Mike Coppola

Warner Bros. Discovery, Inc. (NASDAQ:WBD) bears must be confused as to why WBD has surged over the past three weeks with a stunning recovery, even as management posted higher restructuring charges in December.

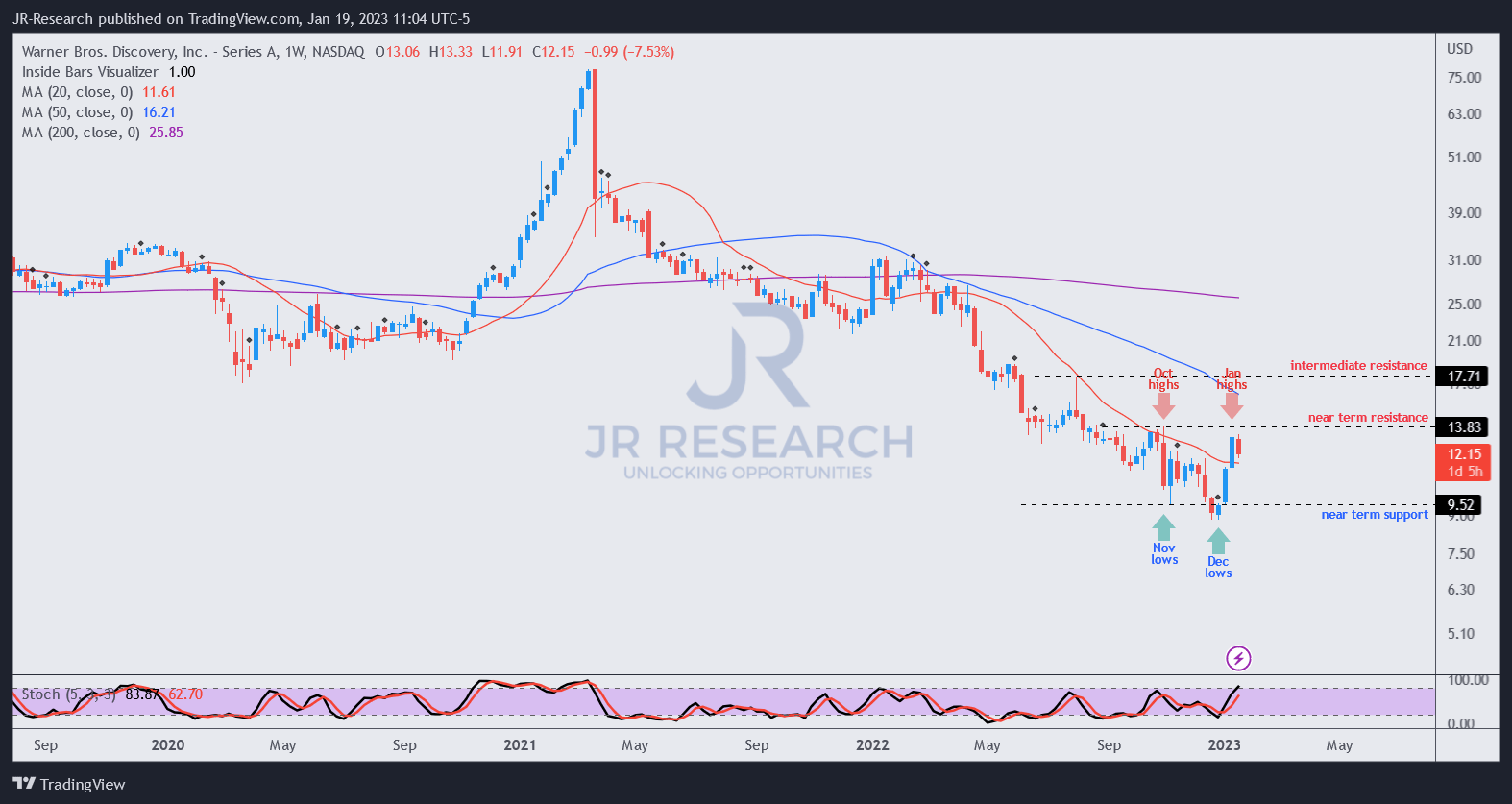

Accordingly, WBD recovered more than 50% from its late December lows through its January highs last week, completing a massacre of bears trapped at the worst possible moments.

We believe Guggenheim aptly pointed out that WBD’s valuation seems relatively attractive. Yet, the firm’s upgrade reported by Seeking Alpha on January 11 coincided with WBD’s highs last week, as it formed a top before this week’s reversal. Therefore, we wonder what took Guggenheim so long to upgrade it before WBD completed its 50% upward recovery. Did it wait for buying sentiments to reach a crescendo first before getting “more confident?” As always, we urge investors to be wary of buying into any momentum surges.

WBD buyers could contend that the company might continue to make solid progress in 2023 as management committed to further cost synergies from its merger. As a reminder, management reaffirmed its confidence at an early January conference in realizing $2B in cost savings in 2023, predicated on its upgraded $3.5B “long-term synergy target.”

As such, we believe savvy investors who bought into WBD’s capitulation lows in December likely anticipated that management would continue to pursue profitability over cash burn as rationalization prevails in the streaming space.

Moreover, we believe it’s critical for investors to remember that WBD is still expected to remain profitable in its transition year, with continued operating leverage improvement subsequently.

Accordingly, Wall Street analysts still expect WBD to post an adjusted EBITDA of $9.17B in FY22, near the lower end of management’s $9B to $9.5B guidance range. As such, pessimism has likely been baked into the company’s upcoming Q4 earnings release, contemplated at its December lows.

But, there are reasons for these savvy market operators to be sanguine.

Americans have continued to spend on discretionary services, including entertainment. Given WBD’s global franchise and an improved slate of theatrical releases in 2023, it should continue to bolster the company’s profitability recovery.

2023 could also potentially be the year film studio executives’ wishes come to fruition, with movies experiencing prolonged theatrical releases before being made available on streaming platforms or cable. Gower Street Analytics Ltd, a company specializing in analyzing the film industry, predicts a 12% rise in worldwide box office revenue for 2023, reaching a total of $29B.

As such, it also augurs well with WBD’s push to lift its pricing and DTC integration for HBO Max and Discovery+ in H1’23 as it seeks to revamp its streaming offering.

Bears could argue that churn metrics must be closely watched as consumers continue to feel the pinch over elevated inflation rates and streaming saturation.

But, we believe WBD’s valuation of 6.9x NTM EBITDA at its December lows is attractive. While it has recovered markedly to 7.8x over the past few weeks, it still trades at a relative discount to Disney (DIS) stock’s 15x NTM EBITDA and Netflix (NFLX) stock’s 24.6x metrics.

WBD price chart (weekly) (TradingView)

With WBD having surged toward its highs last week, market operators have astutely used this week’s selloff to take profits/cut exposure.

Investors who capitalized on its December lows could consider leveraging the recent momentum spike to take some risks off the table.

Newer investors considering adding more exposure to ride on improved buying sentiments on WBD in 2023 should remain patient on the sidelines and wait for a deeper pullback first.

Rating: Hold (Revise from Buy).

Be the first to comment