Bruce Bennett/Getty Images News

Verizon Strong Buy Thesis

I have been compelled to write a follow-up article to my previous Verizon Communications Inc. (NYSE:VZ) article (“Verizon: Strong Like Bull”) published approximately one month ago for two reasons.

Seeking Alpha.

First, VZ stock is up 11% in short order since my last piece, so I did kind of feel like taking a bit of a victory lap. Especially after taking such a shellacking from the bears on my last piece. Secondly, there has been a flurry of bearish articles recently stating something wicked this way comes for Verizon shareholders. Many pundits have been espousing Verizon is headed for trouble and shareholders should brace for impact or chaos. Others are stating there are significant issues to be concerned regarding Verizon’s business and cash flow prospects going forward.

Well, I am here to set the record straight! Let’s get started with the bull case!

The bottom is in

The crux of my last piece was the fact that Verizon had formed a solid bottom after consolidating at the lows for approximately three months.

Verizon chart 12/23/22

Finviz

Right after my article, the stock began to rise precipitously and is now up 10% on the month. Now, I am not taking credit for moving the stock. The fact of the matter is when you see consolidation action like this, my 30 years of experience has taught me that sooner or later you run out of sellers and the stock naturally begins to drift higher.

Verizon chart 1/12/23

Finviz

The primary takeaway from the current VZ stock action is that the bottom is in. This substantially improves the margin of safety for those looking to start a new position. There is strong major support for VZ at the $38 level.

The primary issue I have with the latest bear pieces on Verizon, and I have read them all, is the fact that nowhere in any of them do they reference the dividend. I find this extremely perplexing and downright disconcerting, as Verizon’s most important data point for the majority of shareholders is the safety and consistency of the dividend. So, I decided to write this follow-up piece and make my case Verizon is a strong buy here and “I ain’t got no way to lose.” Let me explain!

My Four Pillars of Dividend Investing

When looking for holdings to add to my Seeking Alpha Dividend & Income Marketplace service, I have four primary attributes I look for prior to digging deeper into the due diligence. If the stock does not pass these four tests, I place it on my watchlist and move on.

Needless to say, Verizon made the cut. The four pillars are: 1) Have a strong growth story; 2) Have a history of solid free cash flow that adequately covers the dividend; 3) Be reasonably valued or more preferable undervalued fundamentally; and 4) Have a safe and dependable dividend payout with and adequate yield.

Let’s see how Verizon stacks up.

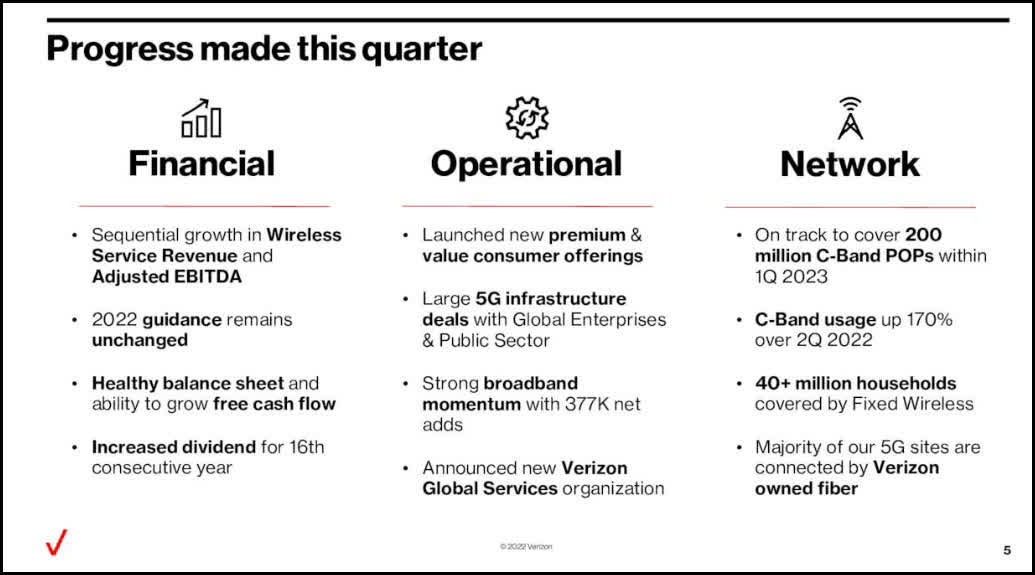

Verizon’s business growth story

Verizon is in the 5G and wireless phone business primarily. This business isn’t going anywhere. As a matter of fact, I see it growing by leaps and bounds as we move into the future and the technology continues to improve. The fact of the matter is that no one goes anywhere without their phones these days. Furthermore, you really need a phone to operate in today’s society. I don’t know anyone that doesn’t go anywhere without their phone. Below is a slide detailing the current state of affairs regarding their business efforts.

Verizon

So check the “Verizon has healthy business prospects” box. Now let’s move on to the next important element, strong free cash flows and a healthy balance sheet.

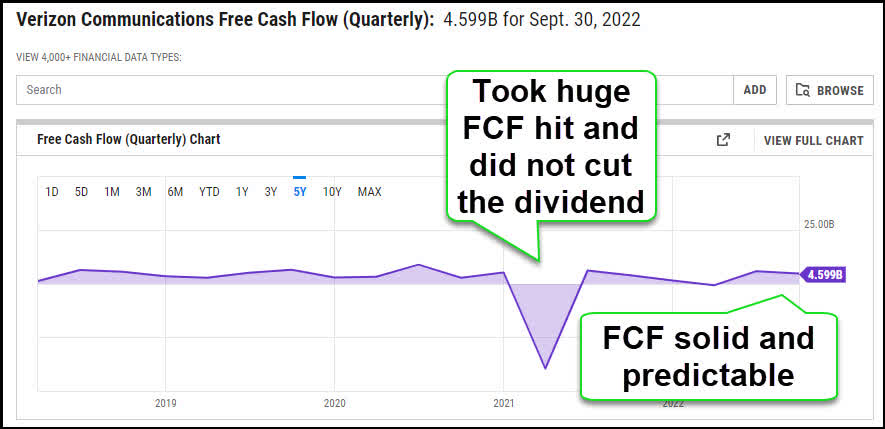

Verizon’s free cash flow status

Verizon has shown it can create solid free cash flow (“FCF”) on a sustained basis. What’s more, when they did take a hit in early 2021, they did not cut the dividend as many predicted. If fact, they keep right on raising it.

Verizon 5 year FCF Chart

YCharts

Free cash flow has remained steady and predictable over the years. In fact, CFO Matt Ellis stated on the latest earnings call:

“We are building momentum and remain confident that our strategy will deliver strong cash flow growth into the future. It is this confidence, combined with the health of our balance sheet, that enabled us to recently increase our dividend for the 16th consecutive year. We recognize the importance of the dividend to our shareholders, and we intend to continue to put the Board in a position to approve annual increases.”

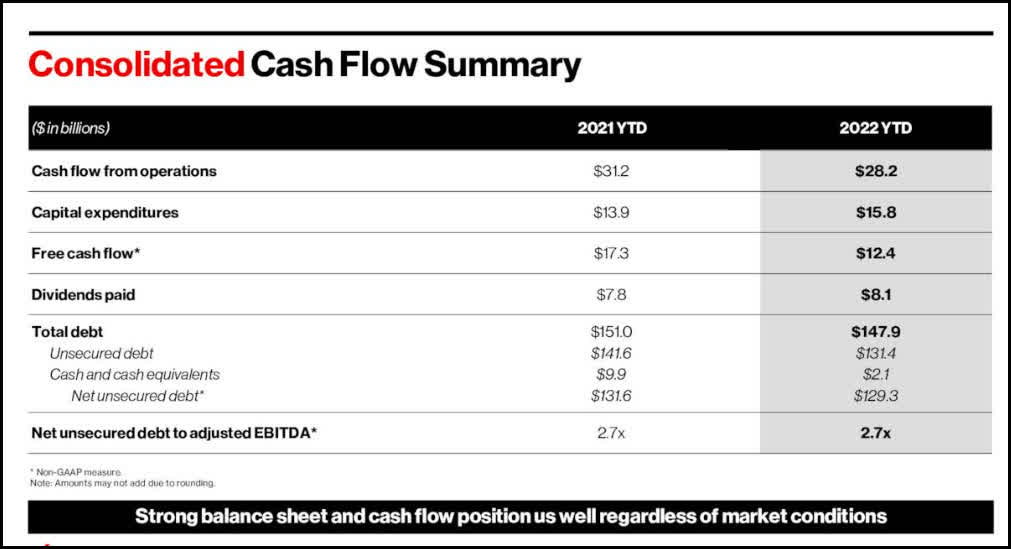

Below is the latest free cash flow slide from Verizon.

Verizon Consolidated Free Cash Flow Summary

Verizon

So we can check off the solid and consistent free cash flow pillar. Now, let’s move on to the valuation metrics.

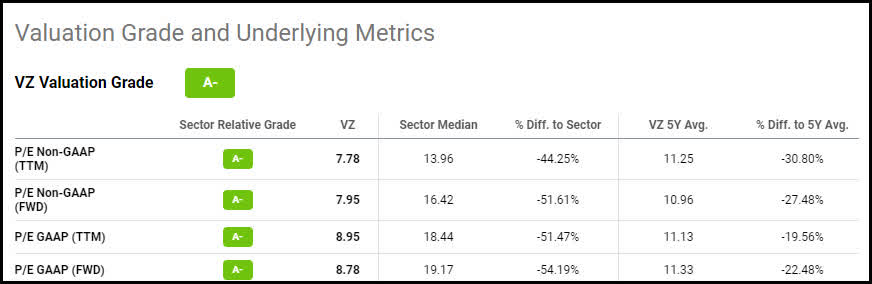

Verizon valuation analysis

Verizon is one of the cheapest large cap communications stocks in the sector. Only AT&T Inc. (T) is cheaper, yet just by a hair with a forward P/E of 7.58 versus Verizon’s at 8.19. The fact of the matter is that they are both vastly undervalued at present.

Verizon valuation underlying metrics

Verizon score an A- regarding its present valuation according to the Seeking Alpha quant metrics. It is currently trading for a 44% discount to its peers and a 31% discount to its 5-year historical average.

Seeking Alpha

It is easy to see VZ stock is undervalued, not to mention it is trading 25% below its recent 52-week high. This equates to a potential for 50% upside in the stock if it recaptures that level. Now let’s turn our attention to the most important factor, the dividend itself.

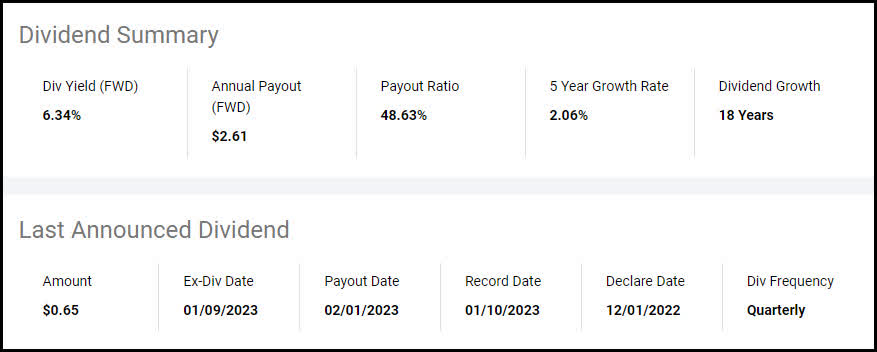

Verizon dividend analysis

Below are Seeking Alpha’s dividend summary statistics.

Seeking Alpha

What stands out to me is the superior VZ yield of 6.34%, the more than adequate payout ratio of 48%, and the 18 years straight of dividend payments and growth. Let’s dig a little further into the details, shall we?

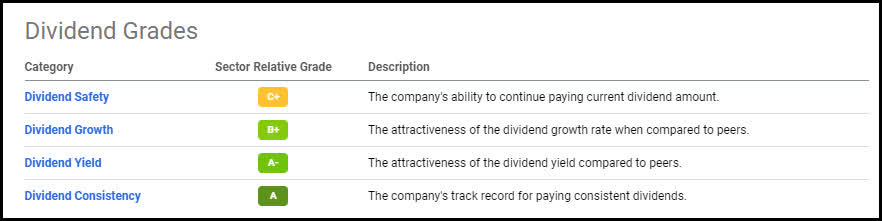

Seeking Alpha’s quant dividend grades

Seeking Alpha’s quantitative analytics does an awesome job of breaking out what is important. Moreover, it provides some unbiased scores based solely on the empirical evidence. I am going to skip the dividend safety grade due to the fact we have already covered that in the previous sections. Let’s dive in and take a look at the consistency of the dividend.

Seeking Alpha

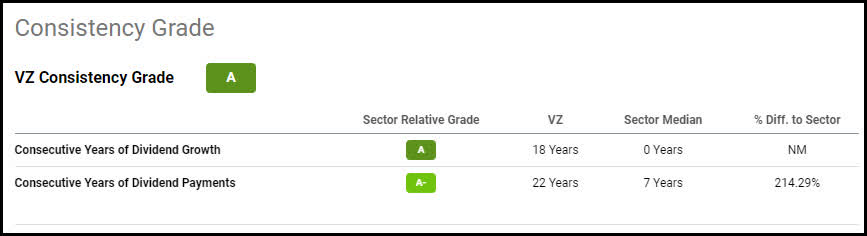

Dividend Consistency A

Verizon’s dividend has been one of the most consistent over the years. Its easy to see why it scores an A.

Seeking Alpha

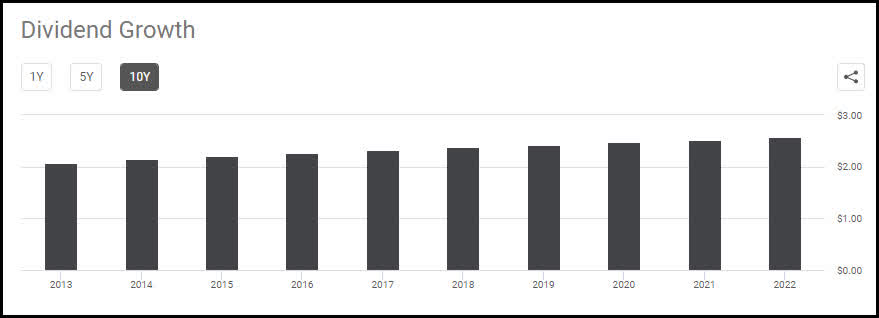

Verizon has paid the dividend each year for the past 22 year without fail. Moreover, it has managed to grow the dividend for the past 18 years. Keep in mind this was while enduring the great recession of 2008. Below are a couple charts detailing the progression of growth through the years.

Verizon 10-year dividend growth chart

Seeking Alpha

Verizon last five years of dividend growth

YCharts

I like this chart because it shows better the slow and steady increase of the VZ dividend over time. Slow and steady wins the race. Now, let’s turn our attention to the current yield.

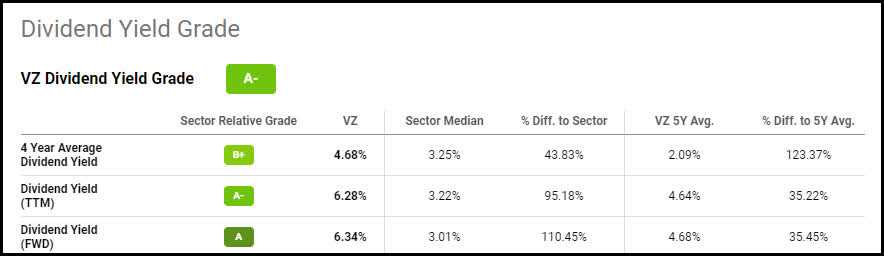

Verizon scores an A for yield

Seeking Alpha

Verizon takes the cake when it comes to the yield. The 6.34% yield is the highest in the DJIA. Furthermore, it is 43% above the sector median and 123% above its 5-year average. Locking in the yield at these levels is a no-brainer. Plus, a majority of analyst predict the dividend growth to continue. This is basically the icing on the cake, so to speak.

Consensus future dividend estimates

A majority of analyst expect Verizon will be able to continue raising the dividend in the coming years.

Seeking Alpha

I don’t put a whole lot of faith in these projections, but at least it is nice to know they don’t predict it is going to go down. Now, let me wrap this piece up.

The Wrap-Up

As I stated in the title, “I ain’t got no way to lose” as a Verizon long. You know why? Because if VZ does sell off for whatever reason, that simply creates a better buying opportunity for me. It gives me a chance to lock in a higher yield and hopefully improve my basis. When managing my income positions, as long and the four pillars remain intact, I look at a selloff as a buying opportunity. Remember, it is buy low and sell high, not the other way around. What’s more, CEO Hans Vestberg stated on the last conference call:

“Based on our momentum and plans, our financial guidance for 2022 remains unchanged. In this period, we have designed a company-wide cost savings program that we expect will save between $2 billion to $3 billion annually by 2025.”

The fact that the CEO has reaffirmed guidance and has a major cost savings program in place helps me to sleep very well at night (“SWAN”). That is why Verizon is one of my cornerstone positions in my SWAN dividend income portfolio. Those are my thoughts on the matter, I look forward to reading yours.

Be the first to comment