gerenme

Company Overview

Polished.com (NYSE:POL) is an online retailer of kitchen appliances, including refrigerators, ranges, washers, and dryers. The company has a scale advantage over local appliance retailers that cannot carry a wide selection and command wholesale pricing that Polished can offer its customers. Polished ships appliances for free, and for a small fee, customers can have new appliances installed and old ones taken away.

But over the last couple of years, Polished has gone through some terrifying events that now present investors with a fantastic opportunity.

Polished.com’s disastrous history

In June of 2021, 1847 Goedeker, a public company involved in the online appliance business, completed an acquisition of Appliance Connection, a company multiple of its size. Before the tie-up, 1847 Goedeker had 6.1 million outstanding shares. To raise funds for the $200 million acquisition, the company sold about 182 million shares and warrants. Shares plummeted from their 2021 high of over $14 to under $2 after announcing the deal.

Appliance Connection survived the merger, and its CEO, Albert Fouerti, was named the CEO of Appliance Connection, and his brother Elie Fouerti the CFO. Mr. Fouerti appeared to be the man to run the company. He had grown Appliance Connection from a single retail appliance shop in Brooklyn, NY, to its current state as a major competitor in the e-commerce appliance market. The company was later rebranded as Polished.com.

Things appeared to be going along swimmingly. The full-year 2021 sales were up 46% to $541.7 million, and earnings vaulted from an $11.2 million loss to $28 million (these were Pro-forma numbers due to the mid-year acquisition). The first quarter of 2022 brought more good news. Sales were up 23.5% to $152.8 million, and earnings came in at $5.9 million. Management also reaffirmed its FY 2022 guidance, including net sales growth of high teens to low 20s. The report came at the beginning of supply chain and inflationary pressures that persisted throughout 2021.

That’s when the wheels started to fall off. In August, the company announced that it would delay second-quarter earnings, but sales were between $145 million and $150 million. The press release also noted that sales growth would be in the low double-digit range for FY 2022 due to supply change challenges that couldn’t keep up with demand. The announcement included another hideous revelation:

“The Audit Committee of the Company’s Board of Directors, with the assistance of independent legal counsel and consultants, has commenced an internal investigation regarding certain allegations made by certain former employees related to the Company’s business operations.”

In November, Albert and Elie Fouerti tendered their resignations. The board appointed Rick Bunka, an industry vet, and Bob Barry, 1847 Goedeker’s former Chief Accounting Officer, as CEO and CFO, respectively. In tandem with the announcement, Polished disclosed that it would also delay its third-quarter results due to its ongoing investigation.

In December, the company’s auditor resigned. Polished’s filings show that the auditor said there may be ‘material adjustments and disclosures necessary to previously reported financial information.’ It went on to say that the board’s internal investigation revealed that it uncovered facts that might cause the auditor to be no longer able to rely on the representation of management. Polished replaced the auditor within a week.

A few days later, Polished announced the results of its investigation. It showed that Fouerti charged the company $800,000 for expenses unrelated to the business, its damaged goods inventory accounting was lacking, and it lacked I-9 forms for its employees. It all seems like an anticlimactic conclusion to a months-long saga. Especially considering, Fouerti will pay $3.7 million to reimburse Polished for the non-business related expenses and the cost of the investigation.

It’s not as bad as it looks

The stock is down 75% over the last year. The stock’s downward spiral fall is likely a combination of the company’s horrendous internal affairs and a poor outlook for durable goods. There is probably more that went on behind the scenes than we’ll ever know, but a few things could put investors’ minds at ease.

Damaged goods are a genuine risk with Polished. It operates out of a few warehouses in New York and New Jersey, and 40% of its 2021 revenues came from products shipped to Midwestern, Southern, and Western states. Moving large items like refrigerators and stoves can cause damage over such a long haul. Worse, customers are upset.

Polished.com 2021 10-K

Having your auditor say there may be ‘material’ changes to your financial statement and then bolting can be reason enough to pass on the stock. But ‘material’ means different things to different people.

In management’s announcement, it said that it does not expect a material restatement of its 2021 results. However, it does expect to restate the first quarter 2022 results to reflect a decrease in revenue of $6 million to $8 million ($152.8 million reported) and a $5 million to $7 million reduction in COGS. Ultimately, the adjustments will decrease EBT between $1 million and $2 million.

Interim CEO Rick Bunka holds no shares and doesn’t seem to have a prior affiliation with Polished. Regardless, his attention has not been on business as much as investors would like. There’s work to be done tying up the investigation. In the meantime, Bunka will be searching for a permanent CEO. Interestingly, Polished will pay Bunka a handsome weekly salary that equates to $875,000 annually. Presumably, Polished will pay such a high salary for him to extinguish the company’s internal tire fire on an interim basis. When he brings in a new CEO, Bunka will receive a $437,500 bonus. More interestingly, if he sells the company, Bunka takes home a $2.2 million bonus. So, a sale of the company is one possible outcome here.

