venuestock/iStock via Getty Images

Today, I’d like to introduce a new candidate for my value portfolio, one in which I’ve taken a starter position, but for which I am still hoping for a bit of a pull back to acquire a full position. Encore Wire (NASDAQ:WIRE) is a long standing Texas based company specializing in the production of electrical wires and cables, typically made from copper and aluminum.

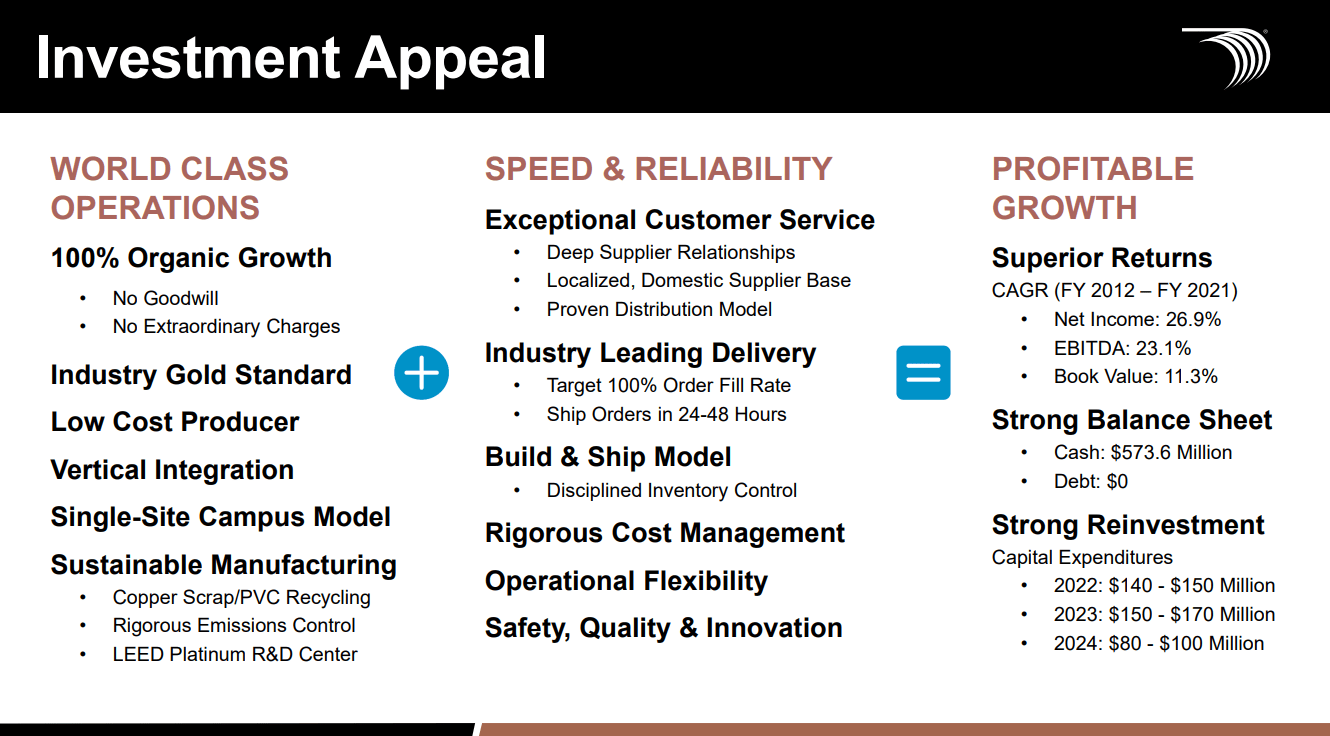

This slide from the most recent corporate presentation sums up the perceived strengths of the company. Of particular note are the vertical integration, long standing customer and supplier relationships, fast order fulfillment and operational flexibility.

Corporate presentation

Financial Performance

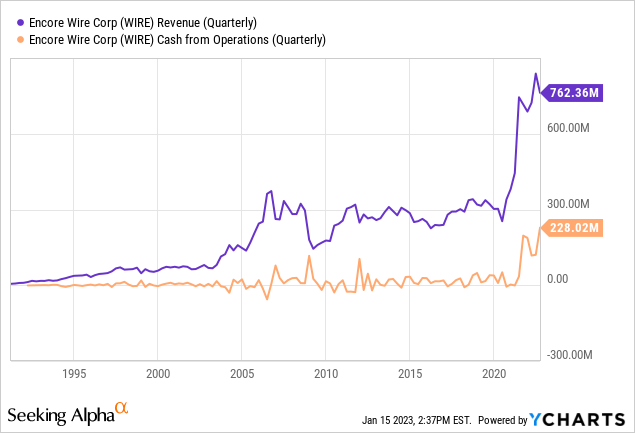

As can be seen from the quarterly revenue and cash flows from operations graph, the company has recently enjoyed a big jump in both measures due to increased demand during the Covid pandemic economy. A key question is whether it can sustain these operating levels or whether the unusual supply chain issues and the demand from home building and renovations during the work from home period are one-time events.

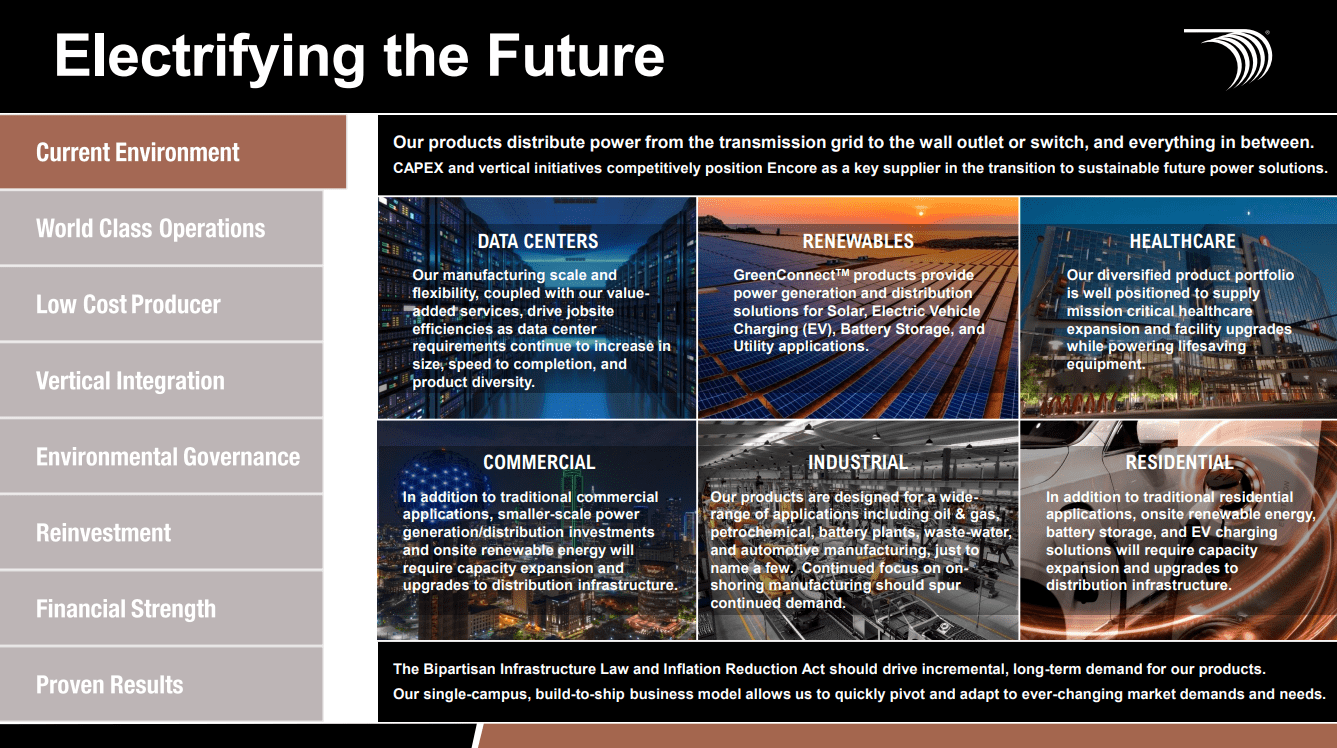

Personally I’m betting that there may be some regression, but that due to the wide variety of markets that WIRE operates in, revenues and cash flows will land somewhere between the 2019 numbers and the 2022 peak values. This slide does a nice job of showing WIRE’s market diversification, with renewables and data centers likely to be growth centers going forward (with no dependence on a pandemic).

Corporate presentation

Moreover, on the most recent earnings call, the company had positive things to say regarding the outlook for all of these markets. Perhaps the one on most analysts’ and investors’ minds is the residential market. Here’s an excerpt with the company’s take on this (my emphasis):

If you look in the third quarter, residential was 28.3% in the third quarter of ’22. If you compare it to the third quarter of ’21, it was 28.7%. So it’s pretty comparable…

There still seems to be somewhat of a backlog on some of the other materials — building materials it takes to finish some of the houses, creating a little bit of a backlog there, maybe in the supply chain side. But overall, we’re still receiving pretty consistent demand and request for quotes for the residential piece.

Moreover, there’s an important difference in the company now vs historically as it comes to reliance on the residential market:

But again, as we’ve tried to communicate and highlight even in the press release and on our website, we’re not tied to the residential starts number as folks have tried to portray us in the recent past. That production capacity that’s in that residential plant, which is the original plant going back to day one, it will be used in other products that go out of here that are considered to be commercial and industrial related.

Finally, here’s WIRE’s take on their markets as a whole:

[T]here’s clearly a healthy demand for the entire product line. It moves up and down slightly. And then right when you think it’s a little slower, it picks up, and we’ve got a strong industrial segment. The commercial segment has been strong. As Bret mentioned, the aluminum demand has been strong and not to take anything away from the copper side. There’s pockets that we have some pricing challenges from competitors on the larger size, copper cables, the basic stuff that’s pretty easy to run through equipment, which really doesn’t surprise me.

Valuation

Having addressed the question of whether recent results are sustainable (I think there will be a bit of a regression, but not back to 2019 levels) we can now look at valuation metrics.

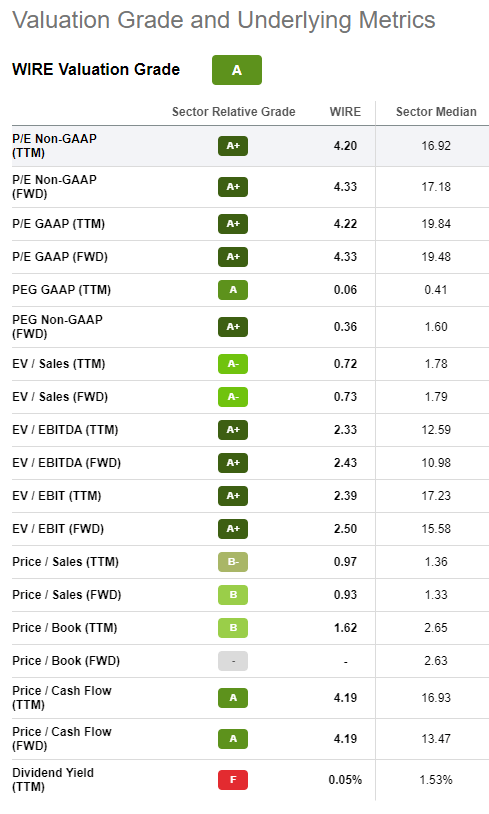

Here’s Seeking Alpha’s summary of this data.

