Joey Ingelhart/E+ via Getty Images

Nobody likes getting small returns on their investments. But getting a little bit of upside is significantly better than experiencing downside, especially if the timeframe we are talking about is a long one. One example I could point to where this kind of disparity exists involves a company called Werner Enterprises (NASDAQ:WERN). For those not familiar, the business provides truckload transportation and logistics services. With a market capitalization of $2.90 billion, the company is fairly small in the grand scheme of things. But it has a sizable network spread across the US. Recently, financial performance achieved by the company has been positive. Add on top of this the fact that shares are cheap on an absolute basis but do look a bit pricey relative to similar firms, and I must say that it makes for a decent, but far from spectacular, ‘buy’ prospect at this time.

Not an awful ride

The last article I wrote about Werner Enterprises was published back in September of 2021. In that article, I talked about how well the company had performed leading up to that point, both from a fundamental perspective and a share price perspective. At that moment, however, the upside the company was experiencing was trailing what the broader market had achieved. All things considered though, I believed that the company made for an appealing prospect, especially because of how shares were priced on a forward basis. This led me to reiterate the ‘buy’ rating I had previously assigned the company. Since then, things have gone quite well. Although the S&P 500 is down 9.6%, shares of Werner Enterprises have generated upside for investors of 1.4%. For context, since my first article about the company back in January of 2021, shares have seen upside of 11% compared to the 5.8% rise the S&P 500 posted.

