Alex Wong/Getty Images News

Co-produced with Treading Softly

You can learn from the Oracle. I’m not talking about Delphi here, although the Greeks felt very confident in their Oracle.

I’m talking about the Oracle of Omaha, Mr. Buffett himself.

I find it humorous that we have become a civilization where if you want to invest “like” someone that we must invest “identically” as them or invest “in” them. Note that those are all very different and unique words.

I like to invest like Warren Buffett. That doesn’t mean I’m pounding back fistfuls of McDonald’s or chugging Cherry Coke to channel his powers. It means I can find principles in his investment style to emulate.

Buffett likes to own companies passively that pay him handsomely – I do that.

Buffett likes to own preferred shares and buy companies when others think they’ve lost their shine – I do that.

Buffett doesn’t like to pay out dividends – I don’t pay any either!

Buffett doesn’t shy away from high yields at appropriate times. This one seems to trip up the negative comments. Buffett got 8% on his privately placed preferreds with Occidental (OXY). He got a 10% yielding preferred from Goldman Sachs (GS) and invested $5 billion in it.

So does the big WB like high yields? Heck yes. He also likes to walk and talk, just like the rest of us!

We can also learn from what Buffett doesn’t do. Unlike his good friend Charlie Munger, Buffett didn’t build his fortune amassing real estate. Instead, Buffett has frequently invested in Real Estate Investment Trusts, REITs. So just like you and me, Buffett likes to avoid the headaches of direct management of real estate and instead collect a nice dividend for his invested capital.

Again, to remind my diligent readers, we can use this principle ourselves without investing in the same REITs he does. We are investing like Buffett, not in Buffett or blindly mirroring him.

Why not simply mimic him? First, our goals differ from his. I’m not Mr. Buffett, and he’s not me. As such, our goals and purposes for investing will differ even if we are applying similar principles.

Second, once Buffett invests in a company, the price tends to go up. If you are always chasing a billionaire, you will consistently pay a higher price and get a lower return. Especially since your ability to demand a Board seat or get a special preferred share created just for you and collect that extra income is nonexistent. Investing tens of billions is simply a very different ballpark than investing tens of thousands.

Our investments will not necessarily be identical, however, we can still learn from the core principles.

Let’s dive in.

Pick #1: BRSP – Yield 9.5%

BrightSpire Capital, Inc. (BRSP), hiked its dividend another 5% last month. This is its fifth consecutive quarterly increase since the dividend was reinstated. Despite this, BRSP’s share price is down about 20% since last year, having joined in the general sell-off across the equity market.

BRSP is trading at a staggering 40% discount to Q1 book value. This is a valuation we would expect for a REIT that is at risk of cutting, not one that is growing! We understand that BRSP doesn’t have a great pedigree. It was formerly “Colony Credit”, CLNC, and it was externally managed by Colony Capital.

Plain and simple, Colony completely mismanaged CLNC. It was a directionless mortgage REIT with too high of an allocation to mezzanine debt and too many big risks. It was absolutely everything that gives mortgage REITs a bad name. Over the past two years, BRSP brought on a new management team, internalized management, and, importantly, overhauled the portfolio.

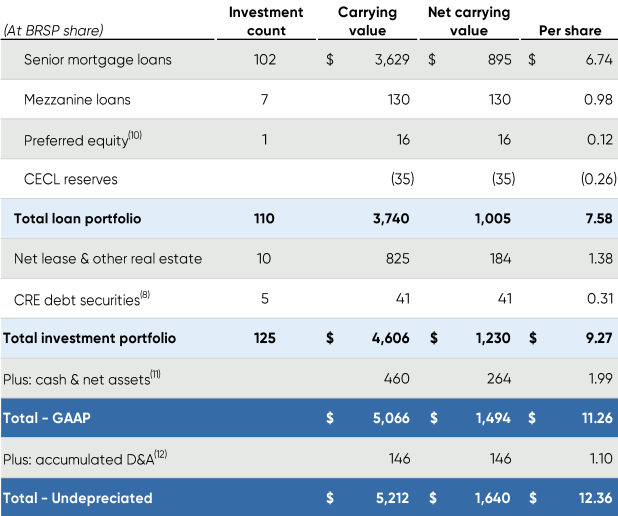

Let’s take a look at the assets that BRSP owns. (Source: Supplemental, Q1 2022)

Supplemental, Q1 2022

Note that cash contributes $1.99 to book value. BRSP intends on deploying much of this cash, and with interest spreads rising, BRSP will be able to invest at higher yields and generate higher returns.

BRSP also has $1.38 in real estate and $1.10 in accumulated depreciation on that real estate. These properties are 97% occupied, and the underappreciated carrying value of $2.48/share indicates a capitalization rate of approximately 7%.

BRSP’s most valuable property is an office campus in Norway, leased to an “AA-” rated tenant, with 9 years remaining on the lease and escalators that increase rent with inflation. We are talking about high-quality properties leased to quality tenants.

Most net-lease REITs trade at a substantial premium to undepreciated book value. The properties could likely sell for more, but let’s assume a value of only $2.48/share.

That is $4.47/share in value before we even start talking about BRSP’s core business! The bulk of BRSP’s investment is in senior mortgage loans. BRSP has a focus on multi-family, a sector that has enjoyed strong tailwinds and benefits quickly from inflation and rising rents.

Supplemental, Q1 2022

These loans are at an average of 69% loan-to-value, providing borrowers an incentive not to default and BRSP with the option to foreclose if the borrower does. Overall, this is a very conservative portfolio in the world of commercial mortgage REITs. This portfolio makes up $6.74 in book value.

The areas of the portfolio which might have questionable value would be the Mezzanine loans, which have a second lien and come in behind the senior loans, the preferred equity, and the “CRE debt securities” that BRSP has been selling off. These higher-risk sectors are contributing $1.41 to book value.

The bottom line is that investors are getting a free ride on the upside of the higher-risk investments with such an extreme discount to book value. On top of all that, 100% of BRSP’s loans are floating-rate. As interest rates rise, that is more cash heading to their bottom line. I’m happy to take advantage of the market’s oversight and keep adding more BRSP.

BRSP reports earnings on August 3rd.

Pick #2: EPR – Yield 6.3%

EPR Properties (EPR) is a unique REIT that operates in the niche of “experiential” properties. This includes movie theaters, golf centers, water parks, ski slopes, casinos, museums, and more. The types of properties that you might go to when your significant other says “hey, let’s go do something fun!”

It was an utterly terrible sector to be in during the year when fun was shut down, as 60% of their tenants stopped paying rent. Their businesses were shut down by the government edict, and Uncle Sam didn’t offer to pick up the rent bill.

If we were devising a “worst-case scenario” for EPR in 2019, I don’t think anyone would have imagined COVID-19. In fact, I remember fielding a lot of discussion about EPR before 2020 and nowhere did any bear posit the theory that there would be a virus and the government would ban group interaction for a year.

In 2019, the story was that “nobody” wanted to watch movies, and theaters are the largest contributor to EPR’s portfolio. We are halfway through 2022, and ticket sales are picking up. After holding back and delaying several releases, content creators are becoming more confident that they can release movies at a profit.

Americans are returning to other entertainment attractions even more quickly. Cedar Fair, L.P. (FUN) reports that revenues are over 20% above 2019 levels. March to May experienced the highest monthly gambling revenues of all time.

EPR came into 2022 with significant liquidity and a plan to buy approximately $1 billion in properties. If you have followed EPR, you might remember they had sold off much of their charter school portfolio in late 2019, leading to them having significant cash on hand. A $1 billion deal to buy a casino fell through because of COVID. After over two years of waiting, EPR is now actively putting that capital to work, which should help EPR get earnings and the dividend back up to pre-COVID levels.

EPR went through the worst-case scenario and came out the other side with a stronger balance sheet, with plenty of cash on hand, and instead of diluting as many companies did, EPR actually bought back shares when they were trading in the $20s!

As EPR acquires more properties and grows its portfolio, I’m happy to go along for the ride and watch my income grow with them.

EPR reports earnings on August 1st.

Shutterstock

Conclusion

Today, we looked at two undervalued and strong dividend-paying firms. If I had Buffett money, you wouldn’t be able to buy more shares – I’d own them all.

Why? Because I am applying investing principles like WB himself and look to buy undervalued and strong income-paying investments to add to my portfolio.

You’re not me. You’re not WB. Yet you can learn from Buffett’s investment philosophy just like you can learn from the High Dividend Opportunities’ Income Method. Will you mirror either of us exactly? I don’t think so.

Millions look to Buffett for principles of good investment and wealth development. We can all glean valuable principles from him to apply to our portfolio management philosophies.

Does Buffett own EPR or BRSP? I don’t care if he does or doesn’t. Nor should you if you want to invest like Buffett. If you want to invest in Buffett, Berkshire Hathaway (BRK.A) (BRK.B) shares are available to buy, but the old Scrooge won’t pay you a dime for doing so.

Instead, I take my Income Method and buy excellent income generating and paying investments, so I can fund my lifestyle, pay my bills, and have a stellar retirement. I don’t need to worry about what anyone else is doing. I can simply enjoy my stress-free retirement.

If you’re worried about how you’ll afford retirement, it’s time to change the strategy and unlock new possibilities. The Income Method doesn’t just mean that you blindly follow me into whatever stocks I buy. My goal is to teach you my methods, which you can then apply to your own due diligence and stock selection to buy the picks that make sense for your goals and your risk tolerance.

Be the first to comment