hanibaram/iStock via Getty Images

Main thesis

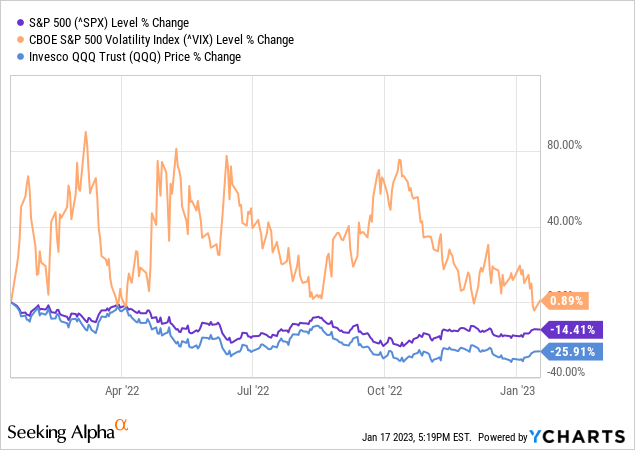

The S&P 500 Index (SP500) is down 14.4%, NASDAQ Composite (COMP.IND) is down 25.9%, and the interest rate is up from 0% to 4.5% YoY. At the beginning of 2022, there was no panic over inflation, no recession scenarios in investors’ heads, and more than enough liquidity in the system. At the same time, the S&P VIX Index (VIX) stays in the same place like nothing happened. Usually, this is a signal for the market to fall.

VIX reflects short-term expectations of market volatility, but there are enough short-term risks now to end this lull and send VIX above 30.

Be fearful when others are greedy

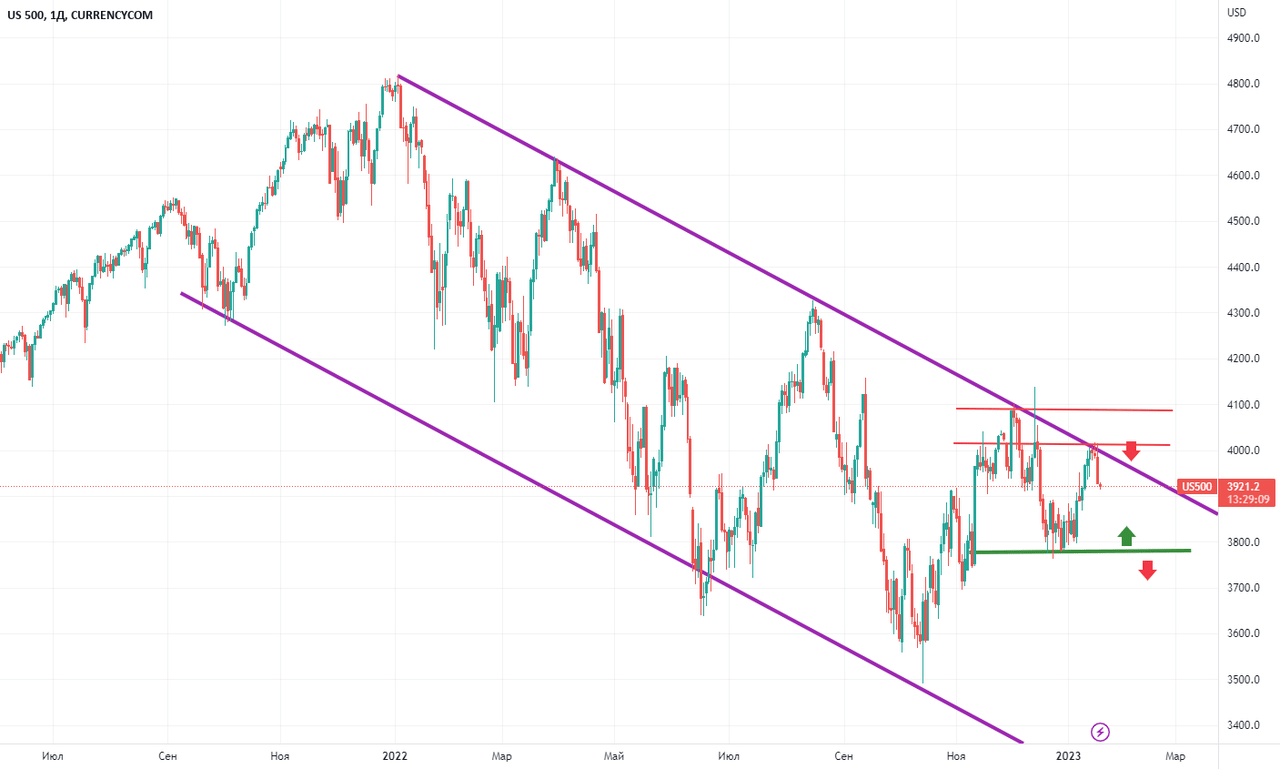

Every time the S&P 500 Index approached the 4000 level last year, the index reversed and continued to follow a bearish trend. Right now, we are in exactly the same position.

tradingview

This is the fifth time we have bumped into the upper limit of this channel, and now there are simply no fundamental reasons to break through this level. For over a year, the “Be fearful when others are greedy” rule has been working perfectly.

Sentiment is negative

We really bounced back on the positive macro news as PPI declined 0.5% last month. However, there was a whole pack of economic data that indicated a serious economic slowdown. Nominal retail sales fell 1.1% MoM while manufacturing production fell 1.3% MoM. The decline in these indicators continues for the second month in a row. In fact, part of the U.S. economy is already in recession, but data on the labor market remains strong so far. However, this is the last domino to fall, and it has yet to feel the pain of rising interest rates.

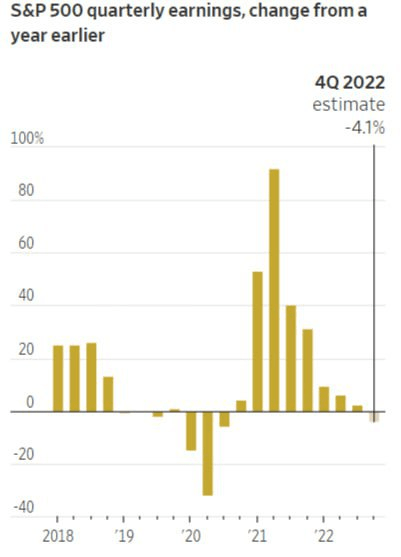

At the same time, the earnings season could be very disappointing. Companies faced many challenges by the end of 2022. These included ever-increasing operating costs, rising interest rates, and a stronger dollar that has hit multinationals particularly hard, as well as fears of a recession. Analysts expect S&P 500 companies to see a 4.1% YoY drop in quarterly earnings for the first time since 2020. Given the unfavorable forecasts of economists for 2023, management will be extremely negative in their forecasts, which will cause a wave of sell-offs in a number of sectors. The expected drop in corporate profits is another wake-up call that fundamental problems have not gone away.

CNBC

The current dynamics can be explained by something like death cramps. The longer this false calm continues, the more panic there can be and the sharper the fall. The peak of the VIX and the bottom of the S&P 500 should coincide with the peak of the Fed rate in late spring – early summer.

Recession is not good for stock (yet)

It is important to understand that these factors will not be enough for the Fed to soften its policy in the nearest future. This will surely happen faster than the market thinks and the regulator will change its shoes again. But just not now.

Inflation still looks undefeated to the Fed as it remains very sticky thanks to wage growth. Thus, the only reason why the prices keep growing is the job market, which historically needs time to cool off. And there is no way the regulator doesn’t understand that. Restrictive policies will continue until the recession not only becomes clear but literally destroys consumer demand. The Fed doesn’t fight inflation, it fights for trust, which it has been losing for quite a long time.

The problem with stock market valuation is that investors are still swinging between a soft landing and a recession. The probability of a recession in the next few quarters is perfectly expressed by the deepest in 40 years 3-month – 10-year inversion.

What is VXX?

VIX is very common among investors as a means of determining market sentiment. It is based on close-term S&P 500 options and reflects 30-day forward expectations of market volatility. Roughly speaking, this is the opinion of the market on how much the current situation threatens the shares owned by investors.

So, the scheme of what’s inside the iPath Series B S&P 500 VIX Short-Term Futures ETN (BATS:VXX) looks like this:

1. Standard & Poor’s calculates the S&P 500 index based on the 500 largest U.S. stock companies with the largest capitalization.

2. Options are traded on the S&P 500 index.

3. Based on options on the S&P 500 index, the VIX index (aka “volatility index”) is calculated.

4. Futures are traded on the VIX index.

5. VIX index futures are packaged in short-term iPath Series B S&P 500 VIX Short-Term Futures ETN futures.

The content of ETNs (exchange-traded notes) can be different. When evaluating an ETN, every time you have to look at the prospectus, that reveals the essence of this financial instrument. The name alone is not enough for evaluation, as the name also reflects the marketing appeal.

Barclays says that by purchasing an ETN, you agree to treat the ETN for U.S. federal income tax purposes as a prepaid derivative contract with respect to the relevant index. ETNs are not depository liabilities of either Barclays PLC or Barclays Bank PLC and are not subject to the Financial Services Compensation Scheme in the U.S., UK, or any other jurisdiction.

Indeed, when buying the VXX ETN, the investor pre-pays (because he pays the full price when buying) the notes, which gives him the right to receive at the end of the notes circulation period an amount equivalent to the value of the VIX index at the end of the period. The owner of the VXX ETN has neither corporate rights nor obligations, but there is an agreement to receive the value of the note at the end of its circulation period based on the current value VIX index.

Thus, income from the sale of VXX ETN should not be treated as a sale of securities, but as income from transactions with derivative financial instruments.

Long VXX or Short SPY?

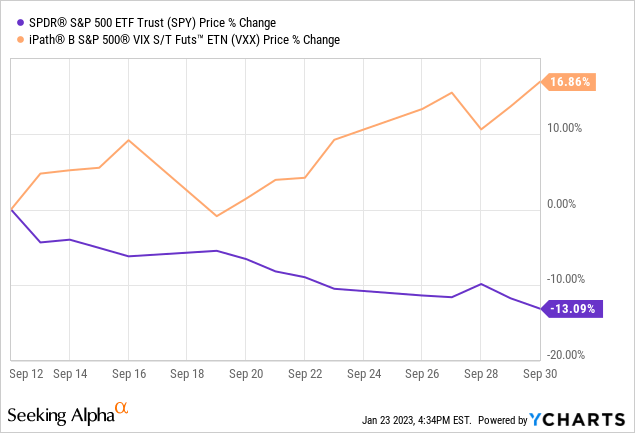

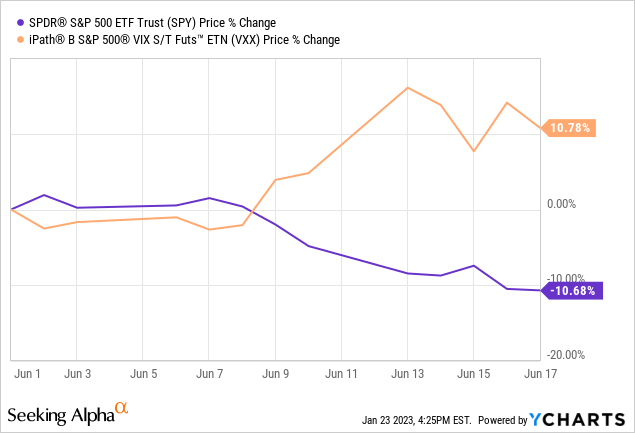

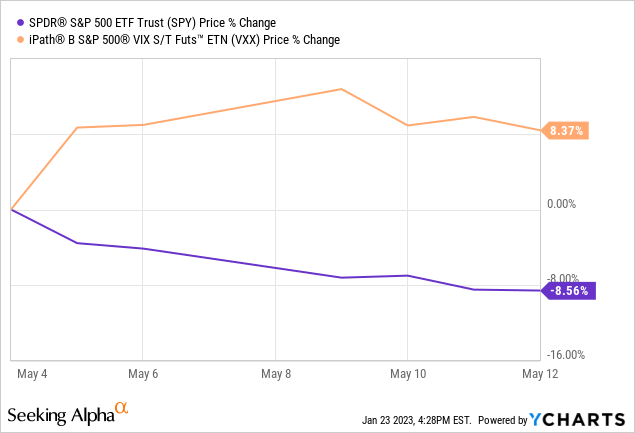

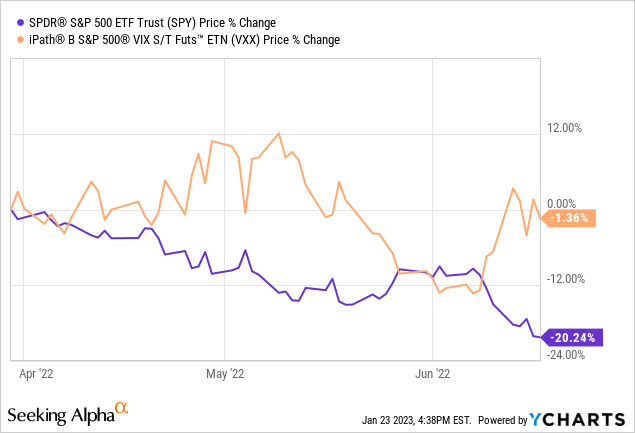

The charts below are one of the most crucial SPDR S&P 500 Trust ETF (NYSEARCA:SPY) falls of 2022 (the performance from local maximum to local minimum). As you can see, VXX does not provide any particular opportunity to bet on the S&P 500 decline.

Concerning longer period of time (Mar 30 – Jun 17), VXX buyers weren’t even able to earn from SPY’s decline of 20%.

Thus, I believe that VXX doesn’t provide any real value to investors at this moment, as it is better to just short SPY.

Conclusion

I think we can talk about reaching the bottom only with the complete capitulation of the bulls. These include margin calls, fund selloffs, and massive household selloffs that have not yet occurred and are usually the final verdict for the market. The economy is still in pretty bad shape, and in my view it only gets worse from here. In my opinion, SPY is overvalued considering that real problem didn’t go anywhere, while there are plenty of short-term risks, like the debt ceiling drama, earnings season, new potential shocks in the debt market and worsening macro data.

That being said, short SPY, avoid VXX.

Be the first to comment