photobyphm

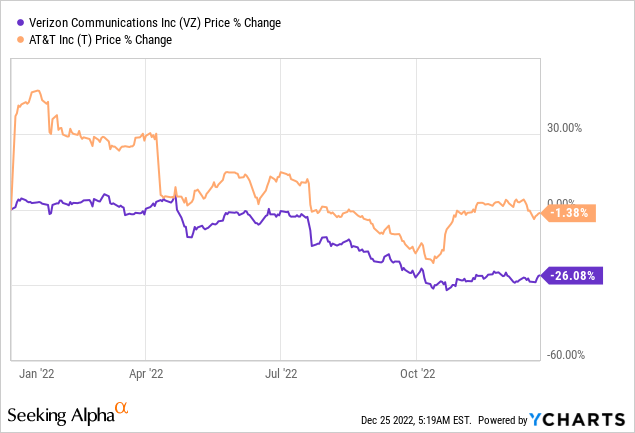

Shares of Verizon (NYSE:VZ) are down 26% year to date and have been widely outperformed by shares of AT&T, in part because Verizon’s rival separated its telecommunications assets from its media/content business. However, I believe the market has turned too bearish on Verizon and there are reasons to be optimistic heading into 2023: the company’s broadband business has solid momentum and the relative under-performance to AT&T could actually be a reason for investors to sell/take profits in AT&T and buy Verizon instead. Verizon has a more compelling valuation and risk profile compared to AT&T whose shares rallied in the fourth-quarter. Although Verizon is the underdog right now, it won’t take all that much for Verizon to see a higher valuation in 2023!

Looking into FY 2023, I believe there are three ways through which Verizon could achieve a higher valuation in the coming twelve months.

Enormous free cash flow prowess will likely continue

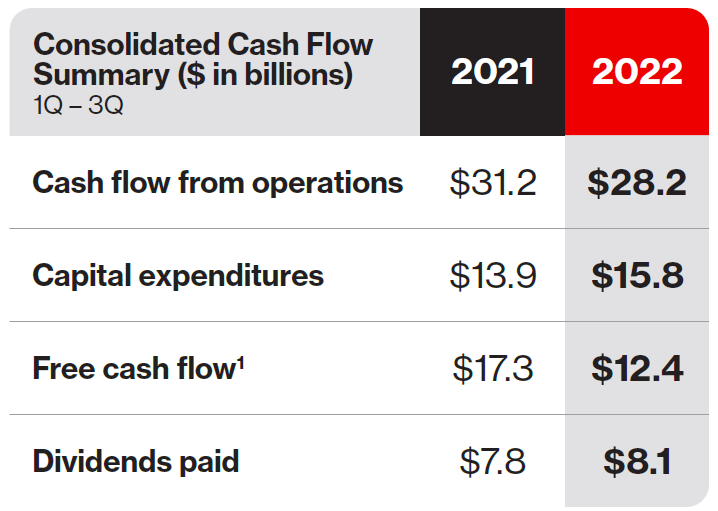

Telecom assets generally are high cash-flowing assets. Companies that offer enterprise and private customers broadband and 5G access are initially faced with high investments, but then look at many years in which they generate predictable free cash flow. Verizon, as an example, generated $12.4B in free cash flow in the first nine months of 2022 and the telecom might achieve $20B in free cash flow for the full-year.

Source: Verizon

Assuming only 5% free cash flow growth for FY 2023, which I believe is realistic, Verizon could generate about $21B in free cash flow next year. Considering that Verizon will pay approximately $11B in dividends in FY 2023, the telecom has an expected free cash flow payout ratio of 52%. Even after paying the dividend, Verizon could have up to $10B left that could be applied toward the firm’s debt. For the current year, I calculate a FCF payout ratio of 54% which is even better than AT&T’s FCF payout ratio of 57%.

Broadband momentum is set to accelerate

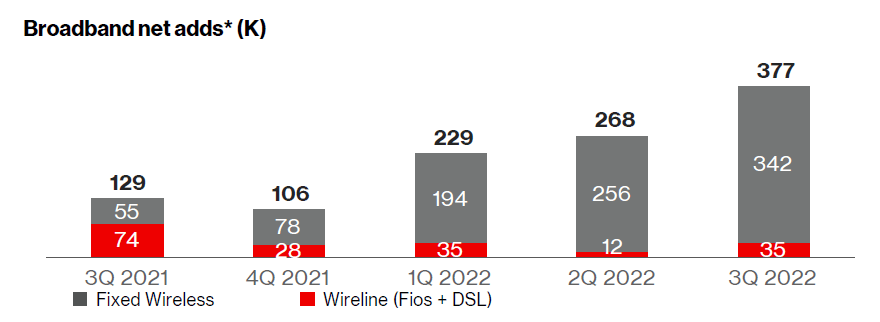

Verizon has an opportunity to grow its subscriber base in the broadband business in FY 2023, which is where the company is already seeing strong customer acquisition rates. Verizon added 377 thousand broadband customers in the third-quarter, on a net basis, which means the company increased its sign-up rate by a factor of 3.0 X compared to the year-earlier period. The Q3’22 net add of 377 thousand subscriber accounts is just slightly lower than the number of broadband accounts Verizon added in the entire previous year — in FY 2021, Verizon added 409 thousand broadband customers.

Source: Verizon

Given the current momentum in broadband net-adds, especially in fixed wireless access, I estimate that Verizon could sign on between 420-430 thousand new customers in Q4’22 and more than 1M in FY 2023.

