Justin Sullivan

AT&T (NYSE:T) is about to report its full-year earnings results on Wednesday and the street is eager to find out whether the business can continue to keep its momentum after reporting record numbers in Q3. What we already know though is that the transformation that started two years ago and focused on the company’s core connectivity strengths has all the chances to continue to help AT&T gain new subscribers, expand its network coverage, and grow its mobility business in the following years. Thanks to being a part of a telecommunication oligopoly, AT&T is also likely to face little competition due to high entry barriers while at the same time, there are reasons to believe that it would become of the biggest beneficiaries of the latest federal programs that are aimed at bringing high-speed internet to distant areas. Considering all of this, it seems that after years of underperformance, AT&T has finally found its footing and has all the chances to continue to surprise investors and create additional shareholder value for years to come.

The Right Strategy

Back in October, AT&T revealed its latest earnings results for Q3, which showed that the business is managing to successfully utilize its core strengths without having to spend time and resources managing WarnerMedia (WBD) which fully became a separate entity in April. Even though AT&T’s revenue of $30 billion was down 4.2% Y/Y during the quarter, it was nevertheless above the street estimates by $140 million. At the same time, the company recorded 708,000 postpaid phone net adds during the period, which signals that the decision of the management to focus on growing AT&T’s core telecommunication business was the correct one as it has been successfully yielding great results in recent quarters. The business is already close to 7 million postpaid phone net adds and around $4 billion to $6 billion in cost savings since the start of the transformation, which indicates that AT&T is moving in the right direction.

Going forward, there are reasons to be optimistic about the company’s future thanks to it being a part of a telecommunications oligopoly that has high barriers to entry and a relatively small number of competitors. As the demand for broadband services is expected to continue to increase, AT&T is likely to be one of the main beneficiaries of this trend. The Q3 was already one of the company’s best quarters as it had 338,000 fiber net adds during the period and it also became the 9th consecutive quarter that had over 200,000 fiber net adds. Add to this the fact that the recently announced joint venture with BlackRock is about to help the company expand its horizon even more and make it possible for it to reach its goal of doubling its fiber footprint to 30 million locations by the end of 2025 and it becomes obvious that the growth story is far from over.

At the same time, AT&T’s wireless business has also picked up momentum and is about to set another record this year. If at the beginning of 2022, AT&T’s management expected to cover 70 million people with its midband 5G, then during the latest conference call, it was revealed that the company is on track to cover 130 million people by the end of 2022. On Wednesday, we’ll find out whether that was the case when the Q4 and full fiscal year results are released, but such an increase of coverage above the initial estimates shows that AT&T is able to deliver on its promises if the management’s focus is on utilizing the business’s core connectivity strengths.

What’s also important to mention is that AT&T is likely to become one of the biggest beneficiaries of federal programs that are aiming to spur economic growth and deal with the rising inflation by improving the country’s infrastructure and bringing high-speed internet to distant areas. AT&T has already indirectly benefited from the Infrastructure Bill of 2021 and the Inflation Reduction Act of 2022 that gave funding to the broadband industry. At the same time, during the latest conference call, the management noted that there are possibilities to pair AT&T’s capital with public capital to open up opportunities that the company might not have pursued on its own. Bloomberg independently also confirmed that AT&T is already looking to work with municipalities that receive federal funding for broadband programs to fund its own expansion in the United States. All of this shows that AT&T has more than enough room for expansion and the growth story is far from over at this stage.

Reasons For Optimism

The release of Q4 results has all the chances to help the company to end the fiscal year on a high note as a few months ago the management has already increased its forecast for the EPS, which is now expected to be $2.50 or higher, above the previous estimates of $2.42-2.46. At the same time, AT&T aims to have an additional 600,000 postpaid phone net adds during the quarter.

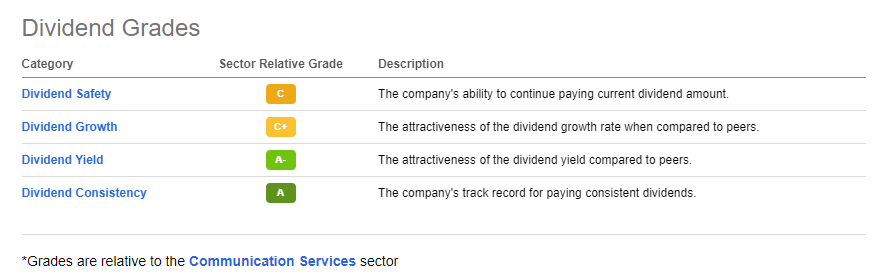

It’s also important to note that all the talks about the potential dividend cut are nothing more than unsubstantiated rumors as the management during the latest conference call already signaled that the business would generate more than enough free cash flow to cover its annual dividend commitment of $8 billion. Seeking Alpha’s scorecard also shows that dividends are mostly safe while a ~6% yield could be one of the main reasons to acquire AT&T’s stock for lots of dividend investors.

AT&T’s Dividend Scorecard (Seeking Alpha)

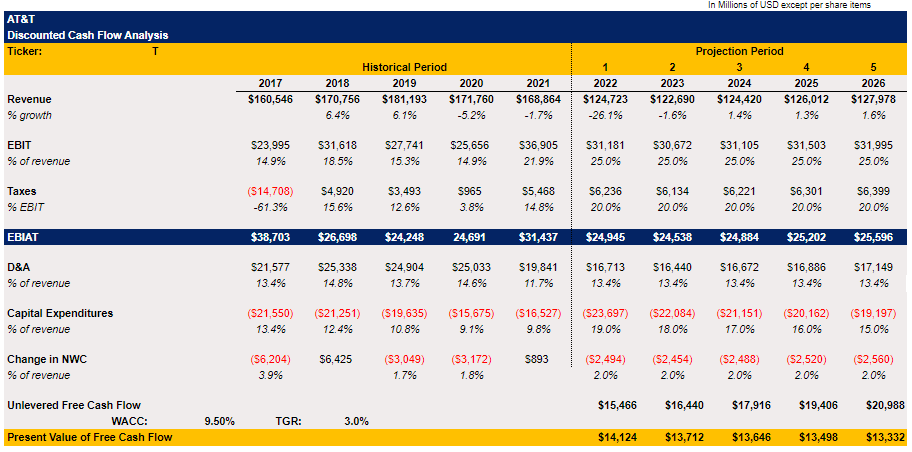

As for the valuation, I’ve made a DCF model that aims to find the fair value of AT&T’s stock to understand whether it makes sense to buy it right now if the dividend argument is not enough for some investors. In the table below AT&T’s top-line assumptions are mostly in-line with the street estimates and a major decline in revenues in FY23 is associated with the spin-off of WarnerMedia that no longer generates any returns for the business in comparison to previous years. The EBIT margin in the model stands at 25%, while the increase in taxes going forward is something that the management has been talking about in the latest conference call. The rates for D&A and the change in net working capital are mostly averages of previous historical periods, while the increase and later a subsequent decrease in capital expenditures is something that the management has been guiding for in its Q3 conference call. The WACC in the model is 9.5% while the terminal growth rate is 3%.

AT&T’s DCF Model (Historical Data: Seeking Alpha, Assumptions: Author)

My model shows that AT&T’s enterprise value is $280 billion, while its implied share price is $20.68 per share which represents an upside of ~8% from the current levels and is close to the current street consensus.

AT&T’s DCF Model (Historical Data: Seeking Alpha, Assumptions: Author)

Risks

There are several major risks to AT&T’s growth story. The biggest problem of the company is that it had $124 billion in long-term debt and only $2.5 billion in cash resources at the end of Q3. With such a debt profile, the company has no room for maneuver, especially in the current high-interest rate environment as a potential non-core acquisition in the future could become terminal for the whole business. The good news though is that at this stage AT&T has a decent debt tower, as 95% of its debt is at a fixed rate and the average yield is 4%. With an interest coverage ratio of over 4x, such debt is manageable.

The problem though is that if capital expenditures exceed the estimates and begin to burn too many resources, there’s a risk that AT&T would be required either to cut dividends or to borrow additional funds at a worse rate in an environment that doesn’t reward the debtor. Therefore, even though the situation is currently under a control, there’s always a possibility that one wrong move on behalf of the management could kill the growth story and make AT&T’s stock less attractive than it is today.

The Bottom Line

The transformation of AT&T’s business that began over two years ago is already yielding great results and there’s an indication that the growth story is far from over. The company’s debt situation is currently manageable, while the expansion of its fiber and wireless network could lead to additional postpaid phone net adds in the foreseeable future. Add to this various federal opportunities along with the lack of major competition and it becomes clear that AT&T has all the chances to continue to create additional shareholder for years to come.

Be the first to comment