dibrova/iStock via Getty Images

Last January, I published “VNQ: Commercial Property Prices May Plummet As Interest Rates Rise,” warning investors of the negative potential rising interest rates would likely have on the REIT sector. The first point of the summary of that article stated, “While 2021 was the year of rising inflation, early evidence shows 2022 is likely to be the year of rising interest rates.” That outlook played out almost exactly as expected, with long-term interest rates doubling since then, negatively impacting economic growth and property valuations. The REIT fund VNQ lost around 20% of its value, underperforming the S&P 500 by a wide degree.

Many investors may be more interested in the popular REIT ETF, Vanguard Real Estate ETF (NYSEARCA:VNQ), this year since its yield is slightly higher. Valuations across the REIT sector are certainly lower, providing a potential cushion. With core inflation moderating, interest rates are also not rising and seem unlikely to. That said, the US economy is slowing more quickly than in the past, causing many companies to experience financial strain that may decrease demand for commercial property assets. The retail, office, and lodging segments appear at the greatest risk. Additionally, the rise in interest rates may not yet be fully priced into the valuation of VNQ and commercial property assets.

Overall, while many individual REITs within VNQ may be strong investments, I believe 2023 may be a more difficult year for the fund than 2022 due to the potential rise in insolvency (or bankruptcy) for certain REITs – stemming from adverse economic and capital market conditions.

Interest Rates Not Fully Priced Into VNQ

Over the past year, the US real estate sector has performed about as poorly as the Technology Sector (XLK), although Consumer Discretionary (XLY) has fared worse with a 36% decline in 2022. Generally speaking, these are the most interest rate-sensitive sectors since firms in those sectors are valued on usually consistent future cash flows, typically with higher “P/E” ratios. Sectors with less consistent cash flows, such as mining, industrials, and energy, usually carry lower “P/E” ratios, making their valuations less exposed to changes in interest rates. Put simply, as bond yields rise, REITs need higher profits to compete for investors.

In a sense, REITs are doubly exposed to changes in interest rates. In the short-term, higher interest rates lower the fair value of REIT cash flows. However, the rise in mortgage rates also decreases the potential cash-flows of commercial property investments, often causing “Capitalization Rates” to rise at the expense of property valuations. If extended long enough, a decline in property valuations can cause REITs to have abnormally high loan-to-value ratios on assets, increasing solvency risks. Commercial property sales volumes declined last year while capitalization rates rose but were still superior to pre-pandemic levels.

Commercial property transactions are often planned well in advance, and data lags, so I believe we have hardly seen the full extent of higher interest rates on the commercial property market. Interest rates rose at the fastest pace in recent history last year, so considering the real estate market is far less liquid, it is understandable if it ends up lagging market trends significantly. One strong indication comes from REIT equity sales, which declined by a staggering 70% last year to the lowest since 2009. As less market money flows into the sector, overall commercial property sales will likely reduce substantially and increase capitalization rates.

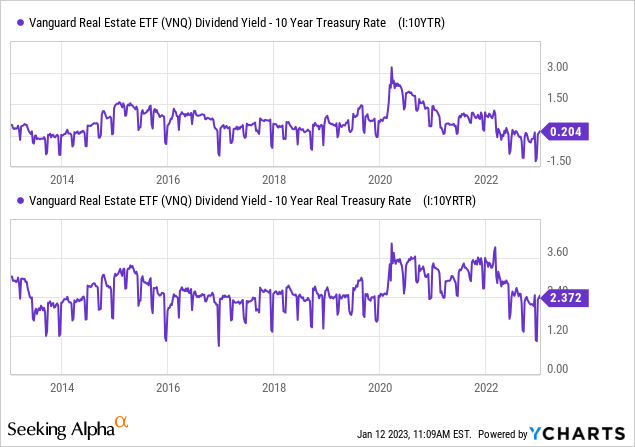

VNQ itself remains slightly expensive compared to 10-year Treasury bonds. The fund’s yield is only around 20 bp above the 10-year Treasury bond, while it is usually around 100 to 150 bps higher. Of course, many expect VNQ’s dividend to rise with inflation, making it more comparable to the “real” or “inflation-adjusted” bond rate. VNQ’s yield is currently 2.37% above the “real” 10-year Treasury bond yield, while it usually is ~2.5-3% above it. See below:

Based on these metrics, I estimate VNQ’s yield is around 100 to 150 bps lower than it “should” be given today’s Treasury bond yield. Given Treasury bonds are the “risk-free” asset, they likely offer a superior risk-to-reward trade off than VNQ, given their yield today. VNQ’s yield would need closer to 4.7% for its spread to the Treasury rate to be more relative to normal levels. Importantly, VNQ would need to decline by around 20% in value for its yield to reach that level. However, it’s only around 10% overvalued if we compare its yield to the “real” or “inflation-adjusted” Treasury rate.

In my view, it is not necessarily likely that VNQ’s dividend will rise with inflation. With higher mortgage rates in 2023, interest costs for REITs will likely trend much higher over time, absorbing much of the potential equity income. Mortgage rates may decline, but I do not believe they will fall below 4% over the next decade due to the persistence of many inflationary factors. For example, food inflation continues to trend higher (10.4% YoY), and higher food costs are likely a net negative for REITs since they lower household discretionary spending capacity. Indeed, with the ongoing rise in recessionary indications, and immense strain on numerous REIT segments, I believe many of VNQ’s holdings could see large income declines this year – some may not survive.

Recession Likely To Hamper VNQ’s Dividend

In my view, the potential impact of interest rates still presents moderate downside risk for virtually all REITs. That said, the effect of a possible recession gives an even more significant risk factor concentrated among some REIT segments. At the end of last year, the commercial brokerage giant CBRE Group (CBRE) published its 2023 market outlook. While CBRE is typically bullish on the commercial market, this report was one of the most bearish I have ever seen published by CBRE. CBRE anticipates recession-related trends to bring sensible investment and leasing activity declines, a continued rise in capitalization rates, and decreased sales volumes.

According to the report, the office, hotel, and retail segments carry the most significant recession risks. These three segments have taken an enormous hit since 2020 as many companies look to switch toward work-from-home or hybrid work programs, with many decreasing business travel (negatively impacting lodging). The retail segment is also under significant strain, with numerous consumer discretionary firms, such as Bed Bath & Beyond (BBBY), Kohl’s (KSS), the theater company AMC (AMC), and others experiencing significant business declines.

In my view, the retail property segment is the single riskiest in 2023 since I believe numerous large retail firms are likely to face bankruptcy this year, likely leading to significant revenue declines for retail REITs. The office segment has seen a massive rise in vacancy rates over the past two years, continuing to trend higher. CBRE sees an opportunity in office “We Space,” catered toward short-term leases and hybrid work; however, I doubt this segment is as strong as many believe, considering the unending rise in vacancies and broader market transition toward work-from-home models. Office REITs may retain value through conversion toward residential or industrial, but I believe relatively few commercial office properties can successfully make that transition. Lastly, lower revenue and rising wages have greatly hampered most hotels, making the REIT segment extremely risky, given the ongoing decrease in household financial stability.

While these three REIT segments appear risky and highly exposed to a recession, there are some “diamonds in the rough.” In general, high-end hotels, luxury retail space, and prime office properties are still seeing strong demand, with some growing faster than before the pandemic. This trend speaks to the broader bifurcation among REITs; as demand for most commercial property falls (primarily due to permanent societal and technological changes), companies and people are only willing to invest in or spend on the “best of the best” properties.

VNQ invests in the entire US REIT sector. It carries higher exposure to “specialized” (mostly data-center and telecom) and industrial REITs, which, in my view, have far lower immediate economic risk than hotels, offices, and retail. That said, I estimate around a third of VNQ’s total holdings carry sizeable direct exposure to an economic recession. In my view, many of these REITs are already at high risk of eventual failure; a recession will only accelerate the process. Importantly, most REITs operate with very thin margins and high fixed overhead costs. So, it only takes a slight 5-15% decline in sales (or rise in vacancy/non-payment) to eliminate all operating cash-flows.

The Bottom Line

In 2008, REITs were hit by a large but short-lasting market crash. Today, I believe losses will last far longer because many commercial properties are effective “zombie companies.” that are struggling to remain relevant within a fundamentally changing economic structure – ultimately stemming from technological and social change that limits demand for many properties. Whether this change is positive or negative is unclear, but in my opinion, it is undeniably evident in market trends and almost certain to accelerate in a recessionary scenario. Indeed, these trends began well-before 2020 but were greatly accelerated by that year’s events.

In my opinion, investors would be wise to understand that the definition of “normal” is changing, and it is improbable the economy can return to the “normal” which existed a decade or two ago. Many REITs within VNQ are still tied to the older economic and social structure. One example is hotel REITs that cater to business travel or retail REITs with “big box” stores. Many people who live in large cities may also be aware of the growing “ghost towns” within them from lost (primarily) small business commercial space. While many REITs in those segments still receive “normal” sales, many tenants within those sectors are seemingly on an inevitable path toward bankruptcy or widespread business closures.

I believe VNQ will likely experience a significant decline in its dividend this year due to the expected strain of REITs exposed to these changes. While most REITs in VNQ are not necessarily exposed, those that are may experience such significant declines that I believe VNQ could permanently lose 20-30% of its value from associated bankruptcy risks concentrated among a minority of its holdings. Further, I expect growth in industrial and data center REITs is not likely significant enough to offset these losses. Additionally, the impact of interest rates may create a negative strain for virtually all REITs regardless of their economic risk.

I am very bearish on the fund and would not be surprised to see it fall more this year than last year. Additionally, I do not think VNQ will rebound as quickly as it did in 2020 since the Federal Reserve is unlikely to pursue dovish policies due to chronic inflation strains. Still, while I believe VNQ will decline significantly this year, investors may find opportunity among high-quality REITs in low-risk segments – industrials being a notable example.

Be the first to comment