vzphotos

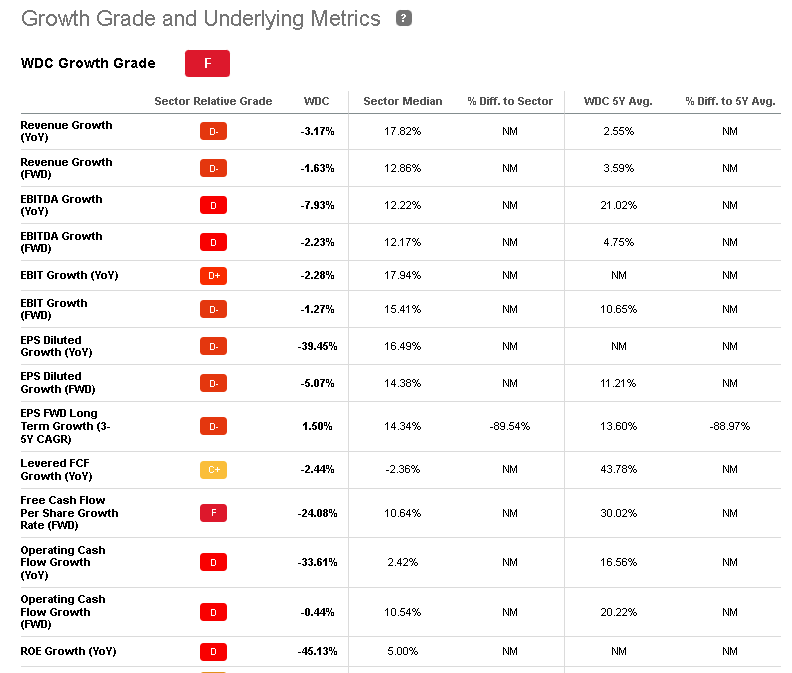

I am a computer technician. I concur with the hold rating that Seeking Alpha Quant AI has for Western Digital Corporation (NASDAQ:WDC). I agree with the correct F growth grade that Seeking Alpha Quant AI gave Western Digital. This pessimistic outlook for WDC’s growth potential is why Quant AI cannot rate it as a buy. The –45.47% YTD performance of WDC could get worse because of the screenshot below.

Seeking Alpha Premium

Avoid going long or averaging up on WDC because it is clearly a falling knife. No bottom-fishing expert will go long on WDC when its downward momentum remains strong. Hold on, be patient. Wait for others to make WDC more affordable. The negative growth performance of Western Digital could change for the better thanks to its cloud storage business.

Holding on to WDC is Justified

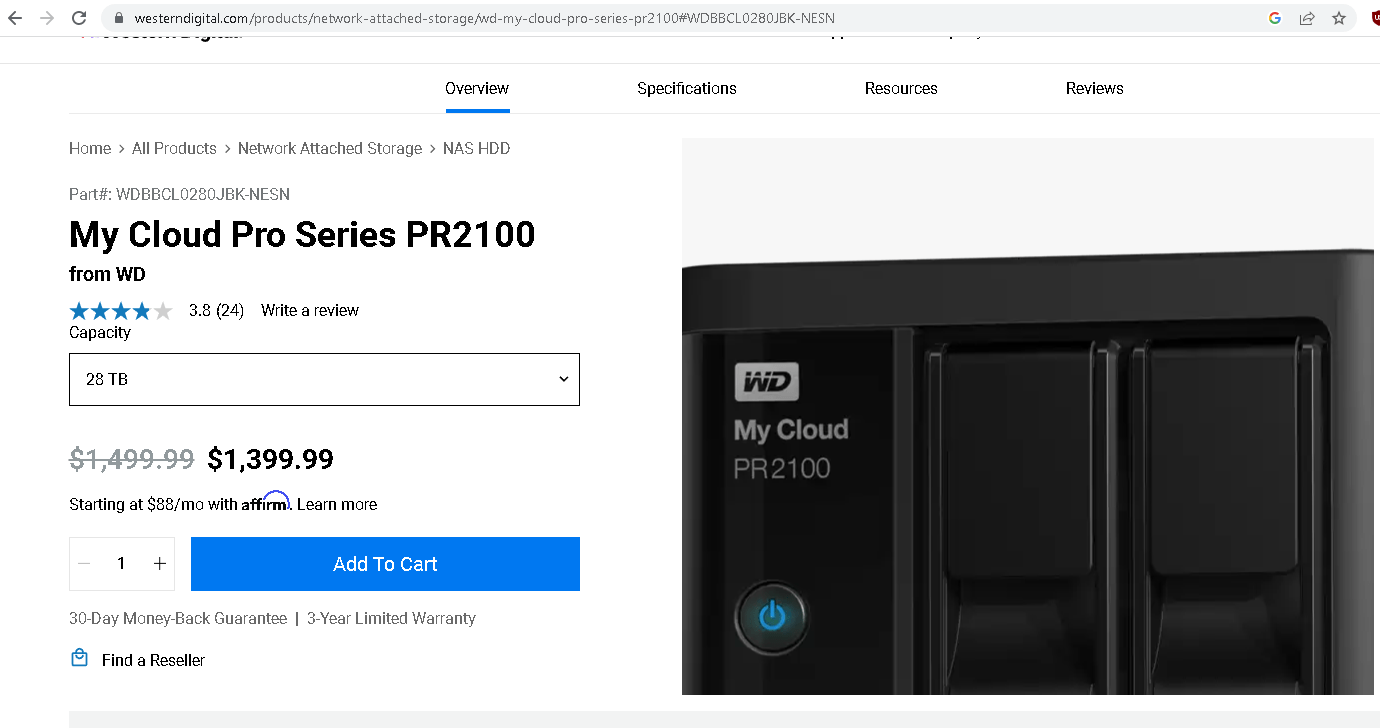

The right way to evaluate WDC is to include its long-term potential as a cloud storage provider. Charging people and business owners for cloud storage is an easy catalyst for Western Digital. WDC’s Cloud Storage pro series plans are not cheap. They are geared for hosting databases, custom enterprise apps, websites, and mobile/web apps.

Westerndigital.com

The optimism for WDC might return after more investors realize this company is engaged in the fast-growing $83.41 billion global cloud storage industry. This niche market touts a CAGR of 24%. My fearless forecast is that the higher possible margin on renting out SSDs and traditional hard disks via cloud storage could help Western Digital keep its good profitability.

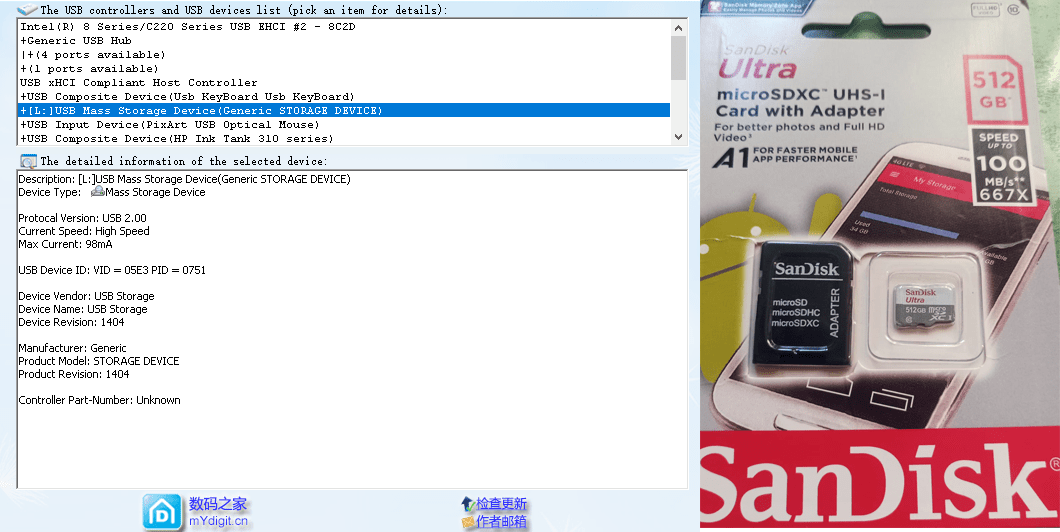

The long-term importance of Western Digital’s cloud storage platform is that it helps reduce the impact of counterfeit or fake SanDisk and Western Digital SSDs. I recently bought a 512GB SanDisk microSD card from Lazada’s 11.11 super sale event. It was from a LazGlobal vendor located in China. Using the free tools for verifying the authenticity of flash storage products, I was able to prove it was a counterfeit SanDisk product. ChipGenius was unable to identify SanDisk as the manufacturer. SanDisk has factories in China.

Motek Moyen

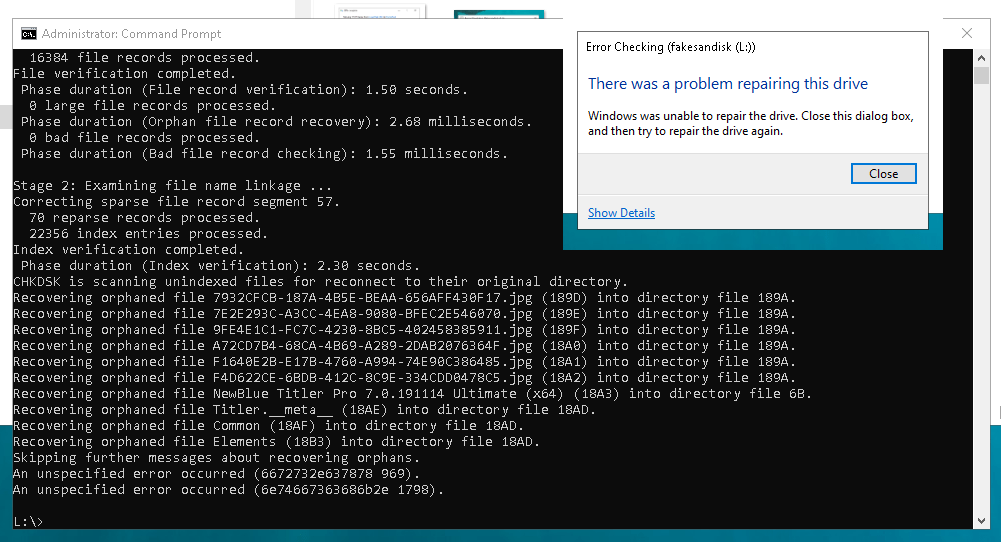

I was able to reformat it from exFAT to NTFS. There were errors when video recording or copying large 50 gigabyte files to this LazGlobal-sourced 512GB SanDisk MicroSD. I tried GUI-based and command line chkdsk, I got errors.

Motek Moyen

I fixed it using MiniTool Partition Wizard. I am able to use it now as a 512gb storage disk. It is not suitable for recording full HD video with an action camera or a smartphone. It has a maximum read and write speed of 19MB/sec.

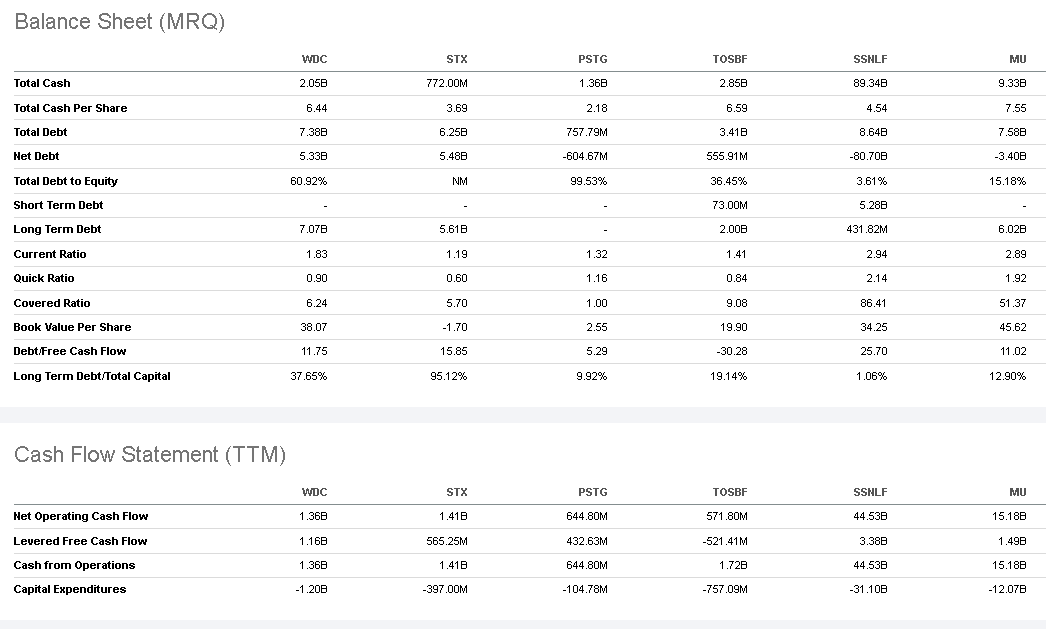

The balance sheet of Western Digital is not that strong. Its total debt is almost $7.4 billion, while its total cash is just $2.05 billion. It cannot afford to spend futile money on chasing after counterfeiters of its flash cards and SSD products. China is still the world’s top source of counterfeit goods. The manufacturing and selling of imitation products persist because the government there is not strict about it. Exporting imitation products still generates foreign remittances for China’s faltering economy.

Seeking Alpha Premium

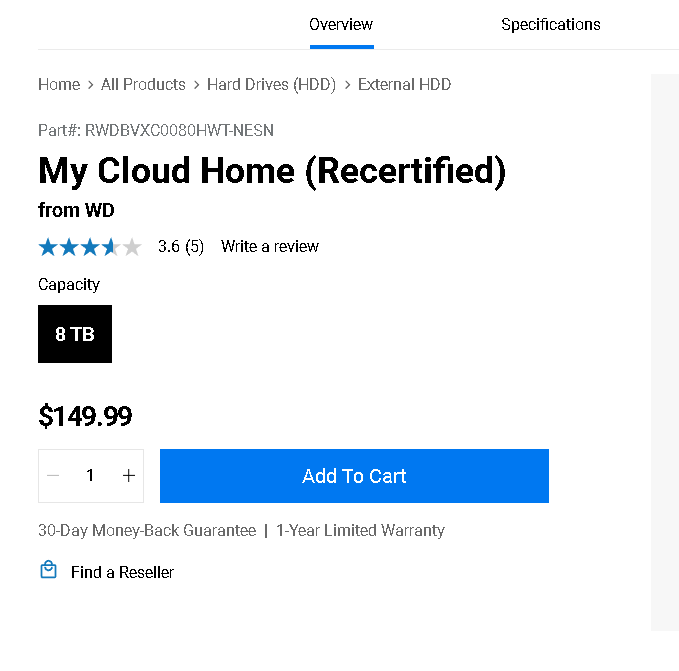

I opine data center-grade cloud storage sales/subscriptions from Western Digital ultimately reduces people’s need to buy counterfeit memory cards and SSD drives. It is a tailwind that anyone can avail of WDC’s affordable cloud storage services. Even a poor Filipino like me can afford the $149.99 price of owning 8 terabytes of cloud storage.

westerndigital.com

Cloud Storage Reduces Pressure from Competition

Western Digital Corporation is not the number one supplier of hard disk drives. It is Seagate Technologies (STX). WDC is also not the number one in NAND flash drive. It is Samsung (OTCPK:SSNLF). Western Digital is a midget compared to Samsung. Samsung will always lead Western Digital when it comes to SSD and memory card sales. Samsung is the fourth-largest advertiser in the world. Samsung spent $9.7 billion in measurable ad placements last year. That ad budget is already half of Western Digital’s latest annual revenue of $18.8 billion.

Cloud storage services will help Western Digital rely less on selling physical retail memory cards and HDDs and SSDs. My new favorite brands for SSDs and memory cards are Ramsta and Kingston. They are not as famous as Samsung or Western Digital/SanDisk, but they are more affordable while also being of high quality. Seagate has its own Lyve Cloud storage service. Kingston and Ramsta still do not offer alternatives to Western Digital’s paid cloud storage platform. Going forward, paid cloud storage revenue should be your most important metric when evaluating the investment quality of WDC.

Cloud storage reduces the headwinds from counterfeit SSD and memory cards. It also helps WDC avoid a pricing war against Ramsta and Kingston. Cloud storage will help protect the good profitability of Western Digital. A negative TTM revenue CAGR is forgivable if Western Digital stays profitable.

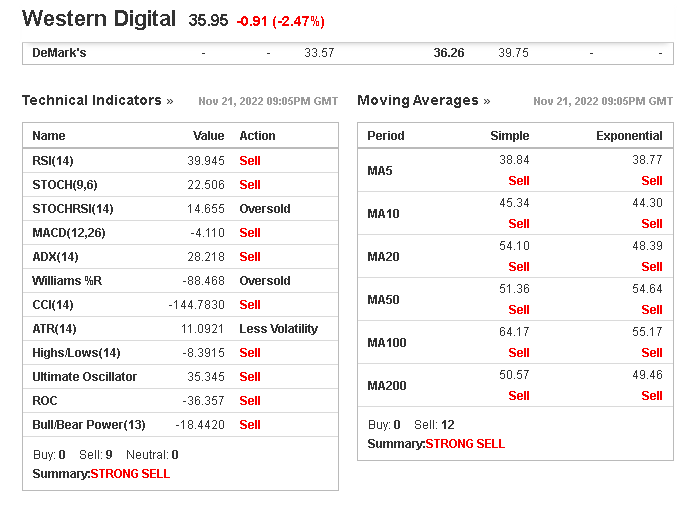

Technical Indicators Are Not Bullish

I cannot rate WDC as a buy because there was no bull run after its decent Q3 earnings report last October 27. My hold rating is also because of the bearish Relative Strength Index indicator for WDC. The rsiBearCross trade alert is a shortcut for RSI Bearish Cross which signifies a short-term bearish signal. WDC’s RSI has crossed below the neutral score of 50.

Do not average up on WDC because other one-month scenario technical indicators are also not bullish on WDC. Refer to the chart below, pick your favorite market emotional indicators. All of them are pessimistic for Western Digital Corporation.

Investing.com

Conclusion

This is a hold thesis for WDC. It is congruent with the rating from Seeking Alpha Quant AI. Wait for others to pummel down WDC. SA authors and Wall Street analysts rate WDC as a buy. The average price target of Wall Street analysts for WDC is $45.02. It could be profitable to trust their highly paid bullish assessment for Western Digital. WDC trades at less than $37.

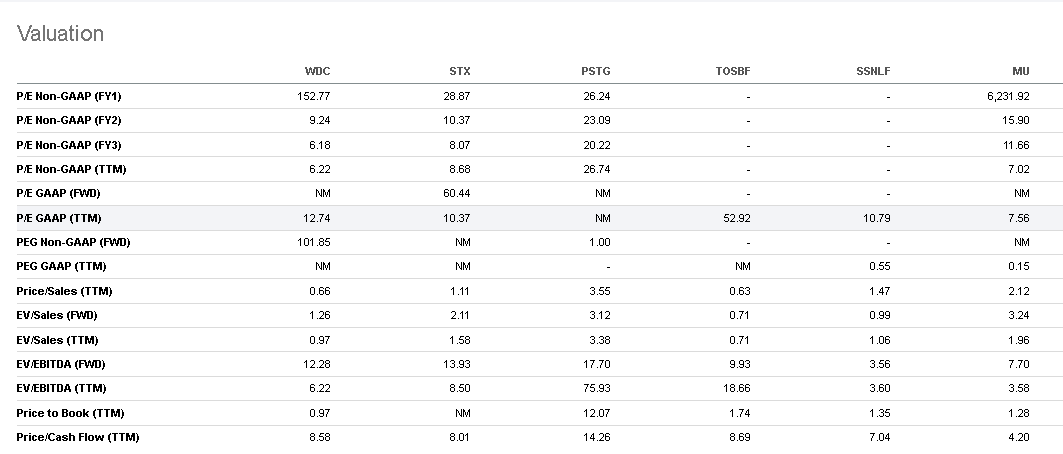

Exercise your own critical thinking. Heed my hold recommendation or go join the buy WDC team. Hold on and wait until Western Digital Corporation has more affordable valuation ratios than Seagate or Samsung. As of now, WDC’s TTM GAAP P/E of 12.74 is a bit higher than the 10.37 of STX and the 10.79 of SSNLF.

Seeking Alpha Premium

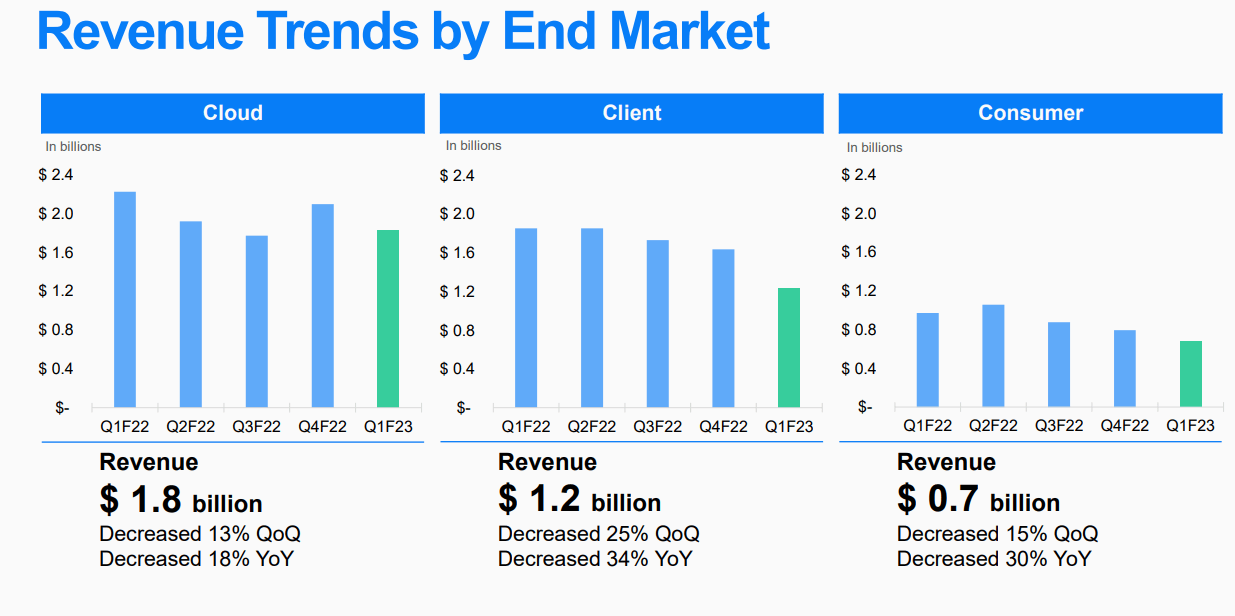

Get out of your WDC long position if the company loses profitability over the next few quarters. It could signal that its cloud or datacenter business is not generating enough money to offset the headwinds from counterfeit storage products and the competition from big and small rivals. We need to see the Cloud segment doing YoY gains to offset the YoY declines of the Client and consumer segments.

Westerndigital.com

The downside risk is that WDC will continue to fall if the Cloud segment’s revenue cannot grow fast enough. Going forward, the partnership with Japan-based KIOXIA Corporation plus the 92.9 billion yen ($654 million) government subsidy, could eventually reverse the falling knife status of WDC.

Be the first to comment