Orbon Alija/E+ via Getty Images

Introduction

Whitehaven Coal [WHC.AX] (OTCPK:WHITF) is a Sydney, Australia-based thermal and met coal mining company founded in 1999. It specializes in very high-quality, high-value coal with primary exposure to the Newcastle coal price and seaborne coal trade. Japan makes up ~50% of the company’s sales destinations and Southeast Asia (S. Korea, Taiwan, India) makes up more than 40% of the rest.

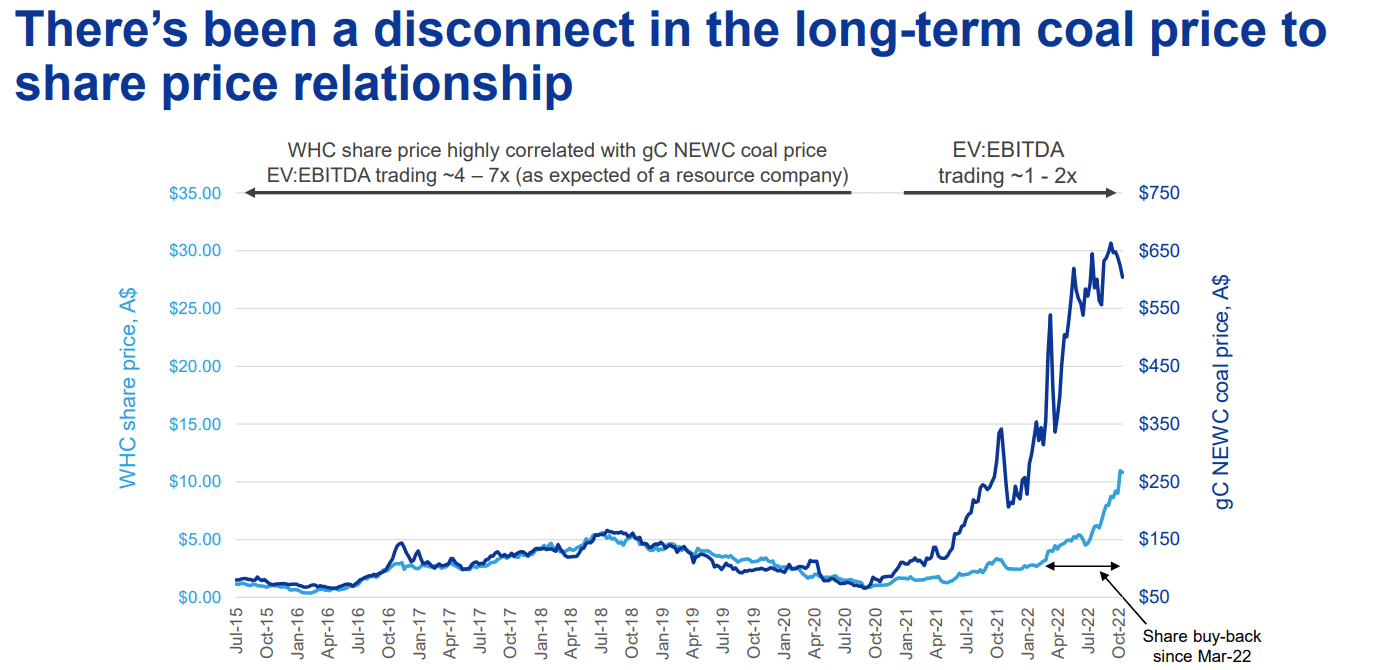

Since the summer of 2021, factors including global energy shortages, ESG policies, and the conflict in Ukraine with Russia have sent Newcastle coal prices skyrocketing. Prices have risen from around $80 to a current price as of writing of ~$375 (chart below), more than a 4x increase, which means lots of cash for producers.

And while Whitehaven has had stellar returns the past couple years, including being the #1 performer on the ASX in FY22, the stock has actually not kept pace with its underlying commodity. Perhaps due to institutional constraints on coal ownership, as well as concerns over geopolitical events, Whitehaven’s valuation has actually fallen significantly, currently trading around 2x EV/EBITDA.

Company presentation 10/26/2022

Efficient market theorists may believe this discount is warranted and WHC could be a value trap in its final death throes, but the evidence doesn’t all seem to point that way.

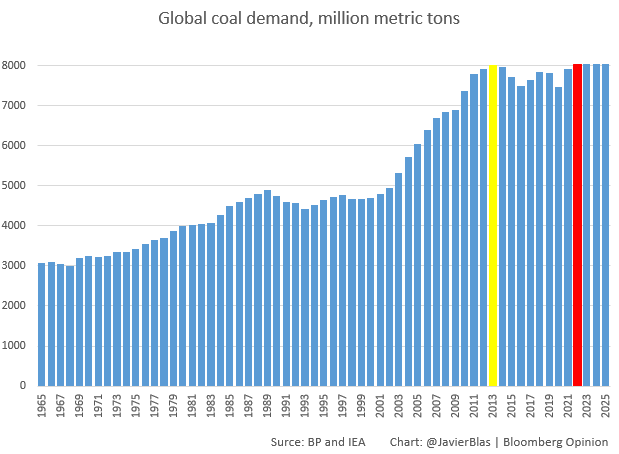

Coal Demand Is In Fact Not Declining

Though some conventional wisdom may say coal is in terminal decline, and we are nearly done with it, this perspective could be seen as Western-centric, and global statistics tell a different story. Coal use will reach a record high this year. China, India, and other parts of SE Asia are still building coal plants. And just last week, the IEA revised its global coal demand forecasts upward, predicting global coal use will not decline but plateau or even continue growing through 2025.

Javier Blas from Bloomberg showed it excellently in this chart:

Twitter, BP, IEA, https://twitter.com/JavierBlas/status/1603783086914797568?s=20&t=NUwDgH7WEaPWYd_XiFxkEQ

You can also note from this chart and international energy organizations that we as a species have never significantly reduced coal usage for any extended period of time. Throughout history, we largely add-on new sources of energy as we develop them (nuclear, gas, wind, & solar) rather than replacing old ones.

Supply is Being Constrained

Even with demand remaining elevated, governments globally are mandating steps toward a green transition, announcing “windfall” taxes and royalties on fossil-fuel companies, and banks are increasingly wary to lend to them. The natural result is that coal operators are being highly disincentivized to invest in new supply.

Even at such eye-watering coal prices, huge players like Glencore (OTCPK:GLCNF) are abandoning assets or seeing their projects being blocked. Two weeks ago, BHP (BHP) announced it had set aside $750m for potential early closures of coal mines in Queensland and “will not make any new investments” there while windfall royalty taxes remain.

As a result, overall supply trends are bearish. While operators under less scrutiny like China can and likely will ramp up their coal production, some of the world’s biggest projects from the biggest mining companies are being curtailed. And with valuations for good assets like WHC sitting under 2x EV/EBITDA, the market is telling coal operators to act like they are in rapid decline and not invest in new growth.

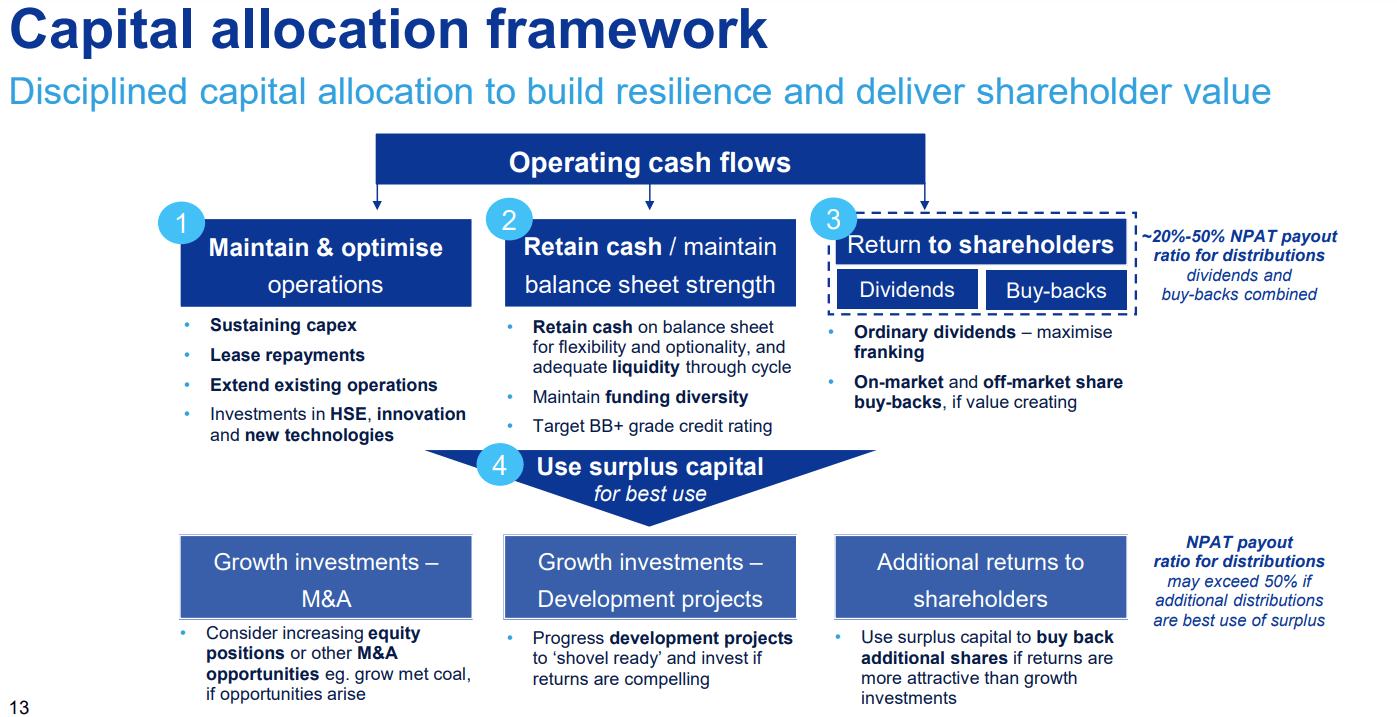

WHC Using Smart Capital Allocation, Buying Back 25% of Shares

When an industry is in decline or is not anticipated to need new supply, the correct capital allocation strategy is to maintain efficiency and necessary operations while returning cash to shareholders.

This is what Whitehaven has done and pledged to continue doing.

At the company’s AGM the end of October, it announced it would be buying back 240 million shares, or 25% of the company’s issued capital, over the next 12 months, and will continue to allocate capital in a manner consistent with a declining industry.

Company Presentation

From the company’s filings, it has been buying back shares lately at roughly 10% of daily volume.

With such a low valuation and continued support from the company’s buyback program, buybacks are an extremely efficient use of capital and are consistently rewarding shareholders. As the table below shows, Whitehaven has significantly outperformed the S&P 500 over the past week, month, year, and even 3-year period.

SeekingAlpha

With such strong fundamentals, the company’s earnings power by increasing by 33% (1/0.75 of new shares = 1.33), and the further capital allocation to shareholders, I believe the stock will continue its excellent run.

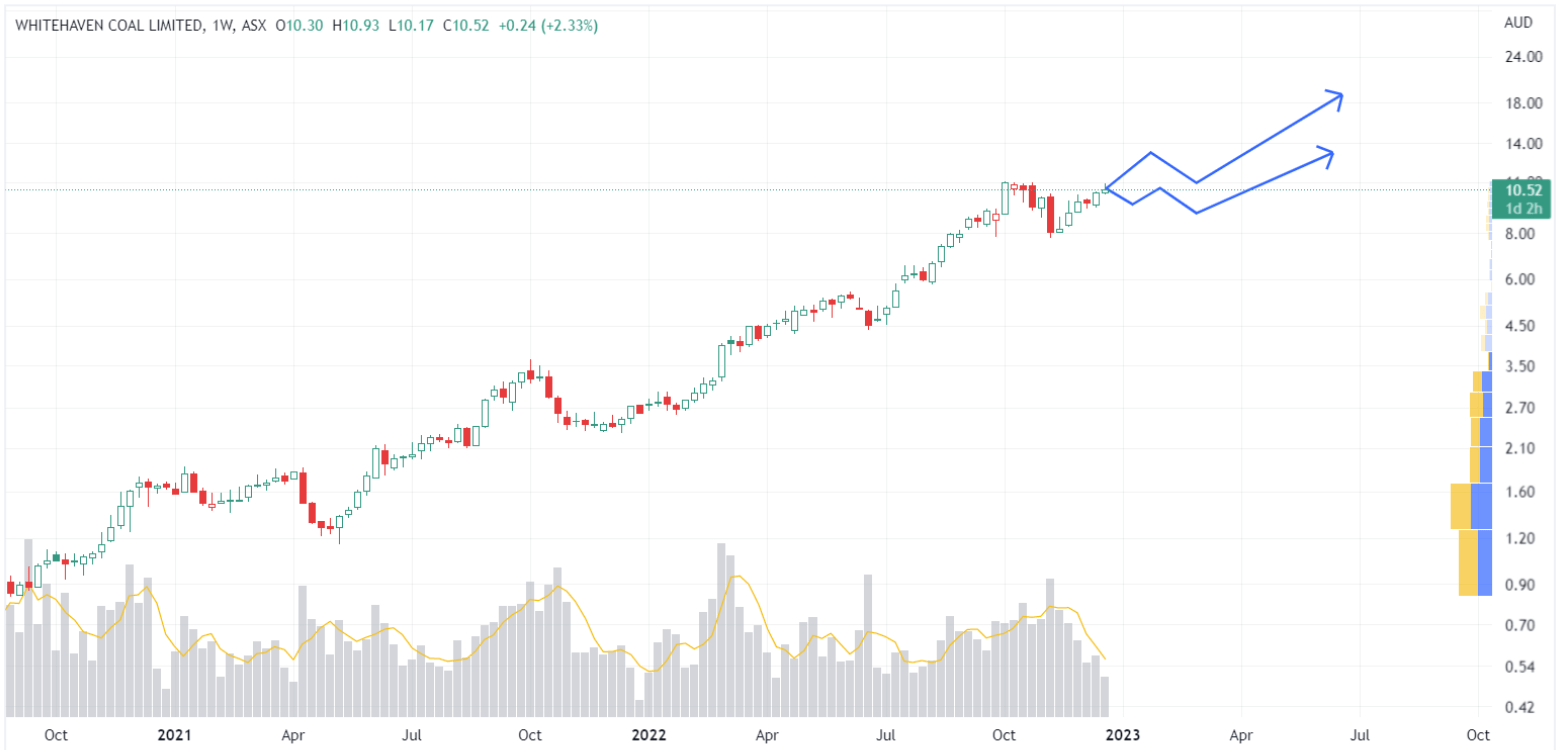

Technical Analysis:

While funds I manage hold a significant position in WHC, it is currently sitting at resistance from the last couple months, which can make buying here risky. Though of course anything can happen in financial markets, I show two possible projections below.

For those without a position, I might recommend buying half here and another half on a breakout and retest or a successful dip lower, as shown by two possible paths outlined below. There is usually a “shoulder season” around February/March as winter ends and coal prices decline. This could provide a good buying opportunity.

Author’s Analysis

In a bullish / aggressive scenario, I believe Whitehaven can get to ~$18-19 AUD by next summer, an ~80% increase from current levels. In a more conservative scenario, I think the equity could rise by 30-40% by next summer.

Though these targets may seem aggressive, Whitehaven’s recent performance, fundamentals, and buyback make me think they are very possible.

Biggest Risk is Ukraine/Russia resolution

While Whitehaven’s extremely reasonable low valuation and constrained global supply provide a margin of safety, the biggest risk I can see occurring to the stock is significant progression toward a resolution in Ukraine/Russia. Russia was a large supplier of high-value coal, and news of the conflict winding down could send WHC down something like 10-15% overnight and perhaps 25%-35% over a matter of a few days.

Without a doubt, Russian volumes would put a significant dent in the Newcastle price and bring down Whitehaven’s future earnings power. However, given the factors discussed above, I believe the global supply situation will remain tight and Whitehaven could recover or even still have some upside left.

Closing

Even though WHC has had an amazing run over the last couple of years, I still believe there is plenty of upside and outperformance left in the name. I currently hold a sizable position and may hopefully trade into more if it plays out according to my technical analysis.

I believe investors also need to keep position-sizing appropriate, as significant risk remains in the event of a resolution in Ukraine/Russia.

Not every investment is appropriate for everyone. Please do what is right for you.

Thank you for reading and for your time. If you enjoyed this, please like, and if you would like to share your thoughts, please do comment below.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment