Mohammed Haneefa Nizamudeen/iStock via Getty Images

Verona Pharma plc (NASDAQ:VRNA) could bring the first innovative product for the treatment of COPD to market. At the end of 2022, the latest clinical trials on Ensifentrine underlined important positive results on symptoms, lung functional metric data, and exacerbation. Also from the safety point of view, the clinical trial indicated high tolerability by patients after 24 and 48 weeks. The potential market with $10B in the US represents a huge opportunity also because millions of patients remain symptomatic even after existing traditional treatments. The company is also sufficiently capitalized with approximately $150M of the debt facility. The share price could be expensive right now but the potential return could also be equally high looking beyond 2024.

The investment thesis implies a high risk mainly due to factors exogenous to the company, but the risk-return ratio is positive in my opinion and I think VRNA is a Buy.

COPD Market Outlook

COPD means Chronic Obstructive Pulmonary Disease and refers to a respiratory disease without a definitive cure. It affects the airways and lungs and can lead to long periods of hospitalization and even death.

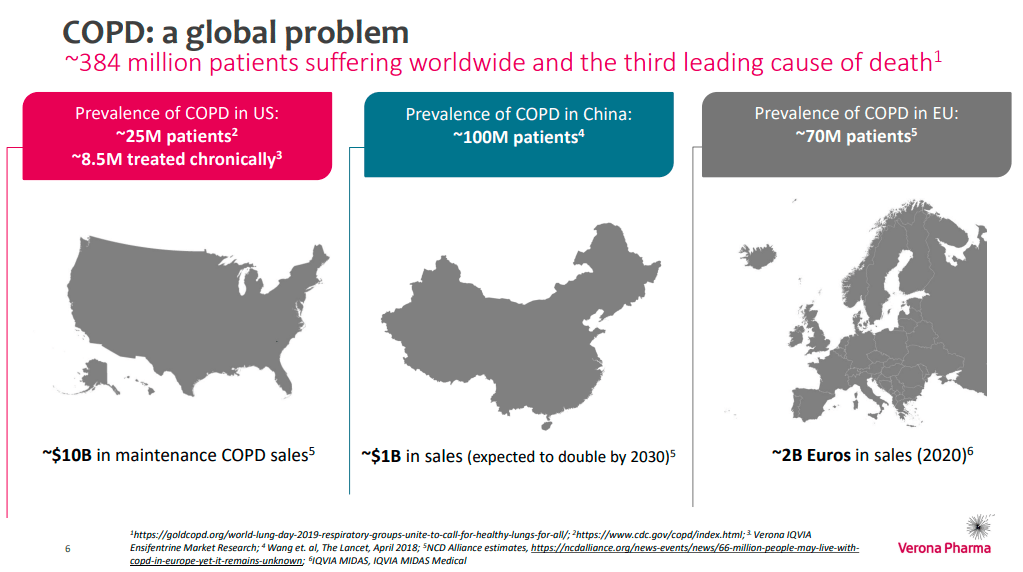

According to the World Health Organization, about 384 million people are affected by COPD globally, representing the third death cause. The COPD therapy target is to improve quality of life by reducing exacerbations. Globally COPD treatments market sales are esteemed at about $13B.

