An Opinion Piece By Todd Rich, Head of Education, Nadex.

With all of the drama and news lately around short-sellers, it’s important to understand how necessary and important they are to the US financial markets. Without short-sellers, our equities markets would collapse, and in fact without short-sellers the foundation of the free market capitalist system in the United States would likely cease to exist. No, that is not hyperbole. Anyone who tells you short-sellers should be banned needs some perspective regarding how our markets work.

You’re probably asking yourself, “How can this possibly be?” Short answer: short-sellers provide absolutely necessary liquidity to the secondary markets; without secondary markets (stock exchanges), the primary markets (private equity) wouldn’t exist; and without the primary markets (which are the cornerstone of the capital formation process which fuels our entire economic system), US capitalism would come to a halt.

The Role of Short-Sellers

To understand this, let’s start at the beginning and work our way through the process in order to understand why short-sellers are so vital to our economy.

First, why does Wall Street even exist in the first place. When someone has an idea to start a company (or a company wants to grow their existing enterprise), they’re going to need capital. Whether starting or growing, companies need money to hire employees, have some basic equipment, and maybe rent an office to start the operation. So, how does a company get that money? There are two ways to fund a business. The company can either borrow money and take on debt, or the company can offer equity (namely shares of stock) in exchange for seed capital.

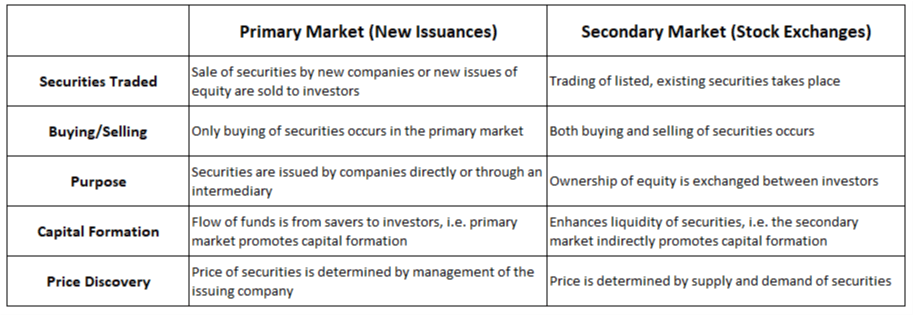

Where do people typically go to either borrow money or issue initial equity? Wall Street. This is the main and primary function of Wall Street: to bring together people who need money with other people who have excess capital and are willing to invest it. This is called capital formation. These private equity markets, where companies find seed money, are considered the primary markets – it’s the first place people go.

Overview of Primary & Secondary Markets

{kind=link}

Learn more about markets from DailyFX education.

Next, let’s think about people who give money to a company in exchange for some initial equity. At some point they are going to want to monetize (or make a profit) from their initial investment. Their expectations are that they would be able to sell their equity at a later date. The question becomes who can they sell that stock to? In the private equity markets, the way initial investors typically get their money back is when the company eventually goes through an initial public offering (IPO) on an exchange. When companies list their stock on a public exchange (like the Nasdaq or New York Stock Exchange), this is the secondary market. The secondary market is where most of us have the opportunity to participate in equity ownership of companies and to try to build wealth.

If the secondary markets didn’t exist, people would likely never take equity in a private company in a private equity transaction (in the primary market) as there would be no effective mechanism for them to ever exit their position to free up that money for a new investment. Private equity would become like a roach motel, you could check in at any time you like, but you could never leave. So, the secondary markets where stocks trade on a public exchange are where retail traders access the markets. And the secondary markets are necessary so people who invest privately in start-up companies (in the primary market) have an avenue to exit their investments. It is through this process that companies can run operations, grow their business, start new businesses – all the things necessary to have a thriving economy and provide everyone for an opportunity for gainful employment.

