niphon/iStock via Getty Images

We’ve recently addressed the high-yield sector’s strong credit fundamentals and historically attractive valuations. We’ve also shown that yield to worst has been a reliable indicator of return over the next five years. Now, we’re turning the spotlight on yet another interesting development in the high-yield market: an inverted yield curve.

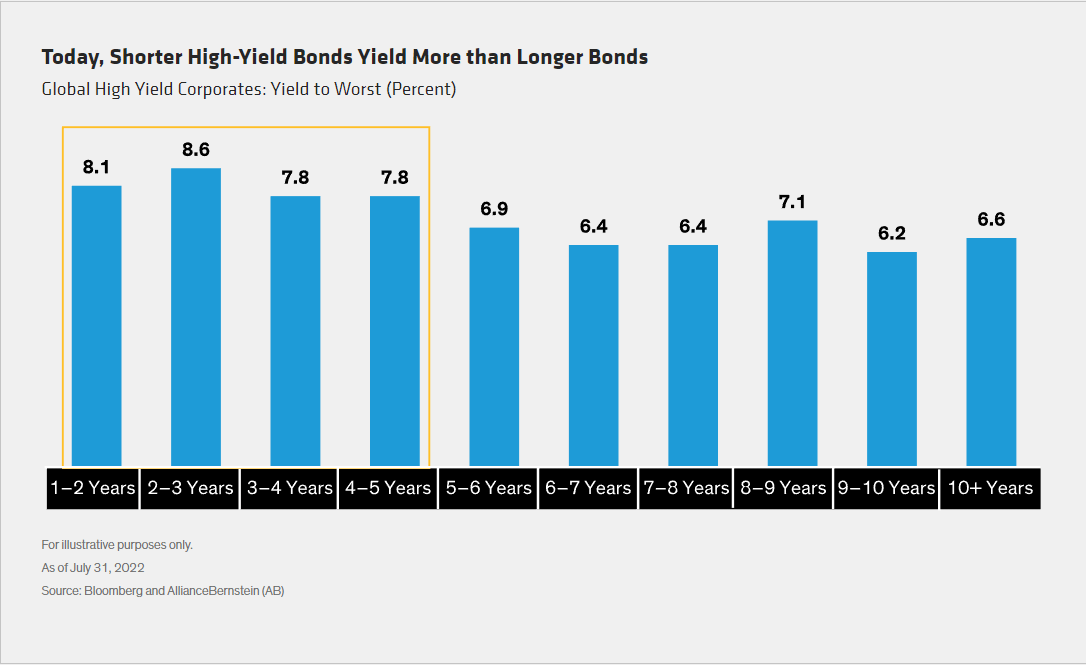

It makes sense that longer-maturity bonds typically provide higher yields than shorter-term bonds. After all, more bad things can happen in a longer period than a shorter one, and visibility is poorer for the next 10 years than for tomorrow. Investors expect to be paid for these risks.

But in an unusual aberration, short-term high-yield debt is currently yielding significantly more than longer-term debt (Display, above). An inverted high-yield curve is great news for high-yield bond investors who are concerned about near-term market volatility.

Even in normal times, a shorter-duration high-yield strategy can provide high levels of income with lower volatility than an intermediate-duration strategy. Historically, a shorter high-yield approach has provided about 85% of the income of a longer-maturity mandate, with about half the average monthly drawdowns.

But with the high-yield curve inverted, as it is today, investors are being paid more to take less risk. We think that’s an income opportunity worth sizing up.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment