Daniel Balakov

All eyes will be on Verizon Communications Inc. (NYSE:VZ) when it reports its Q4 results in 2 weeks (January 24th). With the macroeconomic uncertainty intensifying and inflationary pressures mounting on the pockets of its consumers, investors will be closely watching how the company’s revenue gets impacted in its upcoming earnings report. But in addition to tracking its headline financial figures, investors may also want to closely monitor Verizon’s churn rate, subscriber additions, segment financials and its management’s outlook for the quarter ahead. These items will reveal how well is the company navigating muddy waters and are likely to have a bearing on where its shares head next. Let’s take a closer look at it all.

Operating Metrics

Let me start by saying that Verizon’s top brass has done a good job at growing the business over the past decade. While many prominent telecom companies couldn’t maintain high levels of capital expenditures and went out of business, Verizon management adopted a prudent capital allocation strategy to pay dividends, reinvest surplus cash flow towards growth initiatives and grow their top line over the years. This is a commendable feat and an enviable position to be in, especially in the cutthroat telecom services industry.

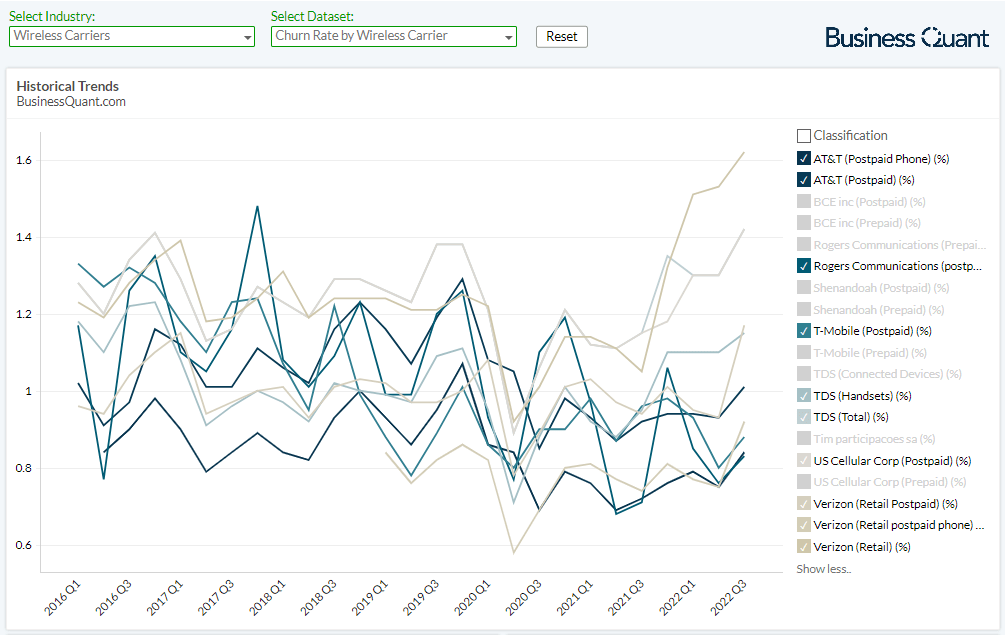

With due credit given, I’d like to add that investing is more about looking into the windshield and less about looking in the rearview mirror. Inflationary pressures are already weighing down on consumer spending, and Verizon decided to hike its prices a few months ago. So, as investors, the first order of business should be to monitor if this pricing event is resulting in the mass exodus of price-sensitive consumers, or if it is business as usual for the company. We can do this by monitoring Verizon’s churn rate and its subscriber additions.

For the uninitiated, churn rate is basically the pace at which existing subscribers are disconnecting their connections with a telecom company or a utility provider. Note in the table below how Verizon’s churn rate soared in the last quarter shortly after it rolled out price hikes across the board. This meant that customers disconnected their Verizon connections at a rapid rate likely because they switched to a competing service (maybe AT&T’s (T)?) that offered better value propositions.

BusinessQuant.com

I estimate that Verizon’s churn rate will stabilize at its elevated levels and remain flat in Q4, without fluctuating materially in either direction. I say this largely because Q4 will be the second full quarter since the price hikes were announced, which means price-sensitive dissatisfied customers would still be in the process of migrating away to rival services. But needless to say, any further increase in Verizon’s churn rate will indicate that customer exodus has accelerated, which is likely to spread panic amongst investors and trigger a selloff in its shares.