Author – SEC EDGAR Data

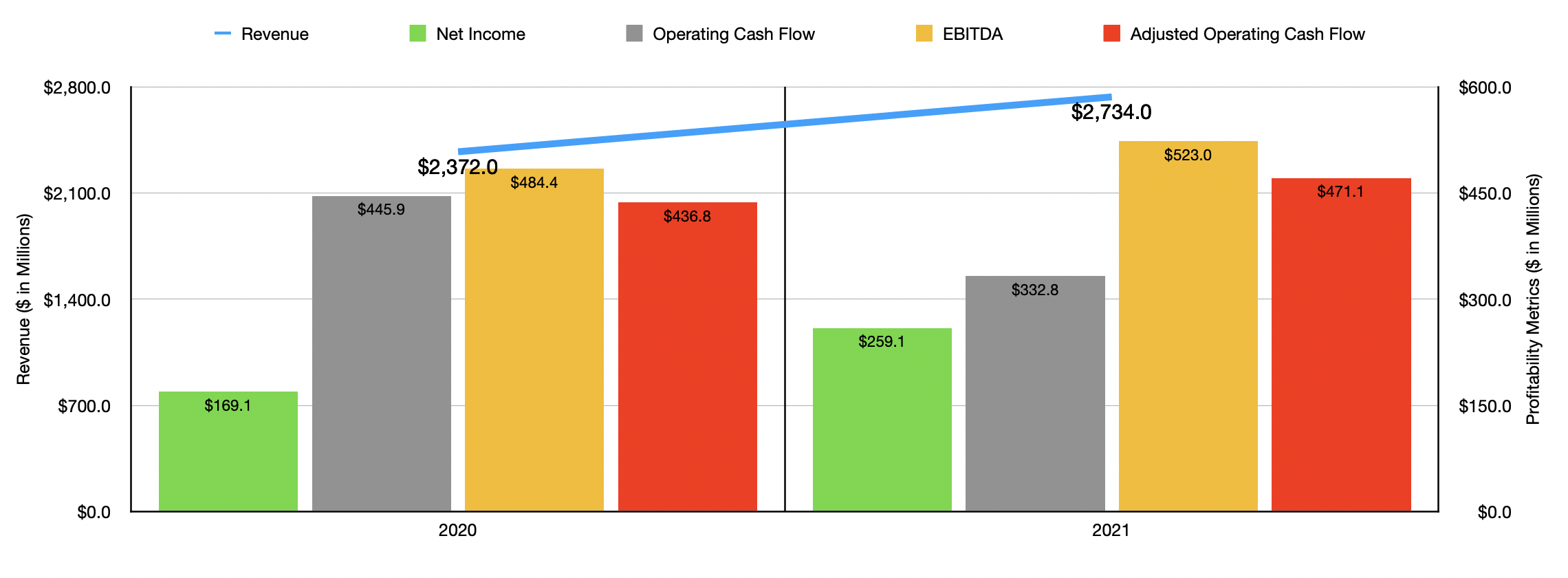

To understand why the company has done so well as of late, I would first like to start with how it finished its 2021 fiscal year. Sales for that time came in at $2.73 billion. That represents a sizable improvement over the $2.37 billion generated the same time one year earlier. This 15.3% increase year over year was driven by a few factors. Trucking revenue, for instance, jumped 7.3% from $1.67 billion to $1.79 billion. This came as the average tractors in service grew by 2.9% and as average revenue per tractor increased 4.3%. A big part of the increase for the company came from a rise in fuel surcharges. This skyrocketed 47.6% from $158.61 million to $234.16 million. Much of that had to do with higher fuel prices. The company also saw non-trucking and other operating revenue pop 26.5% from $17.2 million to $21.8 million. Under its Werner Logistics unit, the company experienced a 32.5% rise in operating revenue, with sales climbing from $469.8 million to $622.5 million. This came as the average tractors in service jumped 32.3% for the company, and was also driven by higher pricing that the company was able to achieve thanks in large part to supply chain constraints.

During this window of time, profitability for the company also improved. Net income jumped from $169.1 million to $259.1 million. other profitability metrics for the company also improved. But not all of them did. For instance, operating cash flow actually declined from $445.9 million to $332.8 million. But if we adjust for changes in working capital, it would have risen from $436.8 million to $471.1 million. Likewise, EBITDA for the company popped up from $484.4 million to $523 million.

Author – SEC EDGAR Data

Strength for the company largely continued into the 2022 fiscal year. For the first nine months of the year, revenue came in at $2.43 billion. That’s 23.3% higher than the $1.97 billion reported the same time one year earlier. Once again, trucking fuel surcharges helped the company in this respect, climbing from $165.7 million to $309.6 million. But this is not to say that other portions of the company did not fare well. For instance, trucking revenue, net of fuel surcharges, still managed to jump 12.6%, shooting up from $1.30 billion to $1.46 billion. This increase, management indicated, was driven by multiple factors. This includes a 6% rise in the average number of tractors in service and a 6.2% increase in average revenue per tractor. Meanwhile, the Werner Logistics segment saw its revenue jump from $437.5 million to $580 million. That increase, amounting to 32.6%, came as the average number of tractors in service skyrocketed 44.7%. This is not to say everything was great. Management did notice, in the latest quarter, that there were fewer premium pop-up freight opportunities, intermodal customer and market challenges, and softening demand and startup costs in the Final Mile niche. The decline in pop up freight opportunities especially is expected to have an even larger impact on revenue and operating income for the fourth quarter compared to the third quarter. But management has not provided detailed guidance on this.

On the bottom line, some of the data reported by management was somewhat mixed. Net income, for instance, fell from $182.3 million to $181.1 million. Some of this pain was associated with a 56.5% increase in non-driver salaries, wages, and benefits in the non-trucking Werner Logistics segment as the company has focused a lot of its growth efforts there. Inflationary pressures have also been an issue. But management did say that they are starting to see some easing in the competitive driver recruiting and retention markets. Other profitability metrics for the company performed fairly well. Operating cash flow went from $253.3 million to $332.7 million. If we adjust for changes in working capital, it still would have risen from $328.2 million to $329.4 million. Meanwhile, EBITDA was also on the rise, having increased from $369 million to $379.4 million.

Author – SEC EDGAR Data

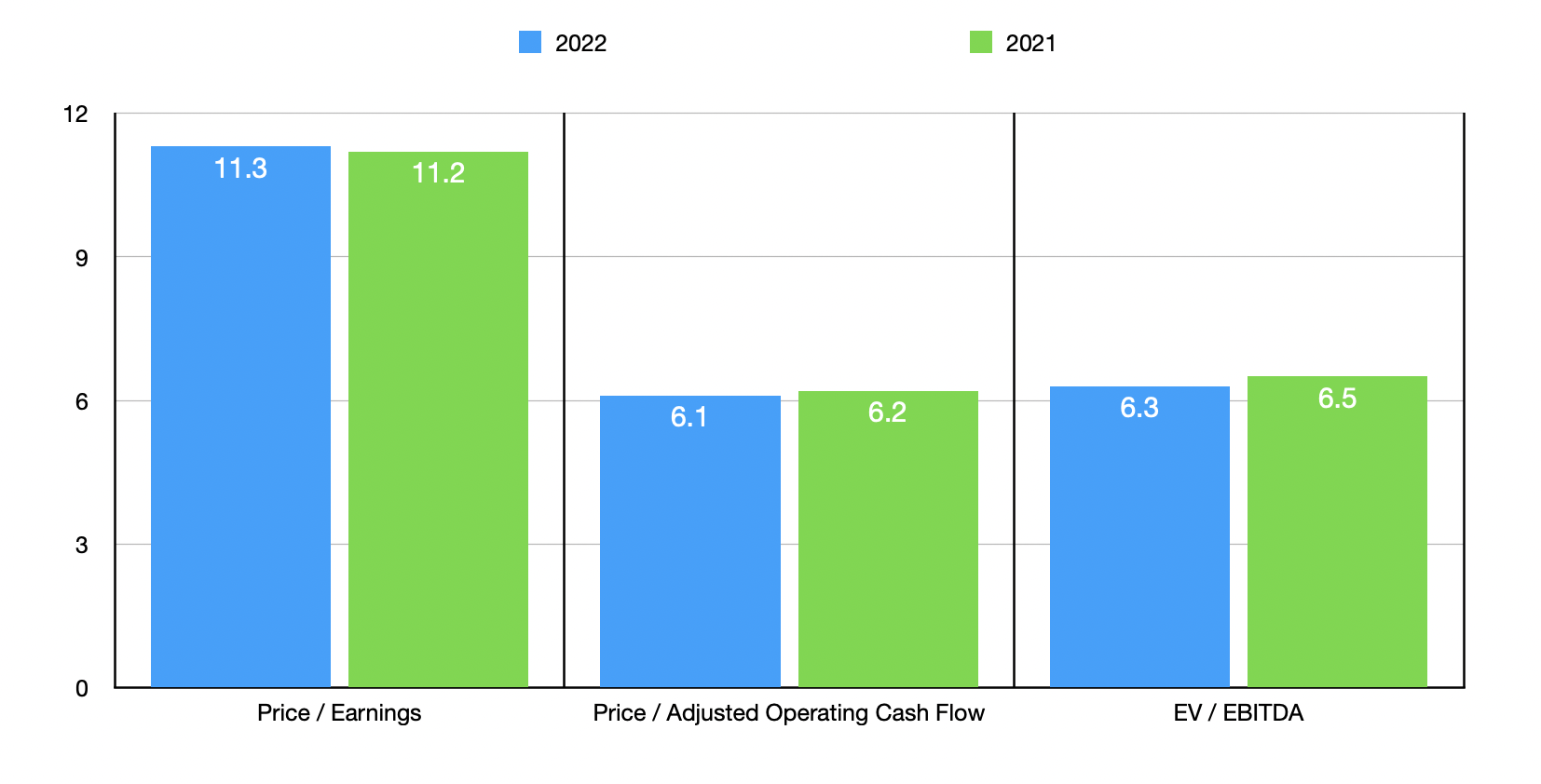

Management has not provided any detailed guidance for the final quarter of 2022. But if we just annualize results experienced so far, we would anticipate net income of $257.4 million, adjusted operating cash flow of $472.8 million, and EBITDA of $537.7 million. Based on these numbers, the company would be trading at a price-to-earnings multiple of 11.3. The price to adjusted operating cash flow multiple would be considerably lower at 6.1, while the EV to EBITDA multiple would come in at 6.3. As you can see in the chart above, this pricing is very similar to what we would get if we relied on data from the 2021 fiscal year. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 5.1 to a high of 15.3. And using the EV to EBITDA approach, the range was from 3.4 to 6.7. In both of these cases, four of the five companies were cheaper than our target. Meanwhile, using the price to operating cash flow approach, the range was from 4.9 to 9.5. In this scenario, two of the five companies were cheaper than Werner Enterprises.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Werner Enterprises | 11.3 | 6.1 | 6.3 |

| ArcBest (ARCB) | 6.5 | 4.9 | 3.4 |

| Marten Transport (MRTN) | 15.3 | 8.2 | 6.7 |

| Heartland Express (HTLD) | 9.7 | 9.5 | 5.9 |

| XPO Inc (XPO) | 5.1 | 5.9 | 4.0 |

| Schneider National (SNDR) | 9.6 | 6.2 | 4.5 |

Takeaway

All things considered, I must say that I continue to be impressed, operationally speaking, by Werner Enterprises. Although the company has faced some issues as of late, its cash flows remain robust and its future will likely be bright. The stock is a bit pricey compared to similar firms. But on an absolute basis, it still falls in the value territory. After taking all of these factors into consideration, I believe that the firm still makes for a soft ‘buy’ candidate at this time.

Be the first to comment