seb_ra/iStock via Getty Images

Investment Thesis

Weis Markets, Inc. (NYSE:WMK) had a great run during 2020. However, the situation looks different now. With revenue and profit growth year-on-year plateauing, the firm needs a catalyst to rise back. Since consumer food retail is a defensive sector, the effects of a recession might be less compared to S&P 500. However, keeping in mind how competitive the sector is, any bad move might get them out of the business. The firm has hinted at a pending partnership with Instacart. The firm’s farm-fresh produce strategy aligned with Instacart’s same-day delivery might help boost the top-line performance of the firm.

What they do

Weis Markets, Inc. is an American grocery store with over a hundred years of experience in the consumer staples sector. This Pennsylvania headquartered food-retailer operates more than 200 stores with a growing presence in the mid-Atlantic region. The firm operates in four business segments with a major share of the revenue from groceries.

With around 35% of the shares held by institutional investors, several ETFs and mutual funds hold major positions in WMK. Some of its major competitors include Grocery Outlet Holding Corp., Sprouts Farmers Market, Inc., Companhia Brasileira de Distribuicao, and Marks and Spencer Group plc.

Recent Corporate Performance

Weis Markets, Inc. has a great business strategy. Apart from countries around the world, Weis Markets sources its farm produce locally from the mid-Atlantic region it operates. This way the firm can conserve a lot of unavoidable transportation costs. It helps the firm in two ways. First, it provides customers with farm-fresh produce and does so at a cheaper price. However defensive the sector is to economic threats such as recession, switching costs among the retailers are negligible. To compete with established national chains in the industry, every step towards cost conservation will highly benefit the firm.

Looking at the recent financial performance of WMK, the top-line and bottom-line performances on the income statement are cyclical, and currently, they plateaued. With year-on-year growth in revenues ranging from 1%-14%. Due to these revenue fluctuations, there is a direct effect on the year-on-year growth in net income ranging from negative 45% to positive 75%. As is with most of its competitors, the profit margins are steady and low.

Strengths

With large market players in the sector venturing into online, same-day grocery delivery, Weis Markets joined the bandwagon. Its partnership with Instacart to produce same-day delivery will benefit Weis Markets as well as its customers. Their farm-fresh orders are just a single tap away. With over 9 million active users using the app, the partnership with Instacart would provide Weis Markets, Inc. with a lot of visibility for its products.

The firm has low liquidity and solvency risks. With a cash ratio (cash to current liabilities) of 1.0, the firm can meet its short-term liabilities with cash on hand. With debt being about a third of its equity, the firm is not highly-leveraged.

Even though the firm performed significantly well during the pandemic, the Cash Flows from Operations are on a downtrend post-pandemic.

Weaknesses

The primary weakness I find with Weis Markets is its limited geographic footprint. With the high competition in the sector, let alone globally, I can never expect the firm to expand to other regions of the United States. Most of its supply chain from supplier to buyer is limited to the mid-Atlantic region.

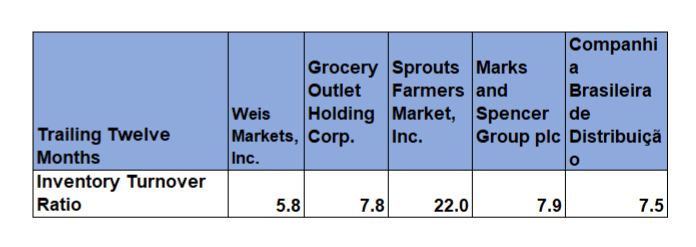

Analyzing a retail-sector stock is never complete until one conducts an analysis of its inventory turnover ratio (ITR). The inventory turnover ratio quantifies how well the firm can convert its inventory into sales. It is given by the cost of goods sold (COGS) to the Average Inventory.

Created by the author using data from company filings (Self)

The firm is improving given its increasing trend in the inventory turnover ratio since 2017. However, ITR should never be analyzed stand-alone.

Created by the author using data from company filings (Self)

Looking at the inventory turnover ratios of comparable firms gives a complete picture. Although it is improving over the past few years, WMK has the lowest ITR among its comparable firms. This implies the firm is less efficient in converting its inventory into sales compared to its peers.

Looking Forward

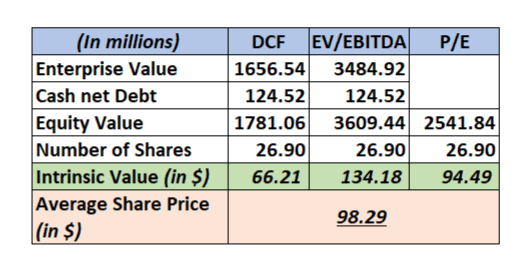

The intrinsic valuations based on DCF (discounted cash flows), EV/EBITDA (enterprise value to EBITDA), and P/E (price to equity) multiples resulted in an average stock price of around $98 vs. the current stock price of $87.

The average EV/EBITDA multiple (based on the peer group) is around 13x compared to 9x of WMK. This shows the firm is overvalued based only on EV/EBITDA multiple. Whereas, the average P/E multiple (based on the peer group) is around 21x compared to 20x, which shows the stock is correctly priced based solely on P/E multiple.

My assumptions for the DCF valuation model are listed below:

-

Cost of Equity: 7.5%

-

Cost of Debt: 2.6%

-

Tax Rate: 22%

-

24-month Forward Beta: 0.47

-

WACC (weighted average cost of capital): 5.7%

Created by the author using data from company filings (Self)

Higher median EV/EBITDA multiples of the comparison firms led to a higher valuation. As high comparable multiples are quite common in the defensive consumer retail sector, I would pay attention to the DCF method of valuation. The DCF valuation gives an intrinsic share price of around $66.

Conclusion

The DCF (discounted cash flows) and the comparable company multiples valuation give contradicting results. The partnership with Instacart to deliver same-day farm-fresh produce might be a good catalyst to boost the firm’s revenue. Yet, I will wait until the next quarterly earnings report to look at how revenues are faring compared to the previous quarter’s revenues. Keeping in mind the cyclical nature of revenue and earnings growth, and the lower inventory turnover ratio compared to that of its peers, I rate the stock a Hold.

Be the first to comment