Getty Images

Dear readers/followers,

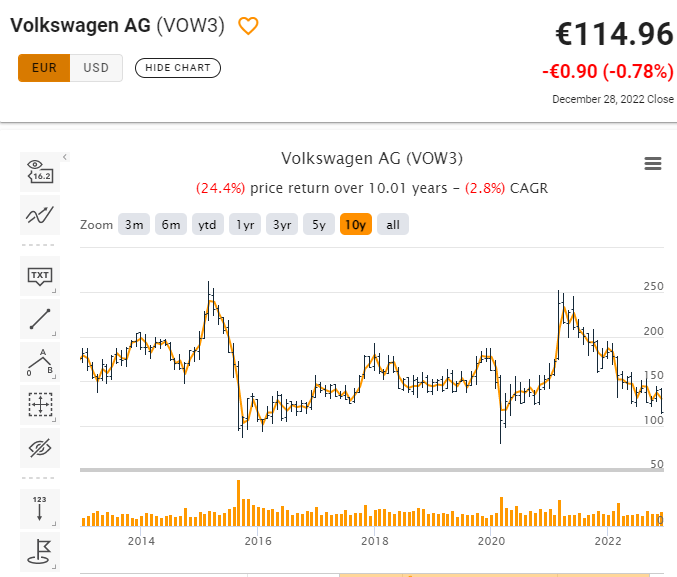

Volkswagen (OTCPK:VWAGY) (OTC:VLKPF) has long been on my list of companies to own and invest in. While the company has gone through multiple scandals and has been very volatile as an investment over the past couple of years, the native share has seen highs of over €300 over the past 3 years, and currently trades at no more than €147.8. At COVID-19 lows, the company was no more than €103, at times closing in on a double-digit share price.

This would imply that Volkswagen is a risky and at times troubled company on a fundamental level. But there is very little truth in that assertion.

Volkswagen – Looking at the basics

Volkswagen is one of the largest car businesses on the planet. While it might not be as “sexy”, as say Tesla (TSLA), it’s a solid business with an 85+ year history with headquarters in the town of Wolfsburg in Germany.

Its unfortunate past involves its creation under the banner of the Nazi party (German Labour Front), which was revived post-WW2 by the British army officer Ivan Hirst.

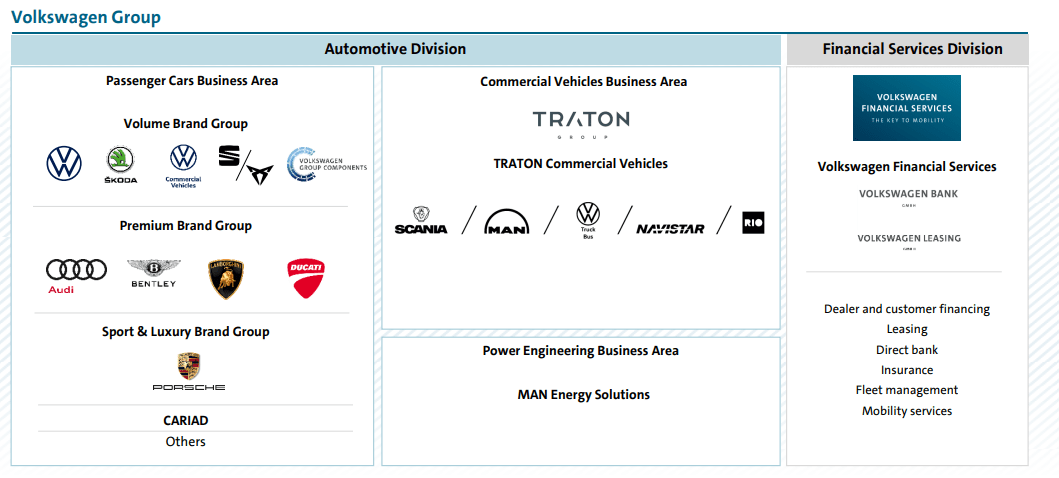

The company is most well known for the iconic Beetle car, and it’s more importantly the flagship brand of the Volkswagen Group, which involves such storied brands as VW, Audi, Bentley, Ducati, Porsche, Jetta, Scout, Seat, Skoda and Traton (OTCPK:TRATF). These are owned to various degrees – most of them 100%-owned by the Volkswagen Group.

VW IR (VW IR)

Now, those of you from NA might not have heard much about Skoda and Seat – they’re sort of European budget brands that hold a similar market-leading position to US budget brands, except they’re over here. Instead of buying typical budget brands you might know, people elect to buy a Skoda or a Seat instead – Seat, especially in Southern Europe.

Volkswagen AG was the largest automotive manufacturer in the world by sales between the years 2016-2017. Like many other brands, its main market is currently China, which delivers around 40 of annual sales and profits.

The company’s relationship with Porsche has been a complex one because Ferdinand Porsche was initially hired by Hitler for the company project, and the first car from Porsche used plenty of Beetle cars, and over the years, Porsches have used many components from the VW shelf, as well as seen shared production for many of its models. There’s also a very complex ownership dynamic, which I describe closer in my Porsche (OTCPK:POAHY) articles.

VW IR (VW IR)

The company produces a myriad of different models, and its lineup of cars can even be market-dependent, with some models available only in some markets.

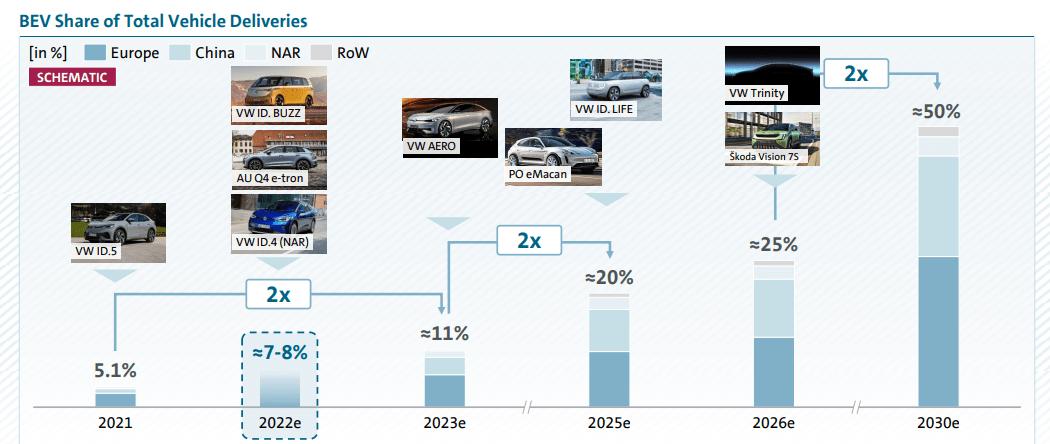

Sales figures are interesting. The best-selling VW area aside from China is Western Europe. The company sold a total of 4.89M cars for 2021, which is 8.1% negative YoY compared to 2020 – however, the sales numbers in NA were up 13%, with every other market down except APAC/Middle East. The proportion of VW BEVs and hybrid vehicles nearly doubled for VW that year – but this is still only 7.5% of the total deliveries for all of 2021, though that number in Europe is 19.3%, not below 10%. A total of 77,100 BEVs (+437% YoY) were delivered in China, including more than 70,000 from the ID. family, making Volkswagen one of the five biggest BEV providers in China. The worldwide most popular BEV was the ID.4.

On a top level, the company’s overall financial fundamentals are solid and in line with other companies in the same segment.

VW IR (VW IR)

Other than that, the SUV craze continues. VW’s non-BEV sales are topped with SUVs, with the Tiguan close to the top there. 40% of the company’s total deliveries are SUVs of some sort – but the best-selling car in Germany despite all this was still uncontested – it’s the Golf.

So VW still has some work to do convincing people to go electric. The Tiguan was the best-selling model in the company’s lineup, as it has been since 2019 when it beat out the Golf on a global basis, and after that, it’s the Polo, The Passat, the Lavida and the Jetta – again, all global numbers.

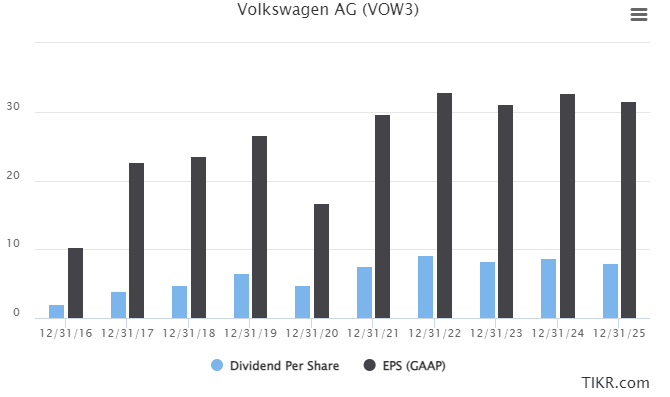

Volkswagen has, despite share price volatility, remained a relatively stable payor of dividends. It’s also a stable-rated company in terms of credit – BBB+ from S&P and an A3 from Moody’s, confirming the safety you get here by investing. The dividends for the preference share which I am writing about, which are tied strictly to company earnings, have generally rewarded shareholders with a comparatively high payout based on solid and stable overall trends. Here is how that relationship, generally speaking, looks.

Volkswagen EPS/Dividends (TIKR.com)

As you can see, the coming free years are currently all for relative income stability, with some ups, and downs, but not much.

Volkswagen is an automotive manufacturer, meaning that it’s fairly closely tied to the cyclicality of the overall market. We can observe this when we look at how violently the company moves up and down. Take a look at the 10-year trend.

Volkswagen 10-year RoR (TIKR.com)

As you can see, Volkswagen hasn’t been a very good investment – at least if you fail to pay attention to valuation trends, which are a bit “core/fundamental” as things are here. The same thing that’s true for any automotive company is also true for Volkswagen. If you buy this business at a too-high valuation, your money can be lost for a decade or more, given the negative RoR you’d be getting in a downcycle, even when including the potential of an attractive dividend payout.

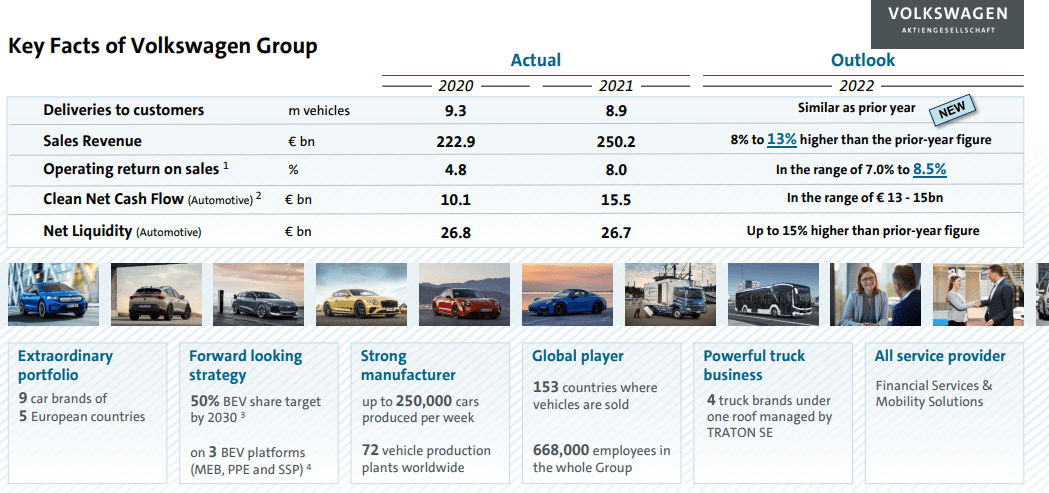

Recent results confirm the challenges the company is under, which is somewhat pressuring the company’s valuation here. Deliveries are down nearly 13% YoY, and this negative is coming mostly due to China and supply chain issues/part availability.

