Andres Victorero

ETF Overview

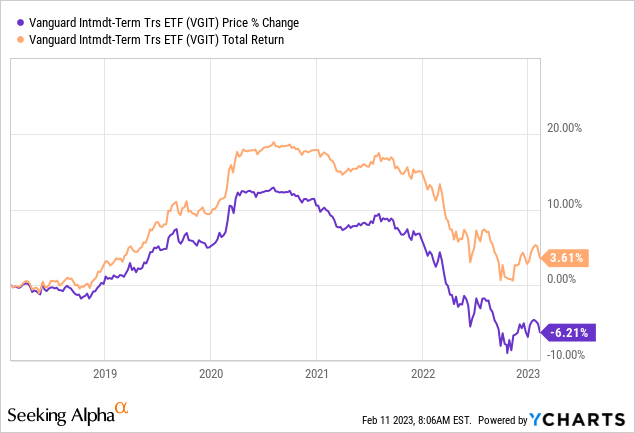

Vanguard Intermediate-Term Treasury ETF (NASDAQ:VGIT) has a portfolio of intermediate-term U.S. treasuries. The fund delivered an abysmal record of two consecutive years of negative returns. Although it is unlikely that the returns in 2023 will be as bad as the previous two years, expected return will likely be limited. This is because interest rate will likely be kept elevated in 2023 due to a persistent job market. Given limited capital appreciation in 2023, we believe investors may want to apply a wait-and-see approach and wait for a better entry point.

YCharts

Fund Analysis

2022 was a brutal year for VGIT

VGIT’s fund price set a record high in 2020 as the Fed fund rate dropped to a historical low in that year due to the pandemic and the Federal Reserve’s effort to rescue the economy. However, as the economy reopens in 2021 and inflation expectation starts to rise, Fed fund rate has moved significantly higher in 2022. As bond prices usually have an inverse relationship to rates, VGIT’s fund price has likewise declined significantly. In fact, VGIT delivered negative total returns of 2.57% and 10.67% in 2021 and 2022 respectively.

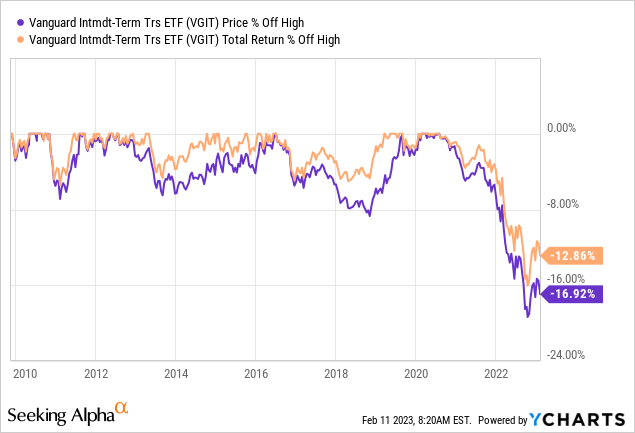

VGIT’s abysmal record in 2021 and 2022 was the worst it has ever recorded since its inception in 2006. As can be seen from the chart below, the fund registered a total return of negative 16.96% since the high reached in 2020.

YCharts

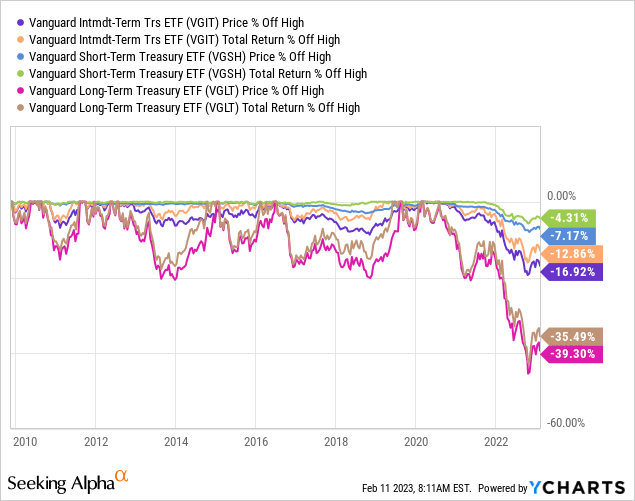

VGIT was not the only bond that suffered negative returns in 2021 and 2022. As can be seen from the chart below, its peer Vanguard Long-Term treasury ETF delivered a total return of negative 35.49% in the past 2 years. On the other hand, its shorter term peer, Vanguard Short-Term Treasury ETF (VGSH) delivered a much smaller total loss of 4.31%. VGIT’s underperformance to VGSH and outperformance to VGLT was primarily due to its “intermediate” rate sensitivity. For reader’s information, the sensitivity of rate on bond price depends on the duration of the bonds to maturity. In fact, bonds in VGIT’s portfolio have an average duration of 5.4 years, slightly longer than VGSH’s 1.9 years but a lot shorter than VGLT’s 16.1 years.

YCharts

Should you invest in VGIT in 2023?

As we have discussed earlier in the article, VGIT has suffered two consecutive years of negative total returns. Will VGIT experience another year of negative return in 2023, making it three consecutive years of negative returns? It is possible but unlikely. Even if there is a loss, the loss will likely be limited. The reason is that we may be near the end of this rate hike cycle as inflation has clearly peaked in 2022 and continues to fall in each of the months since June 2022. As opposed to the aggressive rate hikes last year, the Federal Reserve only increased its rate by 25 basis points in its latest meeting and is expected to do the same in its upcoming few meetings. Therefore, we do not see much room for the rate to go up. Hence, there isn’t going to be much more room for the bond price to drop either. Even if bonds in VGIT’s portfolio decline, the 4%-yielding distributions investors currently will earn will likely be more than enough to offset the decline.

At the moment, we do not expect VGIT’s fund price to return to the same level in 2020 as the Federal Reserve has clearly stated that they will keep the rate elevated for a lengthy period until they see further signs of inflation going away. Unfortunately, taming inflation is not an easy task as a significant portion of the inflation index is related to wage growth. This part of inflation is very sticky as wage growth often results in higher product/service price increase and has a spiral effect. In addition, the 517k jobs added in January has further pushed the unemployment rate down to 3.4%. This was the lowest we have seen in many decades. It appears that the job market is still persistently strong despite the aggressive rate hikes last year. Therefore, we do not see any room for the Federal Reserve to lower the rate in 2023 either. If the rate is going to stay elevated in 2023, there will not be much room for capital appreciation in 2023.

We do expect inflation to eventually drop to the Federal Reserve’s target of 2%, but that will be a story beyond 2023. Therefore, if you do not have a long-term investment horizon, this fund may not be the best for you. Even if you do have a long-term investment horizon, we think owning funds with portfolios of longer duration bonds such as VGLT or Vanguard Long-Term Bond ETF (BLV) will be a better choice. Since longer term bonds are much more sensitive to rate changes than short-term and intermediate-term bonds, there will be more room for capital appreciation.

Investor Takeaway

Investors of VGIT will likely not suffer the same degree of loss it endured in 2022. However, the return in 2023 will likely be limited due to the Federal Reserve’s expected policy to keep the rate elevated. While inflation will eventually drop to the 2% target, it will be a story beyond 2023. Hence, the Federal Reserve will likely not drop the rate any time soon. This means that capital appreciation will likely be limited in the near-term. Therefore, we recommend investors to wait and not to rush to buy VGIT.

Additional Disclosure: This is not financial advice and that all financial investments carry risks. Investors are expected to seek financial advice from professionals before making any investment.

Be the first to comment