milindri/iStock via Getty Images

Wix.com (NASDAQ:WIX) is a casualty of the tech crash though the stock has bounced materially off its lows. This company arguably has a clear-cut thesis, being the backbones of web development, but the steep deceleration in growth rates has not provided support to the stock price. Management issued aggressive guidance at its 2022 Investor Day which called for an eventual recovery in growth rates. Assuming the company can hit those targets, the stock is highly compelling here considering the net cash balance sheet, cash flow breakeven profile, and low valuation.

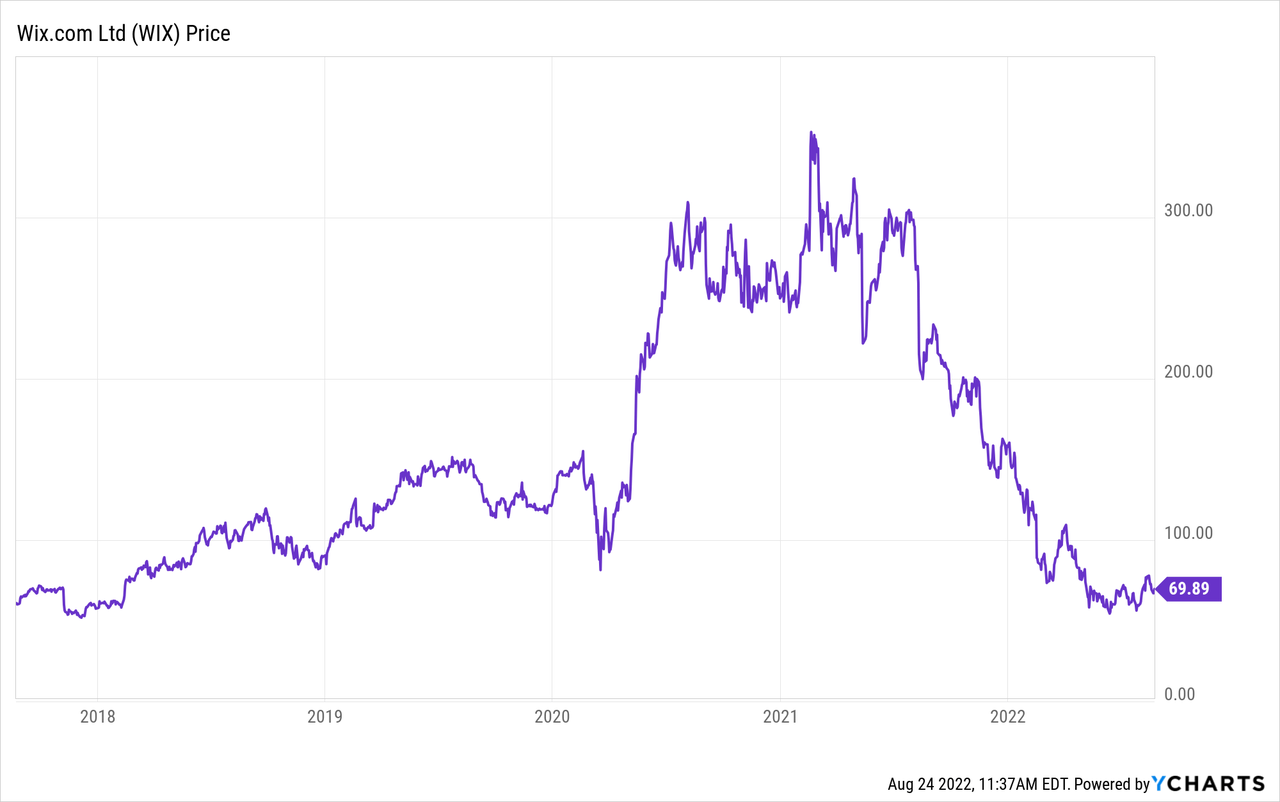

WIX Stock Price

WIX was an unsurprising beneficiary of the pandemic, but the stock has since fallen 80%, leading it to trade at the same levels it did five years ago.

I last covered WIX in March of 2020 during the pandemic crash which at one point was a home run call. The broader tech crash has led to a steep valuation reset and an attractive buying opportunity in the stock.

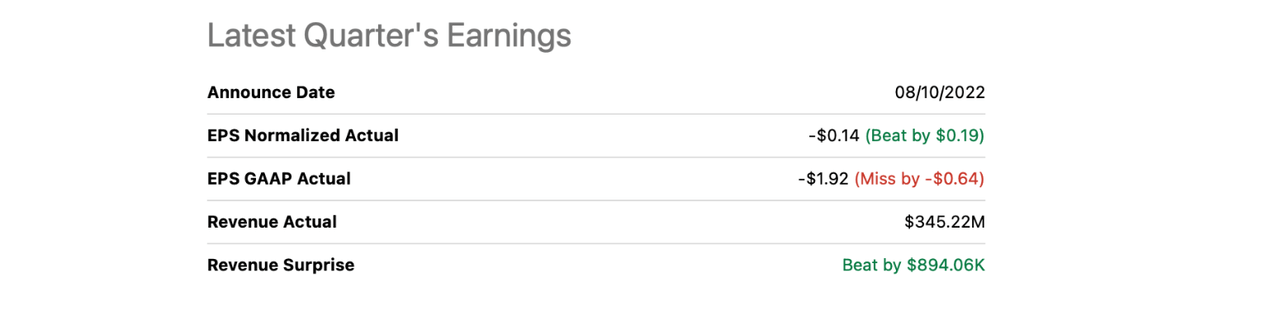

What Were Wix’s Expected Earnings?

WIX had already telegraphed slowing growth for this year with plans to reduce operating expenses.

Did Wix Beat Earnings?

WIX ended up slightly beating on revenue estimates and non-GAAP earnings.

Seeking Alpha

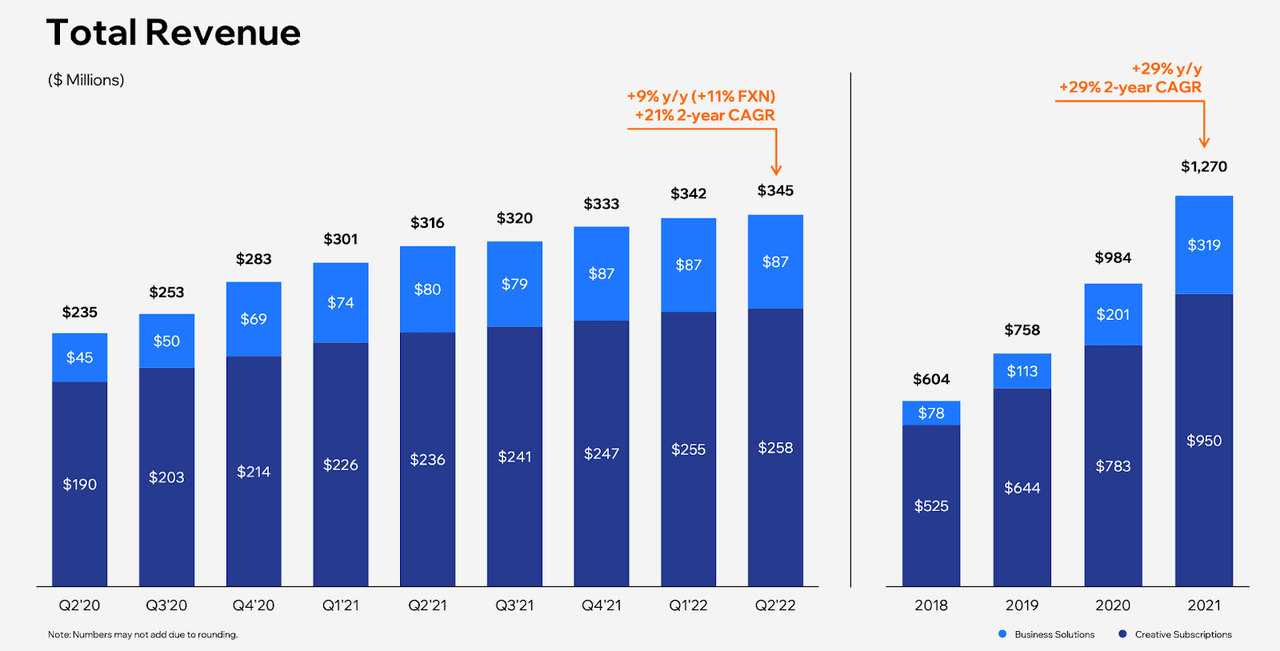

WIX Stock Key Metrics

WIX reported 9% year over year revenue growth though it noted that it represents a 21% 2-year compounded annual growth rate.

2022 Q2 Slides

The non-GAAP net loss was $7.8 million, very close to breakeven. WIX ended the quarter with $1.5 billion of cash and equivalents versus $926 million in debt, for a net cash position of around $0.6 billion. As of recent prices, that represents around 13% of the market cap.

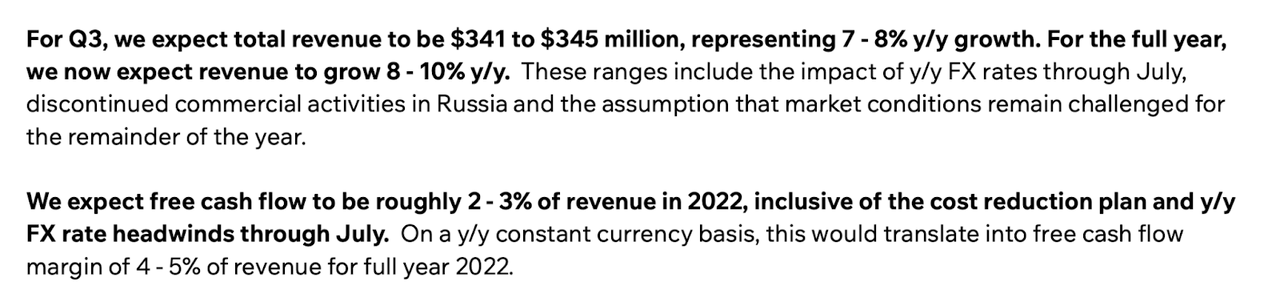

What To Expect After Earnings

Looking forward, WIX guided for revenue growth to decelerate further to up to 8% in the third quarter. WIX expects full-year revenue growth of up to 10%, implying the fourth quarter might not see much of a recovery.

2022 Q2 Slides

Is WIX A Good Investment Long-Term?

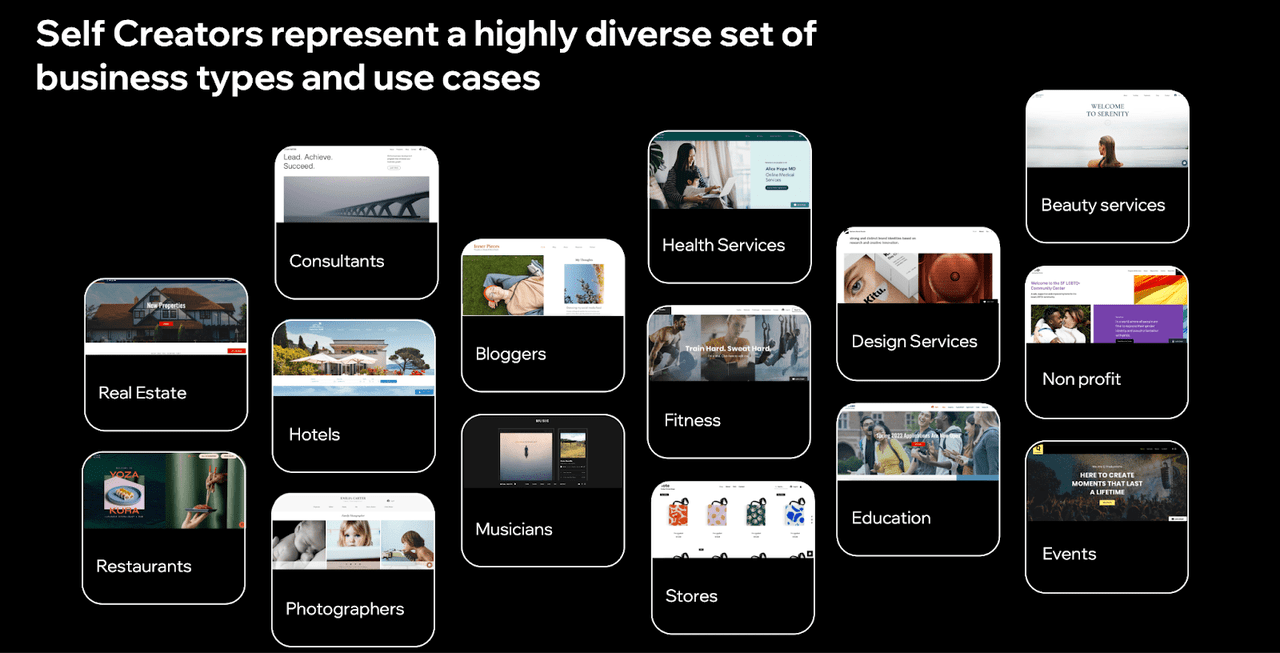

Based on the current growth rates, WIX might not appear so attractive. But one must take into account the fact that the pandemic pulled forward a lot of digital transformation growth, which obviously includes web development. It stands to reason that once WIX moves beyond the tough comparables, growth should re-accelerate meaningfully. WIX has two principal business lines, the first being for Self Creators. This is where businesses or individuals use WIX to create websites for themselves.

2022 Investor Day

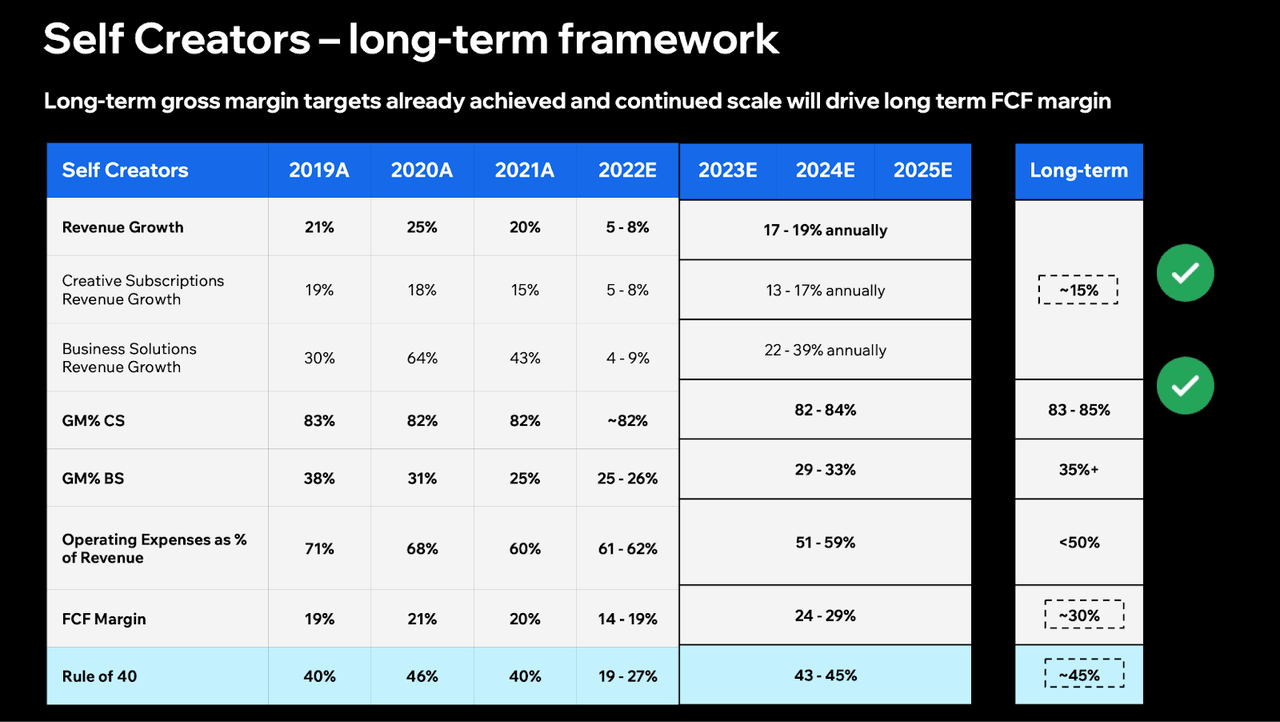

Self Creator growth is expected to decline to only 8% at the high end this year, but WIX estimates that it can accelerate to up to 19% over the next three years and stabilize in the 15% range over the long term.

2022 Investor Day

WIX also has a Partners business line in which web developers use WIX to develop websites for their customers – essentially making them re-sellers of WIX’s products.

2022 Investor Day

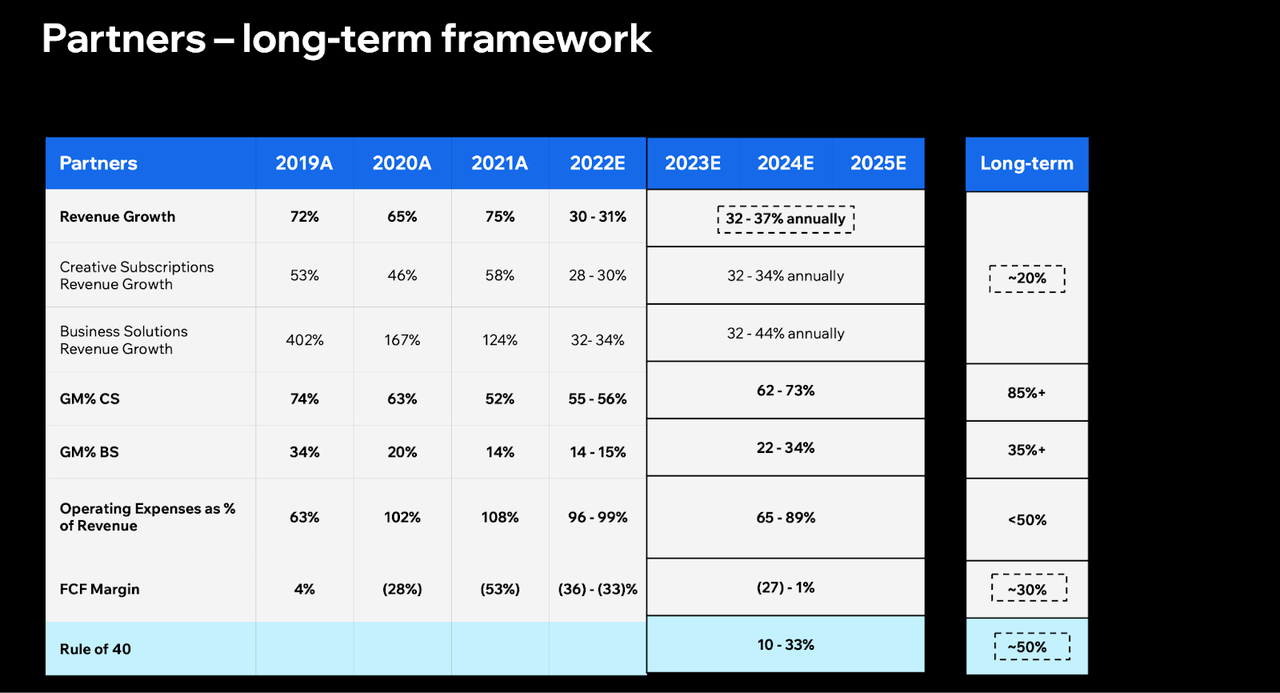

Partners growth is expected to remain strong at 31% in 2022 and even accelerate to as much as 37% over the next three years before settling at 20% over the long term.

2022 Investor Day

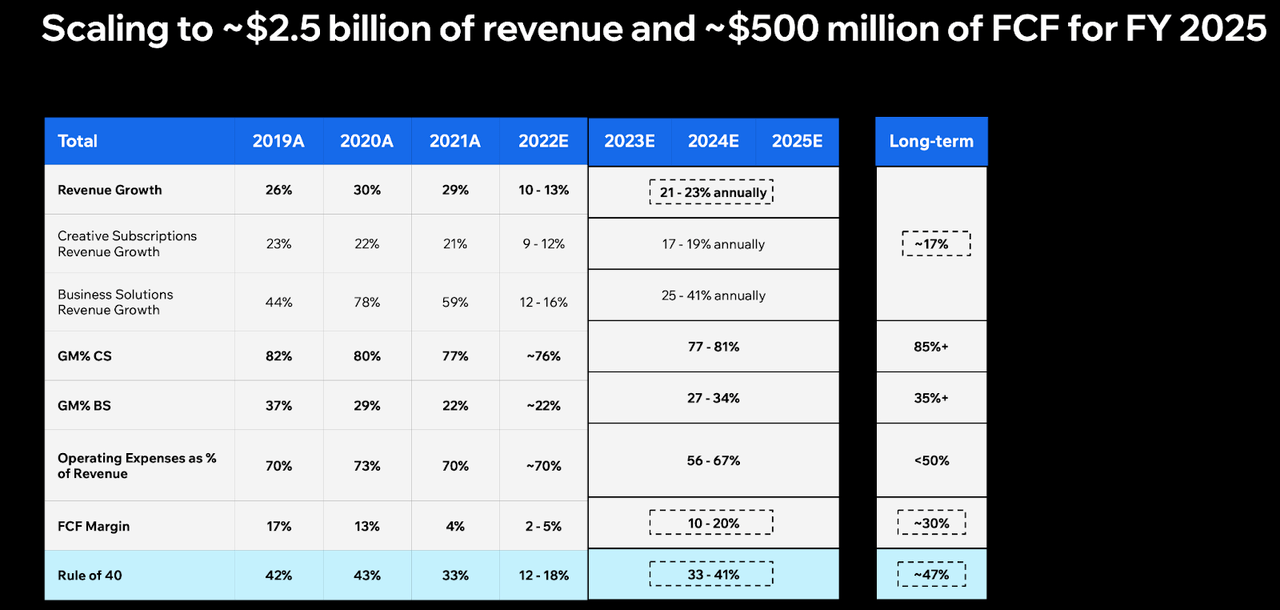

In aggregate, WIX expects to show 23% annual growth over the next three years before settling at a 17% long term growth rate.

2022 Investor Day

WIX is guiding for up to 20% free cash flow margins by 2025 and 30% margins over the long term.

Is WIX Stock A Buy, Sell, or Hold?

Those are aggressive estimates considering the steep slowdown this year, and Wall Street does not seem to buy it, as it only expects $2.1 billion of revenue by 2025.

Seeking Alpha

Yet it should not be forgotten that WIX plays a critical role in the ongoing digital revolution, as it is helping the common person build websites online. As their customers grow, WIX grows, making it essentially a direct play on the growth of the internet. I could see WIX trading at a 1.5x price to earnings growth ratio (‘PEG ratio’) upon a recovery in tech valuations. That would place the stock at around 8x sales by 2025, implying a stock price of $293 per share or 56% compounded returns over the next three years. The key risk here is definitely that of failure to achieve expected growth rates. It is intuitively easier to believe a growth deceleration story rather than a growth acceleration story, even if the excuse of tough comparables is understandable. There is also the risk that WIX has underestimated the potential cannibalizing effect that the Partners side of the business might have on the Self Creators side of the business. The current valuation implies forward growth rates of only 7%, implying some margin of safety, but at the same time WIX is only projecting 8% to 10% revenue growth this year. At these prices, I am willing to wager that growth will return, and multiples will eventually reflect the secular growth story that WIX is – I rate shares a buy.

Be the first to comment