Solskin

It has been about 18 months since my last article about Waters Corporation (NYSE:WAT) has been published. In the article I was cautious about Waters Corporation as an investment and I wrote:

“With the U.S. stock market starting to collapse and some sectors and companies already displaying stock price declines of 50% and more, I still think we should pass on Waters Corporation for now, as we can find better investments. Of course, we should not always search for extremely cheap bargains. As Buffett said: it is better to invest in great businesses at a reasonable price. And the price for Waters Corporation might almost be reasonable, and we certainly are talking about a great business. Nevertheless, Waters Corporation stock is not on my shopping list right now.”

And it seems like Mr. Market perceived the stock in a similar way. The stock price increased about 10% since my last article, but it clearly underperformed the S&P 500 (SPY), which gained 34% in value, and it seems like my “Hold” rating was justified. The main reason for this rating were the rather high valuation multiples the stock was trading for, and therefore, let’s start by looking at the valuation multiples once again.

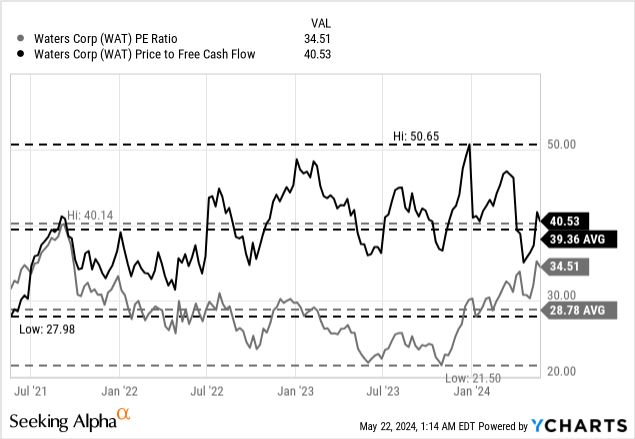

Valuation Multiples

When looking at the last three years (I am excluding previous data from the chart as the P/E ratio spike into the high triple-digits a few years ago would completely mess up the chart) we see fluctuations for the price-free-cash-flow ratio in the last two years (between 35 and 50). But the stock is trading more or less for the same valuation multiple as during my last article. And when looking at the P/E ratio we not only see higher multiples as in November 2022 but also a steep increase in the last few months.

Right now, Waters Corporation is trading for 40.5 times free cash flow and for 34.5 times earnings. And as I have mentioned several times in previous articles about different companies, a valuation multiple of 30 or 40 usually can only be justified by high and consistent growth rates as well as the business having a wide economic moat around it.

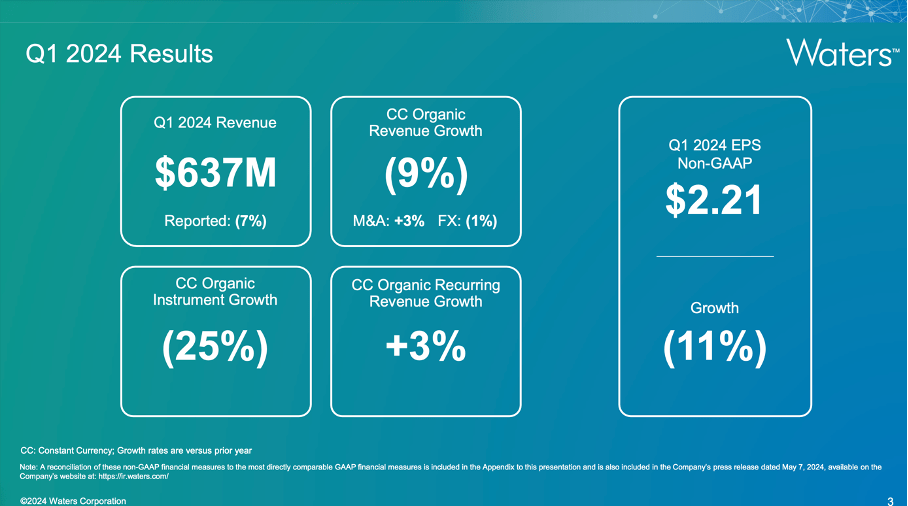

Last Results

On May 07, 2024, Waters Corporation released first quarter results and the results were not great and do not display a business growing with a high pace to justify high valuation multiples. Waters Corporation beating estimates for revenue as well as earnings per share is a “nice-to-have” but net sales declined 7.0% year-over-year from $685 million in Q1/23 to $637 million in Q1/24 (in organic constant currencies, sales declined even 9% YoY). Operating income also declined from $174 million in the same quarter last year to $134 million this quarter – resulting in 23.0% YoY decline. And net income per diluted share also fell 20.1% year-over-year from $2.38 in Q1/23 to $1.72 in Q1/24.

Waters Q1/24 Presentation

We can also look at the adjusted earnings per share and the picture gets a little brighter. But adjusted earnings per share also declined 11.2% year-over-year from $2.49 in Q1/23 to $2.21 in Q1/24. Only free cash flow increased from $166 million in the same quarter last year to $234 million this quarter, resulting in 41.0% year-over-year growth. And free cash flow is certainly an important metric and certainly more important than earnings per share.

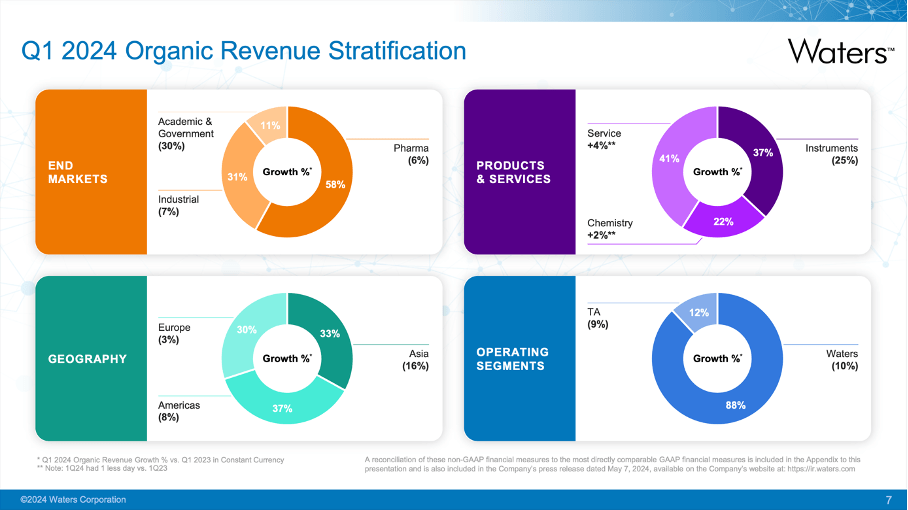

When looking at the results in more detail, it is especially China which is struggling and leading to declining sales for the overall business. Outside of China, sales declined in the mid-single digits and in China sales declined almost 30% (but management expected even worse numbers). In China, the ongoing market challenges and low activity levels for services and chemistry led to these numbers.

Waters Q1/24 Presentation

Bigger Picture

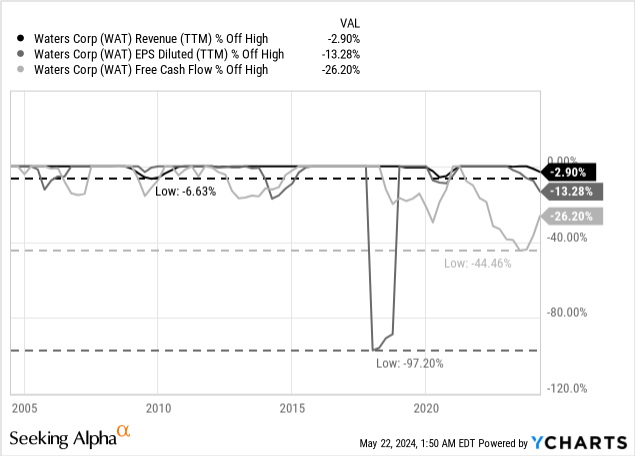

But it is not enough to just look at one single quarter as this is only a snapshot in time and it doesn’t allow us to see long-term trends. When looking at Waters Corporation since the late 1990s, we see revenue as well as earnings per share growing with a stable pace. We also see revenue and EPS declining from time to time and in the last few quarters we witnessed another phase of declining revenue and declining earnings per share for Waters Corporation. And in case of free cash flow, this is the steepest decline in the last 20 years, although free cash flow is improving again (and was growing 41% year-over-year in the last quarter).

