MartinFredy

It has been a while since my last article on Vista Outdoor (NYSE:VSTO) and plenty has happened in the last few years. If you don’t know the name, that is understandable as Vista’s business was mostly focused on ammunition for firearms in the past – but the company has added numerous outdoor sports businesses over the years. Regarding investments in the company, it is important to know that the entire market dynamic has changed, the business has discussed splitting and the board may be dealing with upheaval. So, it is well past time for an update on how the company is doing, plus a review on its recent results.

Numbers In Review…

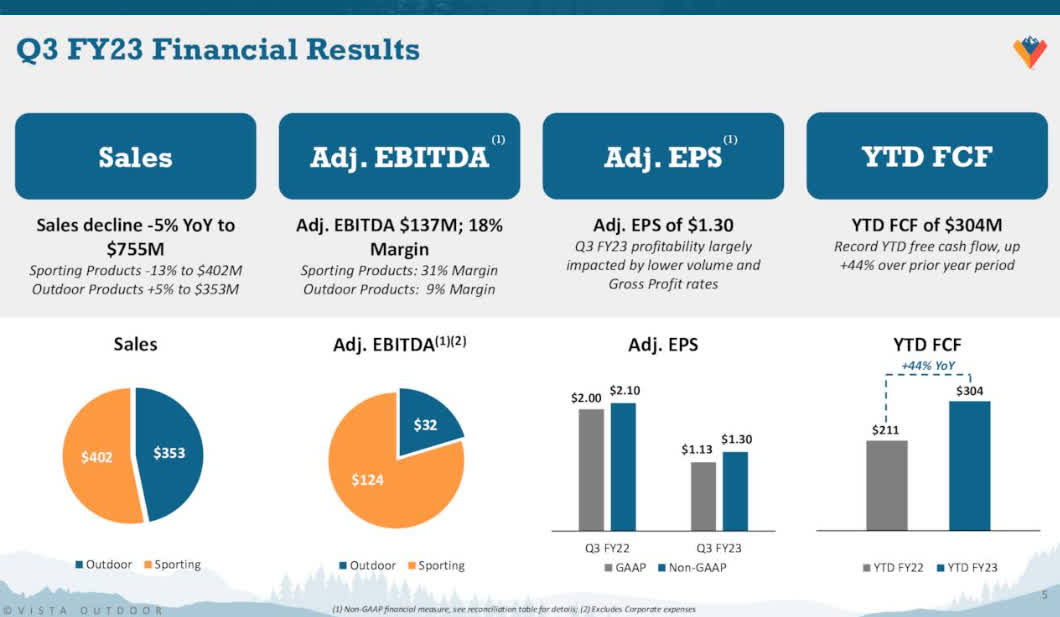

Vista Outdoor reported earnings results on February 2nd, 2023. Vista gave guidance for the future and reported the numbers for their Q3, including mostly good numbers. Results included total revenue of $755 Million for the quarter, this was roughly 5% below Q3 last year but above estimates by $1.28 Million. Non-GAAP EPS of $1.30 beat low analyst estimates by $0.18.

Free Cash Flow (FCF) was a solid $109 Million in Q3, which takes yearly numbers to $304M – 44% higher than past year numbers to date. Outdoor Products had sales of $353 Million, a record for that segment. Segment sales were up 5% over 2022-year numbers. Sporting Products had sales of $402 Million, which is in line with guidance. Sporting segment sales were 13% below YOY numbers. (NOTE: Most of the Sporting Products were in high demand, and very scarce during FY22, which also affected profitability and pricing.)

Forward Guidance & CEO Change…

Starting with the messy business… Vista’s former CEO, Chris Metz, resigned after the board stated they had a loss of confidence in his leadership. The Interim CEO will now be Gary McArthur (on the board since 2015) and the rest of the execs remain in place to oversee future business. The board mentioned that this resignation was due to the loss of confidence and had nothing to do with financial issues – so if we take them at their word, we can assume this was regarding the future vision, or possibly personality issues amongst the board.

Mr. McArthur set the expected FY23 full year to $3.06-3.08 Billion, vs. the previous $3.11B, which lowers the yearly guidance by about one to two percent. They expect FY23 FCF to be at $320-350 Million at the end of next quarter. This works out to a yearly FCF of roughly one fifth the company’s overall market cap, showing it is likely undervalued.

Segments and Upcoming Spin-Off…

To understand what is coming, we must understand the businesses and what each segment will be after the split.

Outdoor Products is the more politically correct portion of the business. This focuses on what would normally be considered sporting goods sold at retailers. The companies include Bushnell (rangefinders and rifle scopes), CamelBak (water bottles and hiking products), Camp Chef (outdoor cooking products and grills), Fox Racing (bike/motorbike clothing and helmets), Simms Fishing (waders, clothing, etc.) and a few more companies that tend to have some overlap with each other.

Outdoor segment sales are roughly $1.2-1.3 Billion per year, accounting for less than one quarter of current Vista profits. This business is expected to have very low debt, stated at less than 1x at spinoff, and will be focused on organic growth and M&A. Considering they state a long term 1x-2x debt ratio, it is a highly probable guess this company would be looking at M&A relatively quickly. Since this side of the business is more PC, it is likely they get a better market valuation post spin-off.

Earnings Slide 4 (Q3 results from earnings slide (Seeking Alpha))

Sporting Products is the more profitable business, but also far less politically correct. The Sporting side includes mostly ammunition and gunpowder sales. The companies include Federal, CCI, Speer, Alliant Powder and the perfectly timed bargain purchase of Remington Ammunition out of bankruptcy for a mere $81.4 Million. (Remington sales were roughly $200 Million before the ammunition surge in 2020, so it’s safe to say Vista has already more than tripled their money on this purchase.)

It is hard to make it clearer that the Vista Outdoor ammunition and powder companies are, together, a MASSIVE portion of the North American ammunition market. Only two other North American companies produce good amounts of ammunition– Olin Corporation (OLN) and AMMO, Inc. (POWW). Both competitors have some issues, as Olin gains only 10-15% profit from ammo sales.

The second U.S. company that competes with Vista, Ammo, Inc., has had some highly questionable management issues which have them dealing with proxy fights and a CSO, amongst others, placed on leave due to possible misconduct. Much of this issue is surrounding the purchase of Gunbroker.com which Ammo, Inc. is already planning to spin-off less than one year after its original purchase. So, politics and the industry they sell to aside, it is clear this is a profitable market and Vista has a large portion of it.

Sporting segment sales are $1.8 Billion per year and have a roughly 33% profit margin. Sales are somewhat cyclical, however ammunition and powder is a consumable product that most people will keep purchasing – as well as governments. This business segment, post spin-off, is expected to have 1.7-2x debt ratio, and they plan to reduce that debt quickly as well as institute a dividend. Since this side of the business is less PC, it is likely they get a low market valuation post spin-off – even though it is the more profitable side. (It is important to note, it is hard to see how they will grow the ammunition sales without the firearm enthusiast market growing – as they are already the largest company making ammunition.)

Valuation…

It is always hard to provide fair value for Vista Outdoor, as there is no other real company to compare it with. Ammo, Inc. is the only other publicly traded ammunition-focused company and it is much smaller. Olin Corp gets only 10-15% of their sales from ammunition, so they don’t exactly correlate. It is however important to note that Vista, and the future Sporting Products spinoff, gets a much larger percentage of North American ammunition sales from consumers than any other.

It is easy to see that a company with a low PE (4.2) a good profit margin and EBITDA rating is undervalued, but the challenge is deciding if that matters to the market.

Author compiled data (Source: Author-gathered data from Seeking Alpha)

Final Thoughts…

While growth depends on the consumer for both sides of the business, the two spin-offs will be rather different in growth trajectory. The Outdoor Product side will have little-to-no debt and will be looking at M&A. So, this side depends on what M&A deals they find, the prices they pay, as well as interest in the greater outdoor sport/event market.

The Sporting/Ammunition market is a bit more intriguing to me, as it is less dependent on M&A – though it also has less chance for growth. Sporting and ammunition is likely to continue delivering profits as long as society allows firearms to be bought and sold. With a dividend expected, and a reduction in debt, the ammunition business is likely to do well as the company looks to return profits to stockholders. The future stock profits of the sporting business really depends on the dividend policy set out by the new board as well as the inflationary cost of goods – namely if you believe, as I do, that the company can pass price increases along to the consumer and it keeps its profit margins.

Given the above information, anyone who owns VSTO stock and wishes to be free from the non-PC ammunition market should take the spin-off outdoor business and hope management makes more smart M&A decisions, as this is likely a safe way forward. Folks looking at a dividend and a stable income producer are likely to do better with the “Sporting” side of the business – as its ammunition is a cash-cow business that is unlikely to have a lack of demand supplying consumable products to a growing market.

Be the first to comment