DNY59

The VIX index measures the implied volatility of S&P 500 stocks. In 2022, the VIX traded between 16.34 and 38.93. At around 20.50 on January 19, the volatility index was sitting well below last year’s midpoint. In early 2023, economic and geopolitical uncertainty make the VIX attractive at the current level.

Implied volatility is the primary factor determining call and put option values, as it’s the market’s consensus projection of the future price variance of an asset. The S&P 500 is the most diversified U.S. stock market index. In the past, the VIX index tends to move higher when stock prices move lower. Options are price insurance, and market participants often flock to insurance vehicles during bearish trends. A bull market in stocks tends to cause market participants to ride the wave without insuring their portfolios.

Markets are nervous in early 2023, with many analysts warning of a deep recession as the U.S. Fed continues with its hawkish monetary policy path. However, the VIX has been trending lower, which could be an opportunity as the index is closer to the 2022 low than last year’s high. The iPath S&P 500 VIX Short-Term Futures ETN product (BATS:VXX) is a highly liquid short-term trading product that follows the VIX higher and lower.

The bearish trend in the VIX since March 2020

The VIX has made lower highs since peaking in March 2020 as the global pandemic gripped markets across all asset classes.

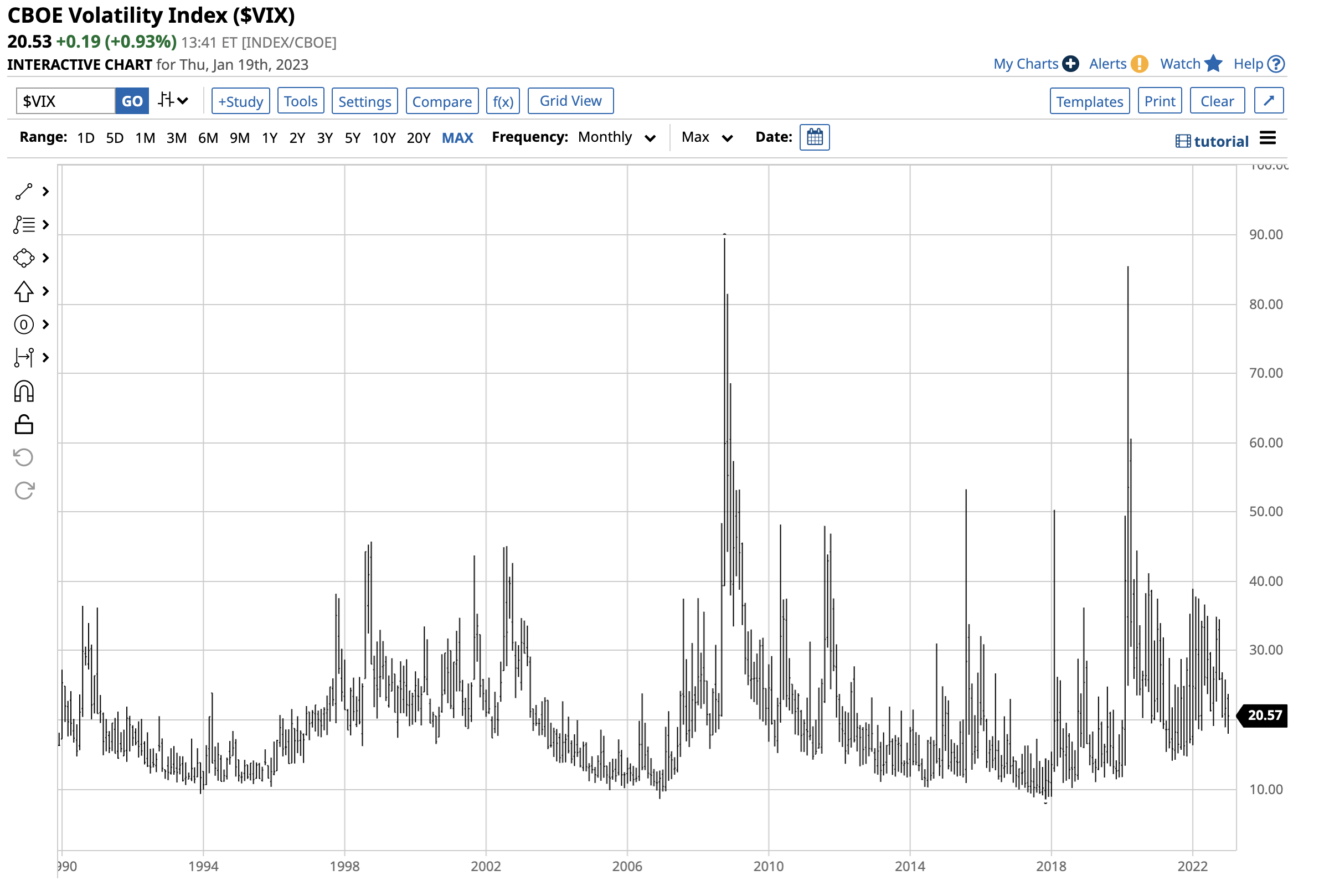

Long-Term Chart of the VIX Index (Barchart)

The long-term chart dating back to 1990 shows two spikes in the CBOT Volatility Index (VIX) in 2008 and 2020. The 2008 global financial crisis caused the explosive move that took the VIX to a record 89.53 high. In 2020, the pandemic pushed it to a slightly lower 85.47 peak.

The VIX remained below the 40 level when Russia invaded Ukraine in early 2022 and has made lower highs since the March 2020 peak.

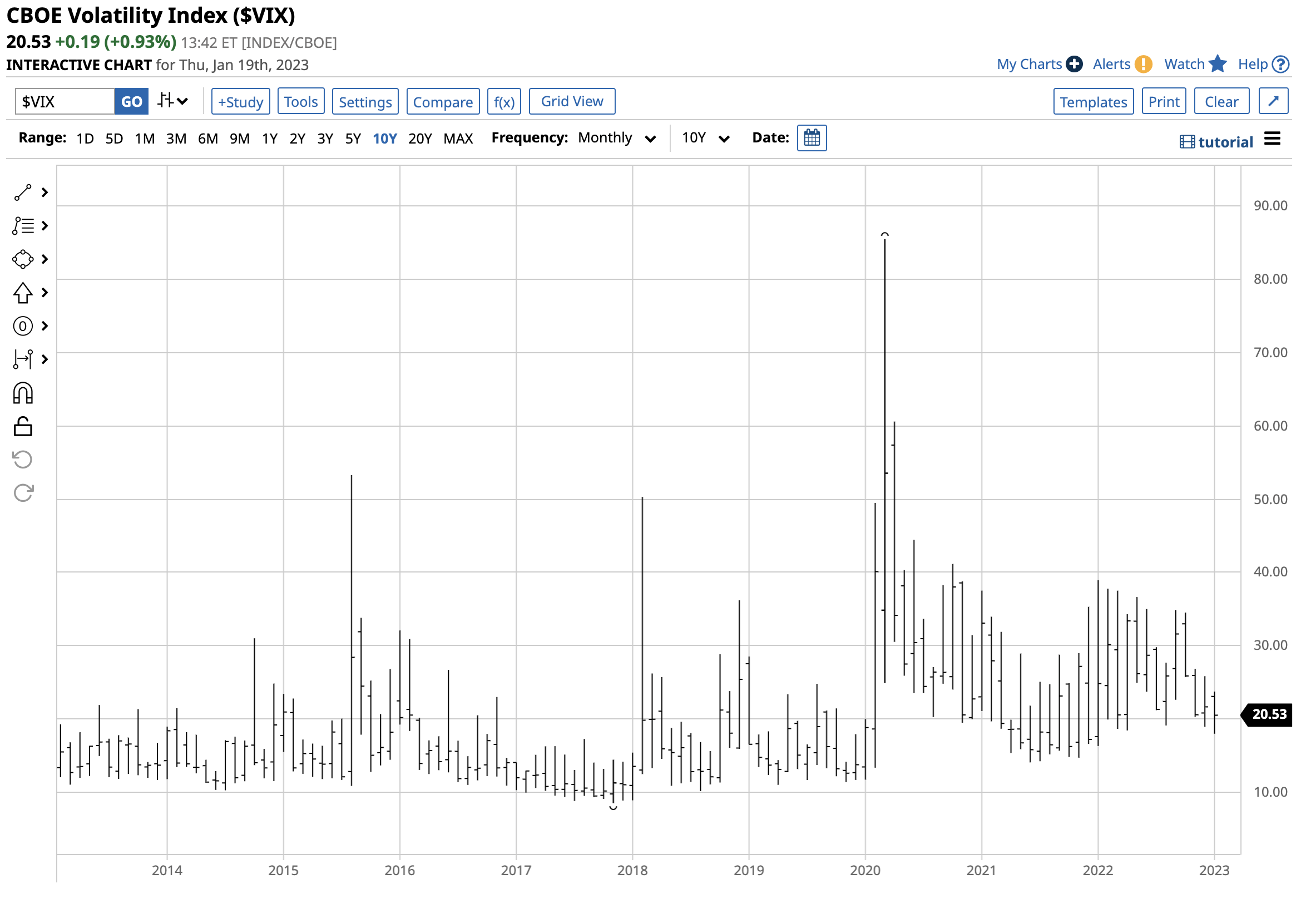

The VIX base level: Rising since late 2017

In November 2017, the VIX index reached rock bottom at 8.56.

Medium-Term Chart of the VIX Index (Barchart)

The medium-term chart shows a pattern of higher lows in the VIX since late 2017. The bottom line is that the demand for price insurance has slowly increased over the past years.

3 reasons to trade VIX from the long side on dips

Markets reflect the economic and geopolitical landscapes, and at least three compelling reasons support periodic upside VIX spikes in 2023:

- The geopolitical bifurcation of the world’s nuclear powers creates economic distortions. China and Russia’s “no-limits” alliance led to the Russian invasion of Ukraine. The scenario surrounding Taiwan is eerily similar. War and conflicts impede global trade with supply-side financial problems that are beyond the reach of monetary policy tools.

- The pandemic’s legacy is the inflation created by a tsunami of central bank liquidity and government stimulus programs. The war in Ukraine only exacerbated the financial condition.

- The U.S. remains the world’s leading economy but faces a looming debt crisis. A slim opposition majority in the U.S. House of Representatives will make raising the debt ceiling a challenging political exercise. Moreover, at $31 trillion, servicing the debt has become a lot more expensive. Hawkish monetary policy and quantitative tightening to reduce the Fed’s swollen balance sheet has caused interest rates to skyrocket. In January 2022, the Fed Funds Rate stood at a 0.125% midpoint. In January 2023, at 4.375% and rising, the annual debt servicing cost is over $1.35 trillion annually. Even if the debt level remains stable, higher rates will cause it to climb, and compounding interest will boost it to over the $40 trillion level in six years. Higher interest rates will cause it to reach that level sooner.

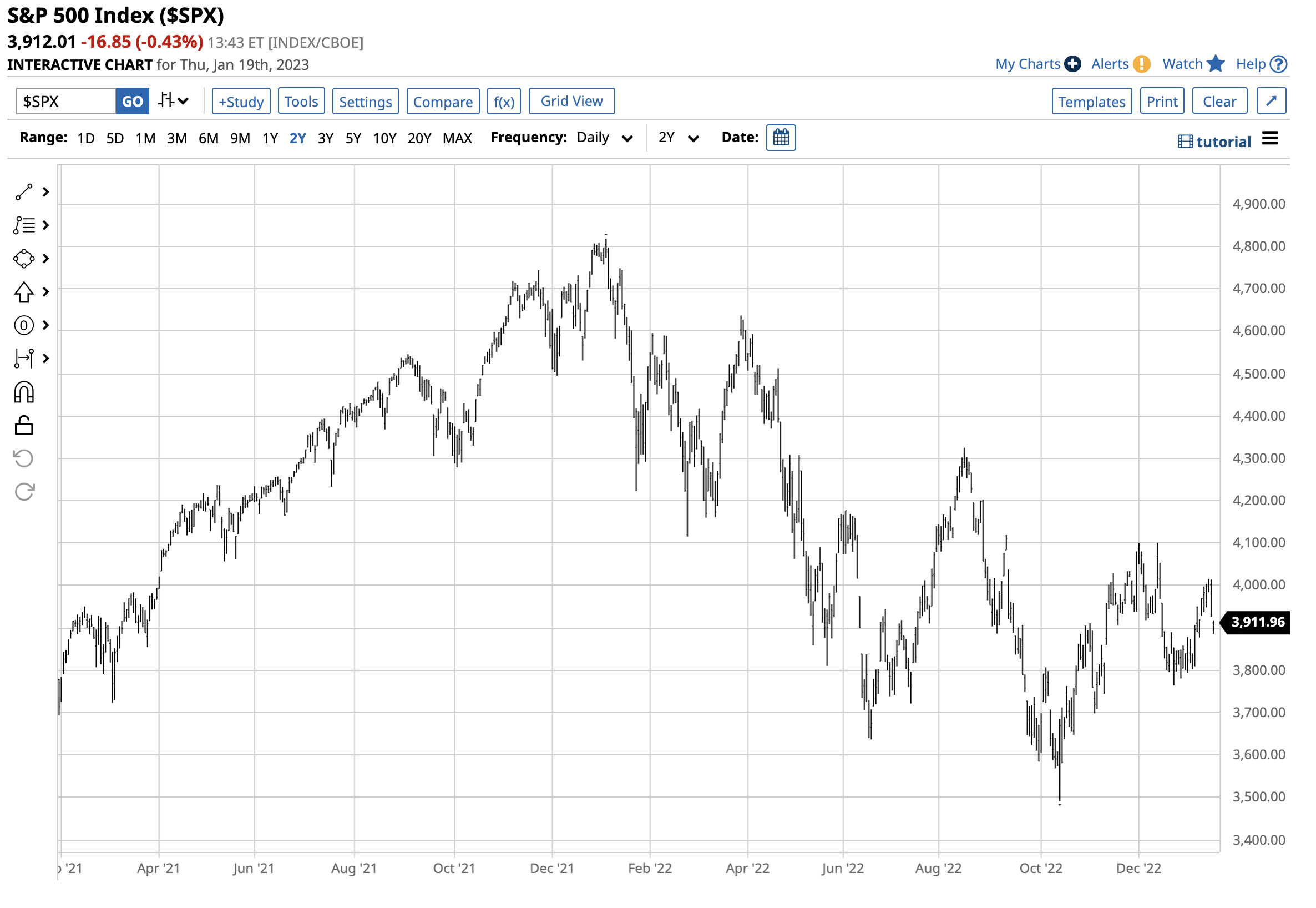

Meanwhile, the S&P 500 index trend remains bearish in early 2023.

Two-Year Chart of the S&P 500 Index (Barchart)

The S&P 500, the most diversified U.S. stock market barometer, has made lower highs and lower lows since January 2022. The trend in any market is always your best friend, and it remains lower in the U.S. stock market. Moreover, the hawkish Fed will likely cause the economy to slip into a recession, weighing on corporate earnings and the stock market. The VIX was trading around the 20.50 level on January 19, 2023, which could be a bargain.

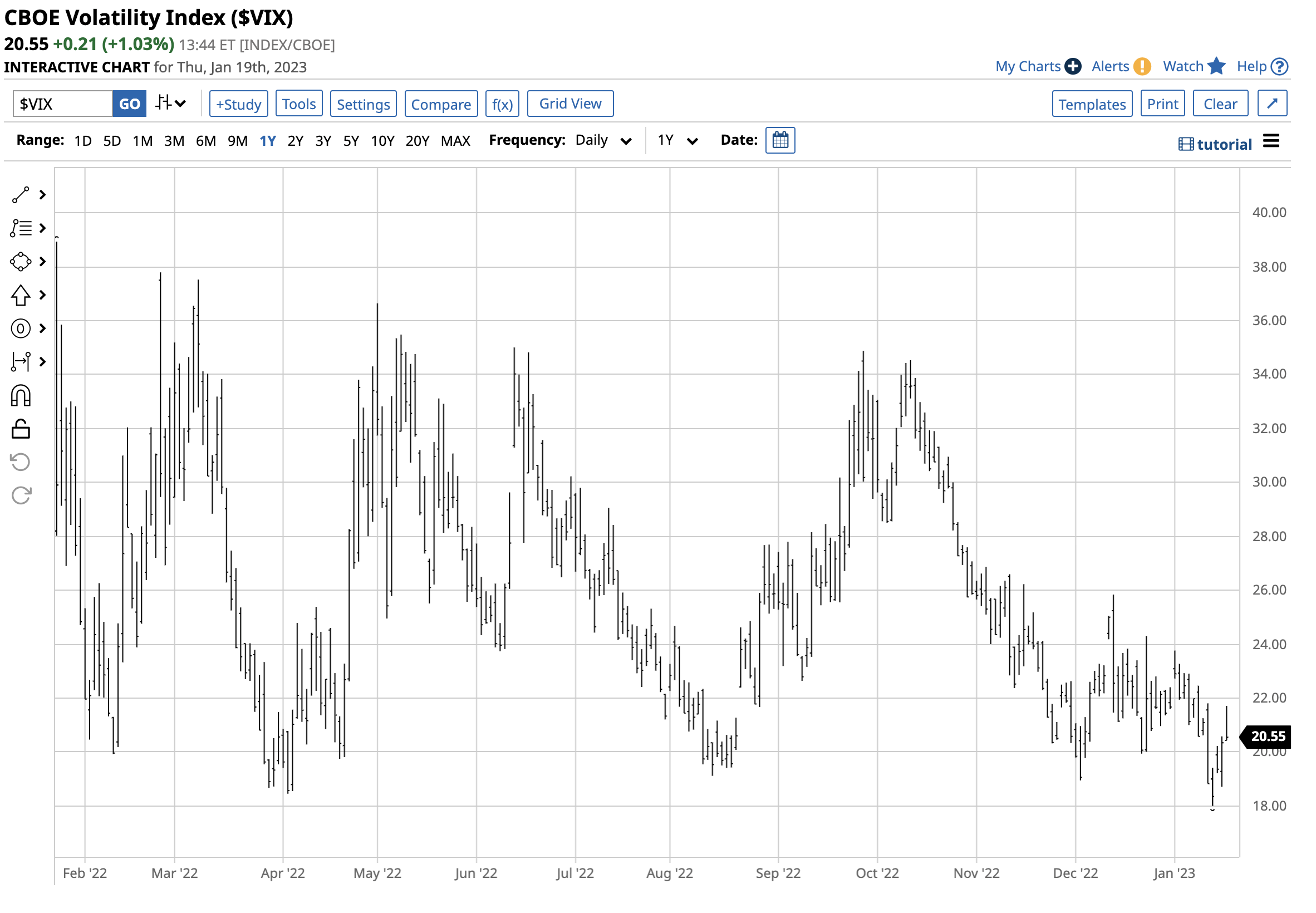

One-Year Chart of the VIX Index (Barchart)

The short-term chart shows that moves below 20 in the VIX have been buying opportunities over the past year.

VXX is a liquid product

The fund summary for the iPath S&P 500 VIX Short-Term Futures ETN product states:

Fund Profile for the VXX Product (Seeking Alpha)

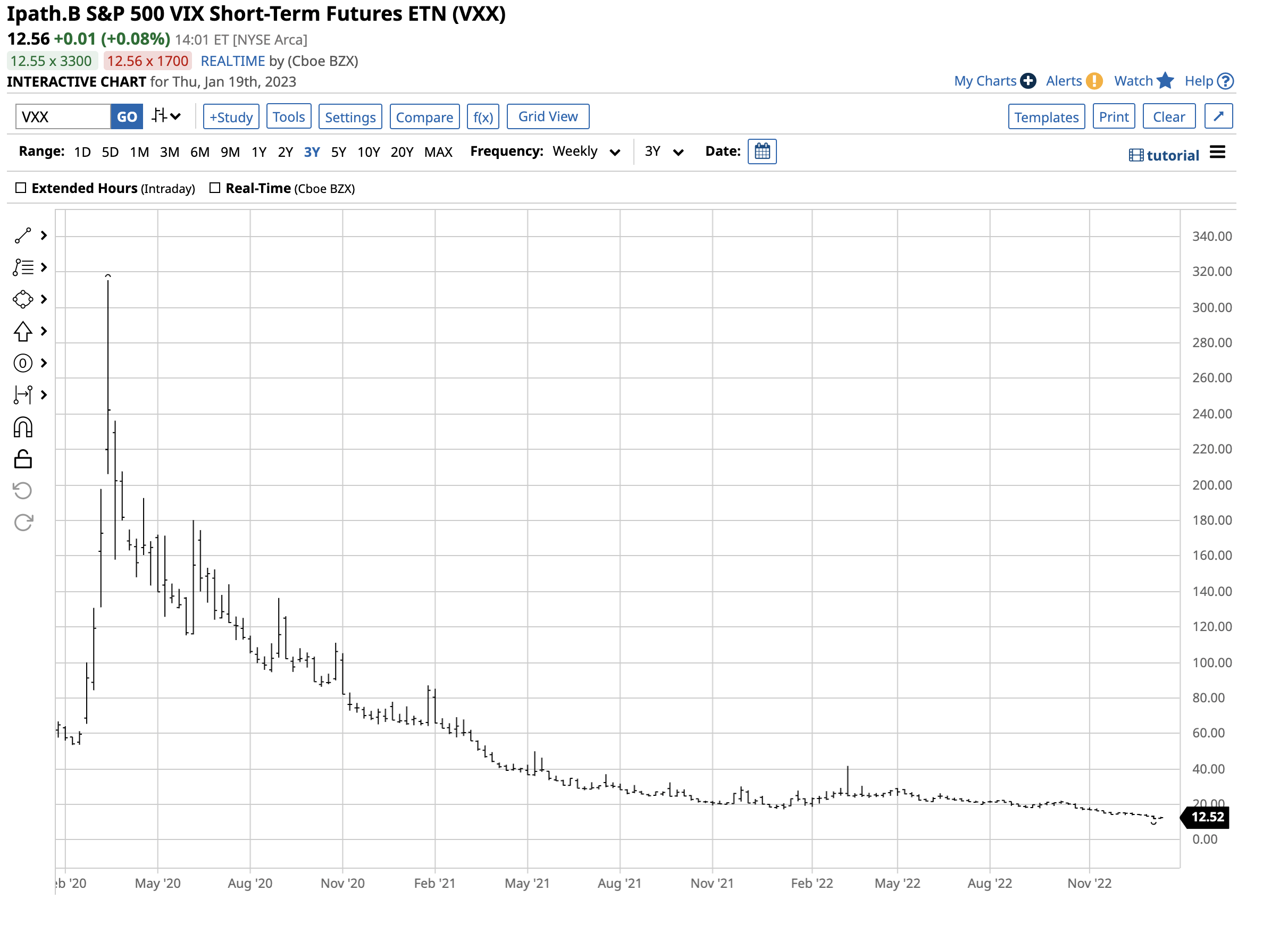

At $12.53 per share on January 19, VXX had $317.60 million in assets under management. VXX trades an average of over 6.9 million shares daily and charges an 0.89% management fee. When the VIX rose to over 85 in March 2020, the VXX product went along for the bullish ride.

Three-Year Chart of the VXX Product (Barchart)

The chart shows the split-adjusted rise to $315.36 per share in mid-March 2020.

Trading, not investing with VXX – planning and discipline are critical

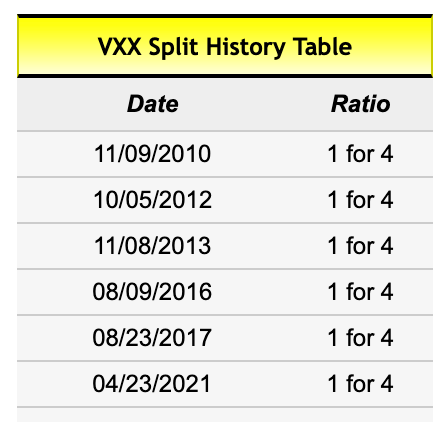

VXX has a history of reverse splits where owners receive one share for every four shares of holdings.

VX Split History (Splithistory.com)

The chart shows the most recent one-for-four reverse share split came in April 2021. VXX is not a product for long-term investors, but it’s a valuable tool for short-term traders with their fingers on the pulse of markets. A long-term position in VXX will likely wind up as a dust collector in portfolios.

Approaching VXX with a dynamic risk-reward plan, including time and price targets and stops, is the optimal strategy for trading the product that moves higher and lower with the VIX index. The objective is to contain losses and ride profits using trailing stops when catching a bullish wave in VXX alongside a downdraft in the S&P 500.

The potential for significant stock market corrections remains high in 2023, and the VXX is a trading product that could hedge or enhance portfolios for dynamic traders.

Be the first to comment