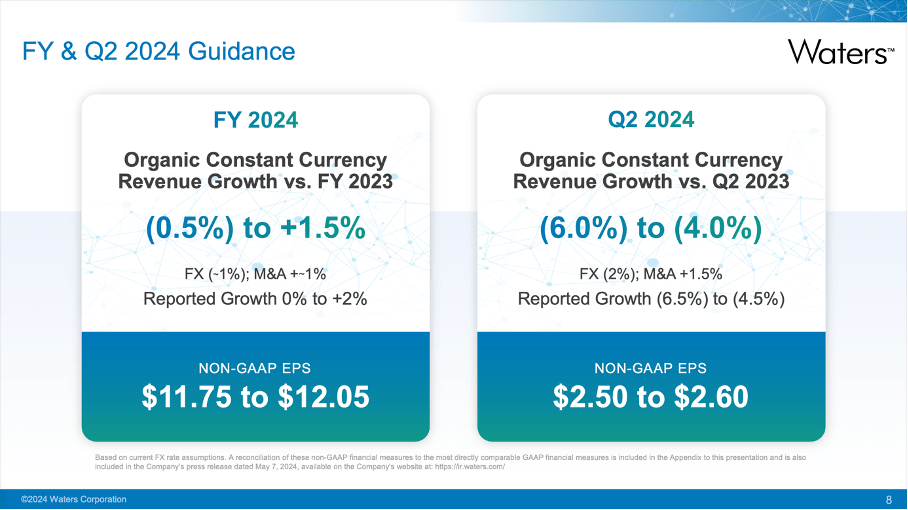

Water Corporations clearly struggled in the recent past. Nevertheless, we can be confident for the business to return to previous growth rates although it might take a few more quarters. For fiscal 2024, guidance is rather disappointing. For the full year, management is expecting organic constant currency revenue growth to be 1.5% at best (it might even decline slightly). Non-GAAP earnings per share are expected to be between $11.75 and $12.05 and compared to non-GAAP earnings per share of $11.75 in fiscal 2023 this would result in 0% to 2.5% year-over-year growth. The bottom-line growth will also be the result of slight margin expansion.

Waters Q1/24 Presentation

Moat and Business Model

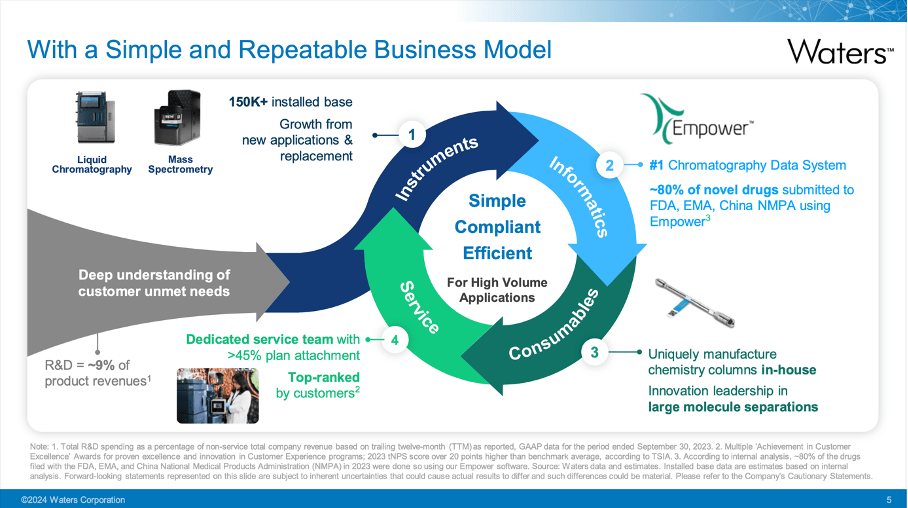

Management is still cautious for fiscal 2024 and not really expecting growth. Nevertheless, over the long run we can be optimistic for the business due to the recurring revenue streams and wide economic moat around the business.

The following chart is showing Water’s business model quite well, and we can also see how the business model is not only leading to recurring revenue, but also to a wide economic moat around the business.

JPMorgan 42nd Annual Healthcare Conference Presentation

The wide economic moat is mostly built on switching costs. Once a pharmaceutical company or research lab has bought equipment from Waters Corporation, it has not only spent huge amounts but also trained its staff using the equipment. In such a case, it seems quite natural that the lab or research facility will also buy consumables and will also need service, which is leading to recurring revenue.

And Waters Corporation is differentiating between “Instruments” on the one hand and “Service” and “Chemistry” on the other hand. In Q1/24, instruments generated only a revenue of $242 million and compared to $303 million in the same quarter last year, this is a decline of 20.1% YoY. The two recurring sources could both grow revenue. Chemistry grew only slightly from $133.5 million in the same quarter last year to $134.2 million this quarter (resulting in 0.5% YoY growth). And services generated $261 million in revenue in Q1/24 – compared to $248 million in Q1/23 this is resulting in 5.2% YoY growth.

These recurring revenue streams resulting from the wide economic moat created by switching costs is also the reason why I think Waters Corporation will be able to grow with a higher pace again – despite Waters Corporation clearly struggling in the last few years.

Acquisition and Share Buybacks

In February 2023, Waters Corporation announced the acquisition of Wyatt Technology for $1.36 billion. The company is providing training and personal services to a global base of scientific customers and more than 40 years ago the scientists were the first to commercialize on-line multi-angle laser light scattering instruments. And with about $110 million in revenue, Waters Corporation certainly paid a steep price as 12 times sales is certainly not cheap (even for a business with the potential for high margins and high growth rates).

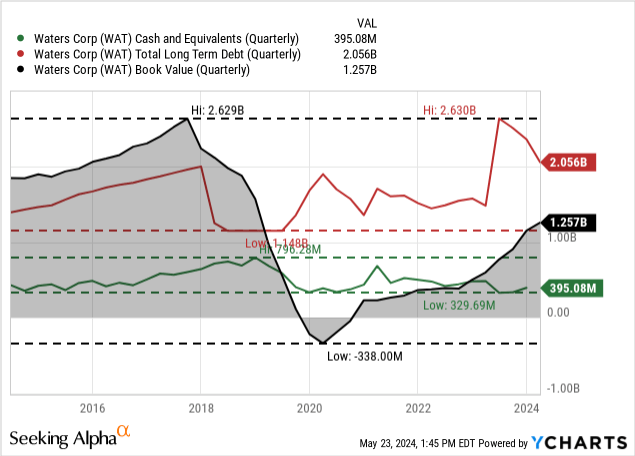

The acquisition also had an impact on the balance sheet. On March 30, 2024, Waters Corporation had $50 million in short-term debt as well as $2,006 million in long-term debt. On the asset side, the company has $338 million in cash and cash equivalents on its balance sheet that we can subtract, resulting in a net debt of $1,718 million. When comparing this amount to the total stockholder’s equity of $1,257 million, we get a D/E ratio of 1.37. We can also compare the net debt to the operating income (around $850 million in the last few years) and it would take slightly more than 2 years to repay the outstanding debt. Both metrics are acceptable for Waters Corporation and no reason to worry.

And finally, the acquisition resulted in management temporarily suspending its share buyback program to focus on deleveraging. Considering higher interest rates and especially a stock that is certainly not cheap (see the following section), focusing on reducing debt seems to be the right choice. We can also assume that management will at some point return to share repurchases, as this capital allocation tool was always playing an important role in the last 20 years.

Intrinsic Value Calculation

I already mentioned above that Waters Corporation is trading for 35 to 40 times earnings and free cash flow, and that these valuation multiples are rather indicating the stock being too expensive. But to clearly determine what an intrinsic value for the stock should be, we rather use a discounted cash flow calculation.

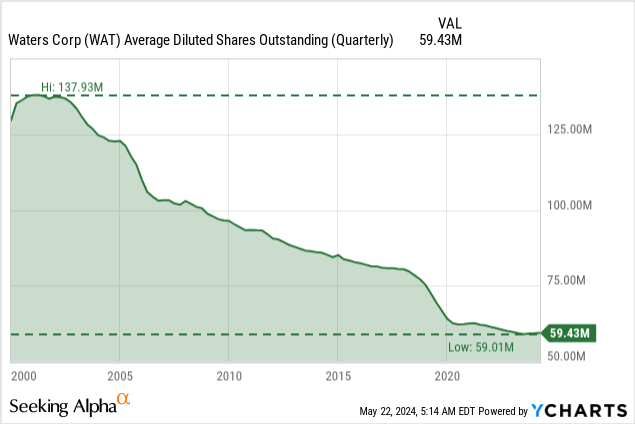

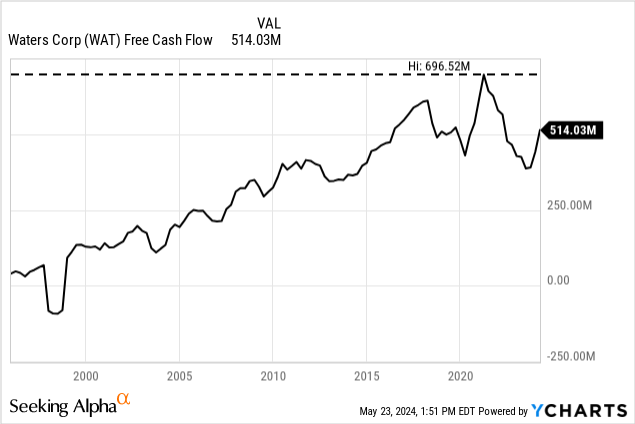

As basis for our calculation, we take the free cash flow of the last four quarters, which was $514 million. Additionally, we calculate with the last reported number of shares outstanding (59.4 million) and – as always – a 10% discount rate as this is the annual return we like to achieve (at least). In order to be fairly valued (when trading for $350), Waters Corporation has to grow 13% annually for the next ten years followed by 6% growth till perpetuity (the growth rate I use for high-quality businesses with a wide economic moat as this is the long-term EPS growth of S&P 500 companies over the last century).

Now we must put some perspective to these numbers. First, Waters Corporation grew earnings per share only with a CAGR of 7.62% in the last ten years and therefore not nearly with a pace high enough to be fairly valued. Of course, the last few years were rather a struggle for Waters Corporation and when not looking at the recent past but previous years, Water Corporation could grow earnings per share with a CAGR in the low double-digits. But 13% growth for the next decade is still not an assumption I would make.

On the other hand, we can make the argument that the free cash flow of the last four quarters is probably not representative of the business, as free cash flow declined rather steep in the recent past. And therefore, we could take a higher free cash flow as basis for our calculation.

If we are using the free cash flow when it peaked a few years ago ($697 million) and calculate with that amount (all other assumptions being the same), Waters Corporation must grow only slightly below 9% annually for the next ten years (once again followed by 6% growth till perpetuity to be fairly valued. And these are growth rates that are achievable for Waters Corporation.

Conclusion

By the way, Waters Corporation is among the top 20 stocks in the S&P 500 with the highest short interest. At the end of April, short interest was 6.95% and Waters Corporation is therefore the top-shorted stock in the healthcare sector. That by itself is probably no reason to be concerned but obviously some investors see it a good target to short and expect much lower stock prices.

And while I would not short Waters Corporation as it is dangerous in my opinion to short high-quality businesses with a wide economic moat, I would still stay on the sidelines and only rate the stock with a “Hold” once again.

Be the first to comment