luza studios

Vertex Pharmaceuticals (NASDAQ:VRTX) is a biotechnology business involved in scientific research and development of treating serious diseases. The company currently has many projects in the pipeline that can help it create its presence in new segments and strengthen its existing segment. I believe the company can target many new customers with the latest research and development, which will act as the main reason for the huge growth prospect of the company. The company also has a high cash reserve that will support future research and development.

About Vertex Pharmaceuticals

Vertex Pharmaceuticals is a multinational biotechnology business that develops medicines and invests in scientific research to develop treatments for patients suffering from serious illnesses. The company has a variety of authorized medications to treat the rare, fatal genetic disease cystic fibrosis (CF), as well as numerous ongoing studies and clinical trials to address the condition’s underlying causes. Out of the total revenue of Vertex, the main chunk is delivered by two medicines – Kaftrio and Trikafta. The company generates more than 70% of its revenue from the sales of these two medicines.

Revenue Segment (Investor Presentation)

Both drugs are used to treat cystic fibrosis in individuals who are six years of age or older. Trikafta has regulatory approval in 32 countries, including the United States and the United Kingdom, while Kaftrio has regulatory approval in the European Union. The company has a smaller customer base than its competitors because it is known for specializing in rare diseases. Sickle cell disease, beta-thalassemia, APOL1-mediated kidney disease, type 1 diabetes, Alpha-1 antitrypsin deficiency, and Duchenne muscular dystrophy are a few more significant diseases for which VRTX has expertise in addition to CF.

New Project Development

FY2021 Annual Report (Annual Report of VRTX)

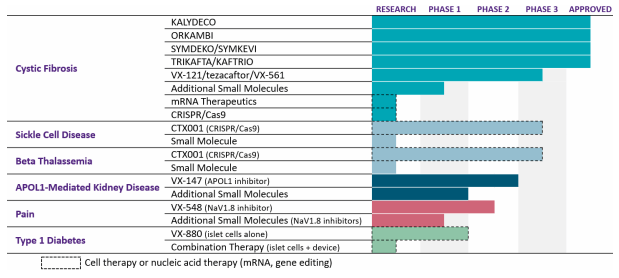

VRTX generates a large part of its revenue from the medicines for CF. Currently, the company is looking for the opportunity to diversify its product portfolio to reduce its dependency on a single product line. The company has many projects related to the new diseases that are under development, and it is also focusing on the R&D of new CF medicines to increase its presence in the market. Below you can find a detailed explanation of the new project development in major segments.

Cystic Fibrosis

The company has started the Phase 3 clinical trials of VX-121/tezacaftor/VX-561, an experimental triple combination that increases the effectiveness of the existing CF medicines. Clinical and experimental findings suggest that this triple combination may offer CF patients additional benefits beyond Trikafta/Kaftrio. The company is also concentrating on genetic therapy research, including messenger ribonucleic acid (mRNA) and gene-editing techniques, to cure the remaining 10% of CF patients who do not produce CFTR protein and are therefore not anticipated to benefit from the company’s small molecule medications. Together with Moderna (MRNA), the company is creating CF mRNA therapies to cure the underlying cause of CF in these individuals by allowing lung cells to manufacture functional CFTR protein. I believe this is more than enough to sustain and increase its current hold in the CF medicine market. The company already caters its services to 90% of CF patients, but with current research, the company can penetrate the remaining 10%.

Sickle Cell Disease and Beta Thalassemia

The company is developing CTX001, an investigational CRISPR/Cas9-based gene-editing therapy, for the treatment of severe Sickle Cell Disease (SCD) and Beta Thalassemia with the collaboration of Crispr (CRSP). According to the Centers for Disease Control and Prevention, approximately 100,000 Americans are affected by SCD. The Rare Disease organization has stated that approximately 1 in 100,000 individuals in the general population suffers from beta-thalassemia. These data points can tell us the market available for the SCD and beta-thalassemia products.

Type 1 Diabetes

In order to provide a functional cure, VRTX is researching autologous, fully differentiated stem-cell derived islet cell therapies that are intended to replace insulin-producing islet cells that are lost in persons with type 1 diabetes. The company is pursuing several programs for the transplant of functional islets into patients: the transplantation of islet cells alone, using immunosuppression to safeguard the implanted cells, placing the islet cells inside a cutting-edge immunoprotective device, and optimizing hypoimmune cell development. The FDA also has lifted the clinical hold on VX-880 Phase 1/2 clinical trial for the treatment of type 1 diabetes. The company will be reopened for screening, enrollment and dosing at multiple sites in the U.S. As per the CDC, 5.7% of all U.S. individuals with diabetes – which amounts to 1.6 million persons age 20 and older – reported having type 1 diabetes and needed insulin. And within a year of their diagnosis, a total of 3.1 million adults age 20 and older with diabetes began using insulin. This shows us the tremendous market for diabetes that VRTX can explore and capture with its innovative medicines, currently under trial.

Apart from the above-mentioned segments, the company is working on the R&D of the APOL1-Mediated Kidney Disease, Pain, Alpha-1 Antitrypsin Deficiency, Duchenne Muscular Dystrophy and Myotonic Dystrophy Type 1, etc. But I believe the development in CF, sickle cell disease, and type 1 diabetes will be the main reasons behind the huge earning growth in the future. That’s because, currently, the company only has 90,000 CF patients, and with new product development it can penetrate new market segments that have a large number of available consumers.

Large Cash Reserves

As of March 31, 2022, the company has large cash and cash equivalent reserves of $8.2 billion. With a market valuation of $73.48 billion, the corporation has high percentages of cash reserves (11% of market value). The company will be able to invest more in its R&D programs for several disease areas, thanks to its high cash reserves. The company also intends to create cell development facilities in Boston by investing in capital infrastructure development. The cash reserves will support such investment opportunities that will aid in the company’s long-term growth.

Analysis of Financial Statements

Revenue for the company was $2.10 billion, up 22% from $1.73 billion in Q1 2021. Trikafta and kaftrio sales, which totaled $1.77 billion, increased by 47.5 % from the same time last year, which were the biggest revenue drivers. Net product revenues in the first quarter of 2022 increased 9% to $1.37 billion in the U.S. and increased 55% to $729 million outside the U.S., compared to the first quarter of 2021. The company has kept its forecast for product revenue for the entire year 2022 at $8.4 billion to $8.6 billion. In Q1 2022, Vertex’s GAAP net income increased by 17% to $0.76 billion from $0.65 billion in Q1 2021.

I believe that increased sales and cost-cutting initiatives in operating expenses contributed to an increase in net income, while also enhancing operational margins. In comparison to $2.49 in the same quarter last year, the GAAP diluted EPS increased by 19% to $2.96. I estimate FY22 GAAP diluted EPS to be in the range of $13.80 to $15.00. I believe the company will benefit from the approval of CTX001, which is expected by the FY22. The effects of this approval will be seen in the results of FY23.

In terms of revenue and profit, the outcomes were as anticipated. Given the company’s objectives for diversification and its entry into a portfolio of widely used medicines, I think revenue will rise significantly in the future quarters. As per CEO and President of Vertex Reshma Kewalramani:

Q1 CF product revenues grew 22% year on year to $2.1 billion, reflecting continued growth in the number of CF patients treated globally. And despite continued significant investment in internal and external innovation, our non-GAAP operating margins remained industry-leading at 56%. We maintained a rapid pace of progress in research and across the clinical stage pipeline with a half a dozen programs now post the POC stage. And we finished the quarter with a strong balance sheet and $8.2 billion in cash and investments.

The Main Risk for Vertex: Dependency on CF Disease Products

The company has a high dependency on two medicines, trikafta and kaftrio, for the cure of CF disease. With 85% of its revenue coming from these two medicines, the company depends highly on them. Cystic fibrosis is a rare disease that affects only about 83,000 people in North America, Europe, and Australia. According to the company’s calculations, just 25,000 of those patients are qualified but unenrolled for treatment with trikafta, its newest medicine, and potentially another 5,000 could be treated by candidates now in the pipeline. Many of those who are qualified but have not yet enrolled are being treated with older Vertex drugs. With limited market size, the growth in the long term appears bleak. But with company looking to enter a new disease market, the growth story can surely change.

Fundamental Valuation

I believe the company will benefit from the diversification in the mass medicine market, which will be a driving factor in the company’s future growth. The company is currently trading around $291 and has a P/E multiple of 20.32x. I think the P/E valuation model is a good parameter to judge VRTX’s valuation as the company is trading at low P/E multiple vs. its growth prospects. I am estimating the FY22 EPS to be $14 and the P/E multiple of 25x for Vertex. This gives us a target price of $350, or 21% upside from the current share price. I have taken conservative EPS estimates as per the company’s guidance, but I believe the EPS of FY22 could be even higher. At the current price level, the company is undervalued. Given the several growth factors discussed, I believe the company will perform significantly better in the coming quarters.

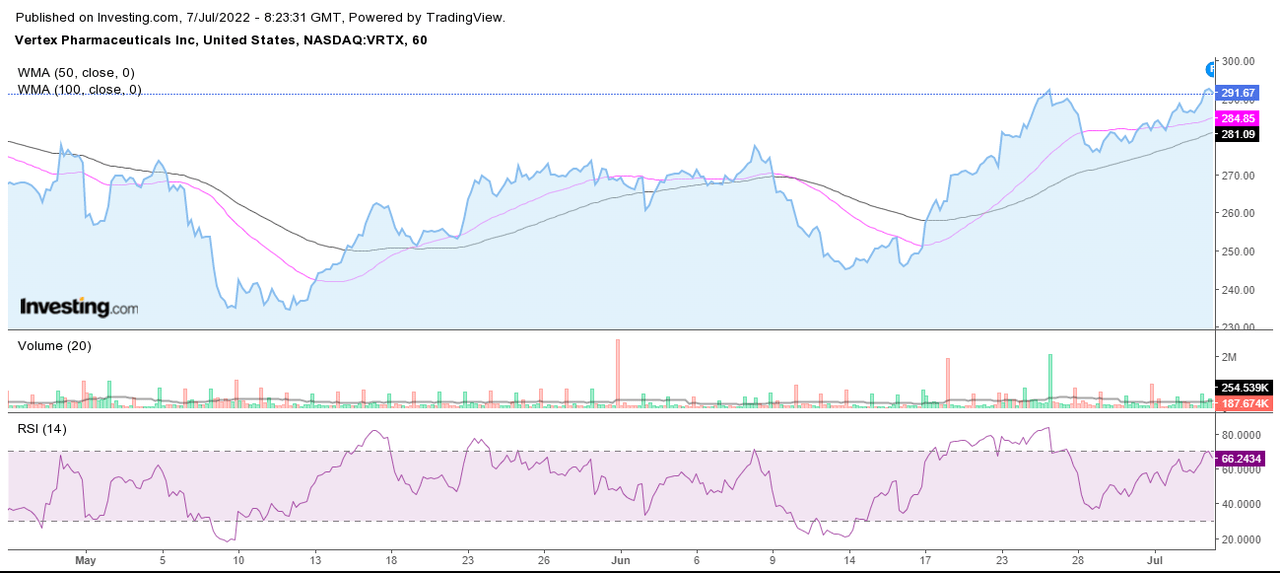

Technical Analysis

Technical Analysis Chart (Investing.com)

The technical indicators suggest that the company is trading above its 50-day WMA (weighted moving average) and 100-day WMA. The stock has a strong support level at the 100-day WMA, and I believe that, after testing this support level a few times, the stock can see significant upside. As per the RSI indicator, the stock is consolidating in the 70-50 range after facing resistance at the 70 band. I believe once the stock crosses the 70 range, we can see fresh momentum in the stock. Overall, the technical indicators are positive and suggest a buy from current levels.

Conclusion

Vertex is a market leader in CF disease treatment, and with the expansion of its medicine line into the mass disease market, the company is well-positioned for significant growth levels. The firm is currently undervalued with a P/E ratio of 20.32x, and I think the company has good upside potential from the current price level. The company faces the risk of high dependency on CF disease treatment, but with late-phase trials of multiple medicines, I believe this dependency will fade by the end of FY22. After taking into consideration all of these factors, I would assign a buy recommendation for the stock.

Be the first to comment