metamorworks/iStock via Getty Images

We have previously covered Verizon (NYSE:VZ) here as a post-FQ3’22-earnings article in November 2022. As a result of the underperformance compared to its competitors, the stock is now trading near 11Y lows, down -35.9% from its peak of $61.5 in mid-2020. This is no wonder, due to the deceleration of postpaid net customer additions by -75.5% YoY and expanding postpaid phone churn rate from 0.74% to 0.92%. The only saving grace at that time, was its dividend yield of 6.55%, which has grown tremendously from 5.05% since our first article in July 2022. However, the expansion must also be viewed in the context of its tragic stock price declines thus far.

For this article, we will focus on VZ’s forward prospects in the 5G market, on top of its partnership with Amazon’s (AMZN) AWS cloud network. Assuming moderate success ahead, the former may experience a quick turnabout, reversing some of its declining stock valuations. Furthermore, with a 19.5% upside potential from current levels, the stock appears to trade with a relatively attractive risk/reward ratio, made sweeter by the speculative dividend yield of 6.9%.

The 5G Investment Thesis Is Robust

By early December 2022, VZ has announced that it is 13 months ahead of schedule in its rollout of C-band wireless airwaves, offering its leading 5G wireless service by Q1’23. That is impressive indeed, given the ongoing supply chain disruption thus far. Furthermore, the 5G Ultra-Wideband will be made available to all US states simultaneously, boosting its chances of success from FQ1’23 onwards. At the time of writing, 175M Americans are already covered by the service, with buildout further accelerating moving forward.

This news is no surprise, since VZ has been aggressively expanding its clearance for the second phase C-band spectrum in 30 major cities since March 2022, notably ahead of schedule by 21 months as well. In addition, the company plans to enhance capacity by activating 100 MHz of C-band spectrum, increasing by 66% from its previous 60 MHz, with an improved capacity of up to 200 MHz of C-band in select markets. This expansion naturally builds upon the company’s ambitious $45.5B investment in 2021, when the Federal Communications Commission auctioned off the C-band spectrum, a repurposed spectrum from satellites that helps to accelerate the deployment of 5G.

Retail demand may be robust, since VZ’s 5G Ultra Wideband service offers peak download speeds of up to 1 Gbps, against the current market 4G offering of up to 35 Mbps, though notably lower than T-Mobile’s (TMUS) Ultra Capacity 5G spectrum of 3 Gbps. The users will have access to remarkable high-speed wireless connectivity on the go, which was previously only available when connected to home internet. These include downloading large documents or 4K movies within seconds, and playing console-quality games, while also conducting fluid video chats/video conferencing on the move. Therefore, the nationwide 5G launch may likely boost the growth of its post-paid net additions with the timely launch of the iPhone 14, as with broadband net additions. We’ll see by H1’23.

VZ has also partnered with AMZN to provide 5G network edge computing with the AWS Wavelength. In doing so, the partnership aims to create 5G applications and services for web-connected industrial devices, which would perform better with lower latency, faster speeds, and expanded capacity. An example of the industrial solution is AMZN’s IoT TwinMaker, which allows developers to build digital twins of building, factory, and production lines. These platforms will then be used to optimize building operations, increase production output, and improve equipment performance without shutting down physical operations. Hans Vestberg, Chairman and CEO of Verizon, said:

And as proud as I am to have crossed this milestone, I am equally proud of the way we are building our network – with the most advanced technologies, industry leading security, a robust fiber underpinning and a robust and varied spectrum portfolio. We are building this right. We are building this as a platform for innovation for years to come. (Seeking Alpha)

On the same note, Nvidia (NVDA) already has multiple partnerships, including BMW, which is building a digital twin of one of its automotive plants using the former’s Omniverse. Accelerated computing and high-performance 5G connectivity naturally improve industrial economics and outcome, which proves to be highly crucial post-reopening cadence and ongoing supply chain disruptions. VZ has also branched into the automotive industry for fleet management, which helped reduce fuel costs and increase productivity/ customer service with digital technology solutions. Alan Falik, president of Poolsure, said:

We’ve seen a sharp decrease in accidents, speeding, violations and out of service events. I have managers in Florida, Louisiana and all throughout Texas – I really need them to have access to real-live information that they can react to at any moment. Verizon Connect allows my managers to focus on what’s most important to my company – that’s making sure my drivers get home safe every night. (Verizon)

While it remains to be seen if VZ will succeed in the intermediate term, AWS has been the leading provider of global cloud services thus far, with record revenues of $62.2B in FY2021 and $58.7B YTD. The latter also boasts the leading global market share of 34% by the latest quarter, exceeding the combined market share of its two largest competitors, Microsoft Azure (MSFT) at 21% and Google Cloud (GOOG) at 11% at the same time. Therefore, tremendously improving VZ’s chances of success in the 5G edge market moving forward.

The overall market demand for high-speed internet has been accelerating as well. The three leading US telecom companies reported 1.29M new wireless consumer adds in the latest quarter, despite the rising inflationary pressures. According to the latest November CPI report, consumers also continue to spend an increased 0.9% sequential sum on broadband solutions.

Lastly, we must not forget that VZ still holds the leading market share in the US telecom market at the time of writing, with 120M regular monthly customers, compared to AT&T’s (T) 84M and TMUS’ 90M. Impressive indeed, despite the massive churn recorded thus far. In addition, the company has established a partnership with Disney (DIS), offering 6 months of free Disney+ subscriptions with select plans. With the latter does not break down its subscription by country, Disney+ boasts growing global subscribers of 164.2M in the latest quarter, with 46.4M attributed to the US and Canada region.

Therefore, VZ’s growing partnerships and 5G strategy may provide critical tailwinds for future growth, potentially triggering the recovery of its stock valuations by H1’23.

So, Is VZ Stock A Buy, Sell, or Hold?

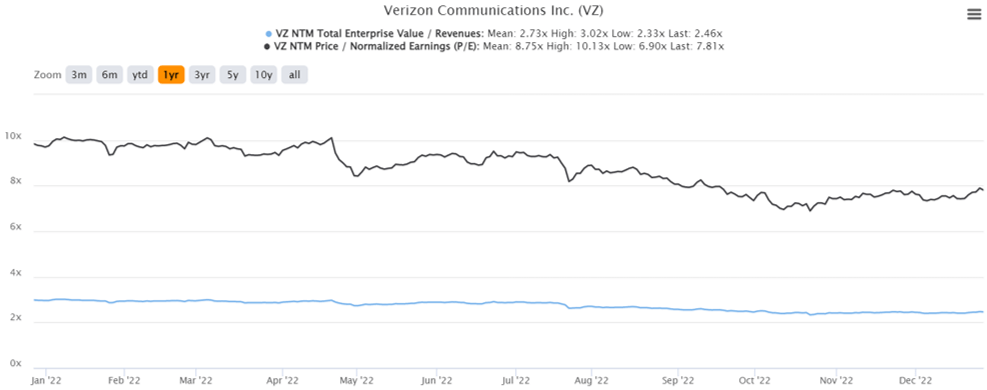

VZ 1Y EV/Revenue and P/E Valuations

S&P Capital IQ

VZ is currently trading at an EV/NTM Revenue of 2.48x and NTM P/E of 7.93x, lower than its 3Y pre-pandemic mean of 2.59x and 12.06x, respectively. Otherwise, the stock is still moderated against its 1Y mean of 2.72x and 8.74x, respectively. In comparison to its peers, T at NTM P/E of 7.20x and TMUS at 22.36x, VZ is also trading with a massive baked-in pessimism. It is no wonder, since T & VZ are expected to record a minimal revenue CAGR of 0.4%/1.8% and EPS CAGR of 1.6%/-0.5% through FY2025, compared to TMUS’ stellar performance at 3% and 30%, respectively.

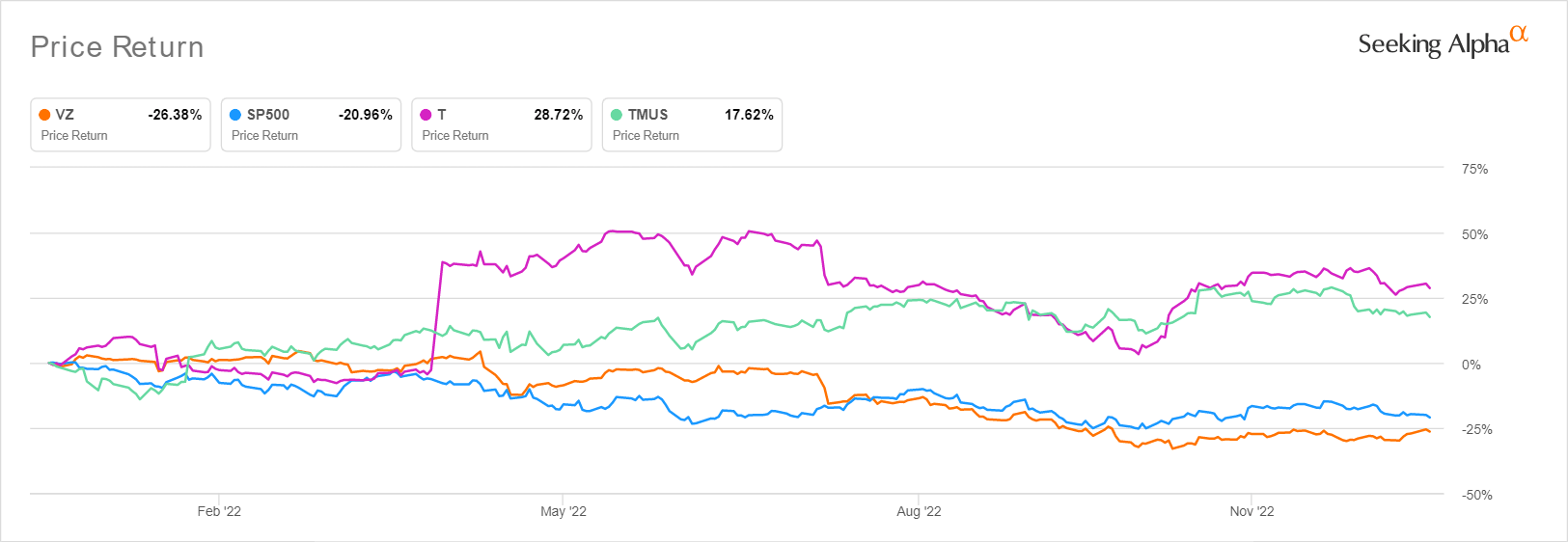

VZ 1Y Stock Price

Seeking Alpha

Nonetheless, we choose to remain optimistic about VZ’s short-term prospects, due to the potential success it might enjoy from the 5G segment. Based on its projected FY2026 EPS of $5.48 and current P/E valuations, we are looking at a moderate price target of $43.45. These mirror the consensus estimates’ price target of $47.11 as well, suggesting an excellent 19.5% upside potential from current levels, significantly aided by the stock declines of -24.5% YTD.

VZ’s 22 years of consistent dividend payouts may also assure long-term investors, since the company is projected to pay $2.75 by FY2025. These suggest a speculative dividend yield of 6.9% for those who add at current levels, against its 4Y average of 4.66% and sector median of 3.36%.

Combined with the abovementioned factors, we continue to rate the VZ stock as a speculative Buy. Naturally, the bleak macroeconomic outlook is unlikely to lift anytime soon, triggering more short-term volatility for investors who add at current levels. However, we reckon that most of the pessimism is already baked in, suggesting its relatively attractive risk/reward ratio in the long term. Naturally, the stock should only be viewed as a dividend stock. Therefore, anyone looking for high-growth stock should probably look elsewhere.

Be the first to comment