diegograndi

VICI Properties (NYSE:VICI) has somehow become a very popular net lease REIT among investors in spite of its focus on casino real estate assets. The stock is trading at notable premiums to arguably higher quality net lease REIT peers, as investors seem to be giving too much credit to the slightly more attractive lease terms and not enough caution to the underlying risk. Pro-forma for the latest deal to buy out the rest of MGM Grand, leverage will be among the highest in the net lease sector. The stock’s valuations look very dangerous considering that NNN REITs in general have seen valuations sell off.

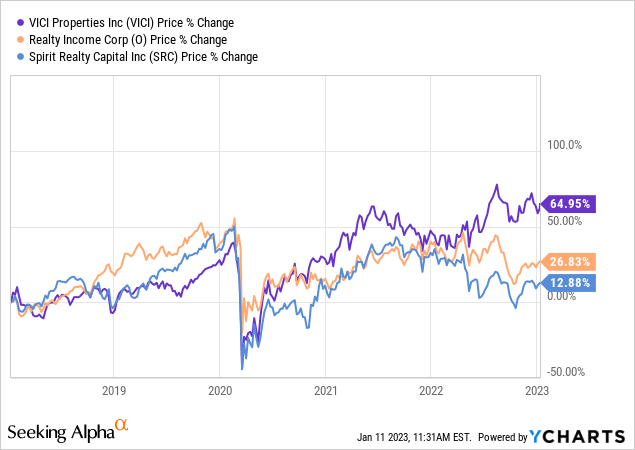

VICI Stock Price

Many net lease REITs including Realty Income (O) are down from highs and remain below pre-pandemic levels. Not VICI, though, as the stock has somehow bucked the trend.

Part of that has to do with the relative undervaluation that it traded at pre-pandemic, but in this report, I argue that much of it may be due to irrational exuberance. I last covered VICI in September where I called the stock “overrated and overvalued.” The latest earnings report and announced transactions have only solidified that view.

VICI Stock Key Metrics

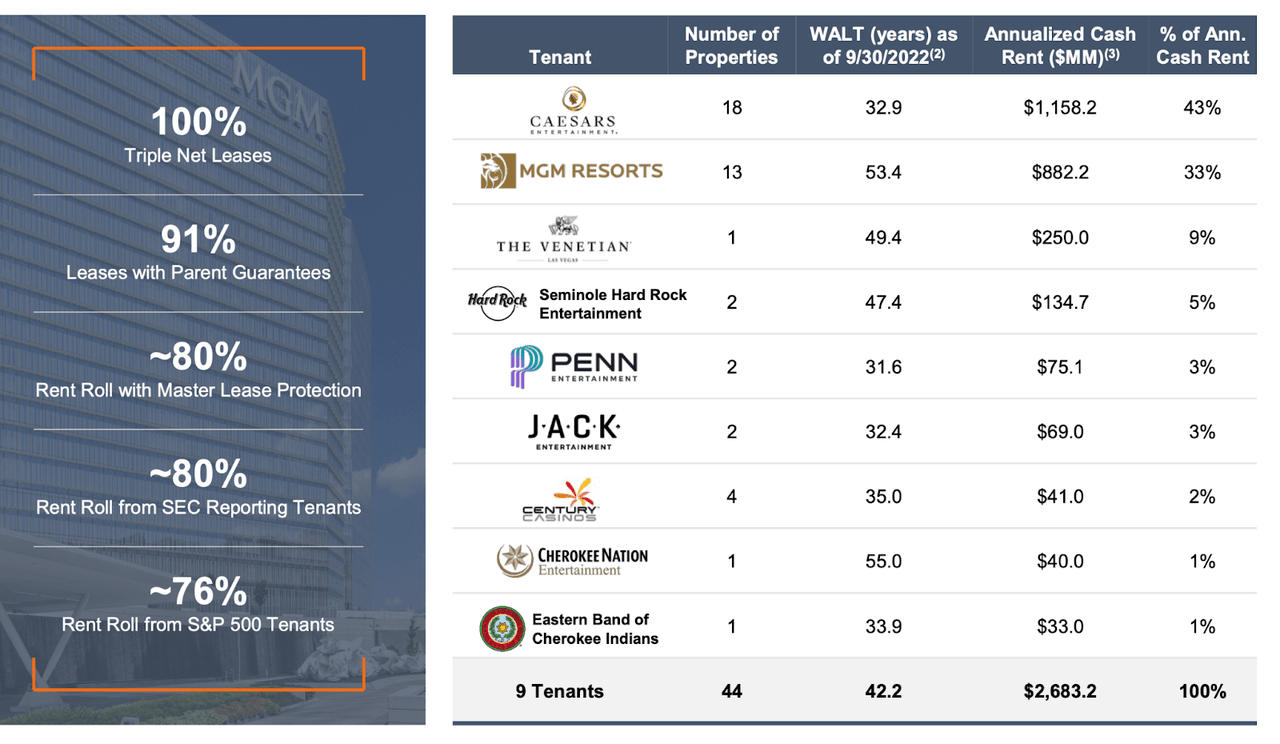

VICI has quickly diversified away from its largest tenant Caesars Entertainment (CZR), which now makes up 43% of annual rent. VICI leases to 9 tenants with MGM Resorts (MGM) being the other large tenant.

2022 Q3 Presentation

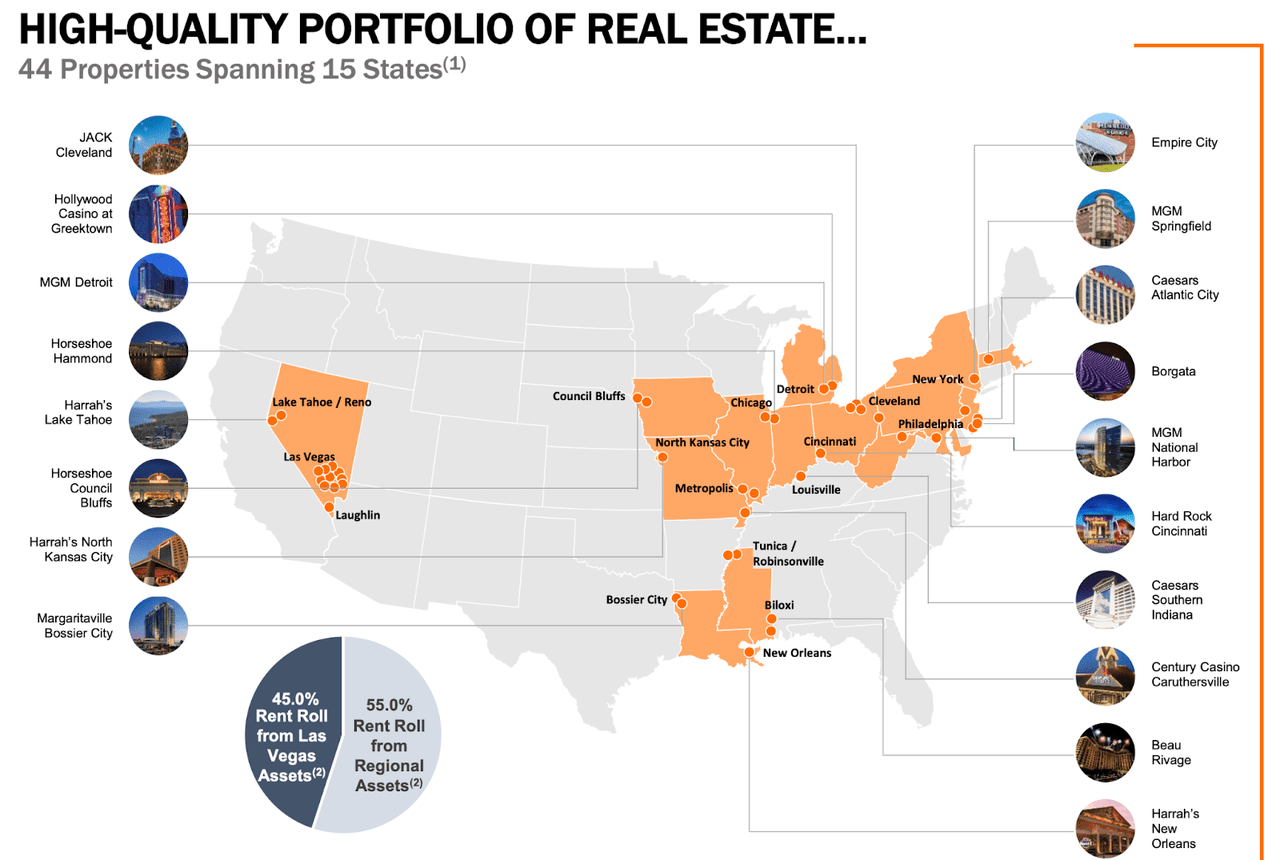

VICI’s portfolio is split between Las Vegas assets and regional assets, giving it a somewhat “diversified” allocation in casino real estate.

2022 Q3 Presentation

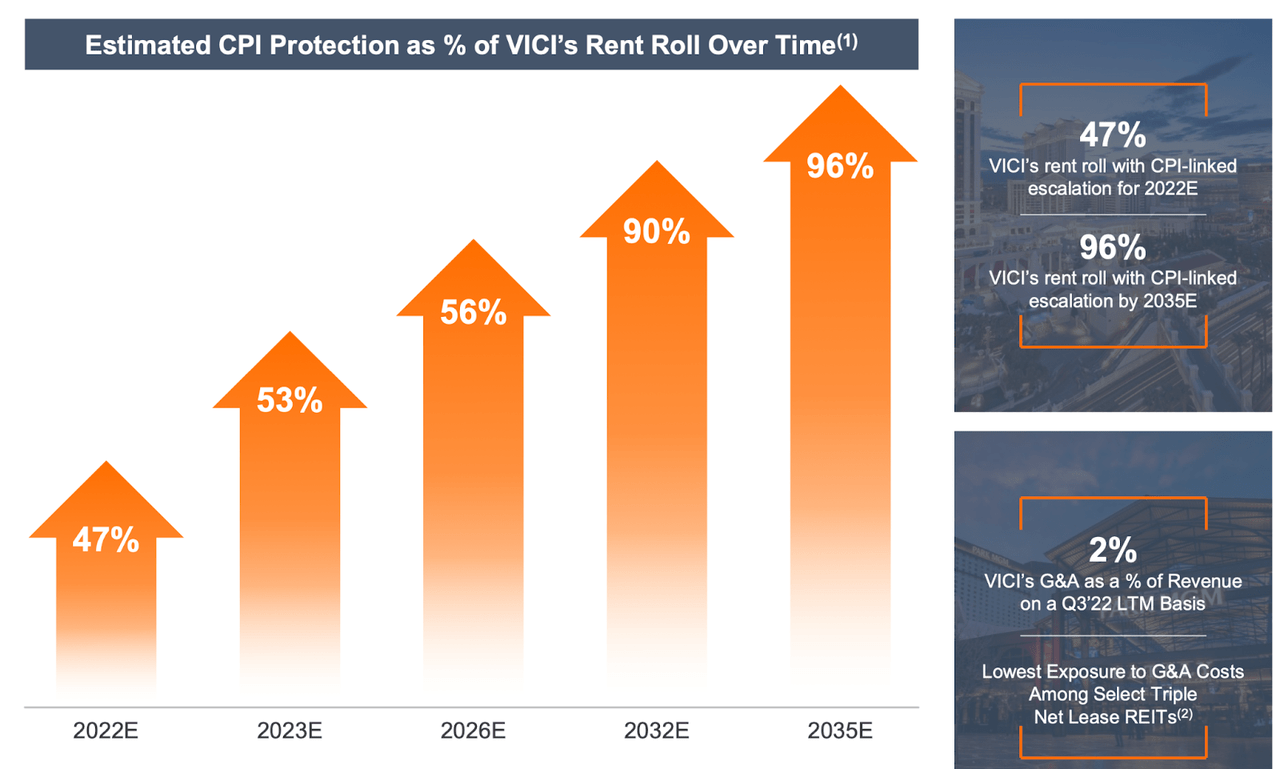

It should be noted that in comparison with other net lease REITs, VICI has great exposure to inflation, with 47% of its leases linked to CPI. That number is set to increase as the years go by.

2022 Q3 Presentation

The latest quarter saw adjusted funds from operations (‘AFFO’) grow 8.9% to $0.49 per share. Year to date, AFFO per share has grown 2.9% YOY and management is guiding for 5.5% growth for the full year to $1.92 per share. On the conference call, management noted that the guidance includes the “uncapped CPI lease escalation of 8.1% that VICI will receive under our Las Vegas master lease and regional master lease with Caesars, effective for the lease year beginning on November 1, 2022.”

Leverage is high here, with debt to EBITDA standing at 5.8x on an annualized basis.

2022 Q3 Presentation

I expect leverage to creep up when the company reports the next quarter due to the subsequent announcement that VICI will be acquiring the remaining 49.9% interest in MGM Grand Las Vegas and Mandalay Bay from Blackstone. That purchase will cost $1.27 billion for the equity and VICI will assume the remaining 49.9% of the $3 billion in debt.

MGM Grand Acquisition Presentation

Based on $154.69 million in acquired rent ($310 million in total rent), that comes out to a 5.6% cap rate – a nosebleed valuation in my view. Investors have cheered this transaction as being one inclusive of super-high-quality casino real estate, but I do not share the enthusiasm. VICI expects to fund the acquisition through cash and settlement of the 15.3 million in forward equity sale agreements, which totals $490 million. That implies $2.28 billion in incremental debt added to the balance sheet. I estimate pro-forma debt to EBITDA to stand at around 6.3x, which would be among the highest in the sector. In contrast, Spirit Realty (SRC) has a 5.4x debt to EBITDA ratio. In general, higher leverage should lead to lower valuations, but that has not happened here.

Is VICI Stock A Buy, Sell, or Hold?

At recent prices, VICI was trading at 17.2x 2022e AFFO. That far outpaces even O’s valuation, which was last quoted at around 16x AFFO.

Some may try to justify that relative premium due to the more aggressive lease terms, with longer lease terms and higher rent escalations.

2022 Q3 Presentation

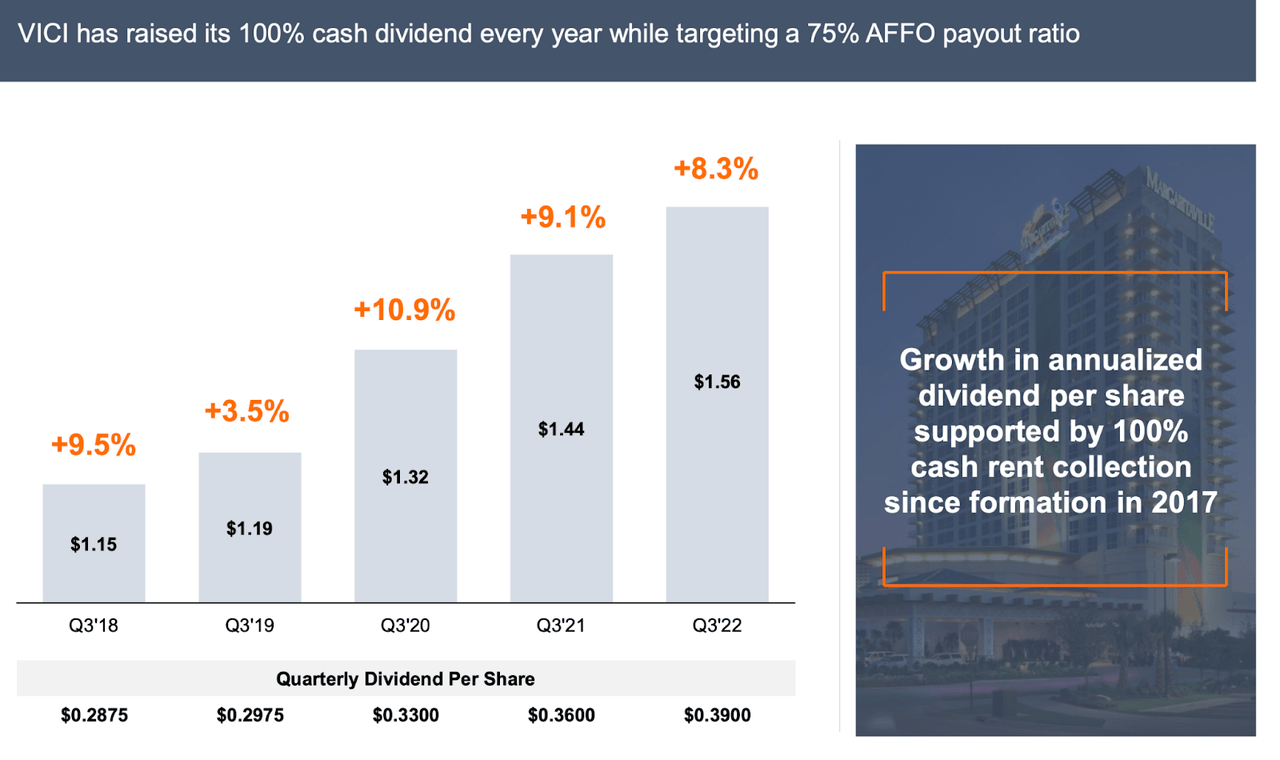

Those stronger lease terms have in part helped VICI sustain strong near-double-digit dividend growth over the past few years.

2022 Q3 Presentation

But I think that investors are missing the big picture. The question that they should be asking is what is the proper cap rate for casino real estate, and why are casino operators agreeing to such aggressive lease terms that differ greatly from industry norms? My long term view of land-based casinos is that they face greatly secular headwinds from the rise of online gambling, similar to that e-commerce headwinds faced by malls. My suspicion is that casino operators are engaging in sale and leaseback transactions to monetize these assets while valuations are high, in preparation for their continued push into online gambling.

Given the higher leverage and secular headwinds faced by VICI, I find the relative premium to the more-diversified and lower-leveraged O to be greatly misplaced. I also find it curious that VICI is acquiring casino assets for cap rates not too far off from traditional net lease real estate. I find it unlikely for multiple expansion to take place from here. I also find it unlikely for VICI to sustain 8% to 10% cash flow growth for more than 3 to 5 years. After 5 years of 10% growth, VICI would be trading at 10.5x AFFO, not far from where I’d expect fair value to be considering that SRC is trading at 10.8x FFO right now. That means that there is great possibility that VICI delivers mediocre returns at best for shareholders over the long term. The math just does not work out for strong returns from here. If one is searching for net lease REITs with superior lease terms than the norm, I personally greatly prefer the cannabis landlords Innovative Industrial Properties (IIPR) and NewLake Capital (OTCQX:NLCP), which are offering both superior lease terms and lower valuations than those seen at VICI. As for VICI, I continue to find the stock dangerous to hold here as the possibility for multiple compression looms large.

Be the first to comment