The company’s 2021 annual report contained a passage that noted its intention to expand its distribution by at least two fulfillment centers in 2022. Expanding its reach would cut down delivery times to customers, extend its reach, and cut down on damaged inventory returns.

Polished.com 2021 10-K

We’ll soon find out if management could execute its intentions or if the task will fall to the next CEO. Either way, I think this is a great business move to put Polished’s damaged inventory issue in its rearview mirror.

Investment Thesis

There are a lot of reasons to like the business. One could quickly say that Amazon will eat its lunch. But Amazon’s distribution isn’t designed to deliver items as large and heavy as a refrigerator or washer/dryer set, and their delivery folks aren’t equipped to install them. Home appliances are available on Amazon but available through third-party sellers.

It takes a unique and dedicated business model and higher volume to support large-scale home appliance distribution and delivery. Competitors outside Polished are Best Buy, Home Depot, and Lowe’s. Their locations and distribution systems make it possible to deliver bulky home appliances. Those competitors are much larger the Polished, but because they sell so many items outside of home appliances, they only stock a limited number of home appliance SKUs. Polished, on the other hand, solely sells home appliances and carries a more comprehensive selection of popular brands.

Local mom-and-pop home appliance retailers have traditionally carried the market but lack the scale to command wholesale prices from suppliers and are at risk of losing business to a short list of scalable competitors. More and more folks rely on the internet to make buying decisions, which should hasten the transition from shopping locally for home appliances to e-commerce sites like Polished and its host of platforms.

Polished has also built a B2B strategy that contracts with real estate developers to sell products directly to newly constructed homes. Granted, the near-term outlook for new homes isn’t great, but the B2B business could be meaningful in the long run.

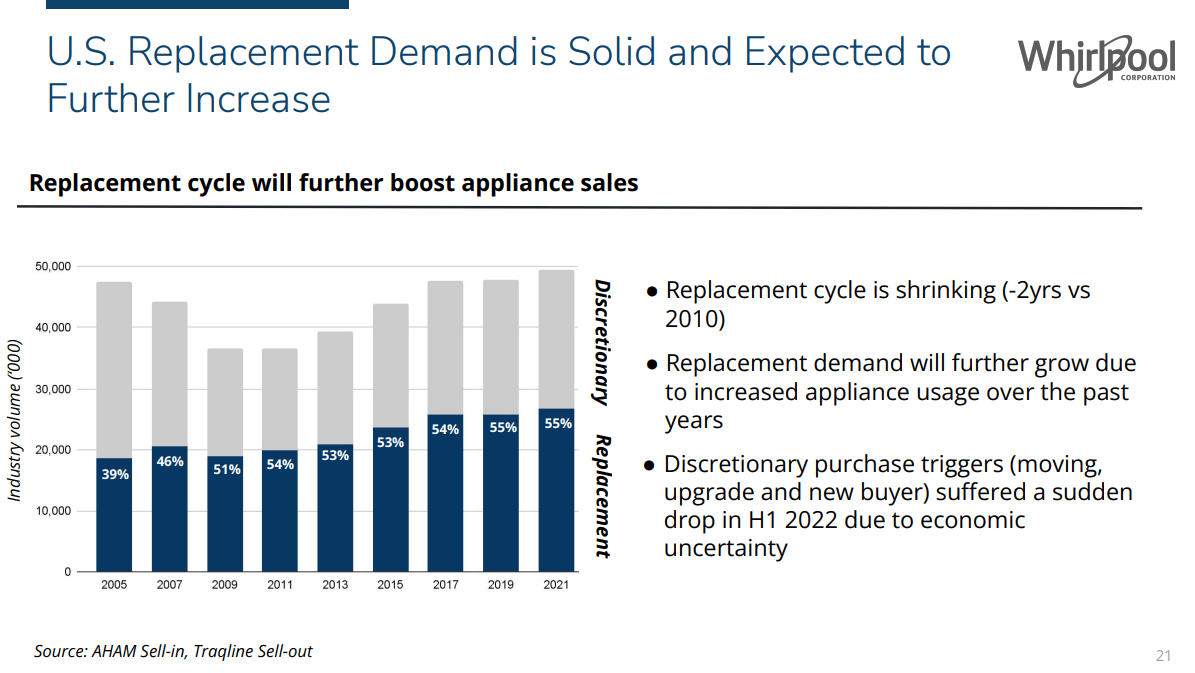

One of the most attractive characteristics of the business is that home appliances are needs, not wants. For instance, if your refrigerator or washer/dryer breaks down, it becomes a high-priority replacement. According to this slide from Whirlpool (one of Polished’s major suppliers), over half of the home appliance market is replacement sales.

Whirlpool Investor Presentation

Of course, the percentage is, in part, based on lumpy annual discretionary purchases. That’s probably why Whirlpool conveniently left out 2020, a boon year for discretionary spending. Though the 2020 bump provided fuel for an upcoming replacement cycle. The chart points toward a powerful ongoing demand for home appliance replacement. Replacement business would certainly cushion the blow of an economic downturn.

