Khosrork/iStock via Getty Images

“Don’t be afraid to give up the good to go for the great.”

– John D. Rockefeller

Investors keep getting reminded that 2022 is one of the worst starts of a year for equities as it has been accompanied by any number of negative headlines. However, all of the indices are coming off fabulous gains achieved in the last 12 months. So the 13% correction for the S&P isn’t bad considering that these types of corrections do come once a year on average.

Bespoke Investment Group tells us just how volatile it has been this year;

“Over half of all trading days this year have seen gains or losses of more than 1%. 57% of UP days have been in excess of 1% while 48% of DOWN days have been greater than 1%.”

Investors had been waiting for a bounce off of oversold levels for some time and they finally got it. “March Madness” took the S&P 500 down ~4.5% on the month while the NASDAQ was down nearly twice that at –8.2%. BUT in just four trading days the tide was turned and both indices now show gains in March. There was more up and down action this week that added to those gains, and when I look more closely every major index ended the week UP for the month.

All of this positive action occurred AFTER the Fed said it will raise the Fed Funds rate one-quarter of a point for the next 8 meetings. AFTER analysts acknowledged the fact there could be a recession after tightening. The yield curve and credit spreads don’t offer much clarity. The “war” is further stressing global supply chains, Inflation is raging, and “out of the blue”, the market went full risk-on. Some are labeling this market “maddening” and touting their view that stocks are divorced from reality. Here is the problem, stocks are only divorced from “your” reality.

Stock prices are by definition, the reality. What that price action tells us is what every investor has to acknowledge and come to grips with to be successful. Markets can and often do rally on bad news. When things are at their worst, the stock market has acknowledged the issues and has already adjusted. It’s the “next” set of circumstances the market is looking at that is important, and for now, the message seems to be “some relief” is ahead.

It also confirms that the technicals matter a lot more than investors might want to believe. There is another subtle message embedded in the price action. Investor sentiment has told us that just about EVERYONE decided to dismiss ANY positive, and it is those positives that I’ve highlighted to members of my service that had them ready for this quick “turnaround”. The first quarter is coming to an end and one wonders if Q2 will be just as maddening bringing more challenges than what we have already witnessed this year. With the uncertain and questionable policy backdrop in place, I wouldn’t be betting on smooth sailing, but that doesn’t mean investors can’t profit from the disarray.

The Week On Wall Street

The S&P entered the trading week coming off a 4-day surge that saw the index post a 6% gain. The S&P waffled around all day before staging a late-day rally and closed flat on the day. Investors have witnessed a decided change in price action in the late day patterns as now it is more of a risk-on buying event rather than a sell into the close mentality. Including the last hour on Monday, over the last five trading days, in the middle of a war in Europe where you would think concerns of overnight headline risk would be at their highest, the S&P 500 has gained at least 0.33% in the last hour of trading for five straight days. It may not be uncommon to see one or two days of similar gains in the last hour of trading, but to see five straight is extremely rare.

The index remained strong in the last hour on Tuesday as well, holding on to gains and closing up another 1% as the S&P made it 5 of the last 6 trading days with gains. On a closing basis, the S&P entered Wednesday’s session up 8% in the last 6 trading days, while the NASDAQ posted a 12% gain in the same period. So, I guess you could say the market was due for a pause.

However, the indices quickly went back to the pattern they were using before this rally started. A poor session, where all of the indices fell, and the only bight spot was, you guessed it, Energy stocks. The trading week ended on a positive note. It almost took an entire quarter but the S&P 500 posted its first back-to-back weekly gains in all of 2022. For the Nasdaq, the first back-to-back weekly gain since November.

The Fed

Now that the Fed’s first rate hike is out of the way, the market goes back to data watching the inflation indicators to gauge what the Fed’s next move will be. Right now, bond markets are pricing in a 46% chance of a 50 basis point move in May. Although the recent CPI report was in line with expectations, energy policy and geopolitical events will likely send near-term inflation higher. This will keep pressure on the Fed to keep hiking and volatility elevated until the monthly numbers start to roll over or demand starts to recede.

It’s important to understand that the Fed’s focus on inflation is still deeply conditional; in other words, if inflation does start to decelerate rapidly, we can be fairly certain that the FOMC won’t feel a need to tighten as fast as practicable. On the other hand, a forecast that sees inflation continue to evolve along a similar trajectory to its recent one ought to assume very aggressive rate hikes at least as fast as current market pricing.

If you are BULLISH, you have to be BEARISH on inflation, because the BEARS are very BULLISH on Inflation. There is very limited “middle ground” here.

The Economy

GDPNow for 1Q22 from AtlantaFed has popped back up to around 1% (back within Blue Chip consensus range).

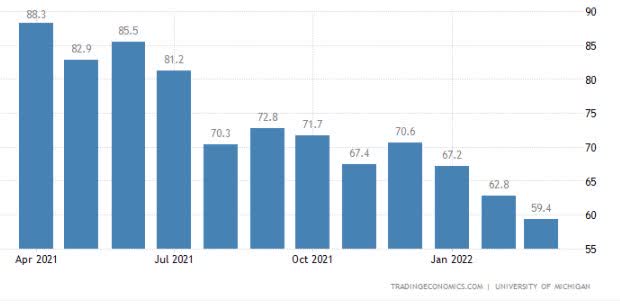

Consumer sentiment was 59.4 for the final March print. That is down another 3.4 points after falling 4.4 to 62.8 in February. This is the lowest since August 2011. Confidence has been in a steady decline since the beginning of the year and is now at an 11 year low.

Consumer sentiment at 11 year low (www:tradingeconomics.com/united-states/consumer-confidence)

A data point that feeds into the slowing economy narrative.

Manufacturing

Chicago Fed’s national activity index dipped 0.08 ticks to 0.51 in February but remains in expansion mode. So far this month, regional Federal Reserve District readings on manufacturing have been mixed with a stronger than expected reading out of Philadelphia and a much weaker than expected reading out of New York.

This week’s release of the Richmond Fed’s index saw the composite reading rose by 12 points to 13 rather than the modest single-point increase that was expected. The same for the Kansas City Fed Manufacturing Index. It surged to 37 in March vs. 29 in February; prices paid spiked to 81 -the highest since Oct 2021.

Markit Manufacturing PMI rose 1.2 points to 58.3 in the preliminary March reading and is at the highest reading since late last year. The services index for March jumped 2.4 points to 58.9 after surging 5.3 points to 56.5 in February.

Housing

New home sales decreased 2% to a seasonally adjusted annual rate of 772,000 units last month, declining for a second straight month. January’s sales pace was revised down to 788,000 units from the previously reported 801,000 units.

Pending home sales tumbled 4.1% to 104.9 in February, a steeper decline than expected, following January’s 5.8% drop to 109.4. It is as the index was improving from the pandemic shock. It is a fourth straight monthly decline and is the lowest since May 2020. A lack of inventory continues to be a major factor. NAR’s chief economist; “Buyer demand is still intense”.

The Global Scene

Flash PMIs from Markit for March were mixed, with manufacturing activity picking up in Australia and Japan versus declines in France, Germany, the Eurozone, and the UK amidst the impact of Russia’s invasion of Ukraine. Services activity picked up for flash PMI countries that reported except for Germany and the Eurozone aggregate.

Bottom line; In aggregate, data remains at or above pre-pandemic levels.

Russia/Ukraine

One of the concerns after the Russians invaded Ukraine was just how ambitious they planned to not only take Ukraine but to start moving into other surrounding countries. The Ukrainian resistance has just about put an end to the thought that Russia is going to merrily march into other parts of nearby territories. The thought of Russia making any attempt to embark on another conflict with a NATO member has to be considered very unlikely.

The Ukrainian resistance has taken the Russian army to its limits. The Russian tabloid Komsomolskaya Pravda, an outlet that is widely viewed as a quasi-official source of the government, reported Russian Ministry of Defense killed-inaction (KIA) and injured numbers. Per the report, 9,861 Russian soldiers have been killed in Ukraine with another 16,153 injured since the invasion started less than four weeks ago. Putting that in context, the U.S. lost 5000 troops during the entire Iraq War.

What was supposed to be a 3-day siege to take the capital we are now on day 31. So as horrible as this scene has been, I suspect this is the extent of their aggression in that region. Another reason to suspect why the stock market is not showing any signs of concern for the daily headlines as it once did.

Investors might also extrapolate this to all of the Cyber threats being bandied about. IF Russia decides to play on that level they will most assuredly feel the brunt of cyber retaliation. It will effectively be an OPEN SEASON on their infrastructure that will have the ability to send their reeling economy to the brink of a depression.

It’s only an opinion, but I’m not so sure they will take that risk.

Food for Thought

China isn’t taking a back seat to anyone and the Chinese version of last week’s call with President Biden signals who is sitting at the head of the table.

China will never accept US threats and coercion. The Chinese side will not sit by and will certainly make a strong response if the US side takes measures to violate the rightful interests of China and the legitimate rights and interests of Chinese enterprises and individuals, the official said, adding that the US side should not be under any illusion or misjudgment in this regard.

China will also continue to urge the US to honor its words and follow through on Biden’s commitment made on not seeking a new Cold War, not seeking to change China’s system, not seeking to target the revitalization of its alliances against China, not supporting “Taiwan independence”, and having no intention to have a conflict with China.

China urged the US to subscribe to the principle of mutual respect, peaceful coexistence, and win-win cooperation, work with China to implement the consensus between the two heads of state and push China-US relations back on the right track of sound and stable development as soon as possible.

On the Ukraine situation, the global community is crystal clear about who is easing the situation, facilitating peace talks, guarding peace and stability and who are flaring tension, adding fuel to the turmoil and fanning up bloc-based confrontation.

As the initiator of this crisis and a contracting party, the US should reflect on the role it has played so far, substantively shoulder its historical responsibilities, take concrete actions to resolve the crisis in Ukraine, and win the trust of the international community.”

There is a lot to unpack there but it’s apparent China is taking a strong stance and isn’t ready to be told what to do. There are many signs around now suggesting CHINA is going to wind up being a clear winner during this global turmoil. As an American Capitalist that makes me cringe, and it should be quite worrisome to every investor in the U.S. markets. Russia will more than likely become subservient to China as they now are dependent on them to buy their natural resources. All to keep their damaged economy afloat. So it’s no coincidence that China is NOT coming out condemning the invasion, and they probably never will.

U.S dependencies on China remain extraordinarily high and unless steps are taken it makes them a much more dominant force in the global economy. That opens up the debate about investing in China. Some view that as un-American, and I “get-it”, BUT while there are risks with the China investment scene that are plenty of “rewards” to be had as well if they continue to dominate many areas of the global economy.

The SEC and Climate?

March Madness is a perfect description of what the SEC is up to these days as they want to make their mark on the climate agenda. The SEC Advances Aggressive Climate Disclosures that will require public companies to disclose significantly more information related to their climate-related risks and their greenhouse gas (GHG) emissions under a proposed rule released Monday by the Securities and Exchange Commission (SEC).

The proposed rule, which seeks to be implemented for FY23, aims to provide a standardized approach for public companies disclosing climate-related information. The SEC contends that this information is necessary for investors to make informed decisions about the impact of climate-related risks, while critics contend this rule is outside the scope of the SEC’s authority. While this rule is focused on disclosure, we always note that disclosure-related rules are intended to change behaviors.

In my view, the proposed rule is a colossal waste of corporate funds and isn’t the necessary piece of information that an investor needs to make investment decisions. Commissioner Hester Pierce agrees with that assessment and hopefully, she can persuade her colleagues to start using common sense.

Sentiment

The Daily chart of the S&P 500 (SPY)

Another positive week for the S&P left the index approaching a level where there is plenty of overhead resistance.

S&P March 25 (www.FreeStockCharts.com)

At the index level, the technical picture shows what has been a directionless market that has frustrated both the BULLS and BEARS. A series of sharp moves that quickly reverses. I suspect we could see more of the same as the market digests the changing investment scene.

Investment Backdrop

S&P 500 companies bought back an impressive $259 billion in stock last quarter, but have already outlined plans to repurchase ~$240 billion in the first two months of this quarter alone. So not only should it far outpace 4Q21, but it could potentially reach $1 trillion for the year. This is not the only shareholder-friendly action taking place either, as dividend growth should be ~8% for the year – the best since 2019 and the second-best over the last seven years.

Might it be equities that can quickly return capital via dividends, should continue to offer potential outperformance in high inflation, rising-rate environment?

Following a Plan

It’s important to distinguish between macro, big picture investment opportunities and shorter-term trading opportunities. I discuss both types of opportunities in my daily reports to investors and my goal is to have my portfolio filled with candidates that satisfy both types. If, for instance, longer-term investment positions are pulling back, that probably means something else is moving higher to take their place for the time being, and much of the work I do managing my capital is constantly recycling and rebalancing these ideas.

I want to have as much “working” at any given time as I can, and that hasn’t been so easy this year as the list of sectors that are working has shrunk. While some of the other sectors have shown trends that have been much shorter in duration. I’ve emphasized the “themes” I want to be involved in with my new playbook and they are the still favorites for investment opportunities over the next several months.

This recent rally has produced a bounce in the HIGH growth stocks that have been punished. But it has also shown decent follow-through from many of the former leaders. Apple (AAPL), Nvidia (NVDA), and Tesla (TSLA) are a few that come to mind.

The 2022 Playbook Is Open For Business

Thank you for reading this analysis. If you enjoyed this article so far, this next section provides a quick taste of what members of my marketplace service receive in DAILY updates. If you find these weekly articles useful, you may want to join a community of SAVVY Investors that have discovered “how the market works.”

Bifurcated Market

HIGH Growth is staging a modest comeback during this recent rally, and in some respects along with Energy and commodities, it has been a leader. Many of the real HOT names suffered 70%-80% losses and now speculative ETFs like Ark Innovation ETF (ARKK) have rallied 25% in less than 2 weeks. While that is going on the more stable defensive names like CVS Health (CVS), Pfizer (PFE), and UPS (UPS) have traded sideways.

I’ve pulled the trigger on what appears to be good short-term trading setups and so far they have paid big dividends. I don’t plan to overstay my welcome and will leave the scene for what I feel will have more staying power into the next quarter.

Small Caps

During the last two weeks, the emphasis here has been the “message” from the Russell 2000 small caps. During the last sell-off, the index went into a sideways trading pattern while the other indices stayed in their downtrends. So, instead of the small caps falling apart and following the other indices down, the opposite has occurred. I believed the small caps did send a message, and if they can continue to outperform, it will help stabilize the equity market.

Of course, where a market participant has their money invested in this group is important. As of the close on Friday, Small-cap Value (AVUV) is UP 2.5% YTD, while Small-cap growth (VBK) is DOWN 12.8% YTD.

Sectors

Aerospace and Defense

The “war” has placed the spotlight on this group, and what has occurred in Ukraine increases the probability that a secular move is being cemented in place. U.S. Military spending is below the 2011 highs and there are overtures from the Eurozone that spending will need to be increased. The Ishares Aerospace and Defense ETF (ITA) is nearing a 52 week high, and in true stair step fashion is likely to continue to its all-time highs set before the pandemic.

Raytheon (RTX) has been a Savvy favorite since the inception of my playbook and it is the largest holding in ITA. RTX has already forged a new all-time high this year and I don’t see a reason to abandon this company anytime soon.

Consumer Discretionary

The sector ETF (XLY) has firmed up nicely recaptured its long-term trend on the back of a nice rally in Amazon (AMZN). From the closing low on March 8th, AMZN has rallied 21%, far outpacing the indices. Consumer Discretionary has posted back-to-back weekly gains totaling 10% and could be ready to power to more gains.

Energy

While there has been plenty of uncertainty around, one thing that remains constant is the Energy trade. WTI moved back to over $110/barrel this week and energy stocks moved higher. After a brief period mid-month where the sector took a back seat performance-wise, Energy (XLE) finds itself back on top of the leaderboard with a gain of ~10 from the lows in the prior week. For the year, Energy is up nearly 40% and once again remains the only sector in positive territory for the year. Technically, oil’s uptrend remains intact, and I continue to view any weakness in the sector as an opportunity to accumulate favored names as needed.

Oil price volatility may remain heightened, but sector fundamentals are very strong and valuations are still attractive. Additionally, energy policy will keep oil prices elevated and industry capital discipline continue to result in robust free cash flow growth used in shareholder-friendly ways.

Financials

With this week’s rally, the sector briefly broke into the positive column for the year. However, as of Friday’s close, the Financial ETF (XLF) is up 2% for the month and 0.70% for the year. The group has settled into a sideways pattern and depending on what analyst you listen to its with time to ditch the group entirely or start adding to this group.

I never go all out on a sector that has “‘value”, so I won’t be discarding BANK stocks in the near term. I’m also not adding at the moment. Instead, I’m staying with selected regional banks that continue to post strong fundamentals with decent growth prospects.

Industrials

The sector (XLI) continues to build relative strength. Not only is strength from the Transports a positive indication on the overall economic environment, but it is also supportive of internals for the sector. Areas like the rails have broken to new highs lately, and I continue to view their backdrop attractive as inventories get replenished.

Elsewhere, as mentioned the aerospace & defense subsector has come roaring back this year on increased geopolitical concerns; and higher defense spending could ultimately be a multi-year tailwind for many names in the group. After getting overbought in the short-term a couple of weeks ago, the subsector has pulled in closer to support at prior highs. For investors trying to increase exposure, I would look to accumulate favored names as they approach these support levels.

Homebuilders

The homebuilders are reporting solid earnings and are well-positioned with record-breaking backlogs in most cases. However, for the second or third quarter in a row, they are handcuffed by the never-ending supply chain issues. For whatever reason, no solutions are being offered on the problem other than ‘lip service”.

The industry is at the nexus of major supply problems. KBHomes (KBH) recently reported orders beat estimates by more than 4%, BUT closings were almost 10% below forecasts thanks to very weak backlog conversion on slightly above expectations average selling prices. In other words, KBH is seeing plenty of demand, it just can’t meet it.

Commodities

I recently mentioned that Uranium has been my “gold” as the metal continues to draw attention. I’ve owned Uranium positions since October ’21 and the recent addition purchased on the last dip on February 28th has produced a 29% gain. Nuclear energy is going to be needed as THE alternative that produces none of the dreaded greenhouse gases that keeps the “chicken-little” mindset in place. If the greenies are truly serious about the climate then they will adopt nuclear energy. Until such time the argument for “everything green” is shallow and full of hypocrisy.

Then we have the so-called geniuses that want to be called environmentalists who are by their mindset and actions increasing greenhouse-gas emissions by forcing the premature closing of serviceable nuclear-power plants. These actions are irresponsible and illogical. At some point, the “balance” between living today and planning for tomorrow has to be a DUAL goal. We’ve already seen how the ONE goal mindset had caused havoc, and economic hardships. That pain might just be getting started IF the results of these actions result in a global recession.

Healthcare

I continue to see the Healthcare ETF (XLV) as one of the better-looking charts (other than Energy) in the overall market. The sector remains a favorite and there are plenty of stocks in the group worthy of accumulation.

Technology

During a rate hiking cycle, Technology is one of two sectors that show 20% gains on average about a year after the cycle begins. The 10-year rose 48 basis points in the past 2 weeks and the NASDAQ along with the Technology ETF (XLK) rose 9.6% and 8% respectively. I reiterate – I’m not a believer that a rising rate environment is toxic for technology.

Semiconductors

I watch the relative strength of the Semiconductor ETF (SOXX) versus the S&P 500 as it has historically been a good leading indicator of the broader market. Thursday was a good day for the equity market, but it was especially strong for semiconductors as the SOXX rallied close to 5%, and every stock in the index was up at least 2%. The ETF has posted a 10.5% gain in the last 2 weeks and stocks like Nvidia (NVDA) have led the way.

ARK Innovation ETF (ARKK)

HIGH growth portrayed by the Ark Innovation ETF (ARKK) has staged a rebound rally (+25%) that has dwarfed many other sectors. That’s not so unusual given the fact that ARKK is still down about 60% from its all-time high. This sector isn’t for the faint-hearted but aggressive investors can grind out profits by selectively adding a position and employing a covered call strategy.

Cryptocurrency

The two largest cryptocurrencies, Bitcoin and Ethereum, have managed to recently round out bottoms after having sat in downtrends since the fall. As shown below, Bitcoin has been making some higher lows since the start of the year and has at least held up at support around this year’s lows.

In my view, the only way to be involved in this asset class is with the use of technical patterns. I avoid getting caught up in the notion that crypto can rise above 100k or become a worthless asset altogether. BTC continues to trade between 41k-44k, below its sideways trending 200-Day moving average, and at various points, during the year the 50-day MA has also been a decent resistance level.

Bitcoin (www.bespokepremium.com)

However, the 50-day has turned upwards and BTC is using that as support now. I continue to HOLD Grayscale Bitcoin Trust (OTC:GBTC) ($30), and Coinbase (COIN) ($189). Both have broken above very short-term resistance and may be ready to rally higher.

Final Thoughts

The equity market has rallied off the correction lows and now it’s time for the stock market pundits to voice their opinions on whether this is a BEAR market rally, a dead cat bounce, OR the springboard to higher stock prices. For a while now, I have emphasized that we are in a different type of market environment. Long gone are the “stocks only go up” days of early 2021 when all you had to do was load up on calls on the most speculative, least profitable companies in the market or buy any little dip in stocks expected to keep compounding at the same high growth rates indefinitely. While I pay attention to the indices for a feel of the general market direction the emphasis has been on “individual” and “sector” setups.

The investment backdrop changed and it became obvious that the “easy” market scene was replaced by a more difficult backdrop and that too is the way the market works. Therefore, it became apparent to me it was going to be much more difficult to make and keep money in the market unless a new playbook was used, and that’s been the message since the latter part of ’21.

ALL of the “issues” that are presently cemented in place today, were pointed out as potential problems last year. So my change in strategy was well-timed and it remains in place today. I follow “continuation” patterns that take advantage of the direction in the underlying trend. That is much easier than following reversal patterns and hoping for a change in the underlying trend.

“Our prayers and thoughts should be focused on the plight of the Ukrainian people who are under unimaginable stress.”

Postscript

Please allow me to take a moment and remind all of the readers of an important issue. I provide investment advice to clients and members of my marketplace service. Each week I strive to provide an investment backdrop that helps investors make their own decisions. In these types of forums, readers bring a host of situations and variables to the table when visiting these articles. Therefore it is impossible to pinpoint what may be right for each situation.

In different circumstances, I can determine each client’s situation/requirements and discuss issues with them when needed. That is impossible with readers of these articles. Therefore I will attempt to help form an opinion without crossing the line into specific advice. Please keep that in mind when forming your investment strategy.

THANKS to all of the readers that contribute to this forum to make these articles a better experience for everyone.

Best of Luck to Everyone!

Be the first to comment