Investor Presentation 2023

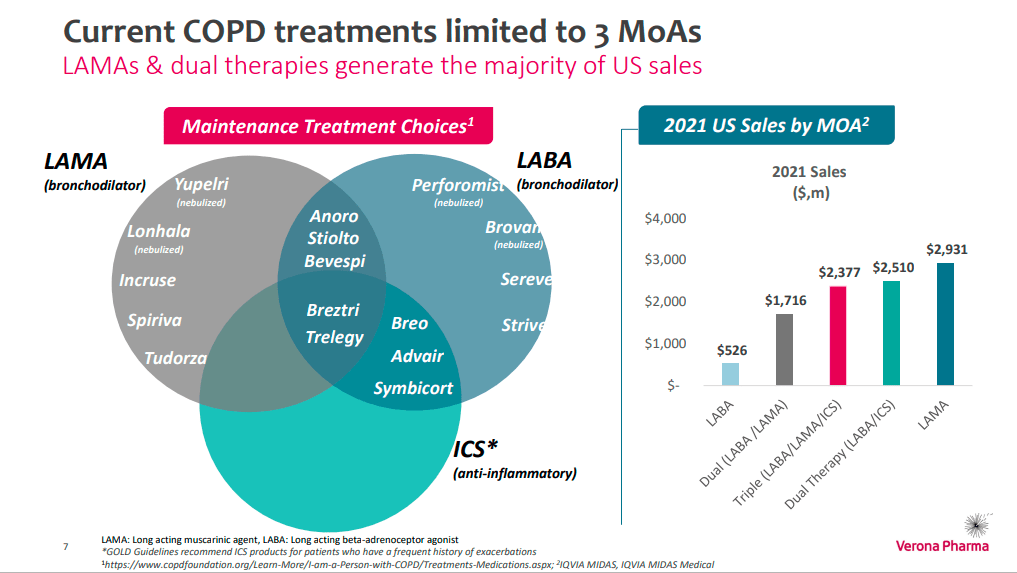

The main COPD treatments (FDA and EMA approved) are based on:

- LAMAs (long-acting anti-muscarinic agonists)

- LABAs (long-acting beta-agonists)

- ICSs (inhaled corticosteroids)

Investor Presentation 2023

These therapies could be used together with a dual or triple action (LAMA/LABA/ICS). Clinical studies estimated that 40% of patients remain with evident symptoms even if undergoing treatment. This represents a big market opportunity and it is esteemed that at least 1.6 million people with very severe COPD patients in the US could urgently need new treatments to improve their quality of life.

Investor Presentation 2023

About Verona Pharma

Verona Pharma is a biopharmaceutical company involved in studies and product development related to respiratory diseases. The operation involved is in a clinical stage and the commercialization of the final product is based on the analysis of great unmet medical demand in COPD.

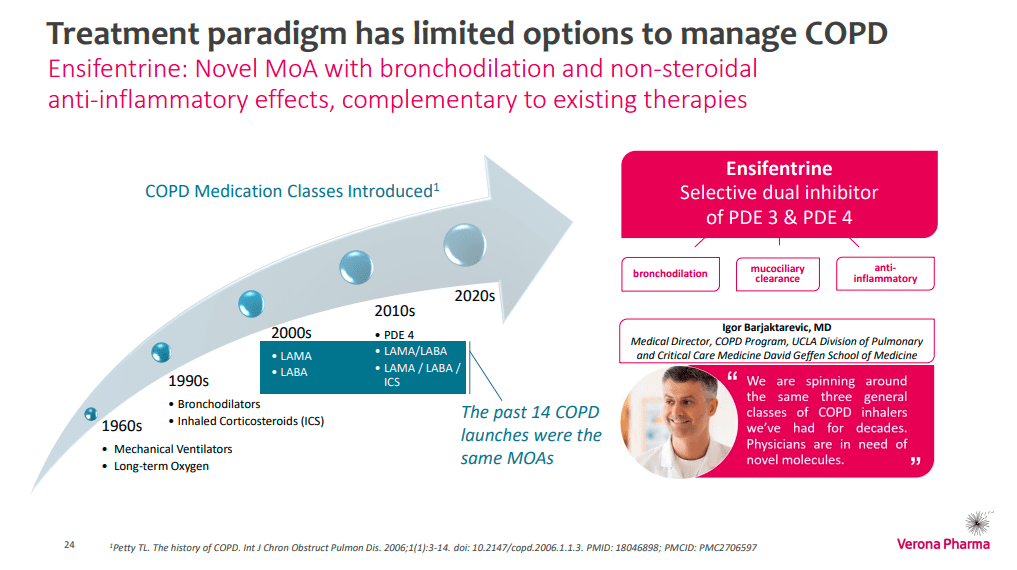

The main product is ensifentrine which is designed to act as both a bronchodilator and an anti-inflammatory. It has to be inhaled and is an inhibitor of both (phosphodiesterase) PDE3 and PDE4 enzymes. The product was born for the COPD treatment and if will be marketed it will represent a novel action for COPD in the last decade.

Investor Presentation 2023

If approved by FDA the product will be directly commercialized via a standard nebulizer in the US. Outside the US the Company has decided to commercialize ensifentrine licensing it to third companies with expertise in the same field. Nuance Pharma Limited is the first commercial partner based in Shanghai with the target to sell the product in China. The company is also searching for new partners in Europe.

Verona does not own production plants and does not intend to build them. For the production, it will rely on suppliers specialized in the production of pharmaceutical products.

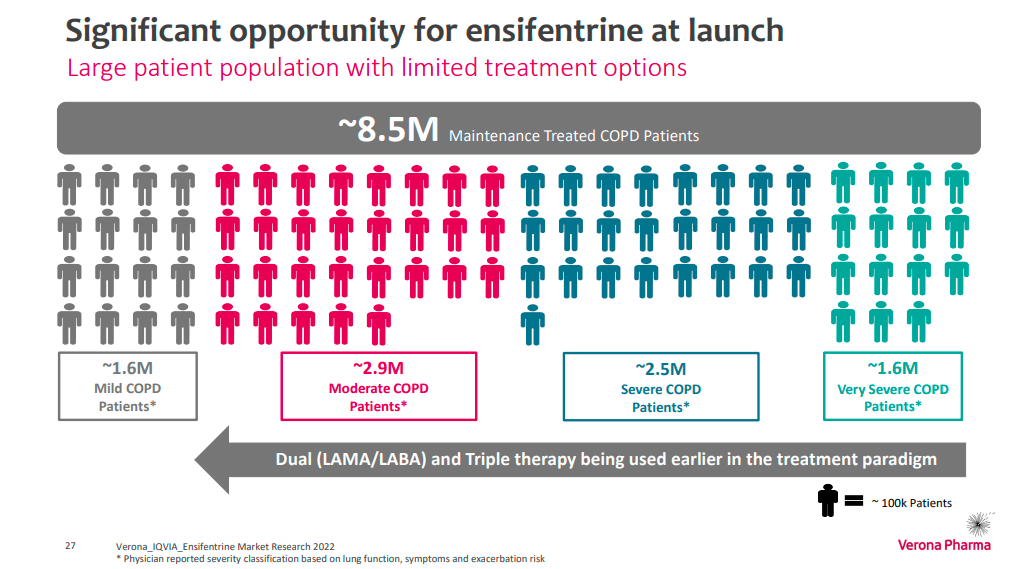

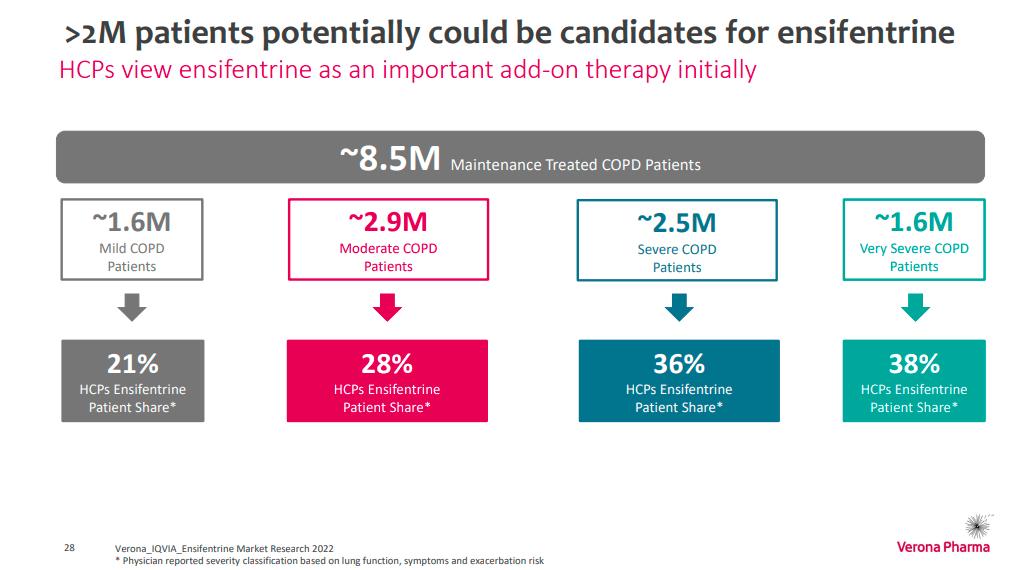

Returning to the number of COPD patients out of a total of approximately 8.5M people, the company estimates that more than 2M people could be candidates for the use of ensifentrine. This uses the entire market spectrum, i.e. from mild to very severe patients, and represents more than 20% of the market share.

Investor Presentation 2023

Company Pipeline and Clinical Program

Investor Presentation 2023

Verona is in the Phase 3 clinical program ENHANCE (Ensifentrine as a Novel inHAled Nebulized COPD thErapy) with the nebulized ensifentrine (first red arrow in the graph).

Phase 3 is the step before the NDA (New Drug Application) with the Governative FDA (Food and Drug Administration). NDA is the last step and if approved by FDA it means that the drug can be on market. But let’s dive into the last trial:

Ensifentrine reaches the target in ENHANCE-1 and ENHANCE-2 trials and defined important improvements in lung functions and COPD exacerbations. The two studies are based on demonstrating the efficacy and also safety of ensifentrine as a sole therapy for COPD in comparison with LAMA, LABA, ICS, and placebo.

The two studies had two endpoints (improvement in lung function at 12 and 24 weeks of treatments) and a safety assessment.

On 2022 December 20th the Company declared…

- 36% reduction in the exacerbation rate vs placebo

- 38% reduction in exacerbation risk with significantly delayed time to first exacerbation

…and in safety terms that the product is well-tolerated with…

“very few events occurring in more than 1% of subjects and greater than placebo over 24 and 48 weeks”

Wanting to translate these results into medical language but more understandable we can hear Antonio Anzueto (Professor of Medicine and Section, Chief of Pulmonary at South Texas Veterans Healthcare System) comments:

“These exciting results demonstrate ensifentrine’s potential to become a first-in-class bronchodilator and non-steroidal anti-inflammatory therapy for COPD. The 36% reduction in the rate of exacerbations observed over 24 weeks in symptomatic patients is impressive. Combined with the significant improvements in lung function, symptom, and quality of life measures, as well as the favorable safety profile, these data confirm ensifentrine’s potential to change the treatment paradigm for COPD patients.”

And from David Zaccardelli (Verona CEO):

The totality of the ENHANCE data including improvements in lung function, symptoms, quality of life measures, and reduction in exacerbations, coupled with the consistent, favorable safety profile, support our belief that ensifentrine will change the treatment paradigm for COPD. We plan to submit a New Drug Application to the US Food and Drug Administration in the first half of 2023.

This underlines the goodness of the results obtained and the concrete possibility of proceeding with the commercialization of the product. The application (NDA) will be submitted by the company by H1 2023 and the official response (PDUFA) is expected by H1 2024. This means that by H2 2024 the product will be able to obtain its first sales.

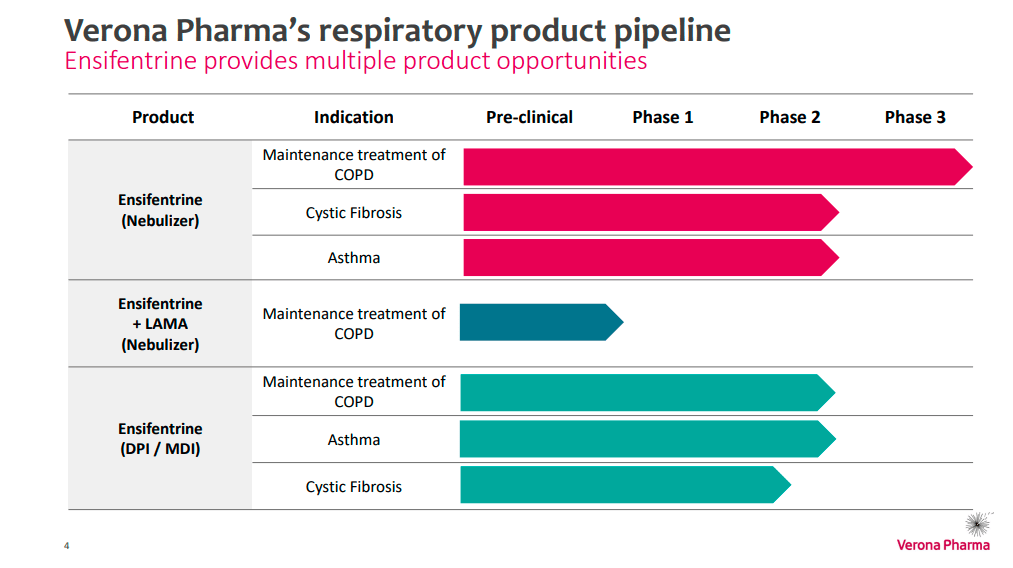

Ensifentrine could have applications also in asthma and cystic fibrosis and if we look at the pipeline we can see that the nebulizer product is in Phase 2 clinical trial. Also, the DPI/MDI products are in Phase 2, representing a good business opportunity in 2024 and 2025.

Investor Presentation 2023

Valuation, Competition, and Peers

Qualitative valuation

It is very difficult to formulate a share price evaluation related to companies that do not have a reliable business plan in terms of sales, revenues, cash flow, and operating costs. Even the part relating to the balance sheet and financial statements is quite approximate if contextualized to the future potential growth and sales.

Avoiding making very risky and unlikely predictions in the current state of things I decided to use a relative and qualitative assessment.

Using the Price to Book Value parameter we can have a relative view of how the Company performs related to the Sector median.

Seeking Alpha

VRNA P/B (TTM) is 7.53 and it is a high value if compared to the Sector Median of 2.07 we can state that VRNA at the moment performs worse than 265.72%. Even if we move on to the P/B 5Y average the figure passes to 5.27 and if compared with the Sector Median, VRNA continues to perform worse than 43%.

From the point of view of the balance sheet, comparing the data with the reference sector, the share price seems to be overrated but we have also to underline that the book value at this stage is very low and could not be fairly representative.

Competition

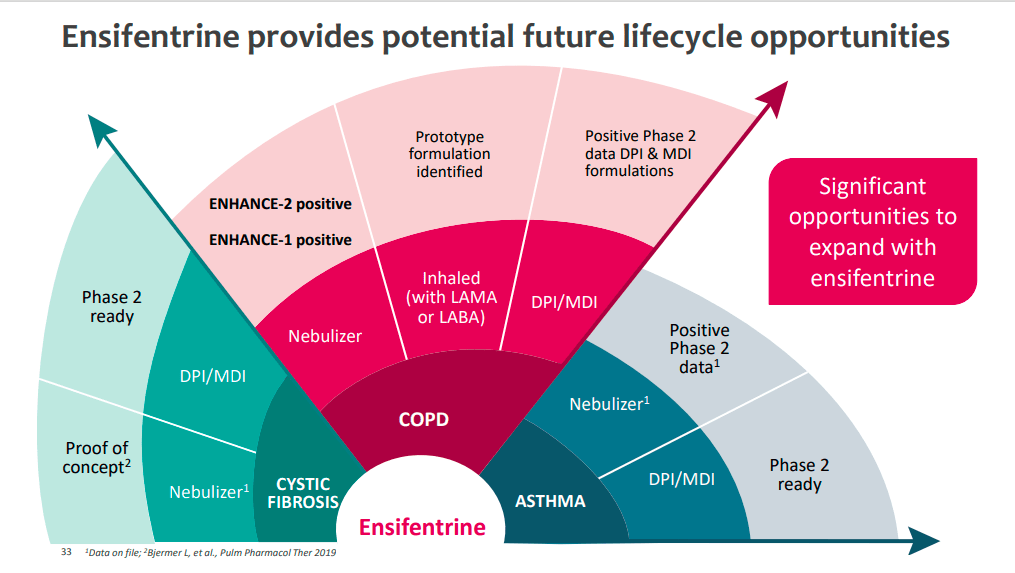

Ensifentrine is the only product that has anti-inflammatory and bronchodilator characteristics at the same time. It seems mainly that there are neither products on the market nor studies on the same chemical principles (PDE3 and PDE4). These unique characteristics allow ensifentrine to compete with all products used today for the treatment of COPD. In addition, it is conceivable that it can also be used in a complementary way to current therapies.

The following chart shows how Ensifentrine could be a potential Blockbuster in COPD disease treatments.

Investor Presentation 2023

Peers Comparison

Moving on to a more detailed comparison, I have selected the following company in Biotechnology and Pharmaceutical Industry involved in the clinical stage.

- Ventyx Biosciences, Inc. (VTYX)

- Arvinas, Inc. (ARVN)

- Aurinia Pharmaceuticals Inc. (AUPH)

- Galapagos NV (GLPG)

Using P/B value comparison:

|

VRNA |

VTYX |

ARVN |

AUPH |

GLPG |

|

|

Price/Book Vale (TTM) |

7.53 |

4.94 |

2.70 |

2.60 |

1.16 |

We can see how VRNA has the highest value and this underlines again that the price valuation at the moment is overrated.

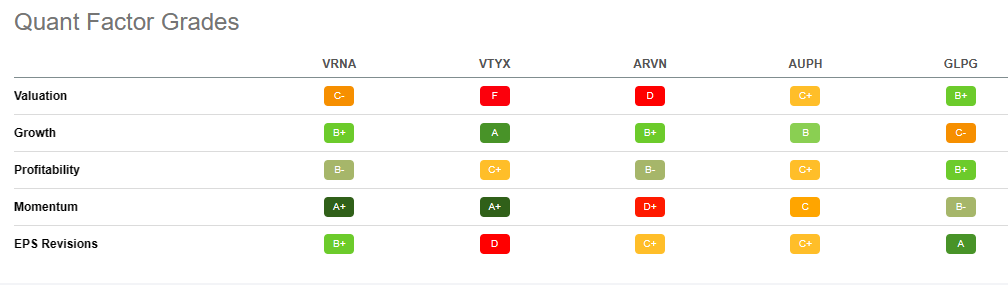

Using Seeking Alpha’s Quant Ratings we have, instead, a ‘Strong Buy’ verdict related to the ‘Hold’ or ‘Buy’ rating of the others company.

Seeking Alpha

Under the Quant Factor Grades point of view, we can see how VRNA is outstanding in Momentum with an ‘A+’ rate but in Valuation CLPG is preferable.

This comparison allows us to understand how at this moment VRNA could be the best choice with global factor grades in his favor.

Seeking Alpha

Many Risks could delay the potential return

At this moment, the financial part of the company seems solid and such as to seem to predict the continuation of operations for next year. The results of the studies are particularly positive and therefore the company’s core business does not represent an element of high risk when compared to other factors exogenous to the company itself. We must underline that at the moment there is no product on the market and that Ensifentrine requires FDA (in the US) and EMA (in Europe) approval before it can be placed on the market. This aspect represents a high-risk element in terms of market timing or terms of costs necessary for the continuation of operations before the first revenues.

Even the production and commercial partnership in place with foreign markets could represent an element of risk as it is not directly controlled by Verona.

Conclusion

Verona seems to be well-positioned to win the challenge in a broad market with significant unmet demand, the COPD treatment. Ensifentrine (the core company product) is in Phase 3 completed with positive data on lung measures and this means that in 2024 investors could see the first sales. Also from a commercial point of view, the company seems to have targeted the opportunity with potential large adoption and potential Medicare Part B reimbursement channel. Share price valuation seems to be expensive but also potential returns could be great. At the moment all pillars seem well grounded and my rate is Buy.

Be the first to comment