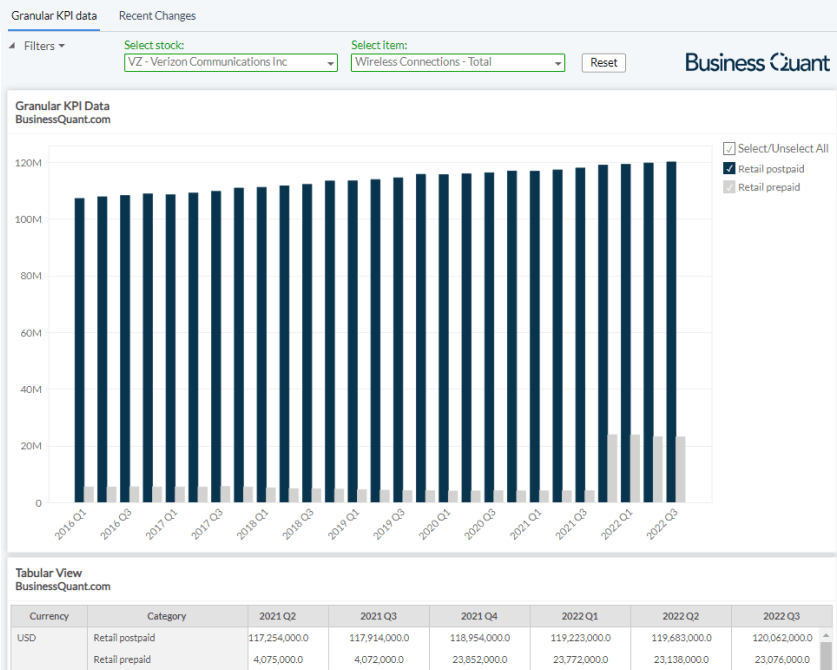

Moving on, also tracking Verizon’s connections count will provide us a well-rounded picture of its competitive positioning. Note how the company had been rapidly adding retail prepaid and postpaid connections since 2020 but its growth was muted last quarter with the implementation of price hikes. I contend that its connections growth will remain stalled in its upcoming earnings report as well, as it’ll be difficult to convince new customers that the recently increased prices will bring along relatively superior network experience (in terms of speed, coverage, uptime, support, etc.).

BusinessQuant.com

These metrics will basically reveal how well is Verizon’s subscriber base absorbing the price hikes. Ideally, it’ll be in the best interest of the company’s shareholders if the churn rate declined and subscriber adds accelerated, but that seems unlikely in Q4, as customers are forced to absorb these price hikes well ahead of its 5G Ultra-Wideband services. But having said that, let’s now shift attention to Verizon’s financials.

Bifurcated Financials

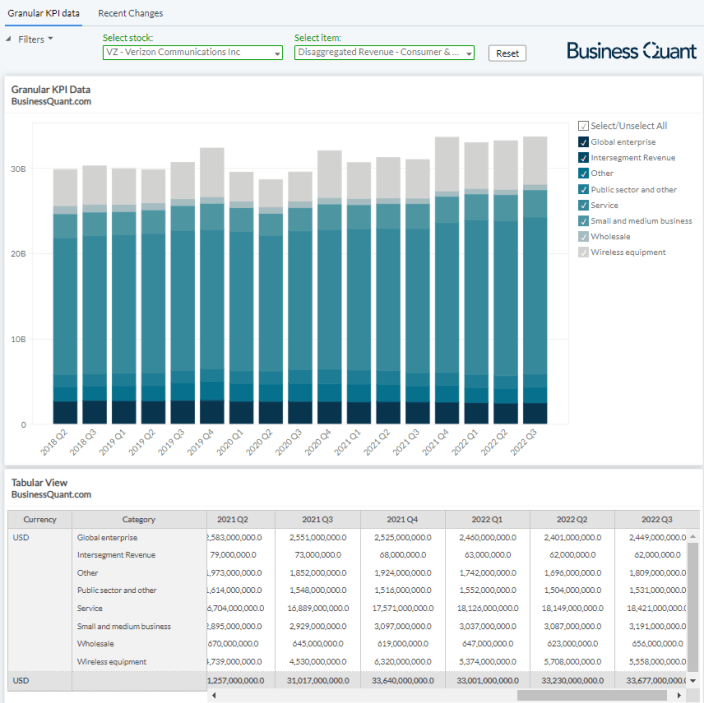

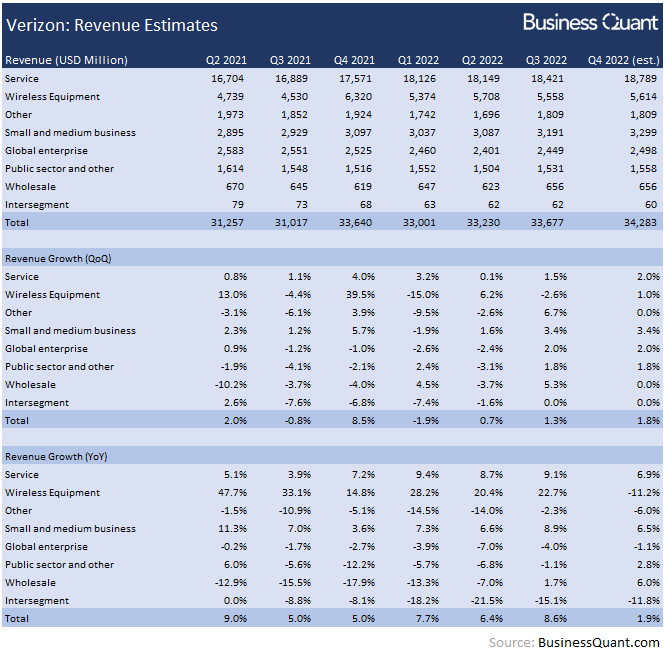

It’s worth noting that Verizon classifies its revenue into broadly 8 different sub-segments. Its consumer-facing Service segment is by far the largest in terms of revenue, accounting for nearly 55% of the company’s top-line last quarter. With the implementation of price hikes, Verizon’s Service revenue is likely to get a boost. At the same time, its elevated churn rate and muted subscriber additions will undo some of these gains. So, I anticipate Verizon’s Service revenue in Q4 to grow 2% sequentially, and amount to roughly $18.78 billion.

BusinessQuant.com

The Wireless Equipment segment is the second biggest revenue driver for the company, representing 16.5% of total sales last quarter. It includes the sale of smartphones, handsets and other wireless-enabled devices such as smartwatches. These payments can be upfront and they can also be broken down in monthly installments. Since there is a recurring element attached to these payments, the price hikes should ideally have a minimal impact on this revenue stream. Therefore, I estimate this segment to post revenues to the tune of $5.5 billion, marking a sequential increase of 1%, but it would also mean a deceleration from the 1.8% growth registered in last 2 quarters.

Moving on, Verizon’s SMB, Public Sector and Enterprise businesses collectively accounted for nearly 21% of the company’s total sales. These segments provide services such as private networking services, VOIP, unified communication tools, network security services, IOT, in addition to core voice and data solutions to a range of enterprises as well as to government agencies. The segments have been posting healthy revenue growth rates due to expanded geographical footprint of wireless and high-speed broadband services, at attractive price points, amongst enterprise clients. Since this growth is diversified and doesn’t hinge on 1 or 2 catalysts, I expect this growth trend to continue on in Q4 as well, with their sequential revenue growth rates to remain in line with Q3-levels.

The remaining 3 segments, namely intersegment, wholesale and others, are immaterial to Verizon’s top-line and lack meaningful catalysts to have a notable impact on the company’s sales anytime soon. So, for the sake of simplistic modelling, I’m anticipating these revenue streams to remain sequentially flat in Q4. This brings us to a company-wide operating revenue estimate of $34.28 billion. The Street’s overall revenue estimates, for the record, span from $34.74 billion and $35.25 billion for the said quarter.

BusinessQuant.com

But with that said, pay close attention to Verizon management’s revenue and churn rate outlook for Q1 FY23 and for FY23 overall. It would shed light on how the company’s customers are responding to the recent price hikes and how the company is positioned amongst its competitors.

Final Thoughts

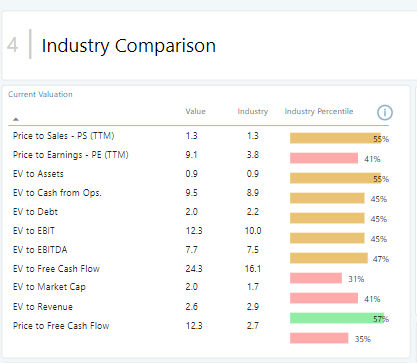

As far as valuations go, Verizon Communications Inc. is trading at industry median levels on a range of parameters. This implies the stock is more or less fairly valued at current levels and it isn’t the screaming buy that many bulls are leading us to believe.

BusinessQuant.com

But perhaps the bigger takeaway here is that Verizon’s consumer business will remain revenue-challenged in the near future. The enterprise-focused segments offset the weakness on the consumer side last quarter, but if recessionary pressures pile on, then enterprises across the globe might cut their discretionary spend, which might as well drag Verizon’s FY23 projections lower.

Hence, I expect the coming few months to be chaotic for Verizon Communications Inc.’s stock price. Investors may want to keep close tabs on Verizon’s churn rate, its subscriber additions, segment financials and its management’s outlook to better navigate these uncertain times. For now, I rate Verizon as a “Hold.” This, however, is not a call to short the stock. Good Luck!

Be the first to comment