Risks

Polished hasn’t published a financial statement since the first quarter of 2022, which the company will likely reinstate. That could make the stock a hard pass for some investors. Current management has reassured investors that downward adjustments will be minor. They also stated that, as of September 30th, they have $26.5 million in cash (slightly more than it last reported in Q1 22) and have not drawn on its $40 million revolver. That’s a positive indicator that the company still made money during a year with considerable internal turmoil and incendiary inflation.

After the company’s head-scratching capital raise, over 100 million shares are outstanding. In addition, 93.1 million public warrants which strike at $2.25 and expire in June of 2026 (about half a million private warrants that strike at $11 and $12. There’s almost no chance they’ll be exercised). Assuming the public warrants are exercised, roughly 200 million shares will be outstanding. That’s an astonishing sum that may be giving the stock a hangover.

The warrants shouldn’t be much of a concern. If the stock goes above the $2.25 strike price by 2026, the stock will be a wild success, and the company will receive a $210 million cash injection, but a duplicative wave of new investors will rudely join shareholders. Otherwise, the warrants expire with no further dilutive effect on shareholders or cash infusion.

Returned merchandise can tarnish your online reputation and diminish your presence. Polished committed to adding two fulfillment centers that would cut down on damaged returns, expand deliverable territory, and shorten delivery times.

Valuation

Share valuation requires a healthy dose of conservatism. The company reported $7.7 million in earnings in 2021 (management thinks the number is solid). But that included only half of the year with Polished. Doubling the number to reflect a full year gets the company to $15.4 million (their full-year Pro-forma earnings were $28 million).

In the first quarter of 2022, Polished reported earnings of $5.9 million. If we apply the high end of management’s adjustment range ($2 million), they earned $3.9 million. Four quarters of $3.9 million get the company to $15.6 million in earnings.

If you’re saying that simply extrapolating a few quarters’ earnings is a recipe for disaster, you’re right. But there are a few things that indicate we’re in the ballpark. Zero revenue growth would get the company over $600 million. A 3% net margin produces $16 million in earnings.

After the board’s investigation, management is confident that financial statement adjustments will be minor. Trusting management’s confidence can also be a mistake. But an increased cash balance and no draws on its credit facility could show that earnings have, at least, been able to support working capital, which has been a headache for almost every American company in 2022.

Operating costs may also come down. The company has two leases that Polish obtained from Goedeker and a small acquisition that came off the books at the end of 2022. The lease payments summed up to over $600,000 per year. That is on top of the $800,000 non-business expenses that Fouerti took in a few short quarters that won’t recur.

Polished’s cost structure would also help it sustain in a rough year. A quarter of its operating expenses are credit card fees associated with sales. Advertising is another roughly 15% of operating expenses that Polished can adjust downward if sales languish.

To be conservative, let’s adjust earnings down to $10 million in a year, which could be described as a train wreck. If that’s the case, the shares are trading at about 5.5x depressed earnings. That’s an attractive valuation for a company with a profitable long-term growth opportunity.

I think there is a significant chance that Polished will take market share and grow earnings over the next several years. If they do, they’ll command a much frothier earnings multiple.

Conclusion

It certainly appears that the company has put many of its concerns behind it. That’s no guarantee that more bad news won’t crop up, but several positives could surface soon. Appointing a permanent CEO would soothe investors. More importantly, leadership could start putting their internal issues to bed and focus on the business.

The company is authorized for 200 million shares to account for the warrants. Shareholders are voting at the January 19th annual meeting to bump that number to 250 million to provide for future stock compensation. Any candidate considering taking the helm will be closely watching the results, which are less than a week away. The company could appoint a permanent CEO shortly after that.

The bigger issue is the company’s financial statements. They’re two quarters behind, and there may be restatements. Sandler, Polished’s new auditor, was appointed at the end of 2022. They’re likely working tirelessly to get caught up. New statements should come forth in the coming months. There is a strong case that the results won’t be as disastrous as investors anticipate. The stock could get another boost, assuming the company has continued to generate earnings.

Given the discrepancy in Bunka’s incentive bonuses, his attention is more likely consumed by a sale of the company than by candidate CEOs. Corporate suitors will need to see audited books and records if a deal is to be struck.

The company also authorized a $25 million stock repurchase program in December 2021. I’d assign a low probability that Polished retired shares while the investigation was ongoing. But if their troubles are truly behind them and the company is on solid financial footing, they have a great chance to retire shares at a price so depressed the company could annihilate nearly half of its shares at the current price.

The company has gone through hell, and the stock price has been vaporized. But it could be near an inflection point. Over the next several months, there will be considerable action within the company. I think it will mostly be good news. But more importantly, I believe there is a great long-term story with Polished. However, it’s certainly not for the faint of heart.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment