{kind=link}

Source: Author, based on company filings.

Summary

Village Farms International (VFF) is a greenhouse tomato grower which owns a majority stake in one of the best-run Canadian cannabis companies. Pure Sunfarms is a very successful cannabis business, with terrific gross margins and very low operating costs. It has 44% net margins over the first three quarters of 2019, which is phenomenal when other Canadian cannabis companies are losing money. If Pure Sunfarms was publicly traded, they would be very attractive.

However, Village Farms’ core business appears to have been unprofitable since mid-2017. This has led to the company needing to raise money during the midst of a market collapse – diluting shareholders at the “bottom.” Further, Pure Sunfarms is partly owned by a co-owner which has recently refused to pay its bills and shows signs of being in financial distress. That may or may not present further problems down the line, although the two have at least stopped bickering for now.

I will stay on the sidelines.

The Tomato Business

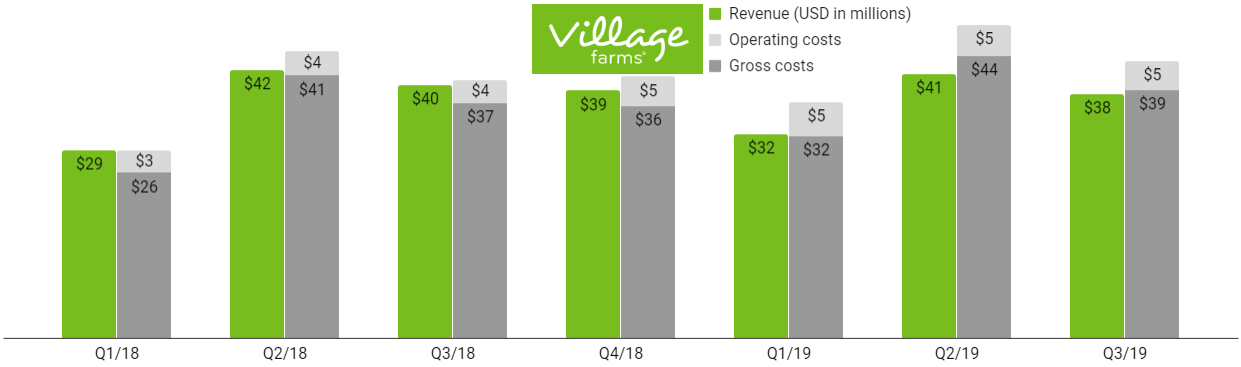

Village Farms’ core business is growing vegetables in greenhouses. The company primarily grows tomatoes, bell peppers, and cucumbers. These products are grown in greenhouses located in British Columbia and in Texas.

This business is very low-margin, or perhaps no margin. Over the past year, Village Farms has negative gross margins, losing $0.52 for every $100 of vegetables it sells on a gross basis. To its credit, Village Farms has very low operating costs, although this is not enough to salvage a profit when you are selling products for less than they cost to grow.

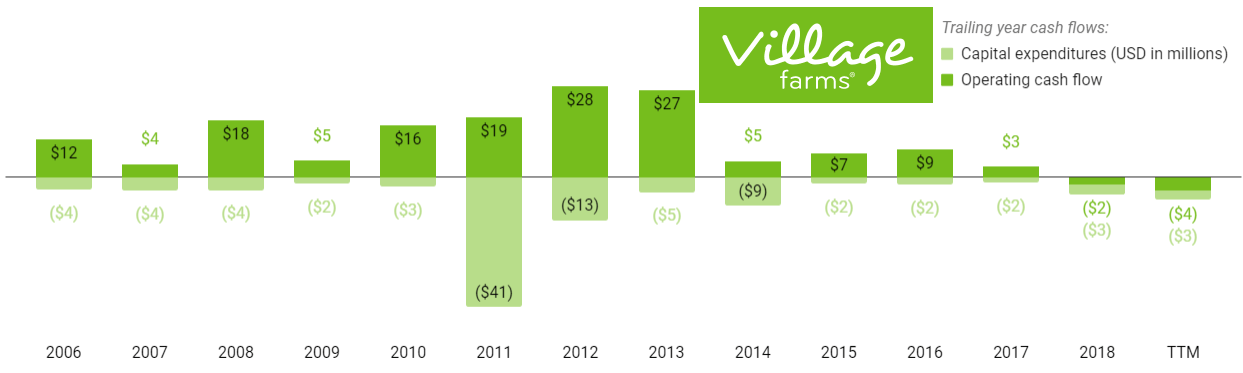

Village Farms’ annual and trailing cash flows in U.S. dollars. The most recent results are from September 30, 2019. Source: Author, based on company filings.

