Avtor/iStock via Getty Images

The stock price for Whole Earth Brands (NASDAQ:FREE) has been in a free fall since March 2022. The company specializes in branded consumer packaged goods, private label and ingredients. The company has recently reported strong financial performance in the third quarter of 2021, with consolidated constant currency revenue growth of 8.1% and adjusted EBITDA of $21.5 million.

The stock price has been declining due to the impact of inflation on cost. However, the demand has been resilient as revenues have been growing each quarter.

Seeking Alpha

The company’s diversification in terms of its channel presence, product assortment, and geographical reach is a strength that continues to drive results. In North America, 80% of revenue is generated within unmeasured channels such as club, e-commerce, food service, private label and ingredients, which continue to see nice growth during the third quarter and are expected to remain a significant force for future growth.

The company’s international Branded CPG businesses also grew revenue 8% in the third quarter on a constant currency basis, with both volume and price contributing as the company continues to grow share in its international markets. The company’s private label and ingredients business complements the branded portfolio nicely through stronger and broader customer relationships and purchasing scale.

FREE’s core strategy is to help consumers achieve healthier lifestyles positions it well for success in the current environment, with approximately 3 in 4 consumers aiming to limit or avoid refined sugar and a powerful movement towards wellness and personal health. The company’s portfolio of brands is well suited to address a variety of consumer needs, with premium and baking-oriented brands such as Wholesome, Swerve and Whole Earth in the U.S. being optimal solutions for at-home indulgence and healthier life science, and mainstream brands such as Canderel and Equal presenting a strong value proposition, delivering affordability without sacrificing quality.

Innovation is a core capability of the company, and it currently represents 17.5% of its North American Branded CPG sales and 12% of its global Branded CPG sales over the last three-year period. The company’s new innovations are tapping into high-growth segments of sugar substitutes with Monk Fruit, which is seeing consumption growth of 42%, and Allulose, which is growing at nearly 14% versus a year ago for the 13-week period ended October 1.

The company is also focusing on expanding distribution across its global footprint. In North America, through its ongoing focus on improving production rates and service levels, the company is seeing distribution wins adding doors across its core brands driven by increasing momentum with national and regional customers. Additionally, its emerging international markets such as Asia Pacific, in the Middle East and Africa, and Latin America, which represents 15% of its Branded CPG segment, once again, collectively posted a strong double-digit growth during the third quarter, confirming the strong secular demand trends for its products.

The company has also recently taken control of a facility that manufactures sachet and bags in Decatur, Alabama, which will help stabilize operations and improve the company’s supply chain.

Valuation

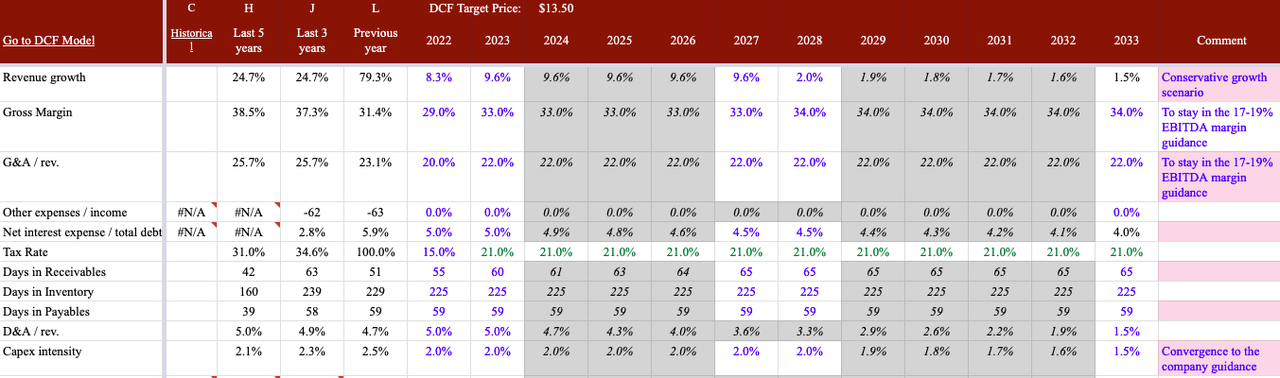

Even taking into account the positive trends in the company and industry as mentioned in the previous section, I decreased my fair share valuation from $18 per share to $13.50 per share. That is due to two reasons.

First, while FREE could pass a portion of inflation to consumers via pricing, I believe FREE would have to absorb a portion of the cost inflation by reducing gross margin, my expectation is that the long term gross margin of FREE decreased 250-400 bps.

Secondly, the rate hikes have increased the risk free rate substantially, so the cost of capital has increased as well impacting the price.

Author estimates

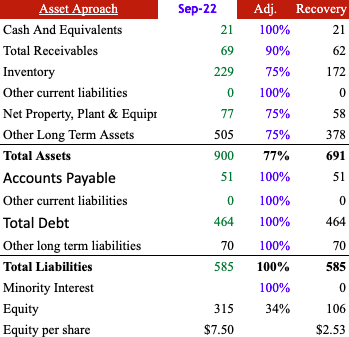

On the risk side, I see the recovery value for FREE shareholders in a bankruptcy scenario around $2.50 per share which is 33% of the book value and a 35% decline from the current share price.

Author estimates

Conclusion

Overall, Whole Earth Brands is a company that is well positioned for growth in the current environment, with a diverse assortment of strong brands, a focus on profitable growth and cash flow, a mission to help consumers achieve healthier lifestyles, and a commitment to innovation and distribution expansion. As such, it can be seen as a positive investment opportunity for those interested in the CPG industry.

Investing in FREE’s shares at the current price offer an asymmetric risk-reward opportunity of 3.5x upside and a 35% loss.

Be the first to comment