Richard Drury/DigitalVision via Getty Images

Thesis

Western Asset Premier Bond Fund (NYSE:WEA) is a fixed income CEF. The fund has current income as its primary objective, and contains a mix of high yield and investment grade bonds. The non-investment grade sleeve is around 27%, while the rest of the fund contains only highly rated bonds. The fund has a 33% leverage ratio and a supported yield.

This CEF sort of falls in the middle of the spectrum, with a composition that is overweight investment grade bonds, but with a 27% below investment grade sleeve. It feels a bit that the fund added HY paper in order to boost the dividend yield here. Historically the fund has had a middle of the road performance, underperforming the much better known CEF BIT.

The fund usually trades at a discount to NAV which has narrowed too much as of the writing of this article (the current z-stat is now 2). There is nothing spectacular or really bad about this CEF. It would make us interested only if the discount was very wide compared to historic levels, but until then not much to see here. BIT for example has taken a very pro-active approach in managing duration through this tightening cycle, which explains its outperformance here. In order to stand out WEA needs to do something outside its current buy-and-hold tactic. Yes, granted they are trying to stand out via their ‘enhanced’ research and due diligence on credits, but with an investment grade portfolio we hardly expect defaults here. We are on Hold for this name.

Analytics

AUM: $0.14 billion.

Sharpe Ratio: -0.1 (3Y).

Std. Deviation: 15 (3Y).

Yield: 7%.

Premium/Discount to NAV: -3%.

Z-Stat: 2.

Leverage Ratio: 33%

Holdings

The fund holds a mix of investment grade and high yield bonds:

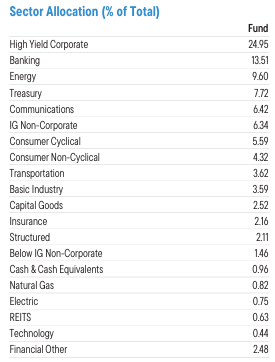

Sectors (Fund Fact Sheet)

The HY sleeve clocks in at 25%, while the rest of the portfolio is split among various IG industries. The CEF has an investment grade tilt from a ratings standpoint:

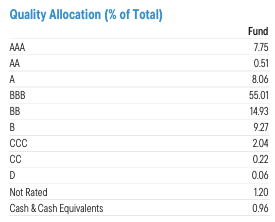

Ratings (Fund Fact Sheet)

We can see from the above table that only 27% of the portfolio falls in the below investment grade bucket (this includes the high yield sleeve and other non rated debt instruments). The vehicle contains a small AAA sleeve as well.

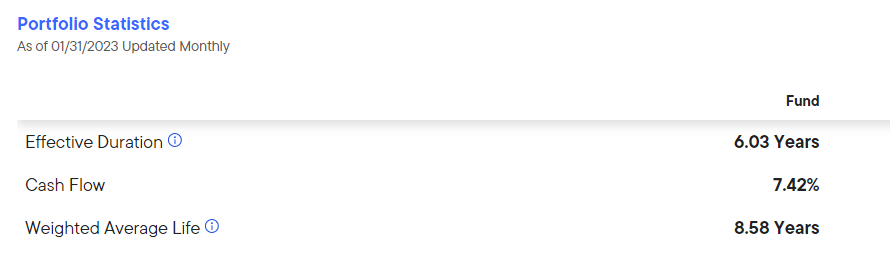

The portfolio has a 6-year duration through its composition:

Stats (Fund)

Given that two thirds of the portfolio is investment grade the prevalent risk factor here is rates, followed by credit spreads.

Performance

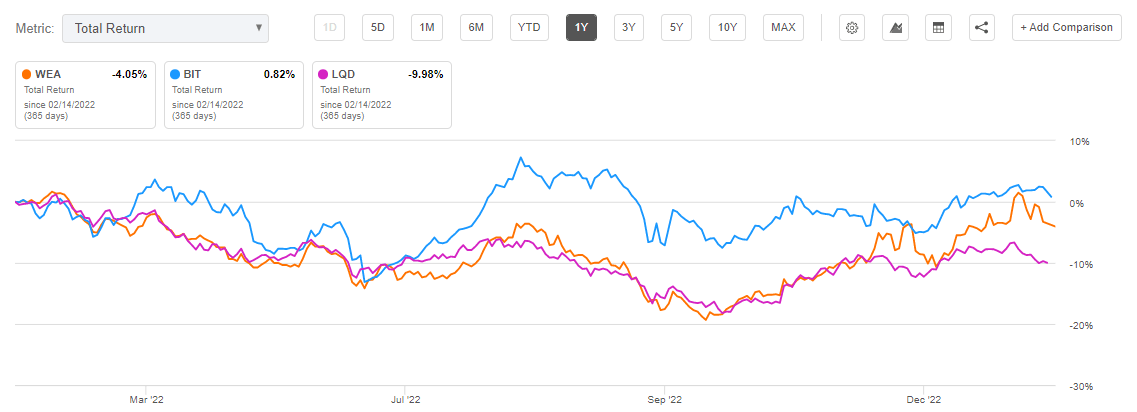

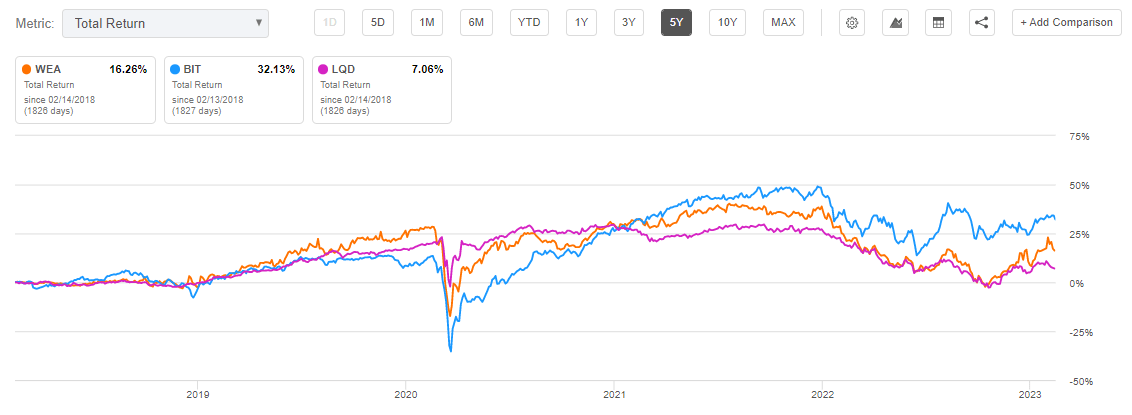

The fund has performed in line with the much better known LQD in the past year:

Total Return (Seeking Alpha)

They are not really equivalent since LQD is an ETF with no leverage and only investment grade bonds, but it is interesting to compare. The closest fund to WEA is BIT, which is also a bond fund with a multi-barbell approach. BIT however was extremely pro-active in managing duration, hence its significant outperformance.

On a 5-year basis the total performance chart is fairly similar:

Total Return (Seeking Alpha)

BIT is the clear outperformer here, followed by WEA and then LQD. Over long periods of time, decent CEFs will outperform ETFs given the embedded leverage. We can see the same story here.

Premium/Discount to NAV

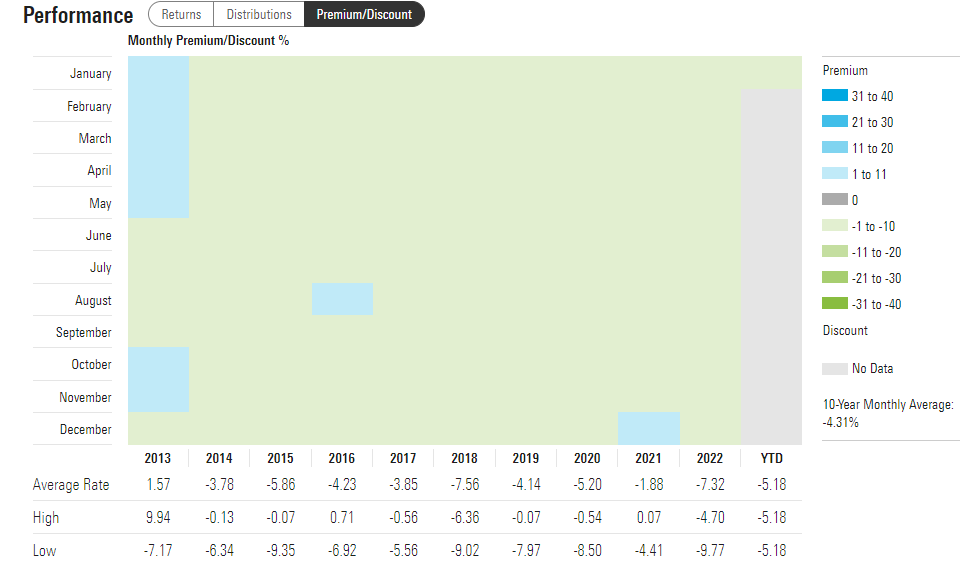

The CEF usually trades at a discount to net asset value:

Discount to NAV (Morningstar)

We can see that in the past decade this fund spent the majority of its time at a discount to net asset value. The wide part of the range clocks in at -10% discount to NAV, while on rare occasions the vehicle saw a small premium, the last time during the zero rates environment in 2021. We expect a small discount to NAV to persist for the fund, given its lack of differentiation.

Distribution

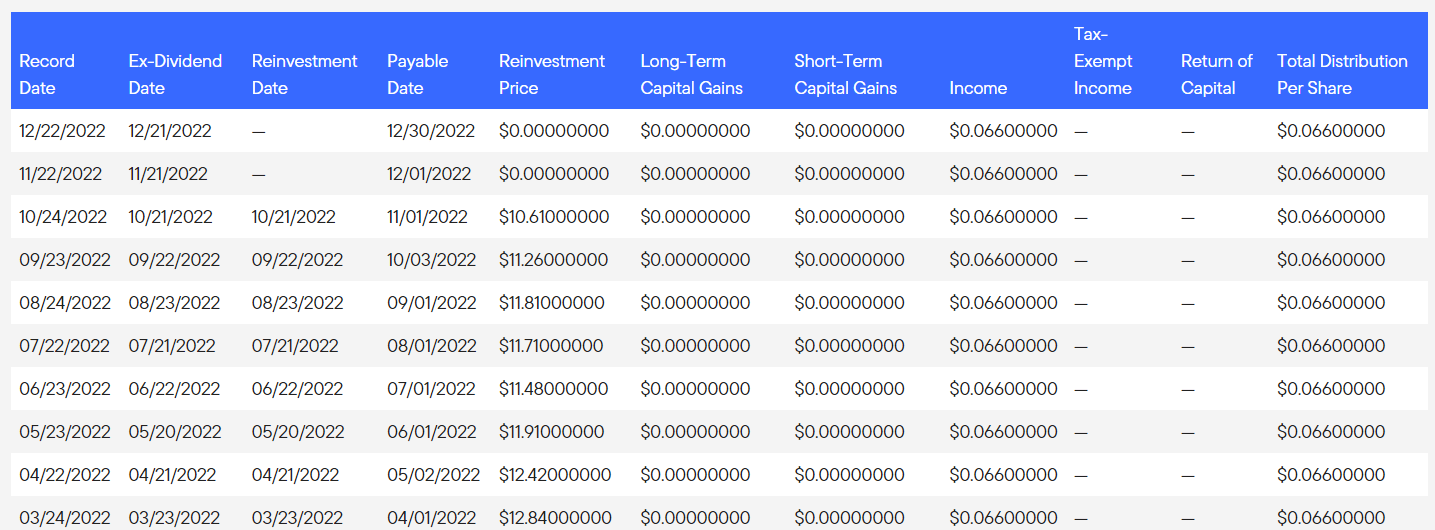

The fund has a well covered distribution:

Distribution (Fund Website)

We can see from the above table extracted from the fund’s website that no return of capital was utilized in the past year. Given the fund’s leverage and low yield we expect the name to fully cover distributions going forward.

Conclusion

WEA is a fixed income CEF. The vehicle contains a 27% below investment grade sleeve, with the rest of the portfolio being U.S. investment grade paper. The CEF has a 33% leverage ratio and a fully supported 7% dividend yield. The fund has had a middle of the road historic performance, given its lack of active duration management when compared to the likes of BIT which we covered here. The CEF is currently trading at a small discount to NAV, but it has always had. In fact the z-stat for the discount is telling us it is at the top of the range. Given its current levels we are on Hold for this name at this time.

Be the first to comment