However, deliveries of BEVs are up 245%, and the share of the total is up to 6% of sales, up from 4.2% YoY. Meanwhile, price bumps and FDX mean that group sales revenue is up 8.8% despite deliveries being down, and that includes around close to €8B from Navistar which has been consolidated into the company since YoY. Also, the company’s financial service arm is seeing continued success despite the macro challenges here.

Pre-Tax profit as a result is up almost €3b to €17B, and this includes an impairment loss of close to €2B for Argo AI, meaning that net profit is up to €12.8B for the company. The company’s net cash flow continues to show stability, and the company’s CAPEX ratio (to sales) stays stable at around 3.8-4.3%.

Volkswagen has no liquidity or cash issues, with net liquidity coming in at €31.6B thanks to successful placement of hybrid notes, as well as a massive cash inflow from the finally-completed Porsche IPO – though note that the IPO is not yet included in this number.

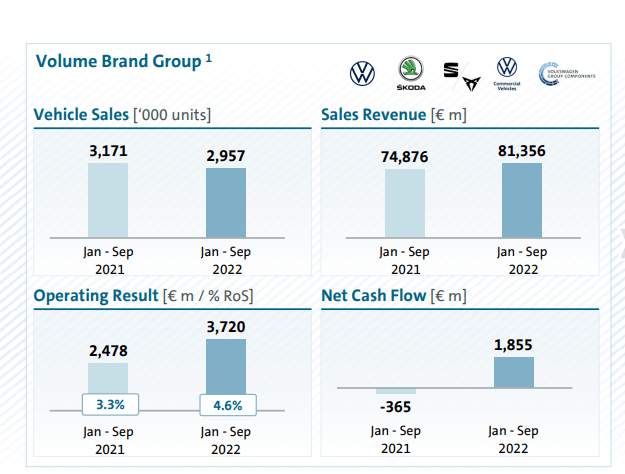

The company is employing over 660,000 people worldwide, and produces its products in 72 vehicle plants across the globe, with a majority in Europe (34 of them). Internally, the company splits its sales/brands between the “volume brands”, which are VW, Skoda, Seat, and similar…

VW IR (VW IR)

…and the Premium Brand group, which holds Audi, Bentley, Lamborghini and Ducati. Tendentially, premium cars tend to give better margins, and indeed the relative operating result growth and margins are better for this segment, despite sales being far higher in the volume segment. A group like VW needs both though. But both Lambo and Bentley performed admirably during the last few months.

So what’s Porsche, you might ask?

Well, that’s what VW considers the “Motorsport & Luxury Brand Group”, which has only one brand – Porsche. The results here are absolutely stellar, and Porsche alone has half the sales of all other premium brands combined, and three-quarters of the net cash flow. That should indicate to you how important Porsche is to the company as a cash flow generator.

There’s plenty to like about Volkswagen’s coming model refreshment and the lineup the company presents – both in and outside of Europe. The company will bring the Tavendor SUV to market in China, Skoda is bringing a new concept car, Seat is presenting the new Tarraco, and Audi is bringing new concepts and products to market. Lamborghini which is part of the business is bringing out the new Urus super-SUV, and Bentley is bringing out the new Flying Spur Speed. Porsche, meanwhile, is driving innovation with its 911 GT3 RS, and perhaps most importantly for VW, especially in Europe, the company is bringing out the ID. Buzz Cargo, their commercial e-mobility solution.

All in all and despite downturns here due to issues in production and market weakness, there is much to like about Volkswagen in a way that has had me waiting on the sidelines for the price of the company to drop below a certain level – which we have now finally seen.

For that reason – valuation, I’m going to be favorable on Volkswagen here – let me show you what I like about the current price.

Volkswagen’s Valuation

Volkswagen plays in an interesting group of peers, both European, American, and Asian, though few but the largest company can really measure up in Volkswagen in terms of sales. Even comparing it to something like Tesla is laughable to a conservative, dividend-oriented value investor like myself, because Volkswagen trades at a below-5x normalized P/E while yielding almost 6% – over 6% for the preferred share that we are looking at, and that yield is relatively well-covered by today’s numbers.

VW’s current trends are looking very attractive. On a sales multiple, VW is used to trading close to 0.5x sales. The company competes with similar operating margins to other car manufacturers, but because it has a high amount of premium and luxury car sales, that margin is higher than some of its peers, coming to 8.6% year-to-date OM.

Well, you might say, Tesla has twice that (or close to) – and yeah, it currently does. But VW also doesn’t trade at a 30x+ P/E ratio, and VW has a solid dividend that’s covered by years and years of tradition, as well as a history going back over 80 years. The two, to my mind, do not compare for conservative investors. One wins a spot in a portfolio, the other does not – the other here being TSLA.

Other peers in the car industry are Toyota (TM), Stellantis (STLA), Mercedes (OTCPK:MBGAF), BMW (OTCPK:BMWYY), Honda (HMC), and Hyundai (OTCPK:HYMLF). I cover many of these and own almost all of them as well. Looking at the valuation of this peer group is something I do quite often. Whenever one of them drops below that elusive 1x revenue number (except Honda, that one’s trading below 0.5x before it gets interesting due to that more difficult mix), they may become interesting.

Volkswagen, from a peer-based perspective, is interesting here because it’s now at 0.85x. It’s also below a normalized 6x TEV/EBITDA, which again is below par here, despite good results for the business.

The company’s share price targets have been significantly lowered since the EV craze, when analysts thought the company was worth €300/share for the common. That’s down to €211.9 at an average base, with a range starting at €148 and going up to €328 (those EV-maniacs are still there…).

However, the more important thing here is that Volkswagen is now trading below even the bottom-line share price target.

All of the numbers I give to you are just a comparative/financial mathematical way of saying that Volkswagen is now more undervalued than it has been in some time.

That is of interest to me. Even to a €200/share PT, the company has close to a 40% normalized upside here. The yield is solid – even if the dividend for the fiscal of 2022 goes down a bit, it’s still a very good yield, and you can’t argue with the company’s fundamentals. Because how do you argue with a company whose annual sales revenues are more than the total GDP of over 30 entire nations, including countries like Slovakia, Ecuador, Oman, Bulgaria, Algeria, Hungary, and Ukraine (pre-war)? It’s not just revenues – the company makes an 8%+ operating margin from those numbers.

Investing in Volkswagen’s preferred share, to me, is like investing in a Bond. You could go either for the native. During the past crisis, I did. This time, I’m going for the pref. Unlike typical preferred shares, this one moves at a far wider range than others – and the yield is better.

I also think you should consider the prefs because the VW prefs are typical with much higher liquidity – they don’t have voting rights, but the chances of you exercising that if you’re reading this is very small, and they also come with priority payout in the case of any issues.

So, here is my initiatory stance for Volkswagen.

Volkswagen Thesis

- Volkswagen is a world-leading car manufacturer that produces some of the most beloved cars on earth, no matter what geography you’re looking at. The company has solid fundamentals, and a solid dividend, and comes with owning Porsche in a way.

- The company is also currently very cheap, after a significant share price decline, and I, therefore, welcome these changes in order to once again start investing in the share.

- My choice is the preferred share – it’s my belief that this should be yours as well. My PT for the pref is around €170, making it around 40% upside from today’s share price. The pref trades at native ticker VOW3.

- The company is a “Buy” for me here.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company fulfills every single one of my investment criteria, and is a “Buy”.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment