LeoPatrizi

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on January 7th.

Real Estate Weekly Outlook

U.S. equity markets rallied on the first week of the new year after employment data showed strong job growth in December alongside a cooldown in wage pressures, renewing hopes of a ‘soft landing.’ Following a dismal year in which essentially every major U.S. stock and bond benchmark recorded its worst annual returns since the Great Financial Crisis, the seemingly ‘Goldilocks’ slate of employment and PMI data showing continued signs of moderating inflationary pressures sparked a broad-based rally across financial assets.

Hoya Capital

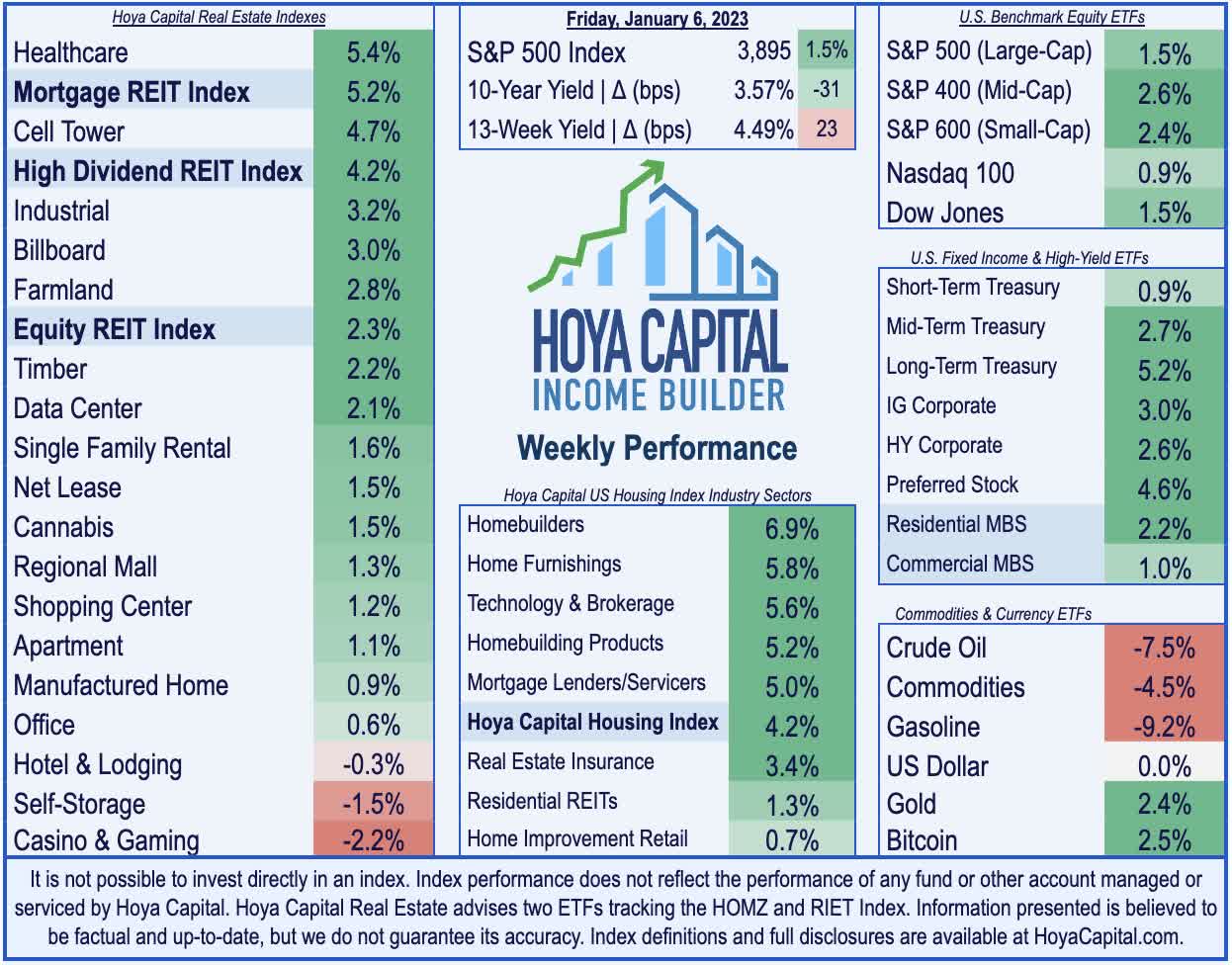

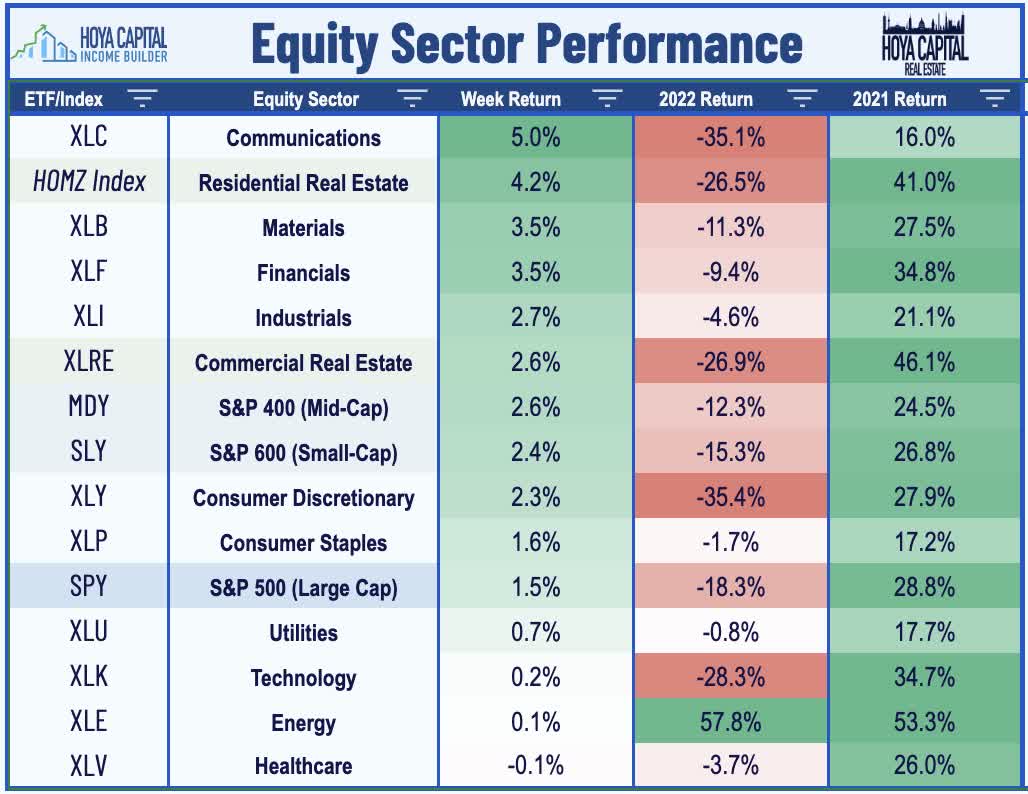

After posting declines of nearly 20% in 2022, the S&P 500 advanced 1.5% on the week – snapping a three-week skid – while the domestic-focused Mid-Cap 400 and Small-Cap 600 each posted gains of roughly 2.5%. The tech-heavy Nasdaq 100 advanced 0.9%, a modest rebound after shedding nearly a third of its value in 2022. Moderating rate pressures can’t come soon enough for the yield-sensitive real estate sector, which led the gains this week after a particularly rough year in 2022. The Equity REIT Index advanced 2.3% this week with 15-of-18 property sectors in positive territory while the Mortgage REIT Index rallied 5.2%. Homebuilders and the broader Hoya Capital Housing Index – companies that have been impacted the most by aggressive monetary tightening in 2022 – were particularly strong performers this week.

Hoya Capital

Evidence suggesting a possible path to a ‘soft landing’ – a course that appeared unlikely in late 2022 given the persistence of inflationary pressures – sparked a broad-based bid for bonds across the credit and maturity curve with the 10-Year Treasury Yield (US10Y) dipping over 30 basis points on the week while the policy-sensitive 2-Year Treasury Yield (US2Y) plunged nearly 20 basis points on the week, reflecting expectations of a less-aggressive monetary tightening course if inflation data continues to trend favorably. Soft global manufacturing data and hopes of easing geopolitical tensions sent Crude Oil prices sharply lower on the week – relinquishing their late-December gains and returning to near-one-year lows. Ten of the eleven GICS equity sectors finished higher on the week – reversing the patterns from 2022 in which all but one sector – Energy (XLE) – finished lower for the year.

