Justin Sullivan/Getty Images News

Nvidia has been a great American Growth Story

Nvidia (NASDAQ:NVDA) has taken the chip market by storm, becoming the maker of choice by many gamers and artificial intelligence applications. Nvidia is a leader in end-user GPUs and graphics cards used not only for gaming, but also for deep learning artificial intelligence applications. Having been involved in a startup using AI to decipher blueprints, I can say that all the graphics cards we were using were Nvidia and our programmers swore by their technology. For older Millenials that have been out of the gaming scene for a while, new graphics cards are not cards at all. The new graphics card market are products akin to a computer inserted into your computer, roughly the size of a VHS cassette with its own internal cooling system.

Nvidia A 100 (Wccftech store)

The growth of Nvidia

The company’s CAGR in earnings per share the past five years was an astounding 25% per annum, growing from an EPS of $1.27 to $3.91 from 2018 to FY 2022. This is certainly a company that would fit into my growth stock bucket, and my go-to method to come up with price targets on growth stocks is to reference my favorite Peter Lynch book, One Up on Wall Street.

The book has several amazing sections on how to use the PEG ratio and what is the max upper limit we should use when calculating the G (growth) of a company. After going through this exercise, my rating on Nvidia is a hold as I await a reasonable price, but would not liquidate my shares at the current SP either.

How the PEG ratio works

The PEG ratio was not invented by Peter Lynch, but he was the most successful individual to implement it. For those unfamiliar with Lynch, he ran Fidelity’s Magellan Fund, and between 1977 and 1990 the fund averaged over a 29% annual return, making Magellan the best performing mutual fund in the world. The ratio equation is quite simple, find the trailing 3-5 years compound annual growth rate in earnings per share, drop the percent sign and then divide the current P/E ratio by that number. When the ratio is 1 or sub-1, then you’ve found a bargain.

In general, a p/e ratio that’s half the growth rate is very positive, and one that’s twice the growth rate is very negative. Lynch, Peter. One Up On Wall Street. 1989 (199)

Referencing this quote, let’s see how Nvidia stacks up to this ratio.

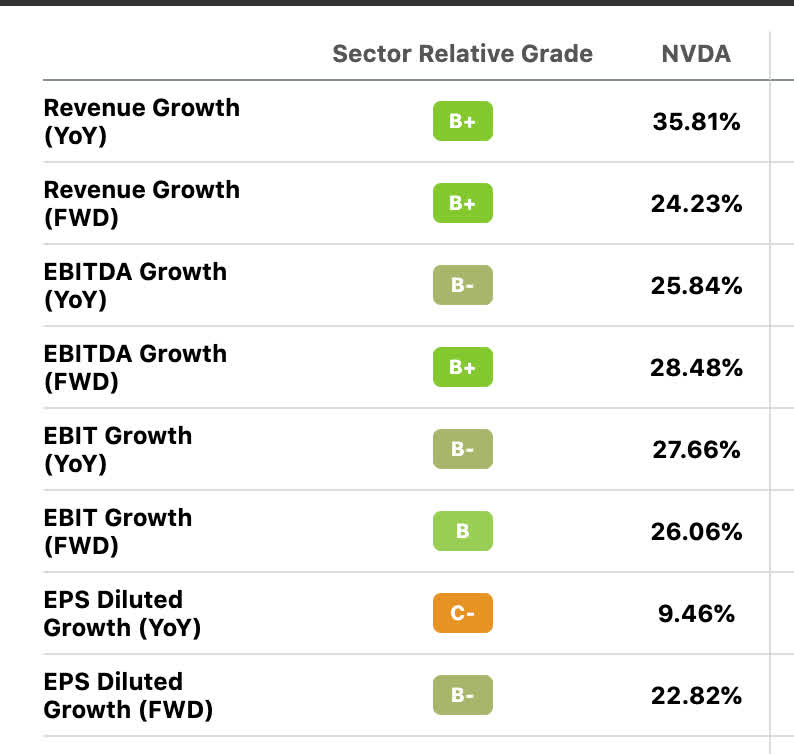

Nvidia financials (Seeking Alpha)

As we can see from the above financial metrics, the YOY growth in EPS has slowed to 9.46% versus its trailing 5-year EPS CAGR of 25%. The Magellan fund successfully hunted for stocks with earnings CAGR ranges of 20-25%, avoiding those exceeding this growth rate as it typically ended up being unsustainable in the long run.

In this price target evaluation, I am going to give Nvidia the benefit of the doubt that they will restart their growth engine in the future and get back to 20-25% earnings growth. Most individuals have probably seen PEG ratios on the company below 1 for most of this year in several screeners. This is a misuse in my opinion of the PEG ratio by analysts creating wild forward projections in earnings growth as their denominator, giving Nvidia a sub-1 ratio. In these situations, Peter Lynch advises against chasing hot CAGR assumptions regarding stocks he labels as “fast growers”:

What has the growth rate in earnings been in recent years? (My favorites are those in the 20 to 25 percent range. I’m wary of companies that seem to be growing faster than 25 percent. Those 50 percenters usually are found in hot industries, and you know what that means.) Lynch, Peter. One Up On Wall Street. 1989 (229)

If investors are referring to Peter Lynch when using the PEG ratio, this is not the way he traditionally implemented it (using forward estimates). It was always an evaluation of trailing growth divided by the current p/e ratio, not the forward growth assumptions divided by the current p/e ratio. This was especially true for Nvidia earlier in the year, when analysts were predicting forward earnings growth above 50%.

So what multiple should we use?

A simple price target multiple we can use when trying to evaluate a stock according to the PEG ratio would be to determine a suitable CAGR of earnings, in this case, the trailing 5 years, drop the percent sign and multiply that number by the current TTM EPS. The current TTM EPS for Nvidia sits at $3.73 a share. Because I like Nvidia, I’m going to use the trailing 5-year multiple of 25 versus the forward diluted estimate of 22. Lynch also advises adding the dividend to the multiple as an additional kicker. As of today, Nvidia has a dividend yield of .11%, so my final multiple I will use is 25.11, a very liberal one if I may say so.

The next part of the exercise is easy, take the growth multiple of 25.11 times the current earnings per share of $3.73, and we can see at what point Nvidia would hit a PEG ratio of one. 25.11 x $3.73 = $93.66. Let’s do the inverse of this for accuracy, $93.66/$3.73= PE ratio of 25.11, 25.11/25.11= PEG ratio of 1. With a current stock price of $134, a price target of $93.66 would represent another 30% discount from this point before the stock is a good value according to this metric.

Let’s take a look at the balance sheet

Nvidia debt position (yahoo finance)

Nvidia’s debt position (Yahoo Finance)

Nvidia‘s current cash position sits at $17.04 Billion, total debt sits at a bit over $11 Billion with a debt to equity ratio of 49%. The current ratio is 3.62 x, so there is no leverage risk here. Rolling into 2022, we can see that the total shares outstanding have increased to 2.5 Billion shares from 2.48 a year ago, a slight increase.

Total debt has grown 51.68% YOY, indicating a defensive position to cover its working capital in anticipation of possible lean years ahead. While Peter Lynch likes to see cash positions increasing while debt is reduced to indicate future prosperity, this situation indicates an increase in both cash and debt. Preservation and possible preparation for R&D and/or an acquisition could be the answer to this balance sheet scenario.

How could they fall that far?

NVDA vs Its Peers (Seeking Alpha)

Let’s keep in mind that the stock is already down a lot. The stock hit an all-time high of $333.59 on November 29th, 2021, at $134, it’s currently 59% off its all-time high. The chip industry trades at an average price-to-earnings multiple of 17.6, thus even at a p/e of 25 x, it would still be the highest valued company in the sector.

We can see above how NVDA has performed this year versus its peers, namely Intel (INTC), AMD (AMD), and Micron (MU). Nvidia has held up fairly well against its peers being that Nvidia was the most expensive stock in the group to start the year, Intel with a much lower valuation at 7.8 x earnings has still performed worse than Nvidia with a plunge of 43%. This shows me that even though Nvidia is in repricing mode, it still has support and a community behind it, something Intel sorely needs.

Headwinds abound

Recent revelations about Nvidia being blocked by the US government from selling A100 and H100 chip sets to China used in AI facial recognition are not good news for the bottom line. This one potential hit to revenue of $400 million is not the end of the world, but it could just be the opening of Pandora’s box when you produce something used in digital facial recognition that could be applied for nefarious purposes.

Nvidia has a net profit margin of 36.23%, so for every billion dollars in revenue limited by government controls, you can expect a hit to earnings of about $360 million. Although Nvidia hasn’t been selling to Russia since the Ukraine war broke out, Alibaba (BABA), Tencent (OTCPK:TCEHY), and Baidu (BIDU) are all large customers that use similar AI deep learning chips sourced from Nvidia. While those companies are not technically state-owned enterprises of the CCP, the US government may determine otherwise.

Government regulations will most likely tighten or loosen depending on how aggressive Beijing and Moscow become. We could imagine that the Defense Department might offer Nvidia further contracts and incentives to help replace some of the lost revenue, protecting one of its greatest national assets. The list of possible avenues for government contracts on Nvidia‘s government project web link includes projects for DARPA and the US Department of Energy. The Energy contracts could be particularly fruitful, as Nvidia has described this opportunity as a one to help solve problems dealing with electric grid efficiency and alternative energy solutions.

Fabless Pros and Cons

Another factor to weigh for Nvidia is their fabless business model, where they don’t produce chips, but simply design them and have them produced by companies like Taiwan Semiconductor (TSM). Intel is a major player in building fabs stateside, and Nvidia has expressed interest in moving some of their chipset manufacturing to Intel in the future. In light of Beijing’s stance on Taiwan, this could work out very well if Intel can execute on achieving 3 nm chips by 2025 to be competitive with what Nvidia will need. While many still doubt Intel’s ability to pull off such a feat, let’s not forget that Intel has also spent enormous amounts on R&D over the past two years, ranking 8th in the world. A reliable Fab in the US is in my opinion the key to protecting and even growing Nvidia‘s profit margin, as being fabless reduces overall overhead and operating costs.

Growth Opportunities

One of my favorite growth opportunities I can see on the horizon for Nvidia would be in the metaverse, with a recently planned collaboration with Meta Platforms (META). In my opinion, re-focusing on US-based AI gaming applications rather than politically charged international markets would be a smart move to avoid regulatory risks. According to a member of Meta’s AI development team, once fully deployed, Meta’s RSC is expected to be the largest customer for installation of Nvidia DGX A100 systems.

We hope RSC will help us build entirely new AI systems that can, for example, power real-time voice translations to large groups of people, each speaking a different language, so they could seamlessly collaborate on a research project or play an AR game together.

Another lesson from One Up on Wall Street

The semiconductor industry is a cyclical one, rising and falling with the economy. Peter Lynch also points out in his book that the cyclicals are usually the first ones to recover once the economy turns around, as we are just entering a global recession, accumulating cyclical stocks at favorable prices is a good way to prepare for the economic turnaround. This is one of my favorite stocks to watch at the moment. I reiterate a hold rating and will be accumulating below $100 with a price target of $93.66 where I would start placing outsized bets.

Be the first to comment