This brings us to the inter-workings of the secondary markets. When you want to buy or sell stock on an exchange, you see a quote that consists of a bid and an ask. The bid is the price at which you can sell, the ask is the price at which you can buy. Rarely (if ever) is there a naturally occurring, tight, liquid market. Would you want to trade a stock if the quote you saw was a bid-ask spread of $5 – $105? Retail traders prefer to see bid-ask spreads that are narrow (like $68.25 – $68.30). It gives you confidence to know you’re getting a fair price at that moment in time since you can see the highest price someone is willing to pay paired with the lowest price someone is willing to sell.

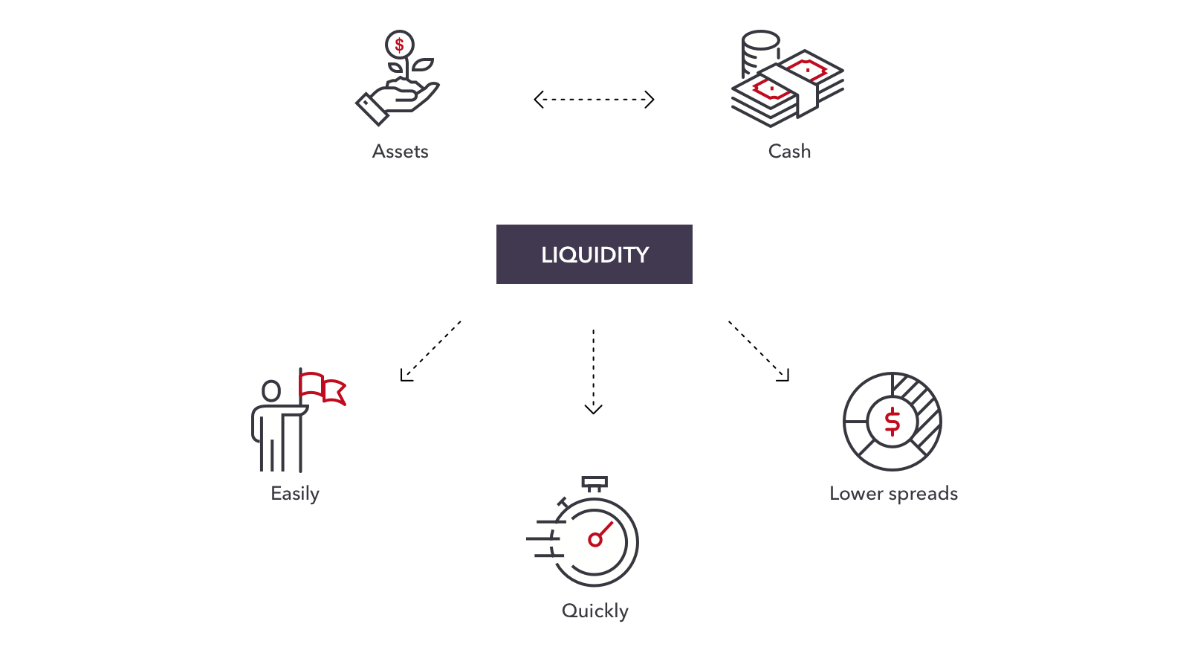

Benefits of Liquidity

Liquidity chart, courtesy of IG.

With tight, liquid markets (narrow bid-ask spreads), if you accidentally bought a stock, you know the price in which you could immediately sell it to get rid of it. Try doing that when you buy a car after you drive off the lot. Or better yet, bring your used meat back to the grocery store and see if they’ll buy it from you. That’s not going to happen. The beauty of the secondary markets is the fact that you can see the bid-ask spread before you conduct a transaction. That is called liquidity, which is what we’ll discuss next.

Most exchanges have open, central limit order books, meaning anyone can post a bid or an offer. However, it is not always the case that the natural bid-ask spread is narrow, and more often than not buyers and sellers don’t show up to execute a trade at the exact same time. As such, there are market makers and other liquidity providers that will step in and either buy or sell with whomever is looking to conduct a trade. They’ll typically trade with anyone whether they’re looking to buy or sell.

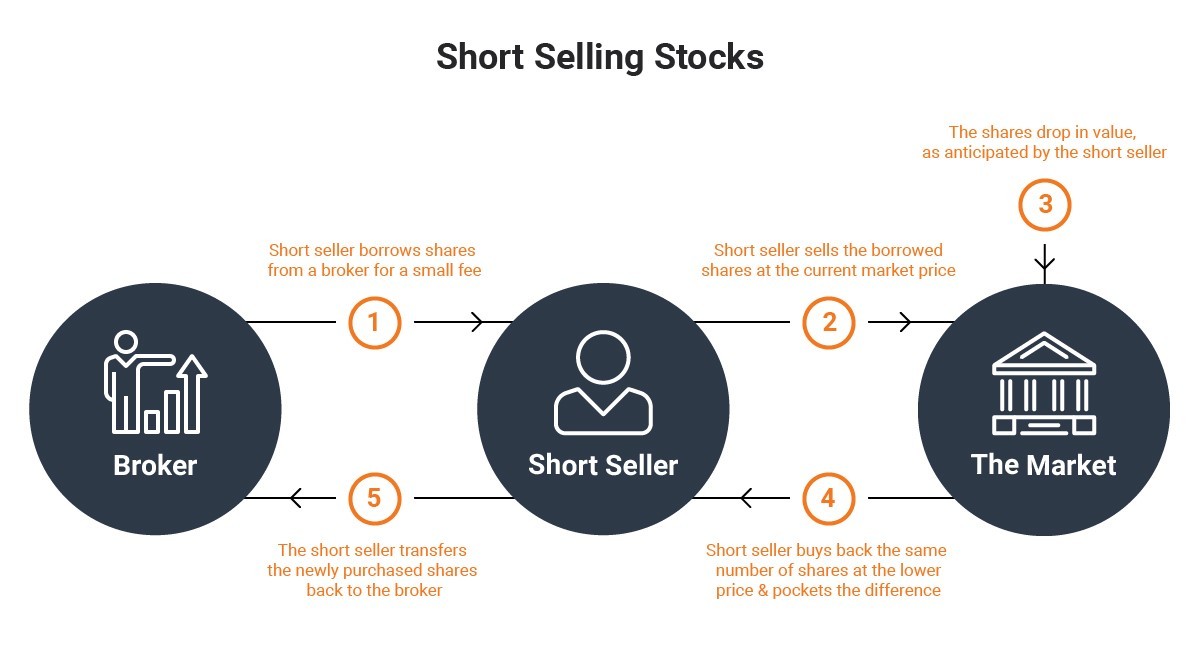

When you want to buy a stock, a liquidity provider is there to sell you that stock. They will then buy that stock from someone else at a later date (or time). Sometimes those liquidity providers have to sell short (meaning they don’t currently have the stock in their inventory to sell to you). Otherwise you wouldn’t be able to buy the stock. Without these liquidity providers, and without their ability to sell short, you would have to wait until someone who does own the stock shows up and is willing to sell it to you.

Chart courtesy of DailyFX. Learn more about short selling here.

Let’s think about that for a second. If you had to wait to only buy stock from someone else that owns it, you could sit around for days, months, or even years before someone was willing to do so. There are large institutional investors in the markets (like pension funds), as well as retail investors with retirements accounts, that hold assets for years if not decades. If they never wanted to sell their stock, no one else would ever be able to buy it.

Without short-sellers willing to step in and sell to someone who was looking to buy, the secondary markets would freeze up. If the secondary markets freeze up and become illiquid, then the primary markets would in turn also freeze up. Remember, it’s unlikely anyone would participate in the primary markets (private equity) if they didn’t eventually have access to the secondary markets. And the secondary markets absolutely need short-sellers in order to provide the liquidity everyone needs to keep the markets functioning.

As a side note, without short-sellers, the options markets (which are currently trading at all time high volumes) would also lose their liquidity. Options markets need market makers to post liquidity across all stocks for puts & calls across numerous strikes and numerous expirations. Whenever an options market maker buys a call or sells a put, they may need to hedge that transaction by selling stock (and it’s unnecessary to go into an entire diatribe about hedge ratios, delta, and gamma, but suffice it to say there is applied calculus happening here). Many retail traders are accessing the equities markets using options, and options markets could not exist if market makers did not have the ability to sell stock short.

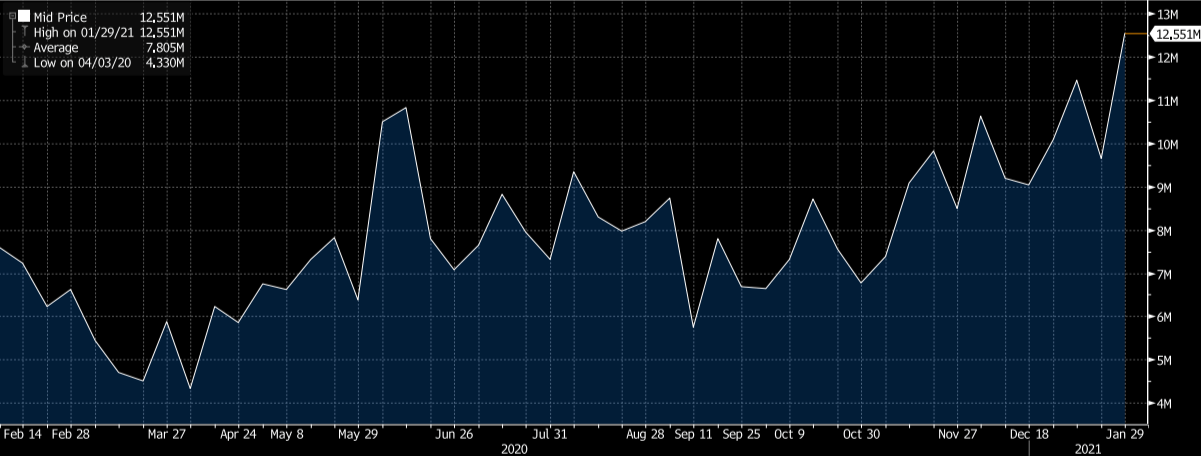

Retail Options Frenzy (CBOE US Weekly Equity Call Volume)

Chart courtesy of Bloomberg

This brings up an interesting concept. Since there are different reasons for market participants to be physically short stock, it does NOT mean those participants are necessarily taking a bearish position on the company. An options market maker is a perfect example of that. While traders may take a bearish position in options, the options market maker will naturally have the opposite, namely a bullish position in the options. To hedge that they would be short stock. The options market maker’s net position might be neutral (even though they might be physically short stock). This was most certainly the case in notable instances like GameStop (GME) and AMC Theatres (AMC). On the flip side, there are traders that are bearish and do indeed sell stock short strictly looking for the opportunity to profit if the stock goes lower. Those sellers are most certainly providing liquidity to people who want to buy the stock. And those short-sellers are taking risk, to be sure.

In the end, short-sellers are a necessary ingredient to the US economy. Our economy is made up of a multitude of companies and businesses across a multitude of industries. All of us have an opportunity to work for these companies to earn a living. We need businesses to offer employment opportunities and to drive economic growth. All of these companies need access to investment capital at some point, whether it’s during their start-up phase or a growth phase. A key component to that investment capital is private equity (the primary markets). Private equity then sells their stock on the secondary market where most of us can then participate in equity ownership and invest in these companies. And the secondary market simply could not function efficiently without liquidity providers having the ability to be short-sellers when needed. So, when you hear about the evil of short-sellers, realize that without them the capitalist financial system in the US would falter as it would have ripple effects all the way to the necessary capital formation process we all need to keep our economy moving.

Want to learn more? Check out DailyFX for details on the short selling process.

Be the first to comment