Hoya Capital

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

Hoya Capital

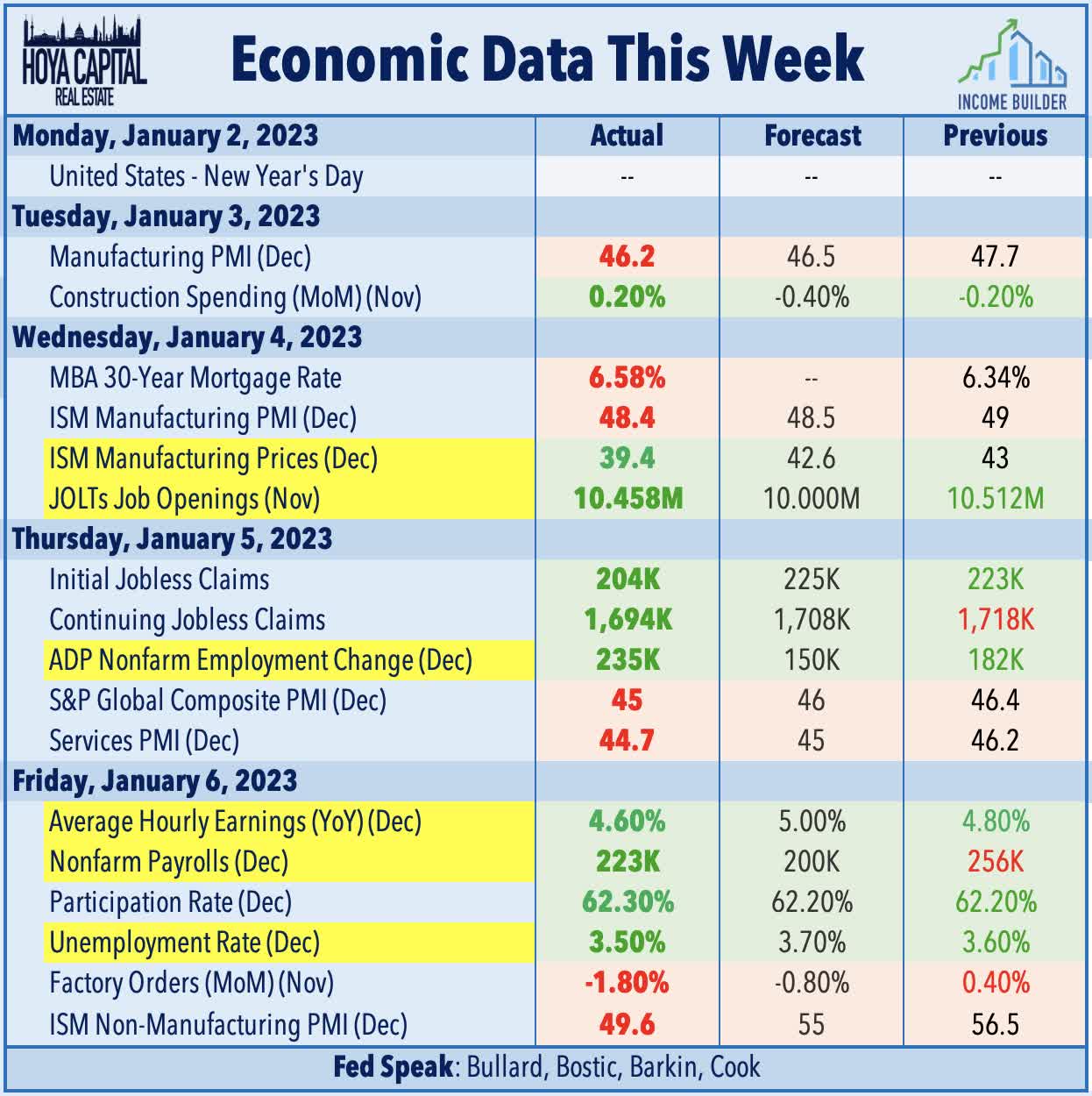

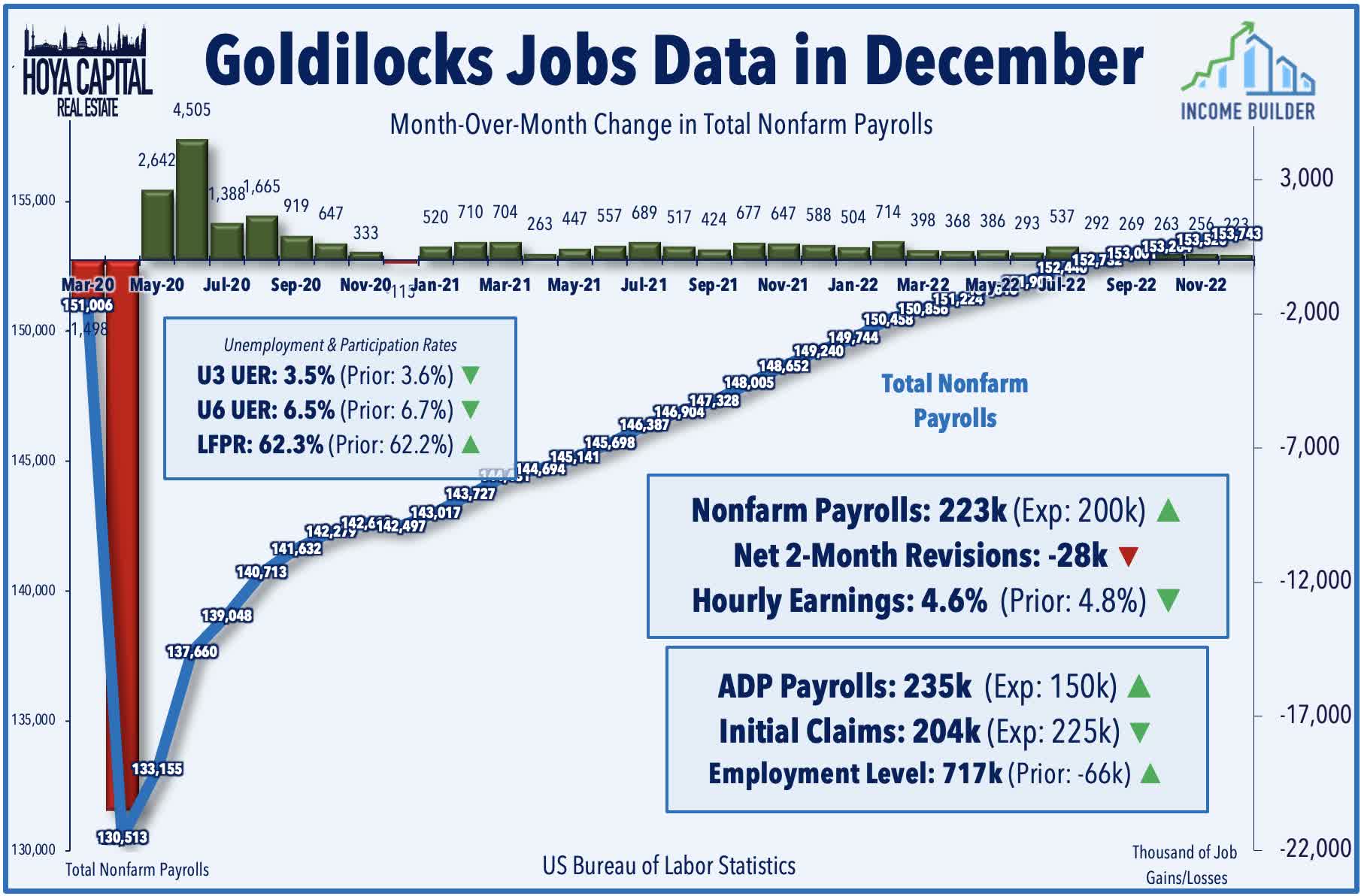

The Bureau of Labor Statistics reported this week that the U.S. economy added 223k jobs in December – the slowest pace of hiring since December 2020 but still above expectations of roughly 200k – a relatively solid report given the continued trickle of corporate layoff announcements in recent weeks including Amazon’s (AMZN) plans to lay off more than 18,000 employees. Job growth was relatively broad-based in the latest NFP report led by gains in leisure and hospitality, health care, construction, and social assistance. ADP data earlier in the week was similarly solid with private payrolls expanding by 235,000 in December – ahead of consensus estimates of 150k – and accelerating from the 182k jobs added in November. Notably, ADP reported that large companies (500+ employees) shed 151k jobs for the month, but relatively strong hiring among small and mid-sized businesses – particularly in the services sectors – more-than-offset these corporate layoffs.

Hoya Capital

The BLS’ household survey – which is used to calculate the unemployment and labor force participation figures – showed that the employment level rose by 717k in December, a notable rebound after posting two-straight months of job losses in October and November. An encouraging rebound in the labor force participation rate came alongside a decline in the headline unemployment rate to just 3.5% – matching the five-decade lows set in late 2019. The most relevant inflation-related metric in determining the path of Fed policy – Average Hourly Earnings – rose at the slowest annual pace since August 2021 at 4.6% while the prior month was also revised downward, providing evidence that a cooldown in inflationary pressures may not require a further intensification of monetary tightening. The Fed is widely expected to raise rates by 25 basis points at its upcoming meeting on February 1st, bringing the benchmark rate to an upper bound of 4.75%.

Hoya Capital

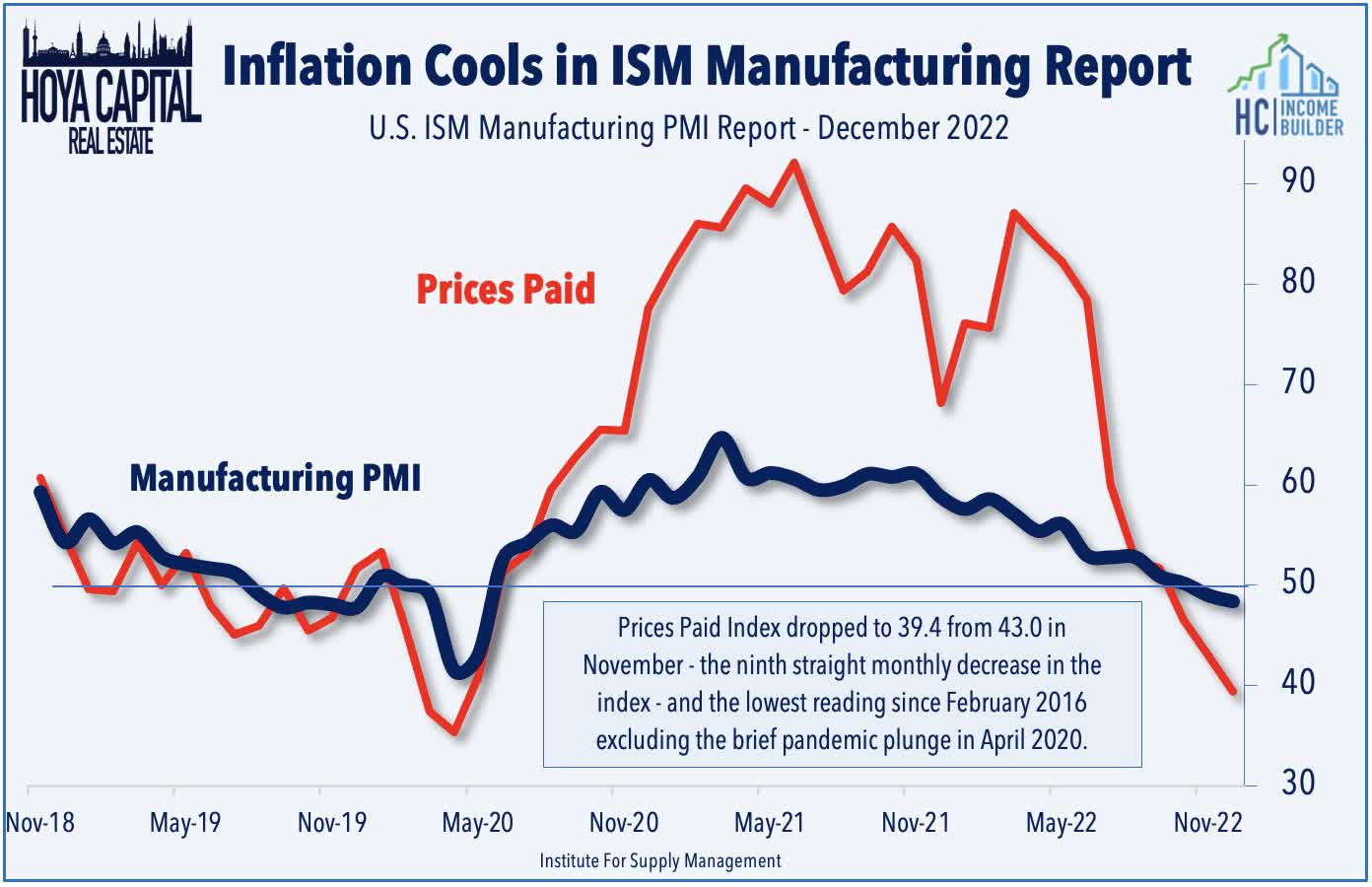

We saw other encouraging news on the inflation front this week as ISM manufacturing data showed that prices paid by factories declined to the lowest level in nearly three years in December. The ISM’s measure of prices paid dropped to 39.4 from 43.0 in November – the ninth straight monthly decrease in the index – and the lowest reading since February 2016 excluding the brief pandemic plunge in April 2020. Whether or not goods-related inflation will carry through to services inflation remains the key question and will be a focus of the CPI report in the week ahead. The headline CPI is expected to moderate to a 6.5% year-over-year rate while the Core CPI is expected to decelerate to 5.7%. As with recent months, the metric we’re watching most closely is the CPI-ex-Shelter Index – which since July has averaged a -1.9% annualized rate – among the most deflationary five-month periods on record.

Hoya Capital

Equity REIT Week In Review

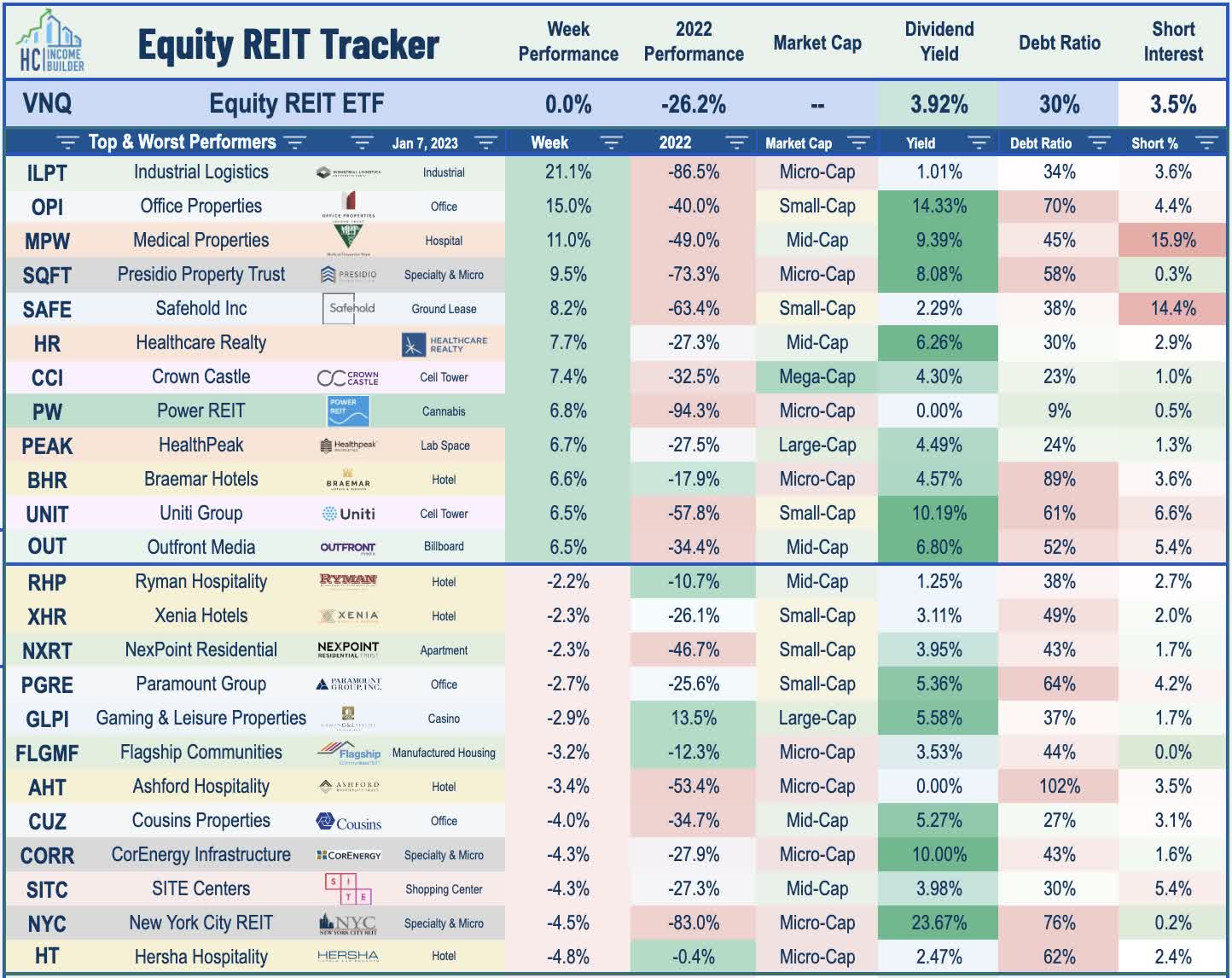

Best & Worst Performance This Week Across the REIT Sector

Hoya Capital

Asset management firm Blackstone (BX) remained in the spotlight this week after it announced that it received a $4B cash infusion from the University of California for its privately-traded real estate fund BREIT, which was forced in December to limit investor redemptions after receiving a wave of withdrawals that exceeded its monthly and quarterly limits. The strategic venture – which UC called “opportunistic” – includes a two-part deal in which UC Investments will acquire $4B of BREIT stock in exchange for a guaranteed minimum annualized net return of 11.25% over the six-year holding period of its investment via a $1B backstop by parent company Blackstone. The deal comes as investors seek to redeem shares at BREIT’s published Net Asset Values that we estimate are at least 25% above comparable public REIT valuations.

Hoya Capital

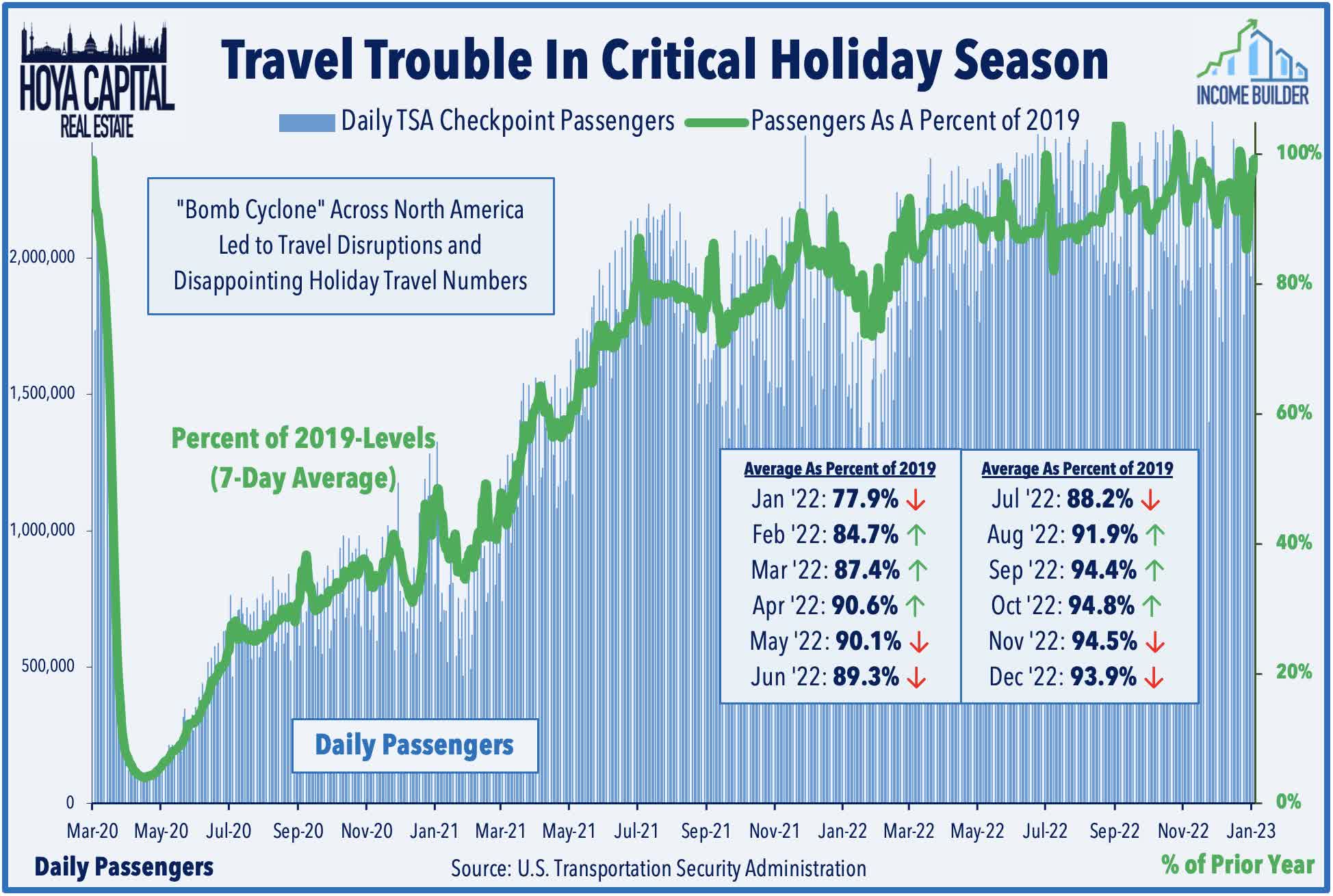

Hotels: Resort owner Braemar Hotels (BHR) was among the leaders this week, surging nearly 7% after it announced preliminary fourth-quarter results showing that its Revenue Per Available Room (“RevPAR”) was 20% above the pre-pandemic comparable levels from 2019. Encouragingly, December was a particularly strong month for BHR with comparable RevPAR increasing 26% over 2019 levels, up from the 15% increase in November and the 14% increase in December. Ashford Hospitality (AHT) – which owns upper-scale full-service hotels with more exposure to business travel – was among the laggards this week after it reported that its fourth-quarter RevPAR was still 1% below comparable 2019 levels. Updated TSA checkpoint data this week showed that, after disruption from the “Bomb Cyclone” during the Christmas holiday, passenger throughput finished the holiday season relatively strong with the 30-Day average hovering around 99% of pre-pandemic levels.

Hoya Capital

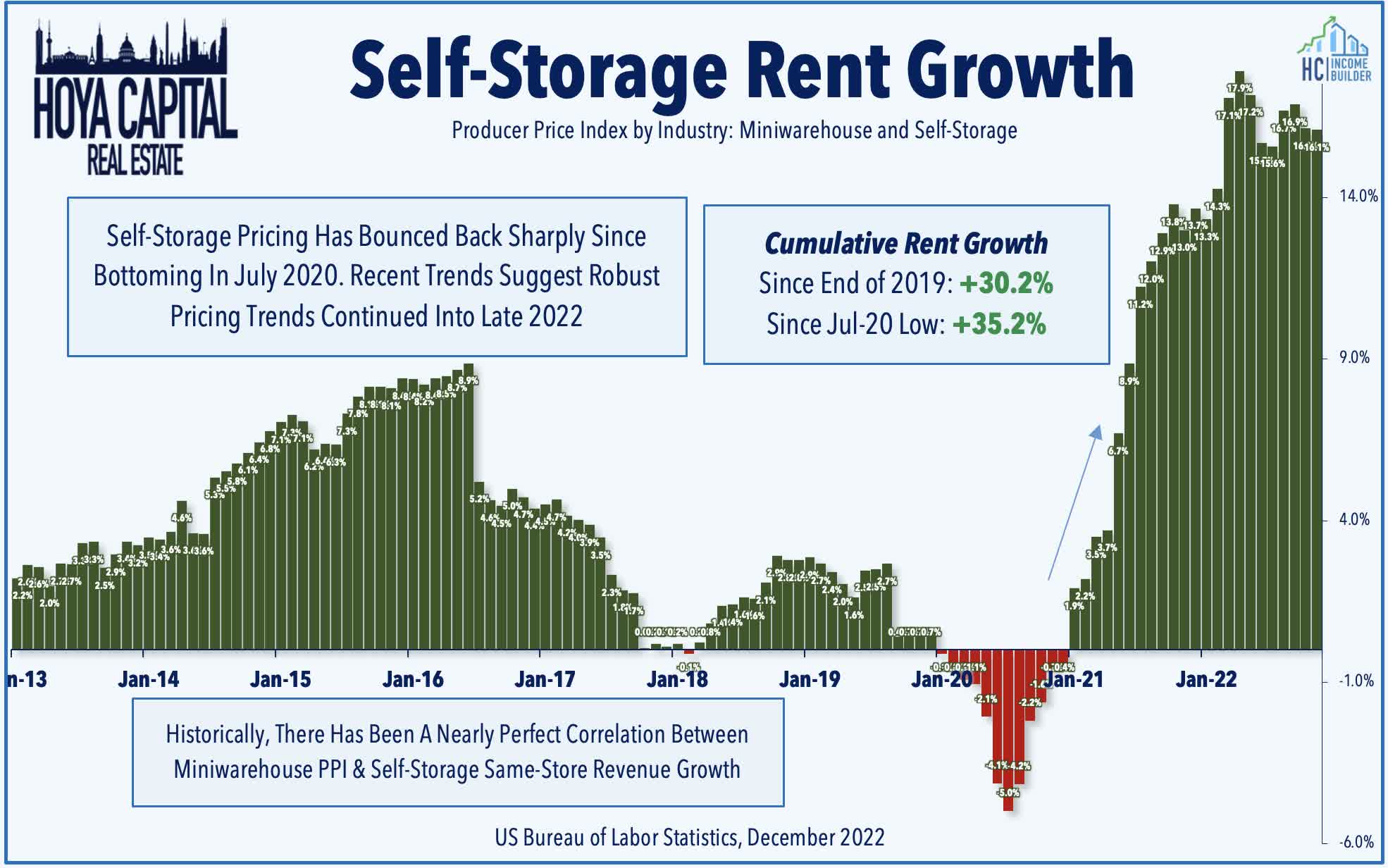

Storage: After more than 125 REITs raised their dividends in 2022, it didn’t take long to see the first REIT dividend hike of 2023. Life Storage (LSI) – which hiked its dividend twice last year – boosted its quarterly payout by 11.1% to $1.20/share. National Storage (NSA) – which we own the REIT Focused Income Portfolio – advanced 1% for the week after it announced that it expanded the total borrowing capacity of its credit facility by $405M to $1.955 billion with an accordion feature to expand the total borrowing capacity to $2.5 billion. In Storage REITs: Locked-In And Sticky we noted that storage REITs have defied expectations to the upside as comprehensively as any real estate sector since the start of the pandemic, delivering earnings growth of over 50% since 2019, but the sharp cooldown in housing market turnover – a driver of self-storage demand – has slowed the demand momentum.

Hoya Capital

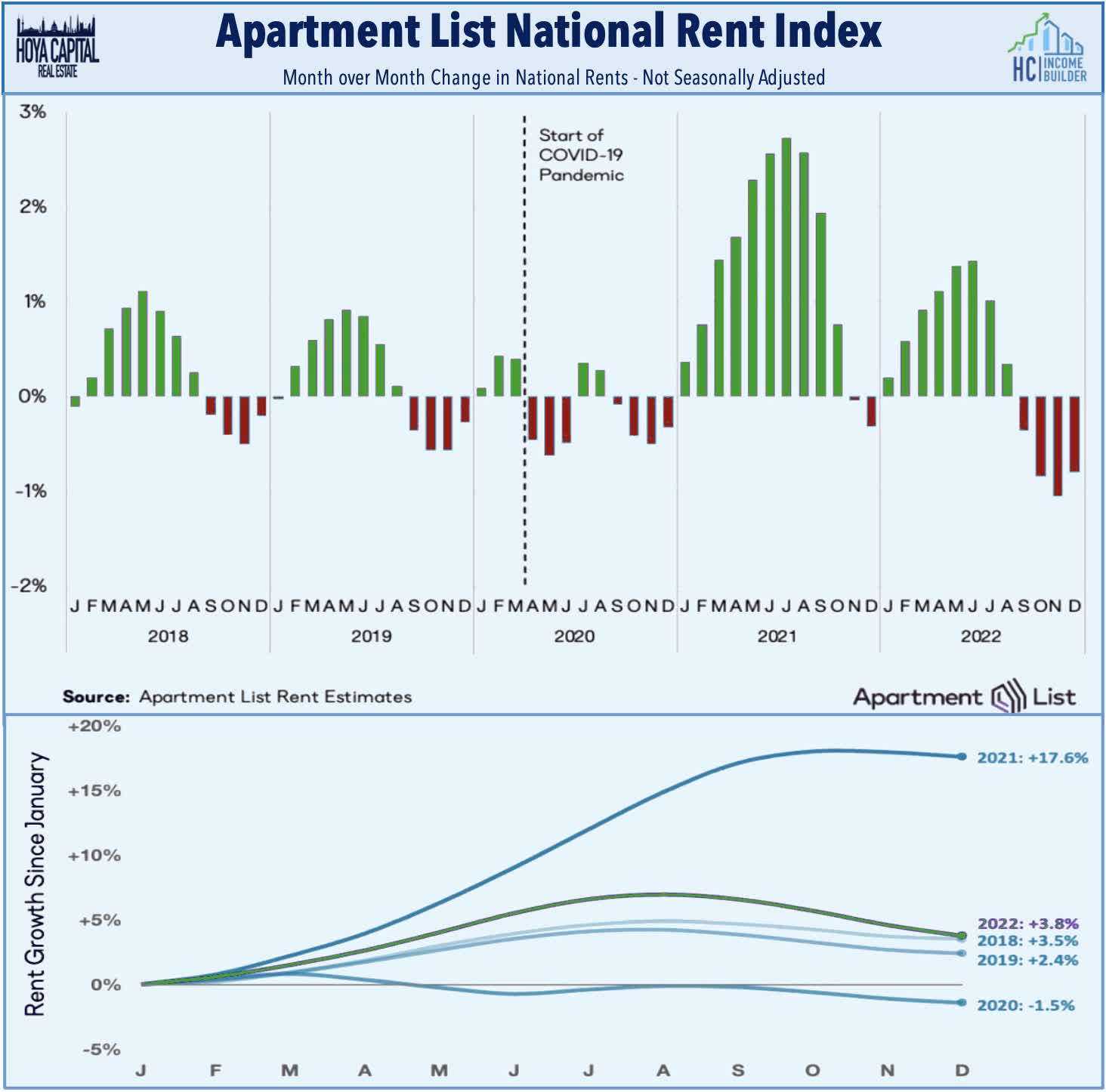

Apartments: Residential REITs were in focus this week after data from Apartment List showed that multifamily rents continued to decline in December – continuing a trend of moderation since peaking at double-digit annual percentage increases in mid-2022. Apartment List’s national index fell by 0.8% over the course of December, marking the fourth straight month-over-month decline. The firm commented that “the timing of this cooldown in the rental market is consistent with the typical seasonal trend, but its magnitude has been notably sharper than what we’ve seen in the past.” For the full-year, national median rent increased by a total of 3.8% – a notably sharp slowdown from the 17.6% surge in rents that we saw in 2021. Rent growth in 2022 still ranked as the second fastest year in Apartment Lists’ records. Rents decreased in December in 90 of the nation’s 100 largest cities with New York City recording the nation’s sharpest monthly decline.

Hoya Capital

Shopping Center: Retail REITs were also in focus this week after Bed Bath & Beyond (BBBY) issued a “going concern” disclosure warning of a potentially looming bankruptcy. The home goods retailer – which has undergone a series of strategic transformations in recent years – had seen a mild revival during the housing market boom in 2020 and 2021 but the outlook has dimmed alongside the broader moderation in home-related spending. The potential bankruptcy comes after the best year on record for net store openings. REITs with the highest exposure to Bed Bath & Beyond include Acadia Realty (AKR), RPT Realty (RPT), and SITE Centers (SITC) which each derive about 2% of their annualized base rents from the company. Acadia Realty also reported this week that it expects to recognize its share of the special dividend related to Albertsons (ACI) pending merger with Kroger (KR) in 2023 instead of 2022 as initially anticipated, therefore reducing its full-year 2022 guidance to $1.17-1.19/share from $1.28-$1.30/share.

Hoya Capital

Healthcare: Senior Housing REIT Welltower (WELL) gained over 6% this week following the release of the fourth-quarter NIC Map Vision report by the National Investment Center for Seniors Housing. The report showed that senior housing occupancy increased for a sixth-straight quarter to 83% – up 5.2% from the pandemic occupancy low of 77.8% in 2Q21 – but still below the pre-pandemic levels of roughly 90%. Despite the reduced occupancy levels, SH operators have exhibited strong pricing power with annual rent growth climbing to 4.9% in Q4 – the largest increase on record. Higher demand and slower inventory growth were consistent trends throughout 2022 with NIC noting that just 11,000 units were added within NIC MAP Primary Markets last year, the weakest inventory growth since 2014. Meanwhile, Healthcare Realty (HR) gained more than 7% after announcing $1.14 billion of asset sales and joint venture contributions since July 2022 at a 4.86% cap rate generating net proceeds of $1.03 billion. Elsewhere, LTC Properties (LTC) announced a $128M deal to buy 12 assisted living/memory care properties in North Carolina while CareTrust (CTRE) announced that it has completed the $13M sale of five senior housing facilities in Virginia.

Hoya Capital

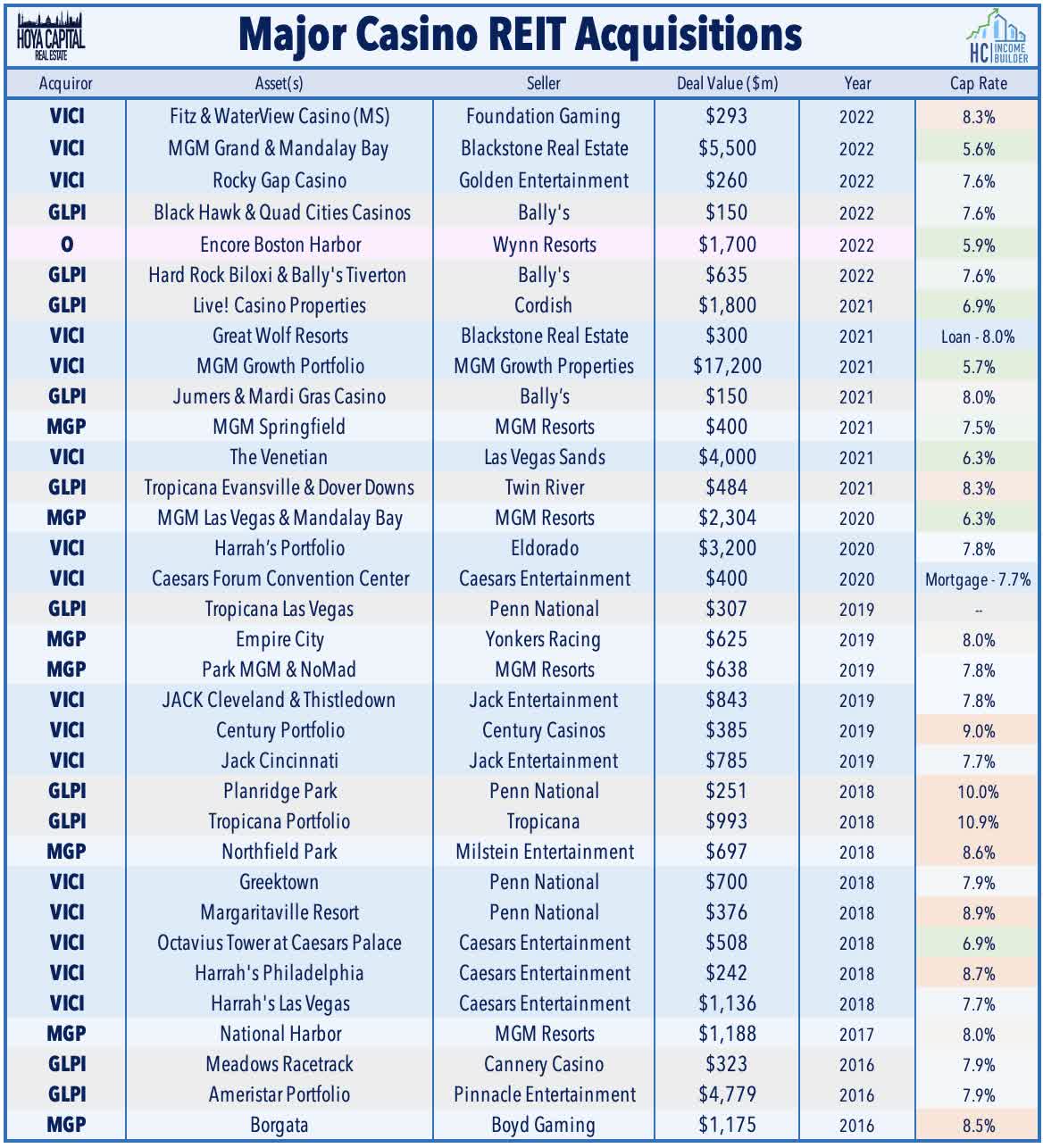

Casino: The lone property sector in positive-territory last year was the laggard on the first week of 2023. Gaming and Leisure Properties (GLPI) announced this week that it completed its previously announced $635M of two casino properties from Bally’s (BALY) – Bally’s Tiverton Casino in Rhode Island and Bally’s Hard Rock Hotel & Casino Biloxi in Mississippi. These properties were added to the Company’s existing Master Lease with Bally’s. The initial rent for the lease was increased by $48.5 million on an annual basis, subject to contractual escalations based on the CPI with a 1% floor and 2% ceiling. The Master Lease has an initial term of 15 years (with 14 years remaining) followed by four five-year renewals at the tenant’s option. GLPI continues to have the option, subject to receipt by Bally’s of required consents, to acquire the real property assets of Bally’s Twin River Lincoln Casino Resort in Lincoln, RI prior to December 31, 2024 for a purchase price of $771M.

Hoya Capital

Industrial: M&A was also a theme in the industrial space this week. Rexford (REXR) gained 3% on the week after it announced the acquisition of ten industrial properties for $336.2M which were funded using a combination of cash on hand and proceeds from forward equity settlements. Plymouth (PLYM) gained about 2% this week after it announced fourth-quarter leasing volume totaled 2.3M square feet and achieved an 18.1% blended cash rental rate spread – up from the 17.6% increase in spreads that it reported in the third quarter. Industrial REITs were one of the weakest-performing property sectors last year despite the robust strength exhibited in property-level fundamentals with average cash leasing spreads rising at a record-high rate of 38.5% in the third quarter.

Hoya Capital

Net Lease: A handful of net lease REITs also provided business updates this week. Agree Realty (ADC) finished flat this week after it announced that acquisition volume for the fourth quarter totaled $404.9 million at a weighted-average capitalization rate of 6.4% and had a weighted average remaining lease term of 10.6 years. Gladstone Commercial (GOOD) gained about 2% after it announced a business update commenting that 100% of Q4 2022 cash base rents have been paid and collected while portfolio occupancy is at 96.8%. CTO Realty (CTO) declined about 1% after it announced full-year acquisition totals of $314M at a weighted-average going-in cash cap rate of 7.5% while its full-year disposition volume totaled $81.1M at a weighted average exit cap rate of 6.2%. Alpine Income (PINE) finished flat this week after announcing that it acquired $187M in properties during 2022 – slightly above its most recent full-year guidance at $180M – at a weighted-average cap rate of 7.1%. PINE sold $155M of properties in 2022 – slightly below its guidance target – at a weighted average exit cap rate of 6.5%.

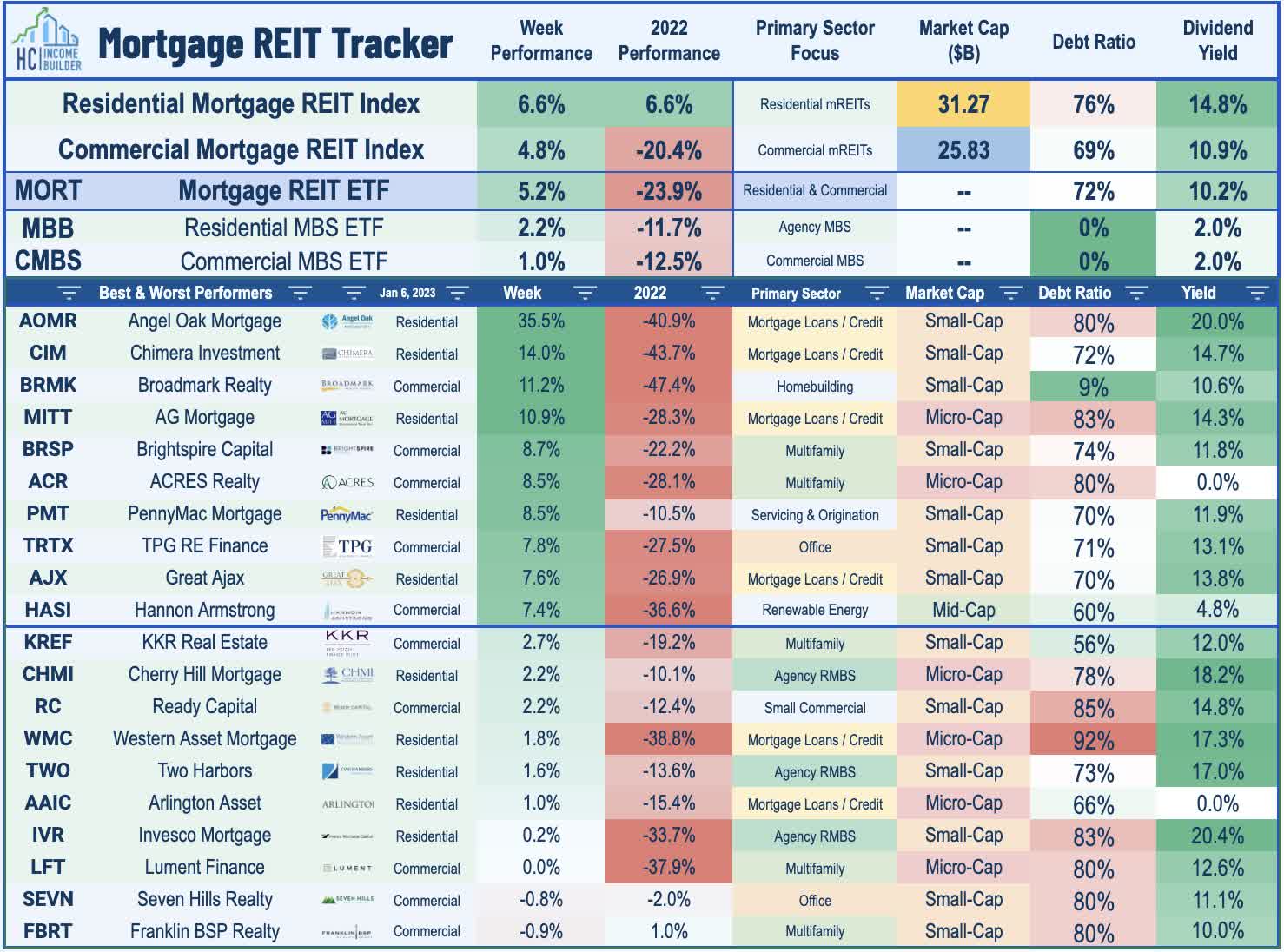

Mortgage REIT Week In Review

Following a sharp sell-off in the final week of 2022, mortgage REITs were broadly higher on the first week of 2023 with the iShares Mortgage Real Estate Capped ETF (REM) advancing 5.2% led by double-digit gains in a handful of the most beaten-down names including Angel Oak Mortgage (AOMR) and Chimera Investment (CIM). On an otherwise quiet week of newsflow in the mREIT space, Broadmark Realty (BRMK) was also sharply higher this week despite announcing that its NYSE-listed warrants (BRMK.WS) – representing a 1/4 interest in BRMK – will be delisted from the exchange due to their low selling price. Hannon Armstrong (HASI) was also among the leaders this week after it closed two new investments in grid-connected renewable energy assets operated by AES Corp. HASI will acquire a 49% equity interest in a 1.3 GW portfolio of 18 operating solar and wind projects located across six states: Arizona, California, New York, South Dakota, Utah, and Virginia.

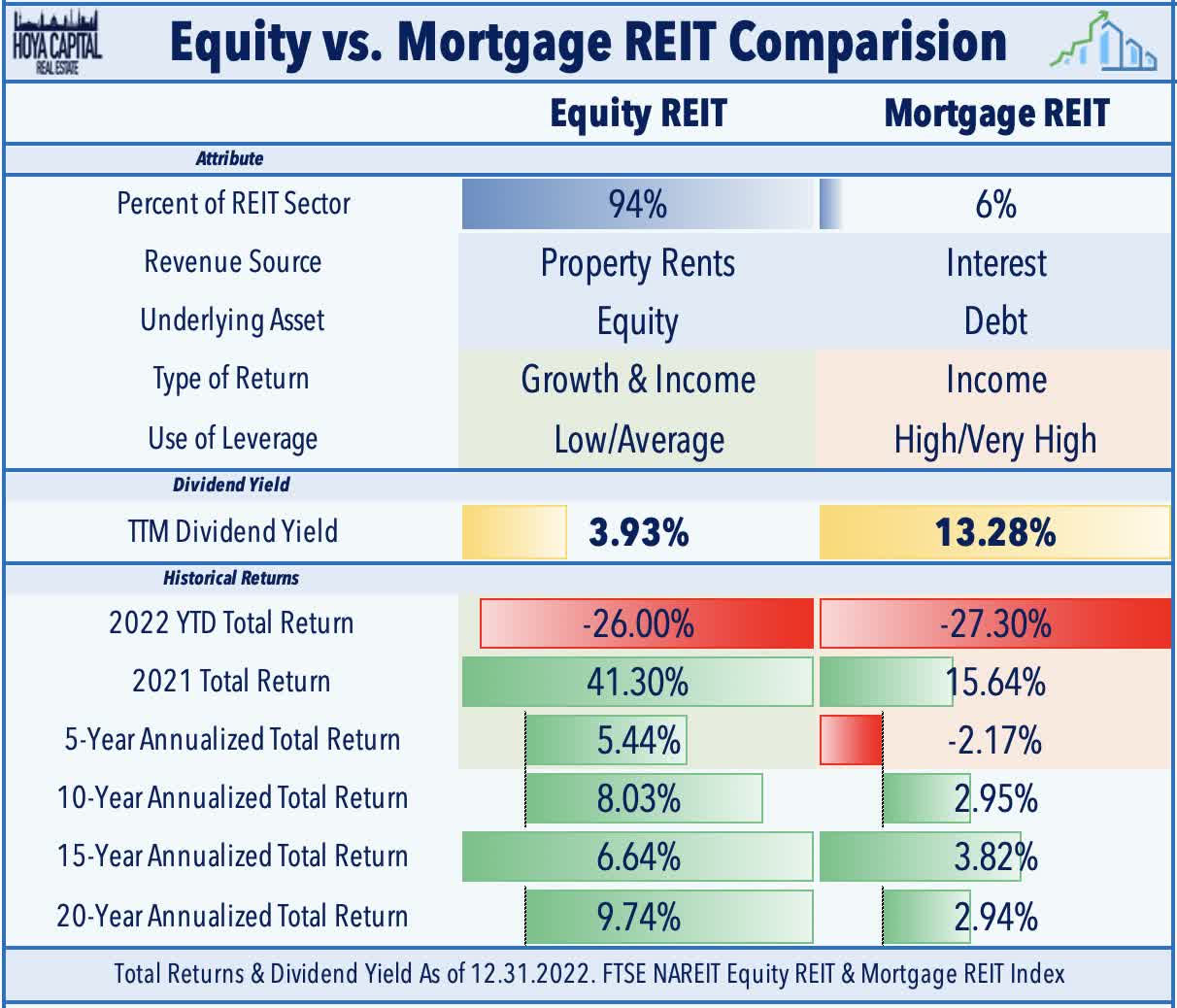

For the year, the mortgage REIT and equity REIT benchmarks each delivered their worst year of performance since 2008, but produced notably similar total returns at -27.3% and -26.0%, respectively, which was the narrowest performance spread on record for the two real estate indexes. Last month, we published Mortgage REITs: High Yields Are Fine, For Now, which noted that despite paying average dividend yields in the mid-teens, the majority of mREITs have been able to cover their dividends, but we flagged a handful of mREITs with payout ratios above 100% of EPS.

REIT Capital Raising & REIT Preferreds

Buoyed by the dip in benchmark interest rates, the REIT Preferred Index (PFFR) advanced 2.6% this week while the broader iShares Preferred and Income Securities ETF (PFF) advanced more than 4% on the week. The solid start to 2023, however, comes after the worst year since 2008 for the REIT Preferred stocks with total returns of -23.89%. Notable movers on the upside this week included the preferreds of mortgage REITs Arbor Realty (ABR), Chimera (CIM), KKR Real Estate (KREF), office REIT Hudson Pacific (HPP), and shopping center REITs Kimco (KIM) and Saul Centers (BFS). REIT Preferreds continue to trade at very attractive valuations, in our view, with an average current yield of roughly 7.5% while trading at a 20% discount to par value.

Hoya Capital

A handful of REITs announced amended credit facilities this week. Realty Income (O) announced a new $1.0B multicurrency unsecured term loan which matures in January 2024 and includes two twelve-month extensions alongside an interest rate swap agreement that fixes its annual interest rate at 5.0%. Host Hotels (HST) extended the maturity on its $2.5B credit facility from January 2025 to January 2028. Sabra Health Care (SBRA) added a pair of six-month extension options to its $1.0B credit facility maturing in January 2027 which includes an accordion feature that expands the total borrowing capacity to $2.75B. American Assets (AAT) increased the borrowing capacity on its credit facility from $150M to $225M while extending the maturity date from March 2023 to January 2025. On the credit ratings front, Fitch Ratings assigned a “BBB-“ rating to Getty Realty’s (GTY) senior unsecured notes (Series O, P, and Q) with a stable outlook while Fitch also affirmed its “BB” credit rating on Necessity Retail (RTL) with a stable outlook.

Hoya Capital

2022 Performance Recap

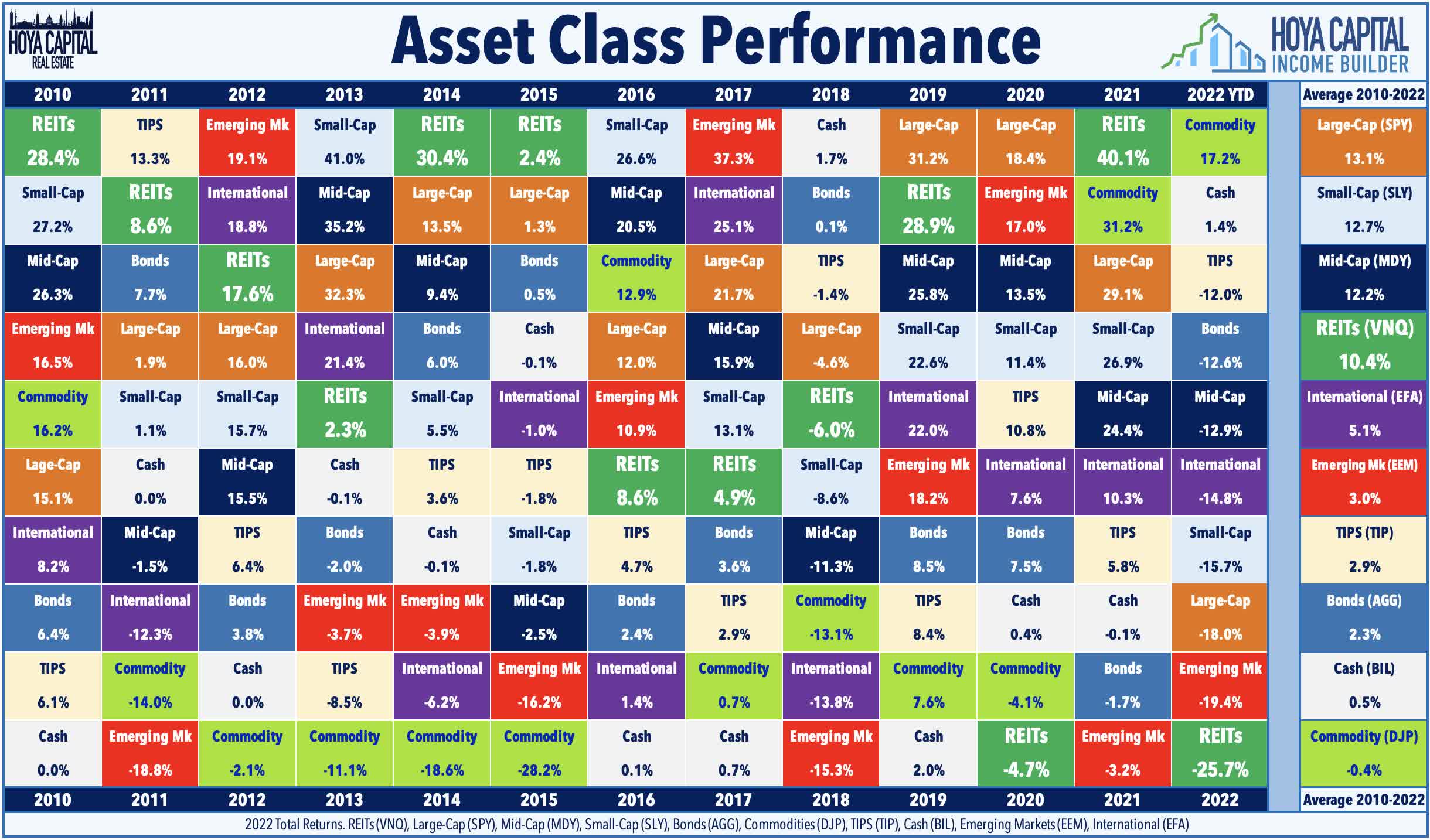

Good riddance, 2022. There were few places to hide across financial markets in a historically brutal year for investors that wiped out nearly a fifth of global financial wealth. The typically-steady US bond market delivered its worst year in history with a loss of 13.01% on the Bloomberg US Aggregate Bond Index, which is over 4x larger than the previous worst year back in 1994 (-2.9%). At 3.88%, the 10-Year Treasury Yield surged 237 basis points since the start of the year. Among the ten major asset classes, Commodities (DJP) were the only segment to see positive inflation-adjusted returns for the year. Fittingly on a year defined by performance reversions, the commodities complex is still the weakest-performing asset class since the start of 2010.

Economic Calendar In The Week Ahead

It’ll be another busy week of economic data with the main event coming on Thursday with the Consumer Price Index for December, which investors and the Fed are hoping will show that the fastest pace of year-over-year increases in inflation is finally behind us. The headline CPI is expected to moderate to a 6.5% year-over-year rate while the Core CPI is expected to decelerate to 5.7%. As with recent months, the metric we’re watching most closely is the CPI-ex-Shelter Index – which since July has averaged a -1.9% annualized rate – among the most deflationary five-month periods on record. Critically, gasoline prices averaged $3.21 nationally in December – down about 13% from the prior month and 3% from the prior year. We’ll also get our first look at Michigan Consumer Sentiment data on Friday – which includes a closely-watched consumer inflation expectations survey – and we’ll be closely watching Jobless Claims data on Thursday as well.

Hoya Capital

For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports: Apartments, Homebuilders, Manufactured Housing, Student Housing, Single-Family Rentals, Cell Towers, Casinos, Industrial, Data Center, Malls, Healthcare, Net Lease, Shopping Centers, Hotels, Billboards, Office, Farmland, Storage, Timber, Mortgage, and Cannabis.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital

Be the first to comment