valuation JPMorgan gave the company in December of 2021.

FINVIZ

That said, the problem is getting there. I do not expect ARNC to start a rally right away toward my target. The economy remains in trouble as the Fed isn’t willing to pivot yet. Even if the Fed pivot, we will likely see a new wave of inflation. The good news is that ARNC is protected against that. It has a lot of pricing power, secular tailwinds, and a strong supplier base in North America.

This sets the company apart from its competitors overseas. It also means I expect ARNC to gain market share going forward. I hope the company comments on that in its next earnings call.

The best way to play ARNC for people interested in undervalued cyclical stocks is to start a small position and add on dips.

Takeaway

The market is in turmoil. This is offering new opportunities. In this article, we discussed Arconic. This company suffered from high input costs in 2021 and early 2022. Now, it is suffering from lower demand expectations as most of its end markets are set to feel pressure from a weakening economy and aggressive Fed.

This toxic mix has pushed ARNC down more than 40% since the start of the year.

The good news is that the company is in great shape. It has a stellar balance sheet, secular tailwinds in aerospace, packaging, and transportation industries, and a valuation that makes it likely that ARNC will double in the next 12-24 months.

However, please be careful. The bottom may not be in. Start with a small position if ARNC is right for you, and take it from there.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment