ErikMandre/iStock via Getty Images

According to wildlife experts, when a bear attacks, you are supposed to loudly and calmly in a low tone tell them to go away.

Oddly enough, the same tactic can be used for a bear attack in the stock market. Just as predatory animals can sense fear, short and distort attackers prey on fear, using obfuscation and insinuation to stoke up as much fear as possible to make their short sale work.

I have long been bearish on Welltower (NYSE:WELL), but even as a former bear I feel compelled to expose the flaws of the recent short and distort attack on Welltower from Hindenburg.

Bearish versus short and distort attack

Bearishness is a healthy part of the market. It is simply a reflection of an analyst looking at a stock and believing it to be overvalued relative to its fundamental prospects. Regular short selling is also a healthy part of the market being the bearish equivalent of buying a stock long.

A short and distort attack is a whole different thing. In my years as a REIT analyst, I have seen quite a few bear attacks and they follow a fairly predictable pattern.

- Find a problem with the business

- Imply that the problem is a result of management failure (laziness, incompetence, fraud or something similar)

- Extrapolate that problem via insinuations about management to the entire business.

Using these 3 steps, short and distort attackers can make a minor blemish look damning.

Another key aspect of short and distort attacks is that they are usually lawyered up so they know what they can and cannot say. Most or all of the factual data in these attacks will be true with the obfuscation instead coming from implications.

Regarding the Hindenburg attack on Welltower, the fear mongering implications begin right at the start with the title of their report:

Hindenburg

As you know, a shell game is a con artist’s street trick to swindle people out of their money.

Hindenburg forms their argument around the recent joint venture between WELL and Integra which contains their ProMedica assets. As usual, it begins with an actual problem with the business as ProMedica is legitimately struggling.

From here, Hindenburg suggests that Integra is not actually a real company as it was just founded earlier this year and is run by a 29 year old kid. In the joint venture, WELL was able to keep its cashflows in place and Hindenburg claims this is due to it being propped up by the fictitious or incompetent entity of Integra.

Here is the headline of the section from the Hindenburg research in which this is insinuated:

Hindenburg

The rest of their report is essentially talking about how woefully unprepared Integra is to handle over 100 SNFs with a suggestion that its failures will take down WELL.