Unprofitable core business: Village Farms is unprofitable on a cash flow basis.

Prior to 2018, the company had generated positive operating cash flow for at least the past decade and was usually generating positive free cash flow as well. Since around mid-2017, Village Farms has been spending more money than it has brought in from the vegetable business, including an operating cash flow deficit in 2018 and a larger operating cash flow deficit over the twelve months ending on September 30, 2019.

The company’s underlying vegetable business appears to be unhealthy, although its losses are relatively small. That said, Village Farms has little cash to absorb this cash flow deficit. The company ended the third quarter of 2019 with only $7 million on its books and a net debt of $27 million, including money due from its joint venture.

Data by YCharts

Data by YCharts

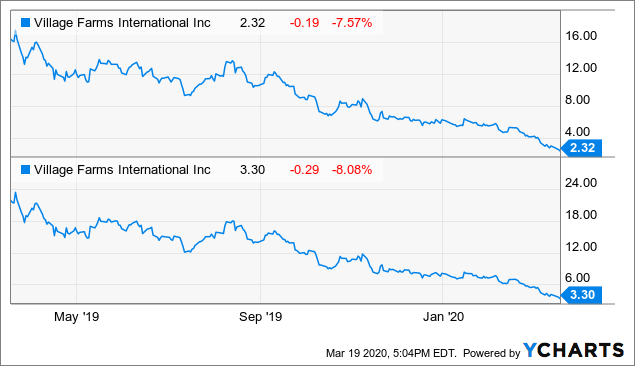

Dilution at the “bottom”: Owing to this weak cash position, Village Farms was forced to raise capital at rock-bottom prices in the midst of an economic meltdown. Village Farms raised C$10 million on March 19, 2020, selling 3.125 million shares for C$3.20/share. This was less than half its market value a month earlier and down 85% from its value one year ago.

Perhaps due to these changing business conditions, Village Farms decided to use some of its Canadian greenhouse capacity to grow cannabis rather than vegetables.

Successful Joint Venture: Pure Sunfarms

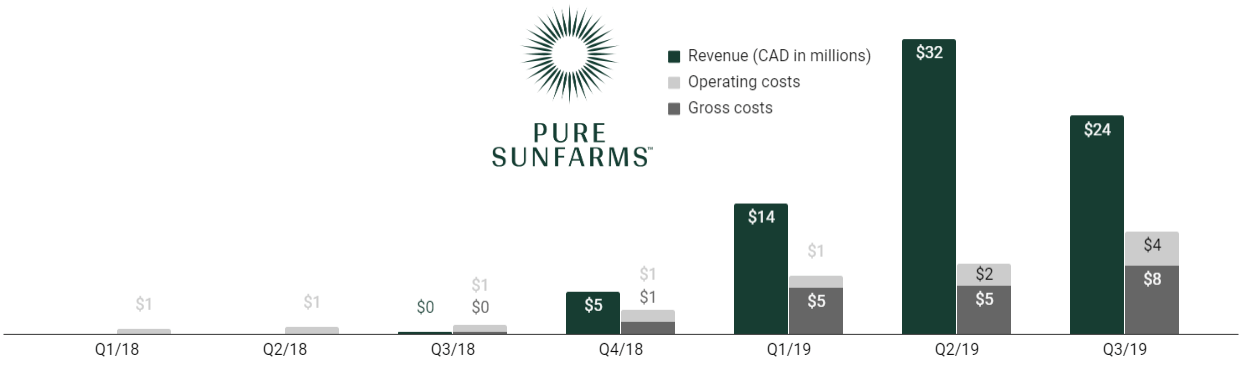

Pure Sunfarms results through the third quarter in Canadian dollars. Source: Author, based on Village Farms filings.

In June 2017, Village Farms entered into a joint venture with Vancouver-based Emerald Health Therapeutics (OTCQX:EMHTF), a very small Canadian licensed producer of cannabis. The two formed Pure Sunfarms, with each company holding 50% of the voting rights. The idea was to combine Village Farms’ greenhouse capacity with Emerald Health’s supposed expertise in cannabis cultivation to grow cannabis for cheap.

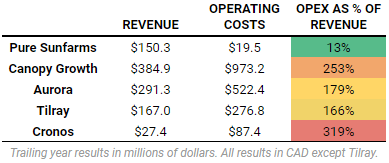

Pure Sunfarms has reasonable operating costs, unlike other pure-play Canadian cannabis producers. Source: Author based on company filings.

Pure Sunfarms has been a great success and is perhaps the most profitable Canadian cannabis company. As with Village Farms, Pure Sunfarms has very low operating costs, especially compared with the other publicly traded Canadian cannabis companies. Many of those companies suffer from extremely poor management which has decided to overspend on posh office spaces and overexpansion rather than keeping costs low and focusing on building a sustainable business.

Pure Sunfarms has been profitable for each of the first three quarters of 2019 owing to its low growing costs and its low operating costs. Cumulatively, the company has reported a net income of C$31 million through three quarters on sales of C$70 million, with net margins of 44%. (This excludes non-cash fair value adjustments which would not be reported under U.S. GAAP accounting.)

Pure Sunfarms products listed on the Ontario Cannabis Store. Source: Ontario Cannabis Store as of March 19, 2020.

Pure Sunfarms initially focused on selling cannabis at wholesale to Emerald Health and other customers, but has subsequently moved towards selling directly to consumers under the Pure Sunfarms brand name.

Pure Sunfarms products are available to consumers in three of Canada’s four largest provinces, with the exception of Quebec. Its dry flower products were the top-selling product in Ontario during the fourth quarter. StockTwits user emdeem closely follows sales on Ontario Cannabis Store (and is a Village Farms shareholder), and he reports that the sales in the first quarter continue to be very strong, although dropping to fourth place as of late February.

In short, Pure Sunfarms is well-run and profitable. Its consumer sales are strong, and it is able to compete on price with any of the other growers, owing to low gross and operating costs. If it was a standalone company, Pure Sunfarms would be a tremendous company and potentially a strong buy depending on its pricing.

However, Pure Sunfarms is not a standalone company. Until recently, it was instead a 50/50 joint venture with bickering parents.

Questionable Business Partner: Dispute With Emerald Health

Emerald Health has poor cash flow and a shaky balance sheet. Source: Author based on Emerald Health filings.

One of my biggest misgivings about Village Farms is the company’s questionable choice in business partners. Pure Sunfarms was formed as a 50/50 joint venture with Emerald Health Therapeutics.

Without going into too many details, Emerald Health has an extremely shaky balance sheet, very poor cash flow, and a slew of related-party transactions with confusingly named insider-owned companies. This has led me to be bearish on the company for years on The Growth Operation, and I remain bearish on it.

Emerald Health’s shaky finances led to a dispute over Pure Sunfarms, which put a bit of a cloud on the company.

Back in April 2018, Emerald Health signed a supply agreement with Pure Sunfarms. Under the terms of that deal, it would purchase 40% of Pure Sunfarms’ cannabis in 2018 and 2019. This was estimate to be about 21,000-24,000 kilograms. This cannabis would be sold at “a pre-determined price per gram.” Their deal further stipulated that if Emerald Health declined to purchase this cannabis, Pure Sunfarms would sell the cannabis to others, but Emerald Health would be responsible for any price difference on Pure Sunfarms’ alternative sale.

Fast forward to October 2019 and Emerald Health had burned through its cash and had few sales to show for it. Over the past year, Emerald Health had generated C$18 million in revenue but had a free cash flow deficit of C$67 million.

Put simply, Emerald Health couldn’t afford 40% of Pure Sunfarms crops, and it didn’t have enough customers to sell that much cannabis. Further, it is likely the the “pre-determined price per gram” was too high – overproduction and under-demand for legal cannabis led to cannabis prices declining significantly in 2019. It is probable that the supply deal in April 2018 did not anticipate how quickly cannabis prices would decline, so Emerald was stuck looking at a deal where it would pay above-market prices for cannabis it couldn’t afford and couldn’t sell.

Rather than try to pay, Emerald chose to walk away from the deal and asserted it owed nothing:

“Under the Supply Agreement, Emerald has the right to purchase, or reject, 40% of the cannabis production of the Joint Venture. If Emerald rejects cannabis offered to it by the Joint Venture, under certain circumstances, Emerald would be obligated to pay the difference between the Purchase Price and the price realized by the Joint Venture.

Emerald believes that under the terms of the Supply Agreement, due to the manner in which the Joint Venture conducted its recent cannabis sales, it does not have a liability to the Joint Venture under the Supply Agreement.”

Source: Emerald Health press release, October 15, 2019

Village Farms immediately disputed this controversial reading of the Pure Sunfarms/Emerald Health supply agreement.

Village Farms press releases:

Over the next several months, the two companies issued a series of increasingly nasty press releases about each other. In these series of press releases, Village Farms and Pure Sunfarms continuously asserted that Emerald Health owed the joint venture about C$6 million. Emerald Health denied those assertions.

Village Farms further offered to pay the C$6 million to Pure Sunfarms, but in return would take ownership of a further slice of Pure Sunfarms, originally estimated at 53.5% ownership from the prior 50/50 deal.

The companies initiated arbitration proceedings on the dispute and reached a settlement agreement earlier this month. Under the terms of the settlement, Emerald forfeited a C$13 million loan it made to Pure Sunfarms, and Pure Sunfarms will release Emerald from all liability for its failure to purchase 40% of Pure Sunfarms’ crop.

More importantly for Village Farms, the settlement agreement increased VFF’s ownership of Pure Sunfarms from 50% to 57.4%. Village Farms also paid an additional C$8.0 million of equity into Pure Sunfarms under the deal. The deal will further cause Pure Sunfarms to recognize an additional C$8.1 million of revenue in 2019 which it had not previously been recognizing due to uncertainty of being paid.

All told, this series of legal maneuvers left Village Farms with a majority stake in Pure Sunfarms but also exposed how unreliable its co-owner is. That unreliable co-owner may or may not be problematic in the future, as Emerald Health continues to own 42.6% of Pure Sunfarms.

Thoughts

In addition to cannabis, Village Farms also has some investments in U.S. hemp farming through Village Farms Hemp (VFF owns 65%) and through Arkansas Green and Gold Hemp (VFF owns 60% directly). Neither of these operations is large, and neither was making any revenue as of September 30, 2019. It is unclear whether these investments will pay any dividends given headlines like these: Hemp prices plunge as CBD demand falls short in a ‘grossly oversupplied’ market (Financial Post, January 2020).

If this were an article about Pure Sunfarms as a pure-play company, I would recommend purchasing shares. Its financials are perhaps the best in the sector.

However, investors cannot invest directly in Pure Sunfarms. Instead, we can only invest in Village Farms (or Emerald Health). I do not find that investment appealing for three reasons:

- Village Farms has a shaky balance sheet. This has led to the company having to raise capital at the “bottom” of a crash on March 19, 2020.

- Village Farms’ core business has not been profitable since mid-2017. Perhaps management can turn this business around, but if not, it threatens to be a drain on the company’s resources.

- Pure Sunfarms is terrific, but its ownership is shared with a financially distressed company that has tried to avoid paying its bills in the recent past.

These issues give me pause, as I would prefer not to hold shares of a company with such a poor balance sheet, with poor cash flow, and with a continued relationship to a potentially unsavory business partner. Thus, I will stay on the sidelines.

Happy investing!

Make better cannabis investments with better information

The Growth Operation is the largest community of cannabis investors on Seeking Alpha. During difficult market conditions, our active chat room and daily news updates help investors make sense of the rapidly-evolving cannabis market. The Growth Operation also includes interactive data, illustrating market sales trends and highlighting companies with best-of-breed financial performance.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment