Leon Neal/Getty Images News

Elevator Pitch

My Buy investment rating for Meta Platforms, Inc.’s (NASDAQ:FB) remains unchanged as per my previous update published on January 13, 2022 which focused on the stock’s valuations and share price outlook. With the company’s share price having corrected by more than a third since my earlier article, I assess FB’s 2022 outlook in this latest article.

Meta Platforms’ 2022 forecasts aren’t great, as FB is expected to see slower revenue growth and a decline in the bottom line this year. But for investors willing to look beyond the company’s expected weak financial performance in 2022, the current risk-reward for Meta Platforms is favorable as evidenced by its appealing valuations which justifies a Buy rating.

FB Stock Key Metrics

FB reported its Q4 2021 earnings on February 2, 2022, after trading hours, and the company’s shares fell by -26% to close at $237.76 on the next day, February 3, 2022. Meta Platforms last traded at $219.57 as of March 24, 2022, which suggests that its share price has dropped by -32% as compared to its pre-results announcement stock price of $323.00.

Meta Platforms’ Q4 2021 diluted earnings per share of $3.67 as disclosed in its financial results media release came in -4% below the Wall Street analysts’ consensus bottom line forecast of $3.82 per share. FB’s top line of $33,671 million registered in the fourth quarter of last year actually beat market expectations by +0.7%, so Meta Platforms’ recent quarterly earnings came in below the market consensus’ forecasts because of higher-than-expected expenses.

The company’s Facebook daily active users or DAUs declined QoQ from 1,930 million in the third quarter of 2021 to 1,929 million in the most recent quarter. Its Q4 2021 Facebook DAUs were also -1% lower than the sell-side’s consensus estimate of 1,950 million as per S&P Capital IQ data. This could be reflective of stiffer-than-expected competition from other social media platforms like TikTok.

In summary, Meta Platforms disappointed the market on its key financial metric (earnings per share) and operating metric (DAUs).

What Is Meta Platform’s Stock Forecast For 2022?

FB’s weaker-than-expected 2022 management guidance was another key reason for the stock’s poor price performance in the last two months, apart from lower-than-expected fourth-quarter earnings as discussed in the preceding section.

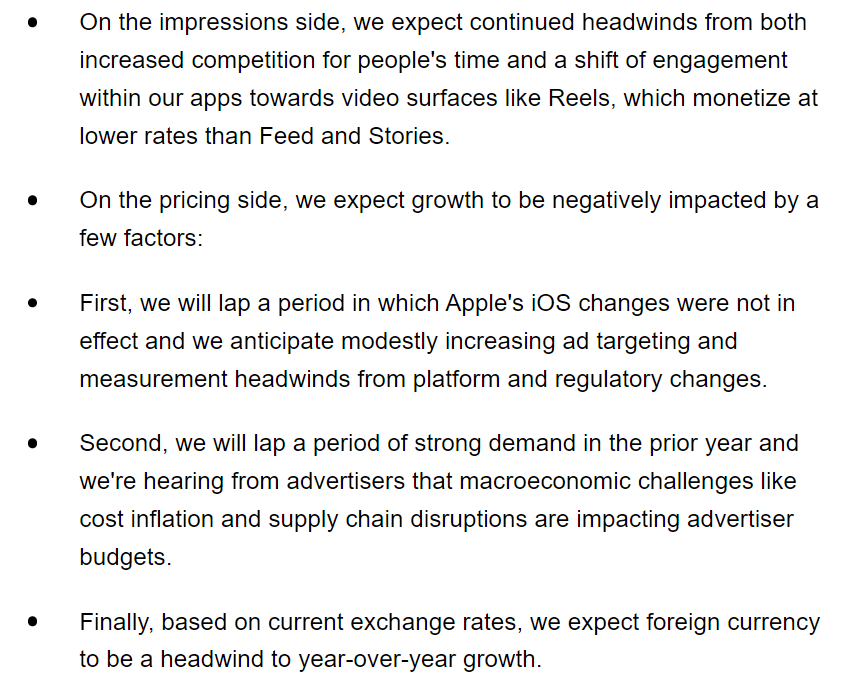

Meta Platforms guided for its revenue to increase by +3%-11% to between $27 billion and $29 billion in the first quarter of 2022, as highlighted in the company’s Q4 2021 earnings press release. The company highlighted the reasons for expectations of slower top line expansion in the current quarter in the extract from its media release presented below.

FB’s Explanation Of Factors Leading To Its Below-Expectations Q1 2022 Revenue Guidance

Meta Platforms’ Q4 2021 Earnings Release

Even if the high end of FB’s Q1 2022 revenue growth guidance (+11%) materializes, this will be Meta Platforms’ slowest quarterly sales expansion since the second quarter of 2020 when it delivered a +10.7% YoY increase in revenue. Prior to Meta Platform’s Q4 2021 earnings announcement, the sell-side analysts had expected the company to increase its top line by a much higher +16% YoY to $30.27 billion in Q1 2022.

To make things worse, Meta Platforms’ Q1 2022 revenue might potentially fall short of market expectations. A March 8, 2022, sell-side research report (not publicly available) published by Piper Sandler titled “Meta through the Pricing Periscope” noted that the company’s 2022 “YTD CPMs (Cost Per Mille) are down 6% y/y and 11% q/q, suggesting low-teens impression growth to hit the mid-point of (Q1 2022 revenue) guide.”

According to S&P Capital IQ, the market consensus currently expects FB to achieve revenue growth rates of +8.5% and +12.2% for Q1 2022 and full-year FY 2022, respectively. In comparison, Meta Platforms’ top line expanded by +20% YoY in Q4 2021, and the company’s revenue was up +37% for the full-year in 2021.

For full-year 2022, Meta Platforms’ management guidance points to a substantial increase in expenses and capital expenditures. FB sees its total costs rising by +30% from $71.2 billion in fiscal 2021 to $92.5 billion in FY 2022 (mid-point of management guidance). Separately, capital expenditures for Meta Platforms are guided to increase by +69% from $18.6 billion last year to $31.5 billion in the current fiscal year.

In my earlier October 7, 2021 article for Meta Platforms, I had noted that FB “expects to spend around a few billion dollars every year on Metaverse-related investments for the foreseeable future” and this is one of the factors for the rise in expenses. Another factor is the increase in investments in “short-form video like Reels” to deal with competition from TikTok which FB highlighted at its Q4 2021 earnings call.

Taking into account FB’s management guidance with respect to revenue and costs, Wall Street analysts forecast that Meta Platforms’ earnings per share will decline by -9.8% YoY to $12.4 in FY 2022. In the next section, I evaluate if the market has factored in the company’s lackluster 2022 outlook into its valuations.

Is Meta Platforms’ Valuation Fair?

FB’s shares are undervalued, instead of being fairly valued.

Notably, Meta Platforms’ forward earnings multiples are way below historical averages. FB’s consensus forward FY 2022 EV/EBITDA multiple is 9.3 times as of March 24, 2022, as per S&P Capital IQ data, while its five-year average consensus forward next twelve months’ EV/EBITDA multiple is a much higher 13.7 times. The stock’s forward FY 2022 normalized P/E multiple of 17.8 times now is also significantly below its five-year mean forward normalized P/E ratio of 25.0 times.

Also, the market consensus’ financial forecasts point to Meta Platforms maintaining its future ROEs in the mid-20s percentage level and achieving a FY 2023-2025 earnings per share CAGR of +20%. In comparison, FB’s forward P/E multiple in the high-teens seems too low.

Meta Platforms’ Stock Catalysts To Watch For

I think that there are catalysts that investors should watch out for, which relates to the company’s stance on future investments.

It is too early to judge whether FB’s bet on the Metaverse or other growth initiatives will be a success or failure. But Meta Platforms has made it clear that it will pivot away from businesses that fail to deliver. At the same time, FB is ready to be more aggressive in spending on specific growth initiatives for which initial results are favorable. At the Morgan Stanley (MS) Technology, Media and Telecom Conference 2022 on March 10, 2022, the company stressed that it “can moderate them (specific investments) over time” if “we are less successful” and it “will be pushing them harder (increase spending)” on certain projects where it “can drive good results.”

This suggests that Meta Platforms’ management team is much more flexible and adaptive than what the market perceives.

A catalyst for FB in this respect will be a future cutback in spending on certain business areas and the return of more excess capital to shareholders, which will improve profit margins and ROEs for the company going forward.

On the other hand, another catalyst could be Meta Platforms disclosing excellent metrics in relation to certain investments that it made in the past, and announcing a further increase in capital allocated to these successful projects. When these things happen, the market will take this as a positive sign that FB has made the right bets in specific areas which are starting to pay off.

Is FB Stock A Buy, Sell, Or Hold?

FB stock is a Buy. The poor 2022 outlook for FB is already priced into its valuations, and I am of the view that there are catalysts in place (as highlighted in the preceding section) to bring about a positive re-rating of its shares in the intermediate term.

Be the first to comment