Why Hindenburg’s interpretation of events is wrong

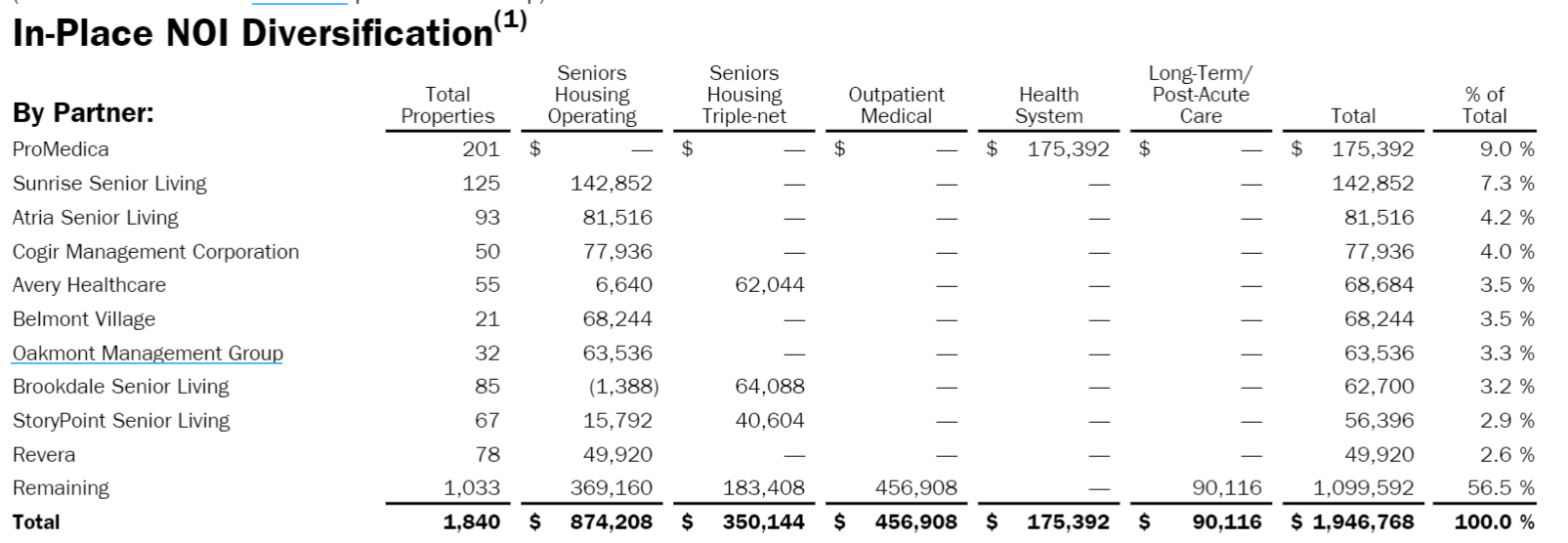

Here is the factual component that they started with. ProMedica is indeed a troubled tenant with weak financial status and is also WELL’s largest tenant at 9% of NOI.

Supplemental

The nature of the problem, however, is not incompetence or fraud or anything sinister. It is simply a result of the fact that doing business in the real world involves risk.

When Welltower acquires assets, they examine the spectrum of likely future scenarios and only buy when the price point and return potential make sense given that outlook. In buying the ProMedica assets, their analysis suggested it was a favorable purchase for shareholders.

It so happens that some of the acquisitions took place shortly before the pandemic.

All the responsible underwriting went right out the window.

That is what black swan events do.

They drastically alter the environment such that even well-planned business activity can turn out to be disastrous. That is what resulted in ProMedica struggling to pay its bills.

To remedy the situation, there was a sort of renegotiation in which ProMedica sold its 15% interest in the joint venture to Integra, making it now an 85%/15% JV between WELL and Integra. The idea is that Integra will help find and install new operators for the properties and they are incented to do so because their equity stake is junior to Welltower’s.

Integra was not involved in the struggles and has simply been brought in as a third party to try to find new tenants. Maybe it will work and maybe it won’t. As far as I can tell, Welltower has not paid Integra a single penny. It was ProMedica’s stake in the JV that Integra received.

So, if Integra does turn out to be a fraudulent shell game as Hindenburg implies (I have no idea on the likelihood), it has almost no impact on Welltower. Welltower would still own the properties and they are still being operated by ProMedica.

The Hindenburg report weaved Integra in with Welltower as a sort of guilt by association and it is unclear to me if Integra is even guilty in the first place. It is very clear, however, that Welltower has not done anything wrong.

They engaged in normal responsible business that struggled as a result of the pandemic which they along with everyone else did not see coming.

Thus, the magnitude of damage potential is quite limited. It is not a systemic problem with how Welltower works, but rather a challenge with the financial strength of a particular operator.

So, worst case scenario is they fail to find new operators and eventually ProMedica is unable to pay rent. Maybe rent gets renegotiated lower or perhaps the properties get sold at a moderate loss.

Depending on how well skilled nursing operations broadly recover, it is a range of outcomes from a slight gain in NOI to a loss of maybe 5% of NOI if there is an unfavorable renegotiation in a rough environment.

That is far from a doom and gloom outcome and easily handled by a company like Welltower with a strong balance sheet.

With all that in mind, I hope we can move forward simply ignoring the fear mongering of the short and distort attack.

Valuation of Welltower today

As expressed in my May 2022 article I have been quite bearish on WELL due to high valuation and fundamental challenges in the skilled nursing (SNF) and senior housing (SH) verticals. That was about 25% higher market price so I think it is worth re-evaluating Welltower at its now lower price point.

Unlike most REITs which have contractual income, Welltower has a large portion of its revenues in SHOP or Senior Housing Operating Portfolio. As such, its revenues tend to be more cyclical in nature which means FFO and AFFO can swing fairly rapidly.

So while Welltower’s 21X AFFO multiple looks extremely high relative to the rest of the sector, it might just be high due to trough earnings.

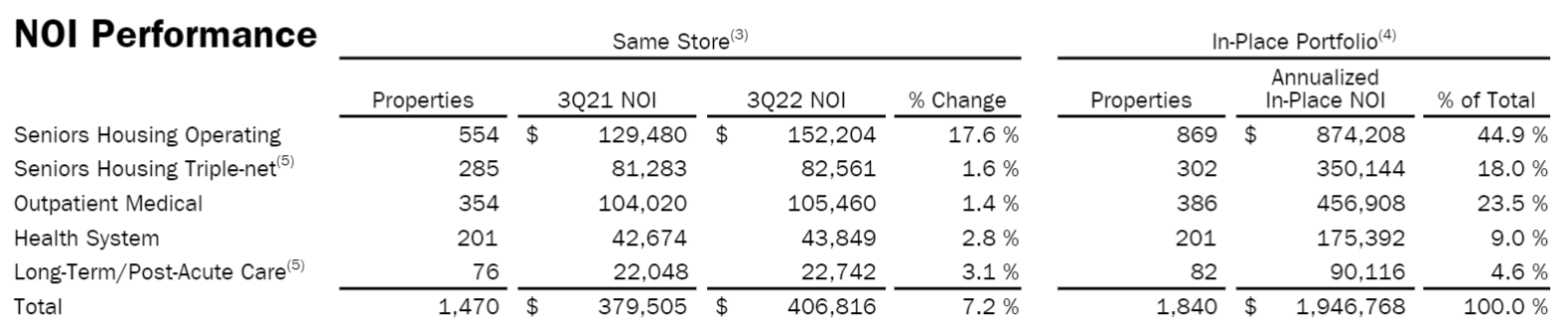

As the pandemic subsides and move-ins resume, WELL’s SHOP segment has been recovering nicely with a 17.6% increase in same store NOI in 3Q22 compared to 3Q21.

Supplemental

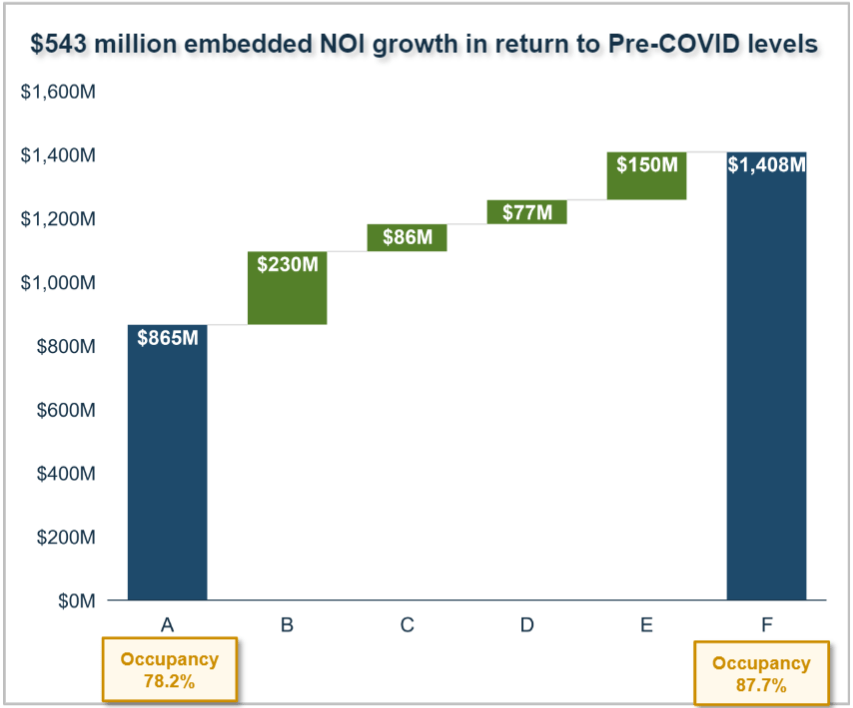

Recovery to pre-pandemic occupancy levels would result in about 60% NOI growth for the segment.

WELL

If that happens, I think Welltower is a legitimate investment. WELL’s currently high multiple is appropriate for that sort of growth trajectory.

I am moving to a neutral stance on Welltower

The reason I am not yet bullish is because I am still not convinced that the occupancy recovery is a near-term event.

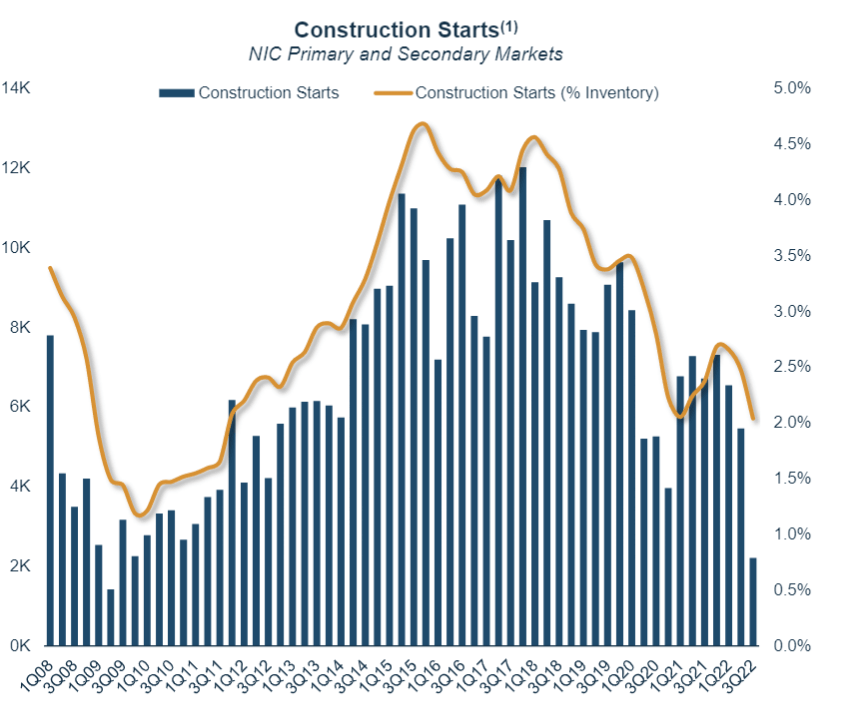

Development in senior housing has been out of control for a decade with 2% to 4% of existing inventory getting delivered each year.

WELL

As financing costs rose in 2022, the supply picture has come back in check, but I think it will be a while before demand fully catches up to supply.

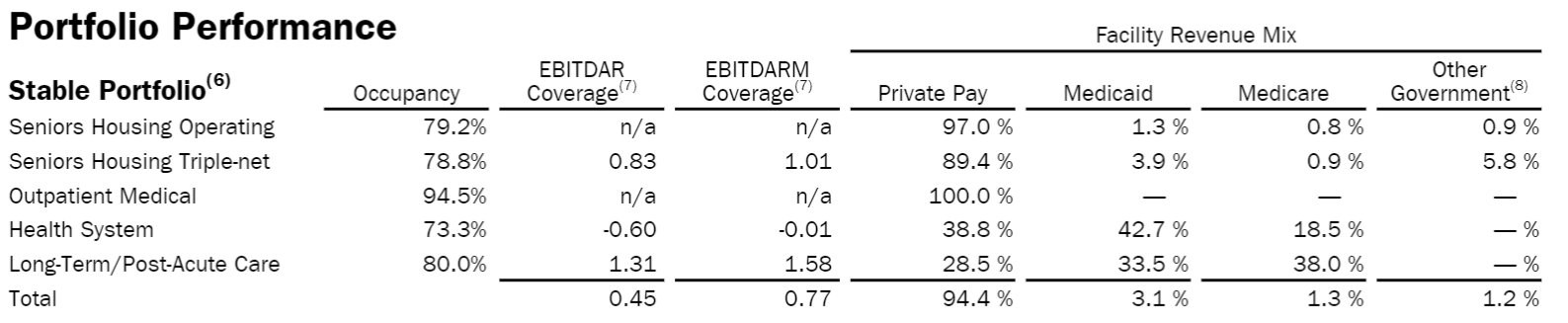

I also remain on the sidelines because WELL’s tenant EBITDAR coverage ratios remain extremely low.

WELL

This is lagged data and I think the coverage is significantly better now than it was for the measurement period, but it does show how fragile the environment is. Anything from another wave of COVID to adverse healthcare legislation could result in more tenant troubles since there is not a buffer in tenant EBITDAR coverage of rent.

I still believe the higher EBITDAR coverage healthcare REITs offer similar upside with substantially less risk.

The bottom line

Welltower is a good company operating in a challenging environment. Its reduced market price appears to be in the right ballpark to reflect the risk and reward of investment.

Be the first to comment