Seeking Alpha

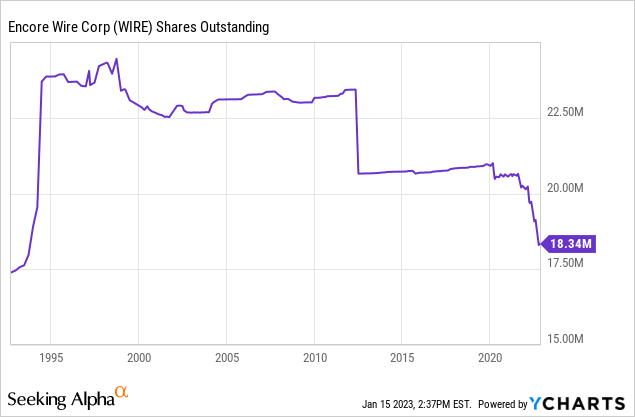

These are stellar metrics, both on a trailing twelve month basis and on forward projections. In particular the P/E and P/EBITDA ratios are exemplary. The only red mark is on dividend yield, and that’s because the company has been returning money to shareholders via share buybacks rather than dividends. The chart below shows how the number of shares outstanding has decreased markedly due to these buybacks.

Cash on Hand

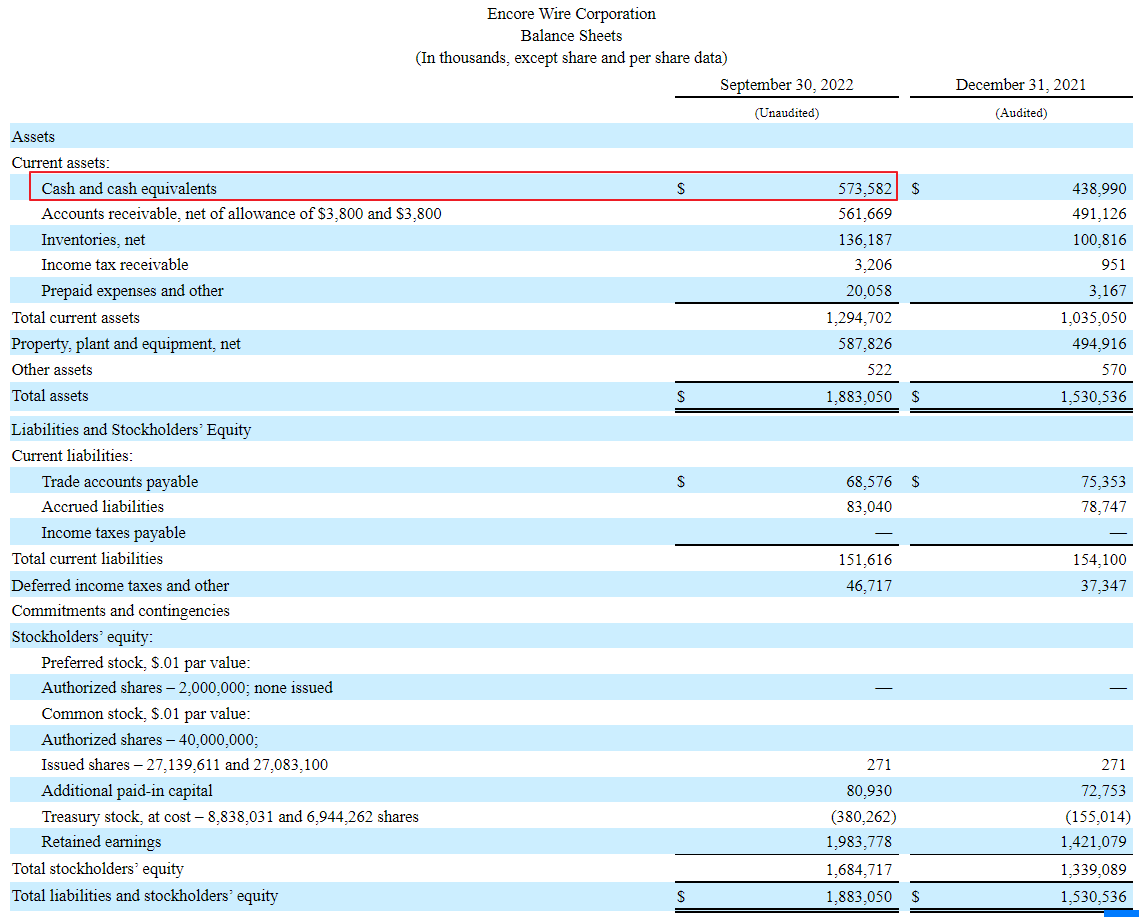

Another metric that’s important to me is cash on hand as it enables operational flexibility and reduces the risk of dilutive financings. Here’s WIRE’s balance sheet from its most recent 10Q:

sec

The company has $573M in cash and cash equivalents on hand. With 18.34M shares outstanding that’s $31 per share or about 21% of the share price with the stock trading at $149.31. In my book, that’s a very healthy cash position that can be used for expansion and/or share buybacks.

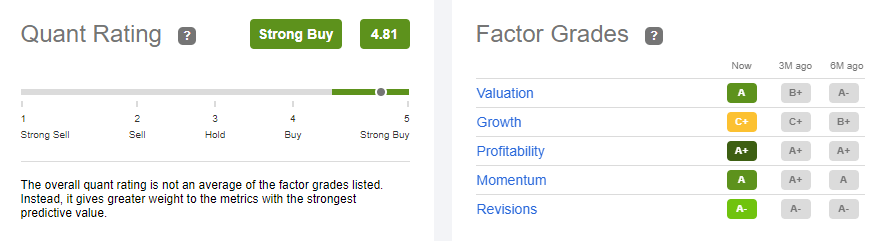

Quant Ratings

Seeking Alpha currently rates WIRE a “strong buy” with an overall quant rating of 4.81. The only blemish in the factor grades is for the growth category, which makes sense since the company saw an anomalous spike during the Covid work from home period. I agree with this assessment and it’s part of the reason I’ve taken a starter position in the stock.

Seeking Alpha

Options

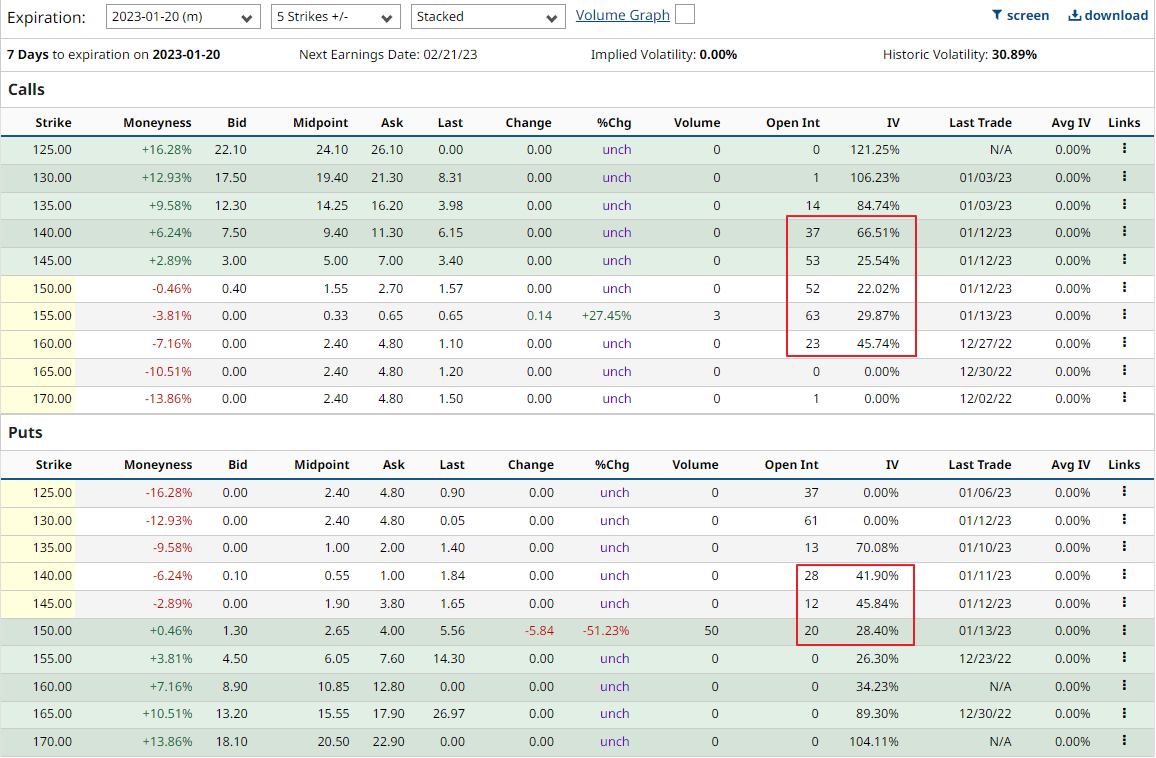

WIRE trades options, but they are relatively illiquid (see open interest), and feature a relatively low implied volatility. Thus it won’t be easy to use them for writing puts or covered calls.

barchart

Risks

The biggest risk for WIRE is that its financial performance declines to levels seen prior to the pandemic and that the stock therefore also trades back at 2019 levels. As I’ve argued above, I don’t think that will happen but it’s definitely a real risk.

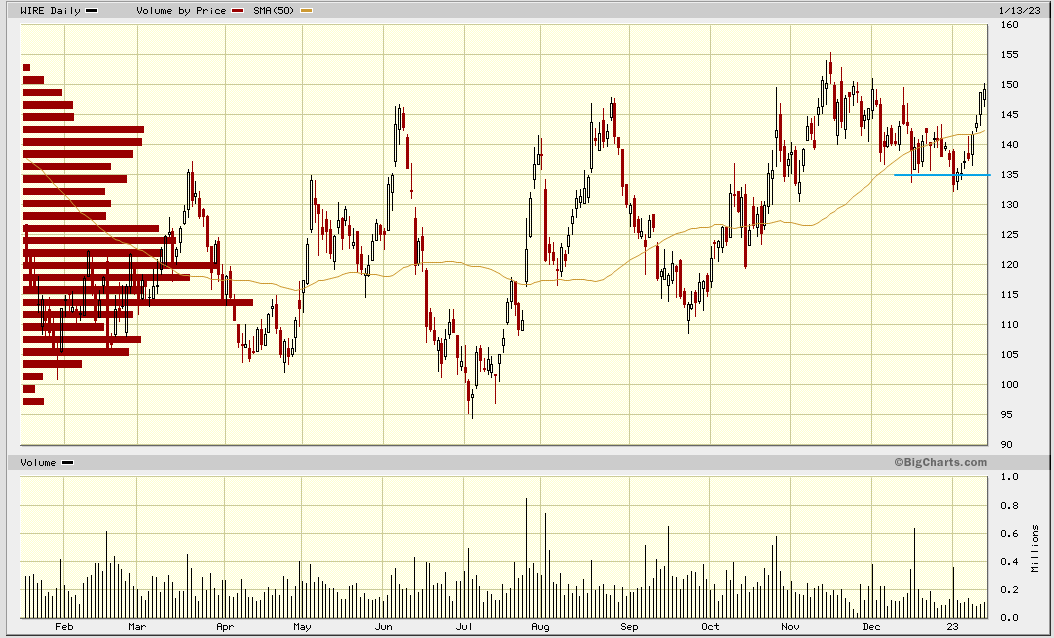

Trading Position

I have taken a starter position in WIRE but am hoping for a pullback to recent resistance levels (around $135) to buy a full position. I will then monitor the valuation and quant ratings going forward, and as long as they don’t descend below “hold” levels, I will likely keep the stock for the long term.

bigcharts

Be the first to comment