We have a modest economic calendar. Only two reports will provide any hint about the coronavirus economic impact. The punditry will not be hampered. Without meaningful data, speculation blossoms. There is one idea that could help both your interpretation of data and your investment decisions. We should be emphasizing:

The crucial importance of time frames.

I am going far beyond the common advice of buy-and-hold and ignore what is happening. I hope to show how the choice of time frame affects every aspect of an important time for investors.

Last Week Recap

My last installment of WTWA, I expected little attention to the economic news. Instead, I predicted discussion about the “message of the markets,” and plenty of variation in what that might be. That was an accurate forecast for the week, especially given the many twists and turns. This cartoon from Joel Pett in the Lexington Harold Leader gets the media confusion just right!

Some of the erroneous messages will form the background for our look at the week ahead.

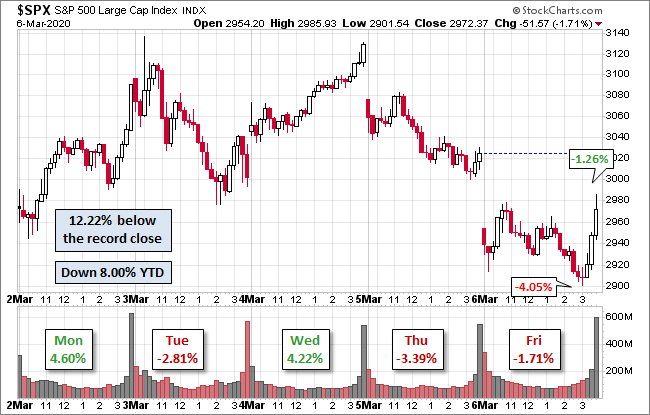

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version, an excellent combination of key variables.

The market gained 0.6% on the week, measuring from the February 28 (last Friday) closing price. There was a gap opening on several days, including Monday. The 0.6% gain would be over 30% for the year if it were the weekly average. For most observers it is lost in the large 8.1% trading range for the week. Tuesday trading was especially noteworthy. It included a spike higher after the surprise Fed rate cut, followed by a dramatic decline and a close near the lows of the day. Once again, we saw a solid and surprising Friday rebound. In times of worldwide risks, traders often are cautious in front of the weekend. You can monitor volatility, implied volatility, and historical comparisons in my weekly Indicator Snapshot in the Quant Corner below.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators are a valuable part of my economic review. His approach divides indicators into three time frames. Currently, the long and short leading indicators are both positive. The nowcast is slightly positive. NDD warns that the coronavirus effects have not yet registered.

The only likely coronavirus impacts so far are intermodal rail loads and possibly the upward spike in new orders, which may represent manufacturers trying to lock in supplies. On the consumer side Redbook consumer spending and on the producer side shipping and rail look like the best and quickest proxies for the impact of a coronavirus panic or pandemic. To be clear, though, I expect the news to outrun even the high frequency indicators.

The Good

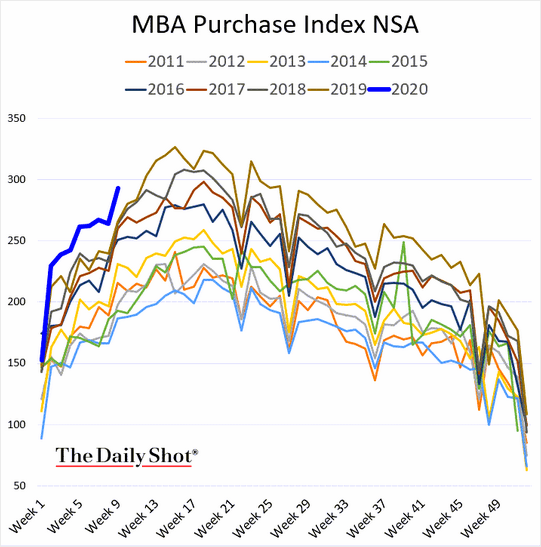

- Mortgage applications increased by 15.1% versus the prior week’s 1.5%. The continued fall in the ten-year note yield is helping affordability.

- Construction spending for January increased 1.8%, beating expectations of 0.7% and December’s 0.2%.

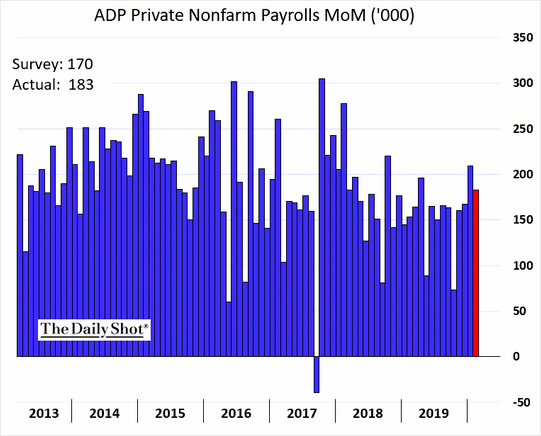

- ADP private employment for February grew 183K, beating expectations of 165K. January had a large downward revision – from 291K to 209K.

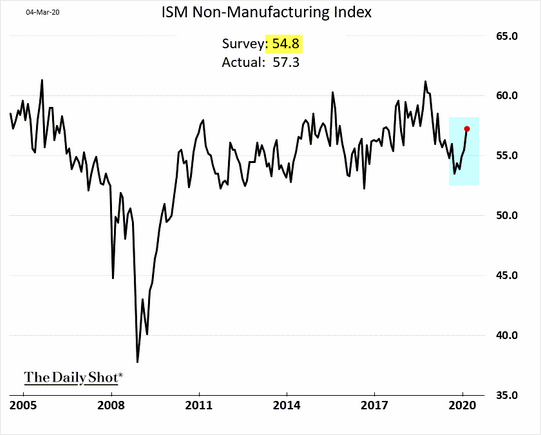

- ISM Non-Manufacturing for February was 57.3 handily topping expectations of 54.8 and January’s 55.5

- Initial jobless claims of 216K was an in-line report. I am scoring it as “good” because it covers the last week of February, two weeks later than the monthly employment report.

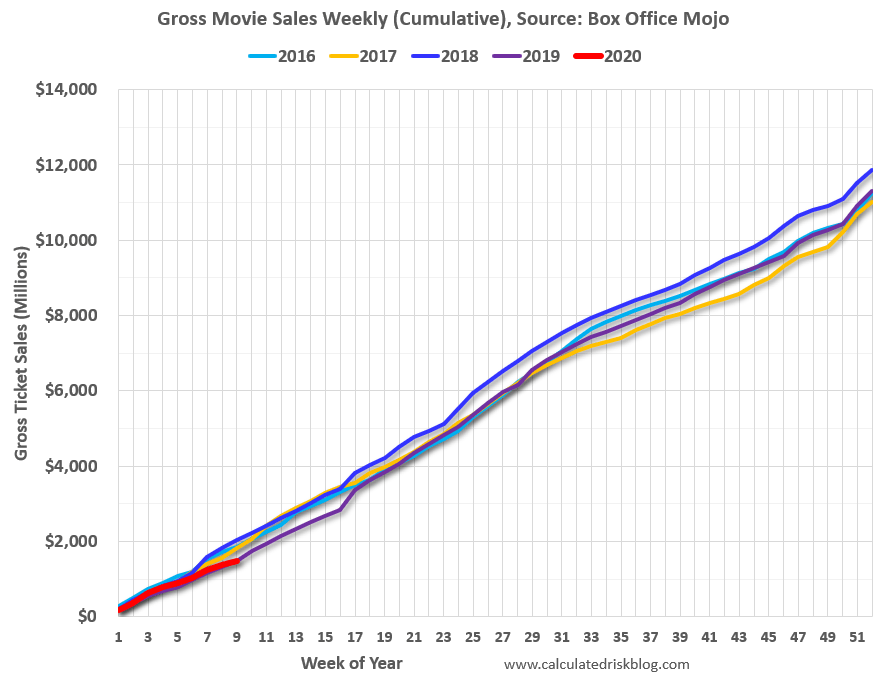

- Movie Box Office reports are also weekly. So far, so good reports Calculated Risk.

- The Employment Situation Report for February was positive. Every discussion pointed out that the reporting period was the middle of February, before any significant coronavirus impact. This report from Barron’s was typical: The February Jobs Report Was Fantastic. Why It Doesn’t Matter for the Market.

- Non-farm jobs had a net increase of 273K, beating expectations of 160K. January was revised upward to 273K from 225K.

- Private payrolls grew by 228K versus expectations of 160K.

- Unemployment dropped to 3.5% without a reduction in labor force participation.

The Bad

- ISM Manufacturing for February registered 50.1, slightly below expectations of 50.3 and lower than January’s 50.9.

- Rail traffic declined at the end of February. Steven Hansen reports a decline of 2.9% in his “intuitive sectors” reflecting the economy. “The big decline this week was intermodal (trucks and containers on flatcars) which accounts for half of the rail traffic.”

- Factory orders for January declined 0.5%, worse than the expected -0.1% and much worse than December’s gain of 1.9%.

- The Fed’s Beige Book described continuing economic expansion and concerns about coronavirus effects. Steven Hansen (GEI) provides analysis of the key points and changes in wording.

The Ugly

More about our dwindling privacy. If you are a California resident, you can see your own report. Let us know in the comments if it is interesting!

Here’s the File Clearview AI Has Been Keeping on Me, and Probably on You Too

An Important Comment on Data Interpretation

Regular reporting of data releases makes it easy to forget that the “news” is often weeks old. When events are breaking fast and markets responding to headlines, this is important to keep in mind. We may still be two months away, or even longer, before we begin to get data which we can treat as important. I plan to continue the economic reports and emphasize those that have more recent data.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

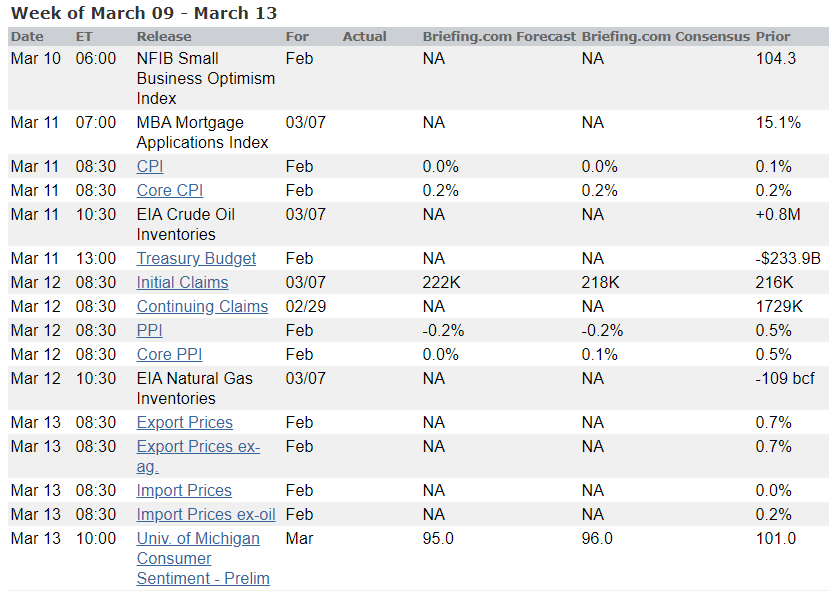

The Calendar

The economic calendar is modest. Inflation reports are of little interest in the current environment. The preliminary version of Michigan sentiment will capture more information from late February and a bit of early March. Initial jobless claims will include results from the first week in March, more current than other indicators.

Primary elections have continuing significance in the two-man Democratic race.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

With little of importance on the economic calendar, it is another opportunity for pundit speculation. While many will continue on the bogus “message” theme, there is an issue with much more value for the individual investor. Will any pundits highlight, The Crucial Significance of Time Frames?

This is not merely the question of whether one is a long-term, buy and hold investor. Time frames are relevant to the analysis of every current issue.

Background

Last week I proposed a logical framework for analyzing the fast-changing news, the economy, and market prices. It was a big effort which I hope will have continuing value. This week I will update that analysis, emphasizing the importance of one’s time frame. This is an important addition.

For each of the key topics I will discuss the immediate perspective and contrast with what we might expect one year from now. I choose the one-year time frame since it is practical and reasonable. Even a long-term investor should expect to reconsider allocations and rebalance on an annual basis. The ten-year time horizon used by many is not very helpful. In each case, I’ll offer my own opinion about the investment implications.

Virus spread

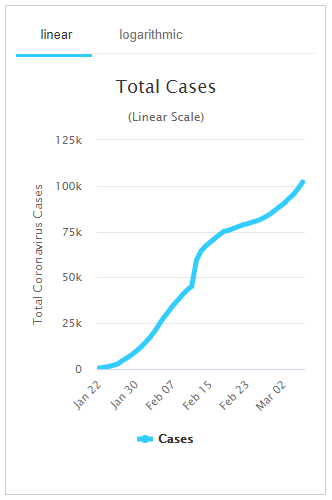

- Immediate. In the short term, we can be very sure of growth in reported cases, including in the US. The low level of early testing implies undiscovered cases and spread. This was apparent in the spike in China cases. It is possible that mortality rates will be lower than current reports, since the total number of cases will increase. From the source I recommended last week, worldometers, you can easily see the China spike. The current report changes regularly, so check it yourself. The death rate is now lower, 5.72% of closed cases, down from 12% two weeks ago.

- One year. No one knows for sure. The time for containment has passed, so it will be more of a treatment and mitigation issue. No one – even expert epidemiologists – can accurately forecast what will happen in the next year. They can only describe what might happen, and hope the reaction is strong enough.

- Investment Implication. Last week I mentioned progress in therapeutics and vaccines. Many are using the traditional FDA rules in their projections. Not so. Some clinical trials are already underway.

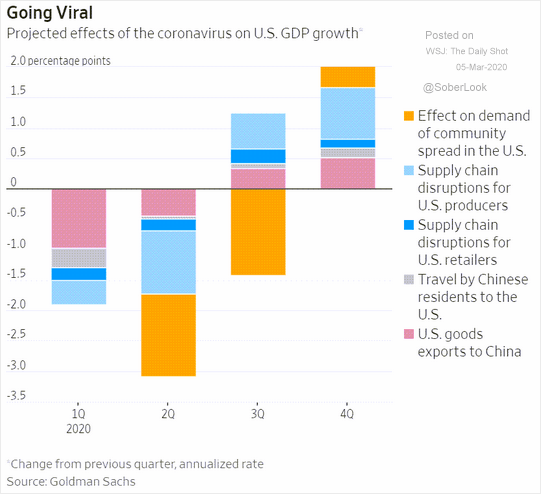

Economic Effect

- Immediate. Last week I listed the businesses where the effects would be obvious. These stories, while accurate, color the picture with many easily understandable stories. While data may be the plural of anecdotes, most people can’t do the math. Compare this description of job cuts with weekly initial jobless claims, nationwide data from employment offices. There will be an important and immediate economic effect. The real question is how much and for how long?

- One Year. While no one knows for sure, the key elements are whether business is permanently lost or just delayed. Earnings calls so far reflect some improvement in the impact. From The Transcript where you can read comments from many companies:

Succinct Summary: Worries about the impact of the Coronavirus are at the top of mind for management teams. The positive thing is activity is picking up in China and the impact is not expected to be long-term. Short -term worries persist, but elections may be the bigger long term risk to US markets in 2020.

Wisdom Tree also sees signs of a China rebound. One of their sources, DeepMacro, uses industrial indicators and people movement.

Industrial activity is clearly below where it was over the last three years but is beginning to improve. If you index their indicator to 100 as of year-end, it is currently reading 47, but this is up from the low 30s, showing that activity is picking up once again.

DeepMacro’s people movement indicators showed cumulative travel down 70% from prior years at bottom, but now travel is picking up and is even higher in some areas than last year.

And Starbucks Says China Is Getting Back to Normal After Coronavirus Slump.

- Investment Implication. There will be an important economic effect in the short term. The speed of the rebound is an open question. But a year from now, prospects are likely to be much better.

Policy

- Immediate. Last week I mentioned several possible policy responses. One of these, the Fed rate cut, happened immediately and was supported by several other central banks. Fed expert Tim Duy underscores that the Fed Can’t Solve This Alone. They seem to understand this point. As usual, while most were clamoring for rate cuts many others called it a blunder. A third camp asserted that the Fed should have increased rates earlier so that they could reduce rates now. Fed bashing is a favorite pundit sport, but it provides little help for investors. FedSpeak is sending a mixed message about further action.

- One Year. I also mentioned the possibility of fiscal stimulus as a policy response. The Trump Administration is floating the idea of a payroll tax cut. Democrats would find this difficult to oppose. Some have also suggested that the President should suspend his tariff program until the end of the crisis. This idea was greeted with a lot of skepticism, but I am not so sure. It would be a grand gesture with an “expiration date.” Expect more ideas to surface.

- Investment implications. One of the biggest weaknesses in Wall Street analysts is in how they view government actions – always static. To take one example, this is why the many predictions about Europe’s collapse did not come to fruition. When powerful forces are lined up to achieve and objective – avoiding a recession, for example – our forecasts must consider that as a factor. One prominent fund manager on my Twitter list of reliably bearish commentators complains that his predictions would have been accurate if not for the Fed. What did he expect the Fed to do? Considering government response is an important and often neglected part of financial analysis.

Stock Prices

- Immediate. No one knows! You can find a wide range of predictions, from one extreme to another.

- Ralph Vince (who does not go on TV so his excellent credentials are unrecognized by many) sees a large and fast rebound.

- The savvy manager Paul Schatz sees signs of a bottom and all-time highs in Q3. He suggests monitoring insider buying and share buybacks.

- David Templeton (HORAN) describes the widening fear across multiple sentiment measures. This is important reading for those trying to consider short-term market moves.

- Kirk Spano sees a much deeper S&P 500 correction.

- Sequoia Capital sees the coronavirus as a “black swan” that requires action on the part of their portfolio companies.

- One Year. Those who see the current decline as the catalyst for an epiphany about market valuation see longer legs for the decline. (Spano). Many observers who are “global strategists” without an economic emphasis are predicting a bear market. Those who see containment and an economic recovery have a different view, of course.

- Investment Implications. I expect things to be much better in one year. Economies put slack resources to use. Governments fight economic declines. Stocks look to the future. I am watching opportunities and will act as indicated.

What Actions Might Investors Consider

I must start by underscoring that I provide investment advice to clients. I provide information to readers – information that I hope will be helpful in making their own decisions. With clients I can determine their personal situations and needs and discuss issues with them when needed. My readers cover a very wide range of circumstances. My challenge is to be helpful in my posts without crossing the line into advice.

With that in mind, here is what I was doing last week – for clients and for myself.

For the basic stock program, I neither bought nor sold, maintaining about 25% cash. (Please remember that this is only the equity portion of portfolios. If someone’s allocation is normally 60-40, they are now 45-40 with 15% cash).

The best opportunity right now involves taking advantage of elevated volatility in option prices. In my Enhanced Yield Income program, I added to positions with more covered calls and also rolled down some existing positions. These include (especially) sectors where we do not expect a fast rebound. You can collect the high call premium, take some income, and reinvest the rest at current low stock prices.

As usual, I’ll describe more of my own conclusions in today’s Final Thought.

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Both long-term and short-term technical indicators continued last week’s decline. collapsed this week. The C-Score declined only slightly, but I am maintaining the recession odds at 48% since the indicators are capturing only some of the current factors. The St. Louis Financial Stress Index is published on Thursday, using data from the prior Friday. As I observed last week, we could expect a higher reading. This might well happen again, but we are far from the danger zone.

I contine my rating of “Neutral” in the overall outlook despite attractive valuations. It reflects the increased risk and the need for patience in either buying or selling.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies. Brian’s current update shows that the reduction in earnings expectations for the year ahead are modest, and less than we saw in 2019.

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession.

Doug Short and Jill Mislinski: Regular updating of an array of indicators.

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely. The drawback this week is that there is a lot of uncertainty surrounding when and how current worries will be resolved.

Best of the Week

If I had to recommend a single, must-read article for this week, it would be a tie. First we have the careful analysis of The Rational Walk. (H/T Abnormal Returns for the continuing effort to highlight good sources). I especially like the combination of education and implications for current investments. On the first topic, the author team writes:

The effects of the virus on business activity and security prices may well be significant, but in the long run, even the worst pandemics will run their course and conditions will improve. Personal and community preparedness is far more important at this stage than worrying about the prices of financial assets.

The investment advice is first-rate. Consider the business exposure, permanent versus temporary losses, the leverage of the business, and the cases where there might be a benefit.

There are certainly other considerations and we should all strive to go beyond first level thinking. One rarely gets paid in financial markets for thinking about the same things that everyone else is thinking about. Since the macroeconomic impacts are being discussed by nearly everyone, chances are that deployment of second level thinking is most likely to be fruitful at the micro level, that is at the level of individual companies.

The article goes on to demonstrate the importance of free cash flow over time. Since many investors are using only P/E ratios, and using a short time frame, they are getting misleading answers to their screens and tests.

Most of the value of a company (the discounted free cash flow) depends on long-term results. The author demonstrates this through a simple but reasonable model using sensitivity testing of differing assumptions.

Next, and with a similar approach The Brooklyn Investor questions what Mr. Market thinks.

If you own a restaurant on a beach and the weather forecast shows a hurricane approaching, are you going to rush to sell the restaurant before the hurricane hits? Are you going to lower the selling price because you know the hurricane is going to hit and you are going to lose a few days or possibly weeks of business? Of course not! So why would you do the same with stocks?

Noting that COVID-19 is temporary, probably worse than expected, and likely to show more deaths, he analyzes what this means for investors. Trying to explain “intrinsic value” he writes:

So this is the part I had a hard time describing. I guess non-financial people (unfortunately including many in the financial press) have a hard time grasping the idea that intrinsic value of a business is the discounted present value of all future cash flows. This person argued that the market looks only at earnings over the next year or two, but not fifty years out. Yes, this is true. But intrinsic value has nothing to do with what the market is looking at. Intrinsic value is a mathematical truth as long as the inputs are correct (or reasonable enough). Intrinsic value is 100% independent of Mr. Market’s opinion. Well, Mr. Market does set the discount rate to some extent.

He also provides a simple but helpful model to illustrate the point. Please read the entire post. Maybe twice. But here is a key conclusion:

So, with the market down more than 12%, it is like the market is discounting no earnings for the next four years! Nuts!When the pundits say that the market is or isn’t done discounting the risk of COVID-19 or a coming recession, you can see how that sort of comment is total nonsense. It is based on Keynes’ beauty contest. They are just saying that people didn’t expect a recession or negative event earlier this year, and now these things are here so the market therefore must go lower as the market lowers their expectations.

Stock Ideas

Chuck Carnevale provides a frank and practical discussion—Recent Market Action From A Value Investor’s Perspective. He calls the overall market “moderately overvalued” but concentrated risk in a place some will find surprising.

The crème de la crème of dividend growth stocks could be considered the S&P Dividend Aristocrats list. However, with interest rates as low as they currently are, high-quality dividend-paying stocks have become overly competitive with fixed income instruments. As a result, demand for quality dividend stocks has driven valuations to extreme highs for most of the best-of-breed dividend growth stocks. I will also provide examples later in the video of just how expensive the Dividend Aristocrats currently are. However, I will also highlight a few that are undervalued as well.

Eddy Elfenbein highlights Aflac (AFL) now down 25% from its 52-week high. While not trying to call a bottom in stocks, he also provides sound advice:

There are three things to do now.

1. Do not panic and sell.2. Expect more volatility. We’ll probably retest the low.3. Pick up bargains with any free cash.

I’ll restate the Peter Lynch quote from last week: “The real key to making money in stocks is not to get scared out of them.”

Want Yield?

Brad Thomas revisits several past reports, discussing how these REITs are trading in the current volatile market. This is solid educational information for those interested in REITs, with a special emphasis on valuation and planning your entries and exits.

Blue Harbinger highlights some select REIT investments, including the monthly dividend payments from Gladstone Commercial Corporation (GOOD).

The Great Rotation

Most of the recent news represents a stumbling block for the Great Rotation. It is not a permanent obstacle. Since we are moving slowly in building positions on this theme, those who have set aside cash for the purpose are enjoying better entry prices. John S. Tobey’s analysis, Coronavirus Just Destroyed Growth Stock Investing provides insight on this subject. He writes:

Therefore, we can expect a three-part adjustment that will sharply reduce the prices investors are willing to pay for growth.

First, reductions in earnings forecasts. Analysts will adjust to the new reality (and uncertainty) and extract any underlying, optimistic assumptions. (Tesla (NASDAQ:TSLA) analysts, are you listening?)

Second, a shortening of the focal point. Gone will be the valuation metrics based on 2021 estimates. The stock market “normally” looks six months out, and that means the great proportion of today’s valuation will be tied to the now-murky first and second quarters of 2020, with a peek into the third quarter.

Third, a return of appreciation for “value” stocks. You know — the dividend payers with slow, steady earnings growth that produce a slow, not-too-volatile pattern of rising stock performance. Lessened will be the willingness to buy at high price the new, exciting, yet-to-be-proven, potentially high growth company stocks of tomorrow. (Tesla investors, are you listening?)

Watch out for

MLPs. Many investors are wondering, Oil & Gas MLPs: Why Such A Sell-Off? The Dividend Guy explains the basics of MLP investing, what is currently going wrong, and mentions a reasonable candidate.

Bad advice! I love the comment this week from business cycle expert Bob Dieli:

Final Thought

For those who missed last week’s post, I strongly encourage you to take a look. It is long – even longer than my typical installment, but you need not read it all. Just focus on the theme and the investor advice. It has a lot of information that I hope will serve you well.

One element of the theme was figuring out the “message of the markets.” The most cited candidate this week was the “evidence” from the bond market showing that the economy is weakening. This topic requires more complete analysis but let me touch on two highlights.

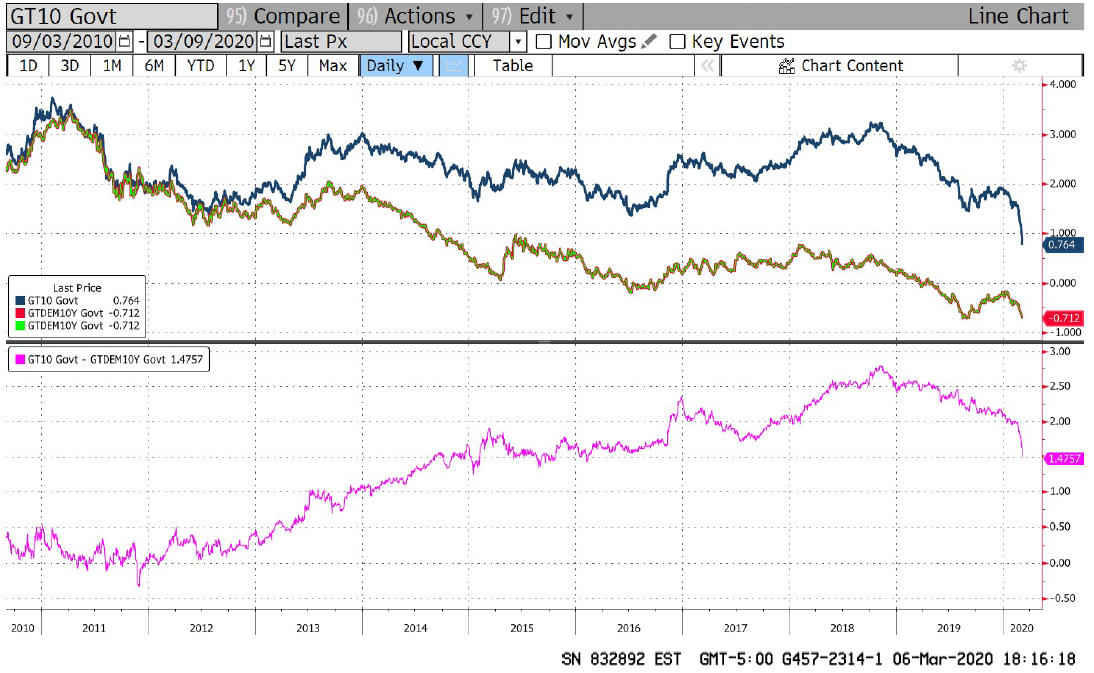

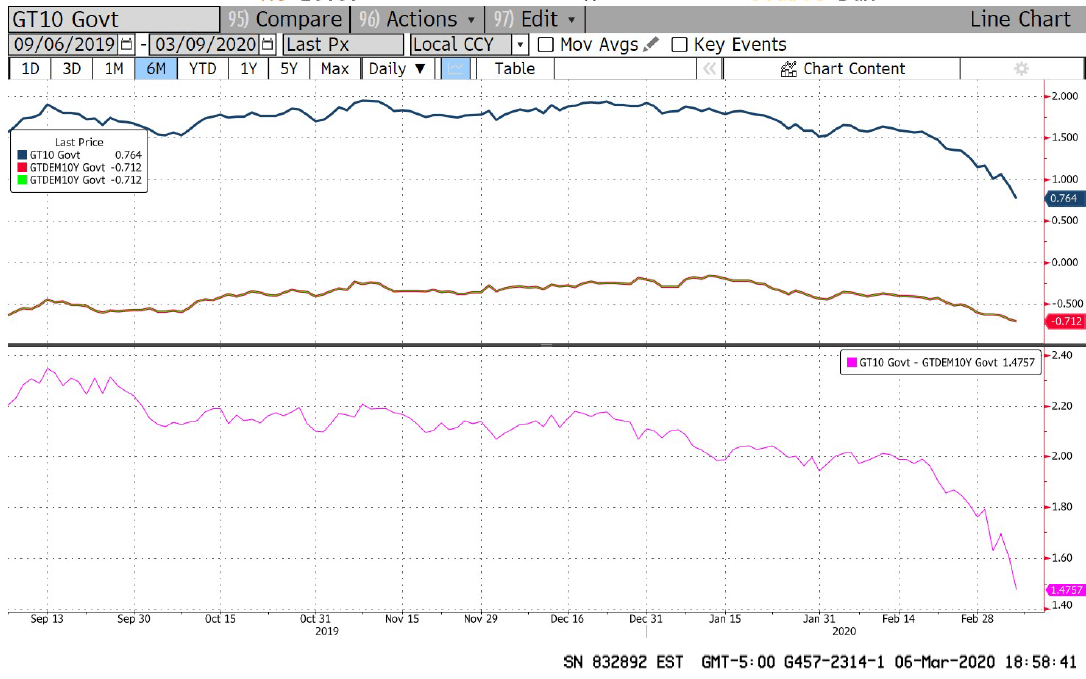

- US rates are closely linked to those of other countries, especially Europe. This is because big investors can execute an arbitrage strategy. Briefly put, they sell short a negative-yielding European bond and buy a US Treasure note of the same duration. This is the equivalent of borrowing at negative rates and lending with a positive rate. There is a currency risk, so the trade requires expert hedging. It is safe enough that the trader’s bank will allow leverage – maybe 15 times. This chart shows the relationship, narrowing as the dollar weakened and the hedge became less expensive. The implication is that US rates reflect weakness in Europe, where the coronavirus has had a larger impact, than in the US. The first chart shows the long-term relationship, including the period where the arb was not attractive. The second chart shows the recent period of closer tracking, and the impact of the exchange rate change.

And here is a further explanation from “Davidson” (via Todd Sullivan). He describes the reaction of algorithm traders and those of foreign investors.

For US algorithm traders, falling rates signal economic decline and they sell stocks and commodities and shift into Treasuries. It is why $WTI (West Texas Intermediate Oil Prices) have plunged as short-term economic fears grow. For foreign investors, it is a combination of US rates no longer meeting return/safe haven perceptions and losses on the currency exchange now going against them. A 4% decline in the US$ exchange rate represents 4yrs of yields at 1% and becomes a powerful motivator to exit. Rates on the 10yr Treasury have fallen as low as 0.67% today as algorithms drive the trend lower. Algorithmic buying of the 10yr Treasury is being countered by foreign investors selling and exiting US$ assets. What we are seeing are actions by investors with differing perceptions. The media is attempting to provide a simple interpretation that is not possible,

And also…

In my opinion, we are seeing a wide misreading of the current economic conditions. It appears that foreign investors no longer happy with US$ returns are in the process of repatriating capital which drives the US$ lower. A falling US$ is very positive for US high-value exports which stimulates US productivity, employment, retail sales and wage growth. With existing US economic conditions already positive, a weaker US$ can only add to US economic expansion.

The Big Picture says buy equities.

- Movements in the ten-year note beget further movements. This is because it is a principal hedge for banks with large exposure to mortgages that might be refinanced. (WSJ).

“Convexity tends to exacerbate market moves—if rates are going lower, convexity will make the move sharper,” said Gennadiy Goldberg, U.S. rates strategist at TD Securities.

Here is how it works. When interest rates fall, many homeowners who took out fixed-rate mortgages refinance to lock in lower monthly payments. The owners of the relevant mortgages and mortgage-backed securities—including the banks—lose out on higher payment streams. As a result, the prices of mortgage bonds tend to rise less in any given bond rally than Treasury securities or some other bonds, making them “negatively convex.”

Got that? I apologize for introducing these relatively arcane points, but I have a reason. The basic news you see does not help with important points like this. There is too much focus on the very near term and not enough on the underlying economics.

Simple explanations are misleading and expensive.

[Readers interested in what I am doing to generate dependable income in a declining market should request our Enhanced Yield information. I also welcome readers wanting to join our Great Rotation email list. You can opt-in to an email list which describes our progress with the design of the program, provides detail on the themes, and analyzes a specific stock we have already purchased. There is no charge and no obligation for participants, and we will not use your email for any other purpose. You can opt-out whenever you wish, but I hope you don’t! Comments and reactions are an important part of my investment process. I welcome your participation. Just write to info at inclineia dot com. There has been a lot of interest. If we have missed you, please write again].

I’m more worried about

- More panic. The expectation of a growth in cases and deaths should be firmly established. Nonetheless, fresh news sparks another round of knee-jerk selling. This frightens those who think Mr. Market knows all.

I’m less worried about

- An economic turnaround. Looking through the impending issues may be difficult for Mr. Market, but easier for investors watching the right indicators.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment