Bruce Bennett

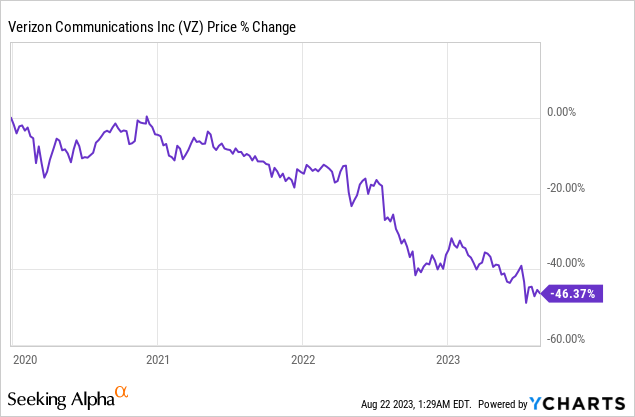

The Verizon (NYSE:VZ) stock is down more than 45 percent since hitting an all-time high in December 2019.

The falling share price, in turn, has led to a historically high dividend yield of almost 9 percent, well above the 5-year average of 4.8 percent! Unlike competitor AT&T (T), Verizon has also never had to cut its dividend. For 18 years, quarterly payouts have increased year over year, despite the financial crisis and the Corona crash. And compared with its competitors, Verizon doesn’t have to hide either. AT&T’s dividend yield, for example, is 7.9 percent after the dividend cut. At Deutsche Telekom (OTCQX:DTEGY), the dividend yield is only 3.6 percent. Only Telefónica (TEF) has an even higher dividend yield of 8.3 percent.

A sparrow in the hand is better than the pigeon on the roof

With a high dividend yield and an adjusted P/E ratio of under 7, everything looks like Verizon is the perfect stock for income investors. I can understand investors who would rather have a yield of 7 percent and no annual growth in distributions than a yield of 2 or 3 percent with the likelihood of higher increases. After all, it’s not certain that companies will increase their dividends by 10 or 20 percent every year. Dividend growth machines like CVS Health (CVS) or General Mills (GIS), are good examples of how annual growth can stop abruptly.

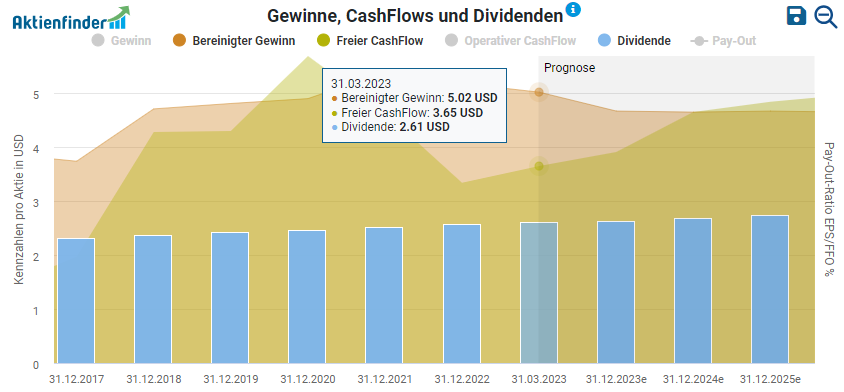

And yes, within the last few years, Verizon’s dividend has grown an average of about 2.5 percent per year. And according to analysts, the dividend is expected to rise by a similar amount again in September. That’s less than inflation in some cases, but it’s still something on top of the generous current yield. Even if business is a bit lame, I think the dividend is safe thanks to the stable cash flow and moderate payout ratios. Currently, the payout ratio is 71.5 percent based on free cash flow and 52 percent based on adjusted earnings.

{kind=link}

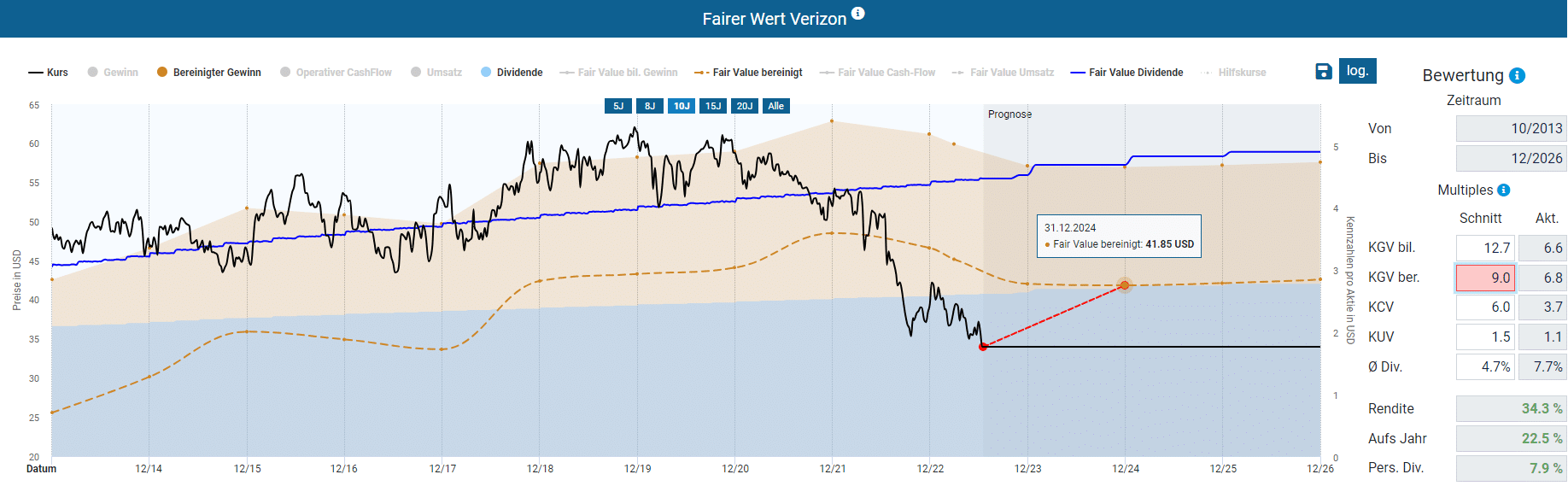

With an adjusted P/E ratio of 6.8, Verizon is trading well below its fair value of 11.9 measured over the last ten fiscal years. Looking at the previous five years, the average adjusted P/E ratio of 10.2 is also significantly above the current valuation. If we take these historical multiples as a basis, a current buy price of $33.02 through the end of fiscal 2024, including dividends, yields a potential annual return of nearly 46 percent.

Even if we set a margin of safety and the fair value of the adjusted P/E ratio at 9, this still results in a considerable potential return of 23 percent for the year to the end of fiscal 2024, including the dividend.

Verizon is a boring investment but in a negative sense

What bothers me about Verizon as an investor, however, is the quasi-guarantee of poor operating performance.

Verizon earns 80 percent of its revenue from its wireless division. The company’s wireless business manages a nationwide mobile network with about 93 million postpaid and 23 million prepaid customers. In addition, Verizon operates as a network operator, running network infrastructure such as fiber and either using it itself or marketing it to third parties for a fee. This can take the form of leasing network capacity or providing data transmission and connectivity services.

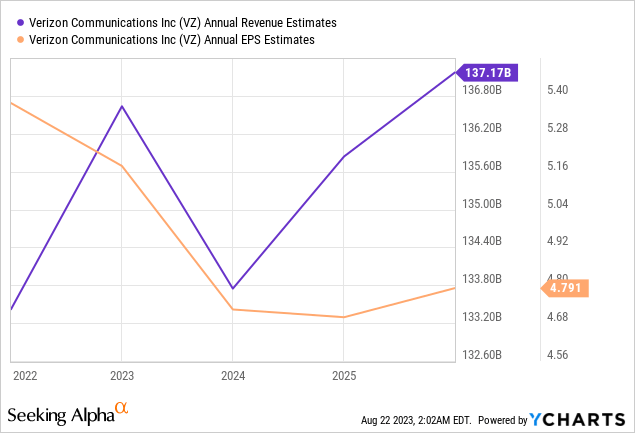

Despite the overwhelming importance of network infrastructure and wireless, revenue and profits have barely budged in recent years, as Verizon’s business has suffered from the highly competitive wireless market. Revenue, for example, climbed just five percent from $131.6 billion in fiscal 2015 to $136.8 by 2022, and analysts even expect revenue to decline to $135.3 billion in the current fiscal 2023. Verizon will be operationally stagnant in the coming years and will only be able to increase revenue minimally. The outlook for profitability paints a similarly bleak picture. For example, the operating margin is expected to improve only minimally from the current 22.2 percent to 22.5 percent by 2024. According to analysts, the net margin is even expected to fall by more than one percentage point.

The reasons for the declining margins lie in the tough price competition with T-Mobile US and AT&T. Verizon’s development of revenue per customer account, the Annual Revenue Per Account (ARPA), is an example of the high price competition in the mobile communications market. These were $125.97 for Verizon in fiscal 2022, but as high as $134.49 in 2018 and $152.63 in 2015.

Unlike AT&T’s report on ARPA trends, Verizon and T-Mobile US report ARPU trends, or average revenue per customer overall, without regard to the number of customer accounts in each case. Despite the different reporting methods, revenues have also been declining here since 2015. However, the decline at T-Mobile US is less pronounced than at AT&T and Verizon. ARPU at T-Mobile US has even been rising again since 2021.

| Dec ’15 | Dec ’16 | Dec ’17 | Dec ’18 | Dec ’19 | Dec ’20 | Dec ’21 | Dec ’22 | Dec ’23E | Dec ’24E | Dec ’25E | |

| ARPU Mobility Postpaid Phone AT&T | 60.5 | 59.0 | 52.5 | 49.1 | 50.2 | 50.0 | 49.1 | 49.6 | 49.7 | 49.7 | 49.3 |

| ARPU Postpaid T-Mobile US | 46.5 | 45.6 | 44.8 | 43.3 | 42.2 | 41.6 | 42.1 | 42.8 | 43.1 | 43.3 | 43.4 |

So Verizon is failing to implement higher prices despite the increase in data volume in recent years. It is therefore doubtful whether the introduction of 5G with higher data volumes will give the company more pricing power in the mobile market.

In my last article on AT&T, I already pointed out how counterintuitive this is. I called it the fairy tale of the 5G revolution:

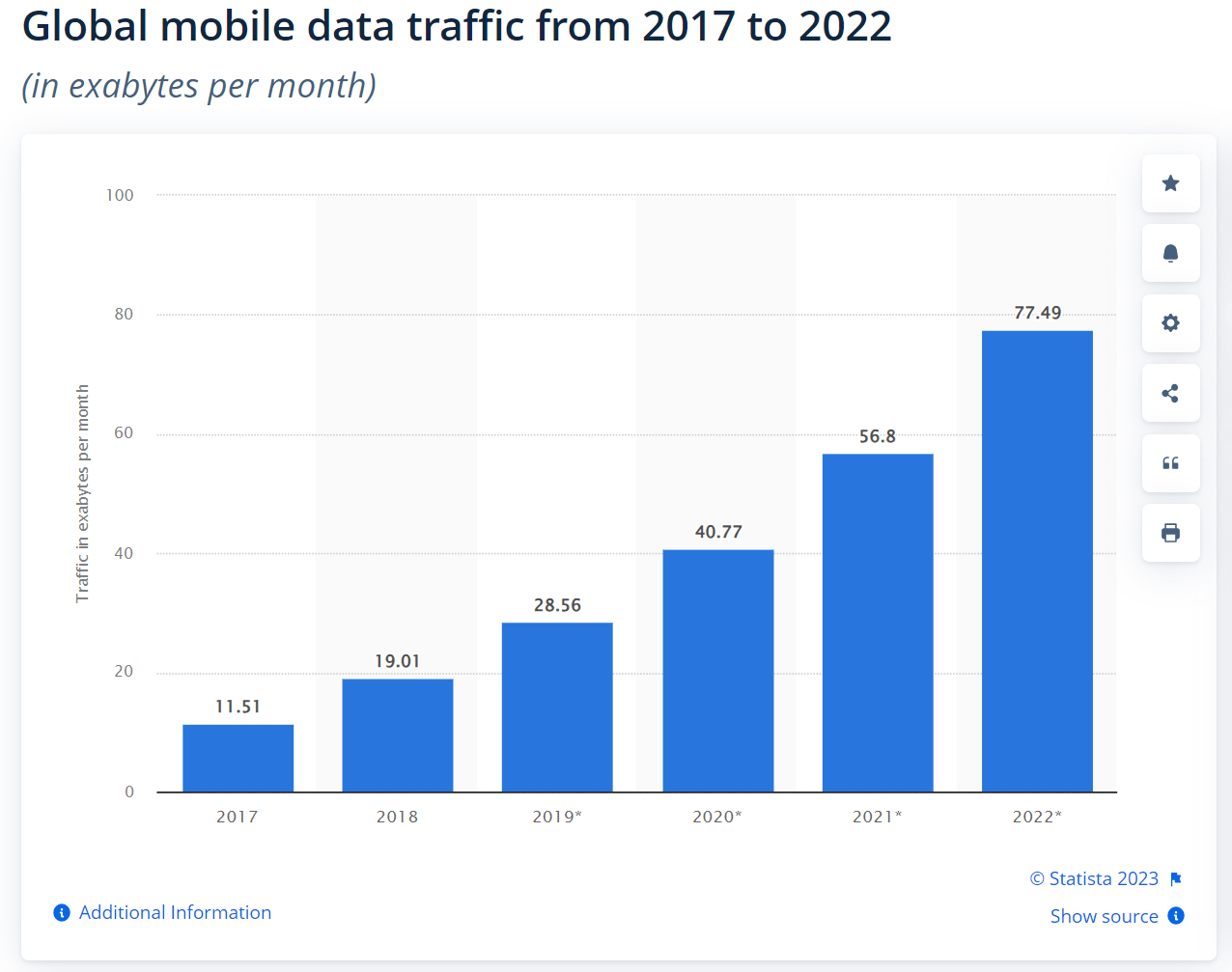

In recent years, I have also pointed to the roll-out of the new telecommunications standard, 5G. 5G will massively increase the exchange of data and, thus, the volume of data.

According to Statista, the global mobile data traffic amounted to 19.01 exabytes per month in 2018. By 2022, however, mobile data traffic was expected to reach 77.5 exabytes per month worldwide at a compound annual growth rate of 46 percent. Given this data, one would think that the mobile tariff providers operating in an oligopoly are in a gold rush, and the shares are rushing from one record high to the next.

Global mobile data traffic (Statista)

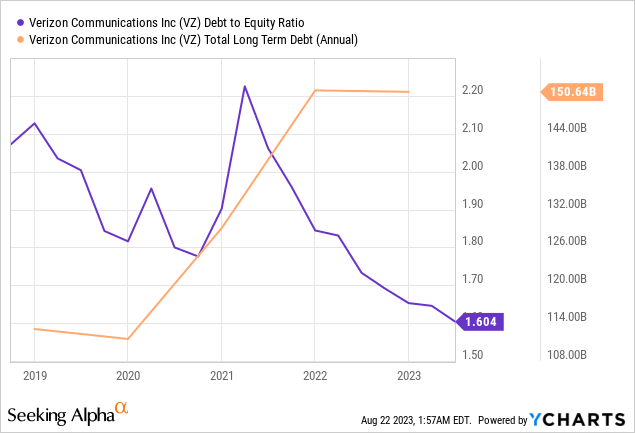

However, this scenario has not materialized. Instead, Verizon is piling up more and more debt without really expecting growth in sales and profits in the next few years.

Interest-bearing debt rose from $113 billion in 2018 to $177 billion now without any significant increase in profits. At least the debt-to-equity ratio has fallen to a multi-year low.

So if 5G is not the growth driver and there are still some unknowns like Amazon’s market entry or possible liability issues around the toxic lead-lined cables hanging like heavy clouds over the stock, then the high dividend yield and low valuation will quickly turn into red flags that investors should take seriously.

{kind=link}

Conclusion

On the downside for all invested shareholders, Verizon stock is down more than 45 percent since its all-time high in December 2019. As illustrated, this is due to a number of factors, including a highly competitive wireless market, stagnant revenue and profits, and rising debt.

Despite these challenges, Verizon has a strong dividend yield of nearly 9 percent. The dividend has grown steadily over the past 18 years and appears safe for now. No question, Verizon stock is therefore becoming attractive to income investors. However, investors should be aware of the risks involved with Verizon. The wireless market in the U.S. is highly competitive and will remain so. The three major providers Verizon, AT&T, and T-Mobile are fighting tooth and nail for market share. This is leading to price pressure, which is putting pressure on the companies’ profits. The need for capital expenditure will increase as a result. Verizon’s sales and profits will therefore continue to stagnate. This will increasingly limit its ability to service debt. Verizon’s debt has risen sharply in recent years.

Investors should therefore not be blinded by the low valuation and the high valuation, but rather invest their money in businesses that are growing.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment