Lemon_tm

The Primary Care Battle Is Getting Too Competitive

Walgreens Boots Alliance (NASDAQ:WBA) has been embarking on aggressive M&A and investing activities, highlighting the massive consolidation trend witnessed in the industry. The company pledged a $5.2B total investment in VillageMD, while aiming to introduce up to one thousand primary care clinics by 2027.

This was on top of WBA’s $2.34B Shields Health Solutions deal – specialty pharmacy serving one thousand hospitals, $722M CareCentrix deal – post-acute and home care services provider, and $8.9B Summit Health deal – a clinician healthcare provider, amongst other partnerships

Therefore, it made sense to a certain extent, that WBA might want to sell its stake in the pharmacy automation business, iA, as a way to shed non-core assets. The company had similarly done so for its shares in AmerisourceBergen Corporation (ABC) for $1B and Option Care Health (OPCH) for approximately $380M.

The $2B price tag appeared enticing enough, since the company originally paid $451M in March 2021. The deal might be structured such that the pharmacy giant might still benefit from the micro-fulfillment strategy, despite not owning a stake. The management might then strategically re-invest the capital into its primary ambitions as discussed above, while similarly deleveraging its debt obligations.

It is unlikely that WBA will revert to the previous pharmacist-filled prescription model, since the micro-fulfillment centers are expected to reduce $1B from the company’s annual operating expenses, against the current $25.58B reported over the last twelve months [LTM]. For now, nine of these automated facilities had supported approximately 3K of its existing 8.8K stores by January 2023.

In addition, WBA continued to guide up to 22 similar facilities by 2025 dedicated to packing prescription medications. Notably, iA owned approximately 1K micro-fulfillment sites in the US, serving pharmacy chains, clinics, and hospitals. Seeing that the market demand for these automated facilities had doubled from pre-pandemic levels, we reckon that the operational cost savings were more than healthy indeed.

Through this decentralization strategy, WBA aimed to expand pharmacists’ roles to value-added services, such as vaccinations, testing/treating general medical conditions such as strep or flu, personalized chronic care through Walgreens Health Corners, and post-hospitalization care, amongst others. By January 2023, the company already operated 112 Health Corners while facilitating over 300K patient care services since its launch in 2020, notably in partnerships with many insurance providers such as Buckeye Health Plan.

Notably, CareCentrix registered over 19M of post-acute members, with 23% of VillageMD’s 161K Medicare patients similarly requiring chronic care. Given the obvious synergy across the end-to-end consumer-centric primary care services, it was no wonder that WBA had embarked on these aggressive M&A and investing activities thus far.

On top of that, WBA had to stay above the intense competition in the primary care market, with CVS Health Corporation (CVS) similarly splashing $8B to acquire Signify Health (SGFY), Amazon (AMZN) launching Amazon Clinic after axing Amazon Care, and Teladoc (TDOC) acquiring Livongo on top of offering mental health care through BetterHelp.

However, the WBA management had been highly prudent in its execution in our view, attributed to the robust balance sheet. Despite the continuous acquisition and investments, the company reported excellent cash/investments of $4.23B, growing by 70.5% QoQ, 2.4% YoY, and 421.5% from Q4’19 levels. The company also deleveraged substantially to long-term debts of $7.78B, declining by -26.6% QoQ and -30.5% YoY. Notably, only $2.15B of its debts will be due in 2024 and $0.36B in 2025.

These point to the safety of WBA’s dividend, significantly aided by the cash from operations of $3.29B over the LTM. Furthermore, shareholder returns have been excellent, with $202M (+31.1% YoY) of shares repurchased and $1.66B (+3.75% YoY) of dividends paid out at the same time. With 862.5M of shares as of the latest quarter, declining by -20.9% since FY2016 levels of 1.09B, there was no doubt that the company had delivered stellar results while similarly maintaining a tight ship.

Most importantly, market analysts expect sustained growth of WBA’s dividends to $2.01 by FY2024, suggesting excellent yields of 5.33% against its 4Y average of 4.03% and sector median of 2.45%. Therefore, long-term investors should simply enjoy the dividends and drip accordingly.

So, Is WBA Stock A Buy, Sell, Or Hold?

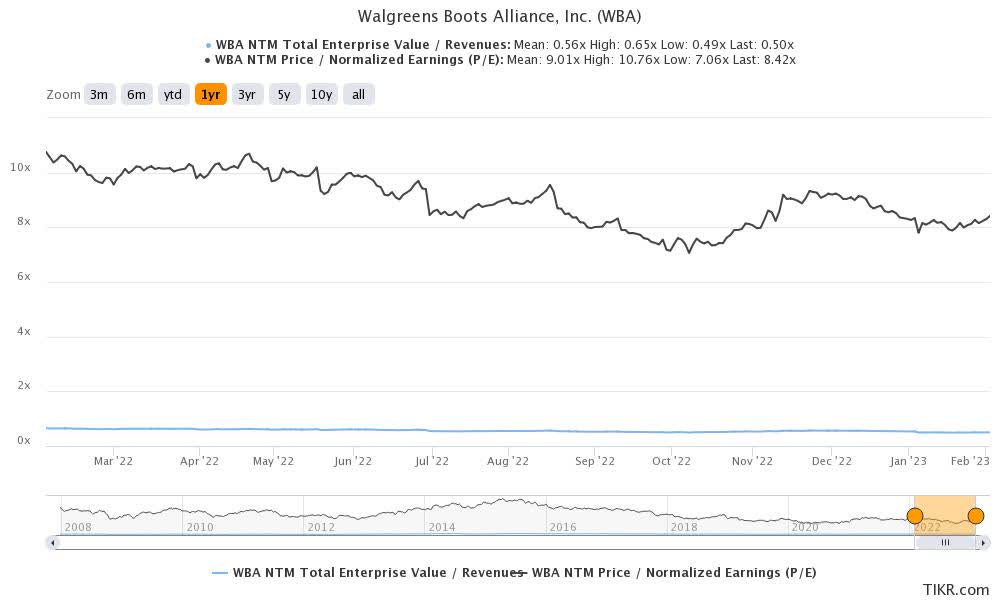

WBA 1Y EV/Revenue and P/E Valuations

S&P Capital IQ

WBA is currently trading at an EV/NTM Revenue of 0.50x and NTM P/E of 8.42x, lower than its 3Y pre-pandemic mean of 0.61x and 11.92x, respectively. Otherwise, it is still slightly lower than its 1Y mean of 0.56x and 9.01x, respectively.

Based on WBA’s projected FY2024 EPS of $4.82 and current P/E valuations, we are looking at a moderate price target of $40.58. This mirrors the consensus price target of $41 as well, offering minimal upside potential from current levels.

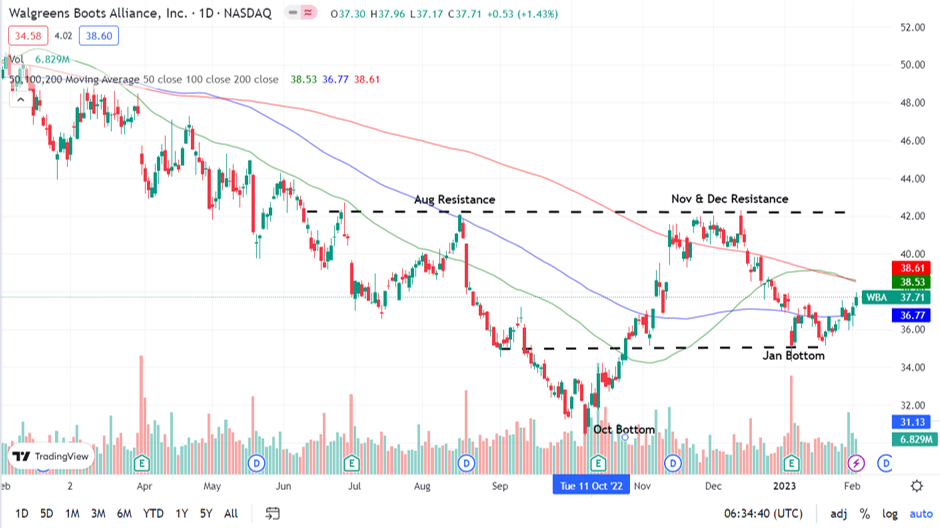

WBA 1Y Stock Price

Trading View

On the other hand, the WBA stock is still trading attractively below its 50-day moving average, nearing its January bottom of $35.19. In addition, the company is expected to record a decent revenue CAGR of 3.6% over the next few years, while sustaining its operating and net income margins at current levels.

Combined with the fact that it is trading near its 10Y lows, we are cautiously rating the WBA stock as a Buy here. We reckon the exercise may consequently lower investors’ dollar cost average, attributed to the management’s excellent execution and primary-care/healthcare ambitions. We think the rally will come soon enough once the macroeconomics lift and market sentiments improve.

Be the first to comment