aprott

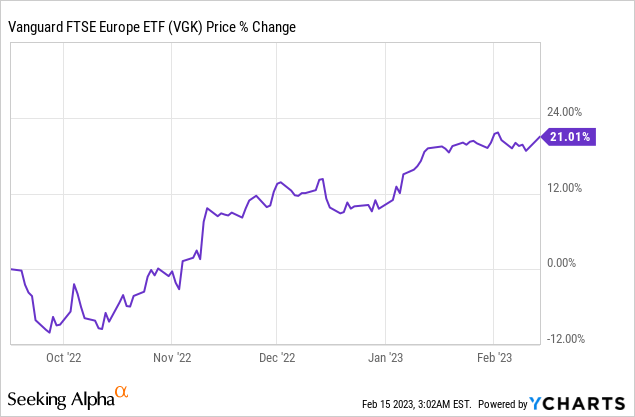

When I covered the Vanguard FTSE Europe ETF (NYSEARCA:VGK) back in September 2022, my position was not bullish, but, as evidenced by the title “Time To Start Looking Beyond the Gloom”, the outlook was undoubtedly optimistic. Thus, VGK has appreciated by 21% since then despite some bearish outlooks mostly based on high-level macroeconomic data.

This shows the importance of not basing oneself purely on economic outlooks restricted to certain countries or regions when analyzing a fund like VGK which provides exposure to stocks from a wide range of countries including the U.K. Thus, my aim with this thesis is to go deep into factors like valuations, dividends, concentration risks, Europe’s position with respect to other regions, inflation, and the possibility of a recession as well as assess the strength of the banking system in case of an economic collapse.

I start with country exposure.

The Country Exposure

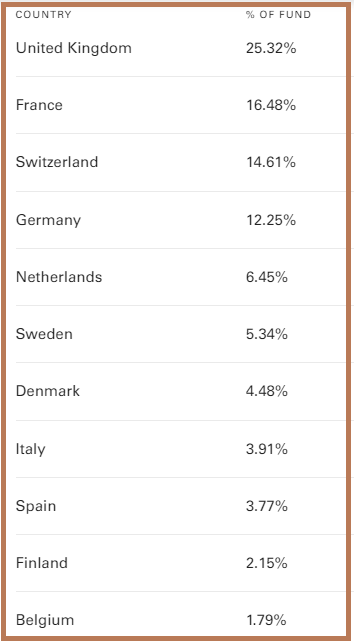

In this respect, 25.32% of VGK’s assets are exposed to the U.K. as pictured below. Now, as a result of hiking interest rates implying higher borrowing costs and record income tax, this country is expected to be the worst-performing G7 (Group of seven nations) economy and likely to suffer from a prolonged recession in 2023. However, despite having reached its highest level in five years, the price-to-earnings valuation of the FTSE 100, or the hundred most valuable stocks listed on the London Stock Exchange (in terms of market capitalization) is only 10.77x, compared to 18.38x for the S&P 500, or 70% more.

VGK’s Country-level exposure (advisors.vanguard.com)

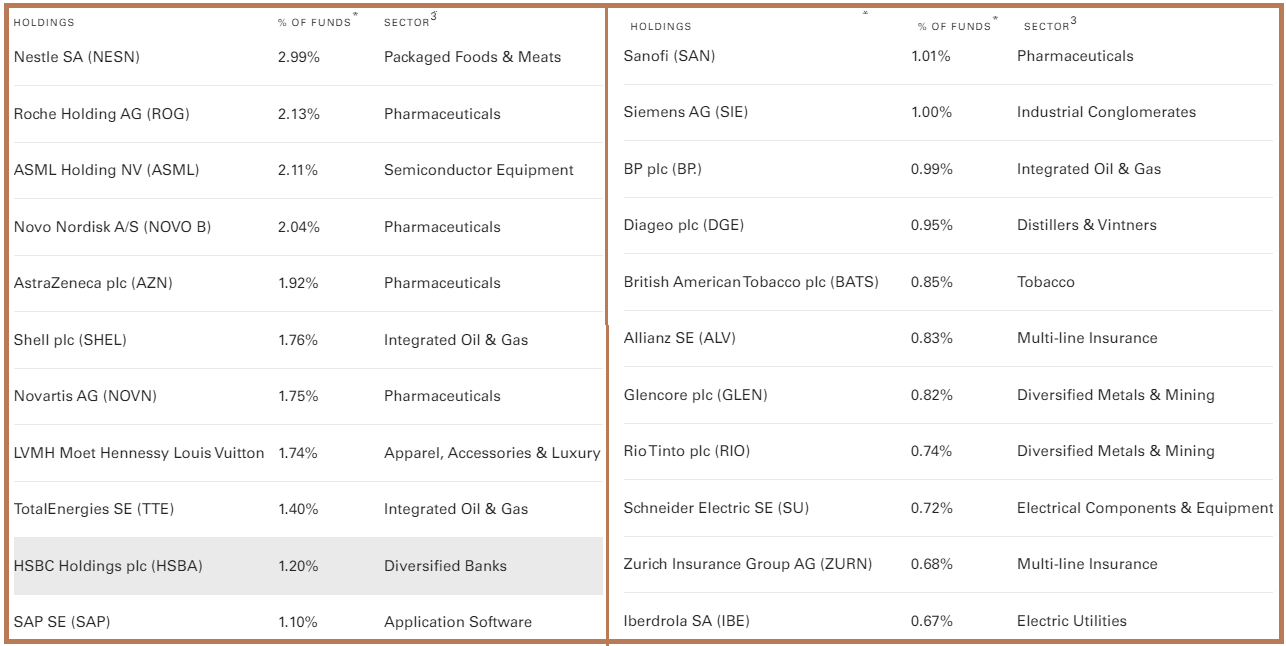

In addition to the value factor, some of the stocks like AstraZeneca (AZN), Shell (SHEL), and HSBC Holdings (HSBC) pay high dividend yields which imply that part of the FTSE 100 upside is also being driven by income seekers who may also be diversifying their investments to the U.K, while also profiting from the weakness of the GBP with respect to the greenback.

Furthermore, there is another factor that has been overlooked as the market participants focus on inflation and which by the way was the base case for my optimism on VGK in September. This pertains to the resiliency of the banking system, as in case of a protracted economic slowdown, it is banks that tend to suffer the most initially. In this case, according to research by S&P Global, U.K. banks have the strength to “confront these challenges with a strong earnings outlook, solid regulatory capital positions, robust asset quality, and stable funding and liquidity positions”.

Top 22 Stocks forming part of VGK (advisors.vanguard.com)

As for the rest of Europe, a drop in natural gas energy prices has changed the outlook considerably, especially for the German industrial base, which on top, should benefit from the Chinese Covid reopening. Here, companies that come to mind are industrial conglomerates like Siemens AG (OTCPK:SIEGY) as pictured above. In this case, in addition to exporting to China, the medical arm of Siemens has been adopting a strategy involving localizing its production in the Asian country, thereby contributing to its made-in-China agenda.

This strategy is not without risk though.

The Risks, Mitigation, and Europe’s Positioning

In this respect, China has remained Germany’s top trading partner for seven consecutive years. Therefore with economic activities getting unfrozen in China as peak infection rates subside, there should be more demand for capital goods like machinery from Germany. On the other hand, with the European country importing more than two third of rare earth metals from China, there are risks of an over-dependency for commodities just like for natural gas from Russia. Thus, similarly to the Ukrainian conflict, in the event of geopolitical tensions rising between the United States and China or a possible invasion of Taiwan, Germany would again face supply chain risks for raw materials crucial for producing EV batteries and semiconductors.

There are also unfavorable macros as the Ukrainian conflict lingers on. Thus, despite falling slightly, inflation at 9.2% is way above the comfort level of central bankers and entails higher interest rates being applied to the monetary system, in turn, keeping borrowing costs on the high side for a continent that has been used to zero interest rates for more than a decade.

However, it is not so gloomy out there, as, according to Goldman Sachs (GS), inflation should slow by the end of the year to reach 3.25%, as the price of goods falls, while service inflation is expected to remain elevated due to rising labor costs. Thus according to the investment bank, after the increase of 50 basis points in February, there should be the same percentage point hike in March, before the ECB (European Central Bank) slows to 25 basis points in May, which should bring terminal rates to 3.25%. These are the highest since late 2008, but, it is important to pay attention to the context, which is that most central bankers around the world remain hawkish, implying that interest rates remain high globally.

Going into further details, higher borrowing costs have led to a reduction in business appetite throughout the world resulting in sluggish growth, but, a lower inflation print for December, a fall in natural gas prices, and China reopening have resulted in a more optimistic outlook by the economists at Goldman, even at the point of them announcing that a technical recession should be avoided this year.

This augurs well for VGK, but, to mitigate country-level risks, VGK has a reduced exposure of 12.25% to Germany, and equally important, it’s largest German industrial holding, Siemens only constitutes 1% of total assets. Along the same lines, the inclusion of more “defensive” French and Swiss names in pharmaceuticals goes to a further extent in reducing volatility.

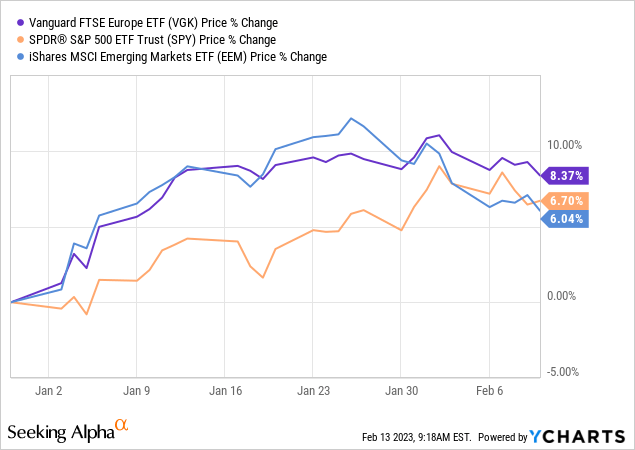

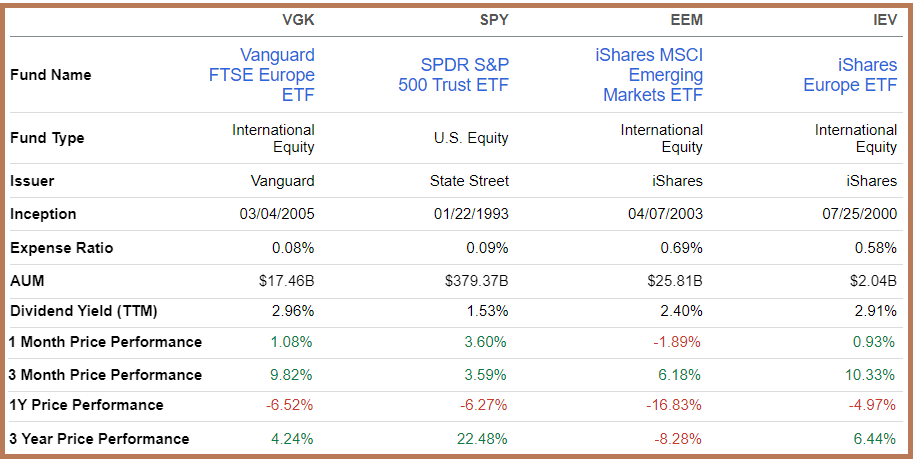

Looking deeper, as a result of splitting its holdings and restricting their weight to below 3%, the Vanguard ETF has significantly reduced concentration risks, which has translated into better price performance. Thus, a comparison of the performances of VGK with the SPDR S&P 500 Trust ETF (SPY) and the iShares MSCI Emerging Markets ETF (EEM) puts into evidence it’s lower volatility since the beginning of this year.

Looking at EEM, there has been lots of volatility in emerging markets as credit conditions should persist as the fast pace of monetary tightening in most countries has created recession risks with the strong dollar also causing headwinds in the balance of payments of individual countries.

Therefore, between the high valuations in the U.S. and risks around emerging markets, Europe appears to be rightly placed, with European stocks having seen more inflows. This is likely to continue unless there is some drastic escalation of the Eastern European conflict.

As a matter of fact, investors’ preference for European stocks started about three months back as pictured in the table below, and has been sustained despite the ECB appearing more hawkish than the Federal Reserve in its desire to stay on course for fighting inflation.

Conclusion

Interestingly, as shown in the table below, compared to SPY, the European ETF is still at a three-year low, with an 18% difference in performance. Thus, assuming a 6% upside for 2023, I have a target of $65 (61 x 1.06) for VGK based on its current share price of $61.

Another reason for being bullish is that the peer comparison also shows that, while charging less, VGK offers a higher dividend yield of 2.96% especially compared to another European fund, the iShares Europe ETF (IEV). Thus, the Vanguard ETF is attractive for income seekers.

Comparing VGK, SPY, EEM, and IEV (seekingalpha.com)

To sum up, based on a number of factors which also include macroeconomics, and relative positioning with respect to other geographies, this thesis has shown that VGK should rise further in 2023, as the old continent avoids a recession.

Finally, in the worst-case scenario that there is a recession, do expect equities to be particularly volatile over the short term, but, still, I am optimistic over the longer term and this has to do with banks. Thus, as per SPG Global’s Banking Industry Country Risk Assessment, the banks in the European countries the ETF provide exposure to exhibit low risks to very low risks, with the exception of Italy, but, to be realistic, this country accounts for only 3.91% of the ETF’s assets.

Be the first to comment