izusek/E+ via Getty Images

Palantir Technologies Inc. (NYSE:PLTR) stock has been a total disaster for longs, and there are countless retail “bag-holders” here. It is frustrating. We get it.

Despite what has happened, we continue to like the company long term, but Palantir stock is just not working right now. Continued dilution, slowing commercial demand, and governments that will likely tighten their belts on lower tax revenues in a recession are all reasons to be cautious. It seems the company is trying to control expenses and wants to reduce the stock-based compensation (SBC), but the high level of growth seems to be grinding to a halt.

Of course, Palantir is not alone. Technology stocks, especially those that are potential game-changing names, have all been obliterated. The company just reported earnings, and we follow back up on the name in this column. Let us discuss.

It is a long road

Stocks like Palantir are indeed often extremely expensive in the early stages, but this company has been around a long time. But the innovation space is unique. For a long time, the Street could not value them on an earnings basis because there are no or very little earnings. The Street looked to the future based on sales, cash flows, etc. But with rates rising, money-losing stocks are out of favor. Debt becomes more expensive, and many companies will suffer.

Thankfully Palantir is in a decent balance-sheet position, but is a money loser. Palantir also has a massive dilution problem, which means consistent positive EPS gets kicked further down the road. We think Palantir has a lot of potential, but this market is beyond unforgiving to those companies that do not make money or have sky-high valuations. Now, growth is becoming a concern.

For years, Palantir may lose money or hover around breakeven. $7 is a level where we like this name, with all issues baked in. Speculative, but we like it. Operationally, we are seeing some positive signs, and some negative signs. The company is not bleeding out and losing money hand over first. Palantir is losing some money or is breaking even, but we would like to see a more concerted effort to boost margins and get to sustained profit, and profits that grow. But it is tough when growth is stalling.

Palantir’s Government and Commercial sectors showing slowing growth

In the just-reported quarter, performance was strong on the top line and ahead of consensus estimates. Total revenue grew 22% year-over-year to $478 million, beating estimates by almost $3 million. However, Palantir’s profitability was lower than expected by $0.01, and worse, guidance was less than consensus. That is currently crushing the stock today. But, that said, both segments are moving along, though the pace of growth has certainly stalled.

As you are likely aware, Palantir has two reporting segments: both the government and commercial segments. The commercial revenue stream has been growing rapidly, while government results have been slowing for several quarters. There are some concerns with backlog as well, but the company this year had expanded its sales team and they have been working to secure new orders. However, it is unclear if this has been effective. Government revenues have slowed their growth and now commercial growth is a concern too.

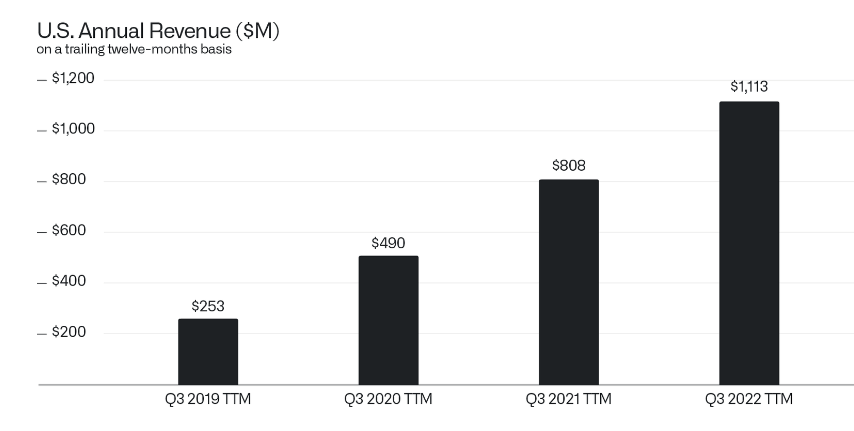

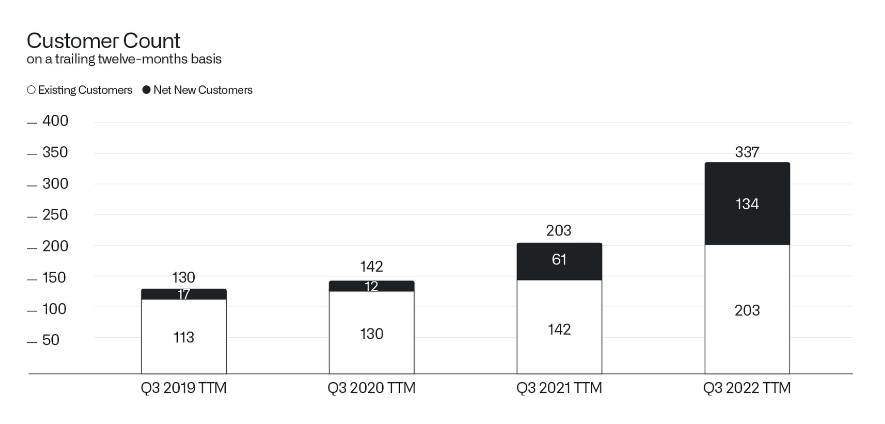

Deceleration of revenue growth is definitely a negative for a company like this that does not enjoy high earnings. That said, U.S. growth is still strong. U.S. revenue rose 31% from last year, and the company grew overall customers by 66% year-over-year.

Palantir Q3 shareholder letter

We think it is important to note that the commercial space is outpacing government customers growth, but customer growth continues to be solid. While there are growth concerns emerging, the company is certainly still growing. That is a fact.

Palantir Q3 shareholder letter

Government revenue was still up 20% form a year ago, while U.S. commercial revenue grew 53%. All in all, solid performance. Palantir is seeing very positive momentum in its margins as well. Positive movement in margins is important in a software company as it really highlights strengths, or weaknesses, in the way it distributes its products. Palantir is delivering. Gross margin was 77%. Adjusted income from operations, excluding stock-based compensation and related employer payroll taxes was $81 million, representing an adjusted operating margin of 17%, a bit lighter than the 20% margins we had seen.

Hovering around breakeven, but positive cash flow

The company lost $62 million in the quarter operationally, but adjusted income from operations was $8 million. The company is still free cash flow positive. Adjusted free cash flow was $37 million for the quarter, and the 8th-straight quarter for which this was positive. That said, the company was profitable at a $0.01 adjusted EPS bottom line figure, but this missed estimated by $0.01, so that is a negative, and another reason the stock is down.

But margins need to improve and growth must remain to offset stock based-compensation. This is still a problem, and a problem for many similar companies. Every share that is issued waters down the ability to increase EPS, that is a fact. In short, shareholders could be diluted into losses. While Palantir’s technology should help governments and businesses alike operate more efficiently, and therefore more profitably, we could see reduced spending on services like this as recession risks are mounting.

Still expensive

On the valuation front, Palantir stock is still expensive, even though shares have been crushed. Looking at traditional price-to-earnings does not work here, as it is very pricey at 150X. Silly really. Perhaps the more appropriate measure is the price-to-sales ratio, but not only is this still very high, the market has basically said it is no longer willing to pay for sky high multiples. Keep that in mind. At 9X sales, the valuation has improved from where it was last year, but this is still high. The best measures here are the cash flow metrics. Given that there is no debt and a ton of cash on hand ($2.4 billion), Palantir is in strong shape to weather any recessionary storm.

The outlook disappoints

The biggest concern right now is not valuation, it is a slowdown in performance. The Q4 guidance was pretty weak relative to expectations, despite upping the full year outlook. The Street is slamming the stock. For Q4, management guided to a base case of $503-505 million in revenue. This was below consensus of $506 million, but they upped their adjusted income from operations for the year by about 10% to $385 million. That was actually bullish in our opinion. As we look ahead, we think the company can still deliver 30% annual revenue growth, but we would like to see more work done on margins to boost cash flow and to get to real earnings. Like it or not, this is what the Street wants to see.

Take home

Look the interest rate issue hammering tech stocks does not really apply here as there is no debt and Palantir has nice positive free cash flow. They are poised to benefit from strong secular trends in big data and using analytics to improve operations. The growth rate is slowing some, but the growth is strong. Palantir valuation is still expensive, but we think the key indicator to watch aside from growing customer accounts and contract values will be margins. It has been a painful hold, but we still like the stock at $7. The one thing Palantir Technologies must do to regain confidence from investors is show that it can widen operational margins and grow profit.

Be the first to comment