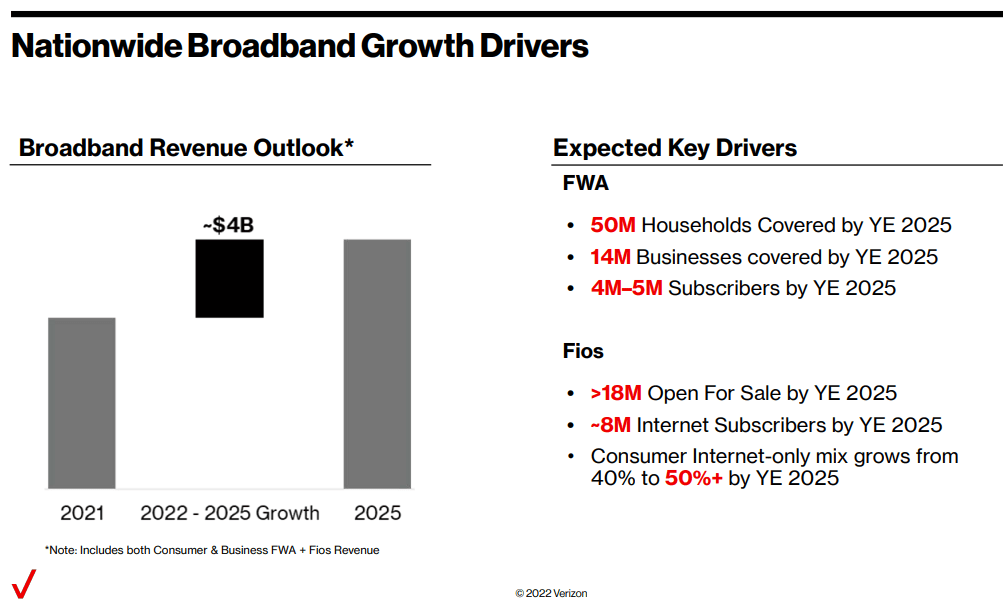

Broadband is obviously a huge growth opportunity for Verizon and the firm expects to capitalize on it by covering 50M households and 14M business with fixed wireless access by FY 2025. In dollar terms, this expansion in the broadband sector is expected to yield $4B in additional revenues between FY 2022 and FY 2025.

Source: Verizon

The dividend will continue to grow

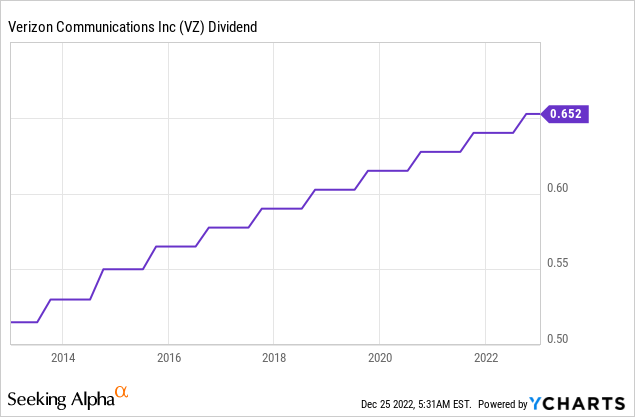

Possibly the biggest signal that the market may is wrong about Verizon is that the telecom continued to raise its dividend in the third-quarter… which is something a struggling company would hardly want to do. The increase in Verizon’s quarterly dividend rate to $0.6525 per-share in Q3’22 — reflecting a raise of 2.0% — sent a strong signal to investors that management remains committed to dividend growth, yet the market ignores Verizon’s very credible dividend growth prospects. For FY 2023, I expect Verizon to raise its dividend pay-out to a new range of $0.6650 to $0.6700 per-share which would show an increase of 2.3% and reflect a potential forward dividend yield of approximately 7%.

Verizon’s valuation

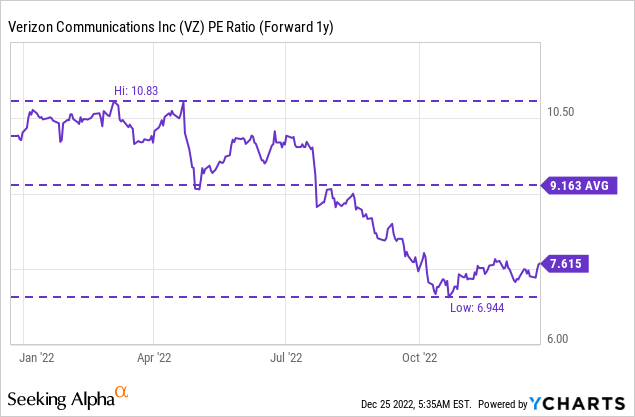

After shares have lost 26% of their value in 2022, Verizon represents truly deep value for investors. The stock is trading at a P/E ratio of 7.6 X, significantly below the 1-year P/E average of 9.2 X. I don’t believe the drop is justified considering that Verizon continues to face strong earnings and FCF prospects in FY 2023.

Risks with Verizon

Verizon operates in a mature and saturated market which limits the firm’s potential for broad top line growth. Another potential impediment to valuation growth could be the firm’s indebtedness. Verizon is highly leveraged and reported $132.9B in long term debt, which is an amount Verizon needs to reduce. If Verizon fails to address its debt situation, investors may continue to hesitate to buy the firm’s shares.

Final thoughts

2022 was obviously not a great year for Verizon. However, I believe it would be a mistake to ignore Verizon considering that the underwhelming performance of 2022 raises the odds of potential outperformance in 2023… if management executes well. Verizon is seeing strong momentum in the broadband business and the telecom is still generating an enormous amount of free cash flow… which are two key points of strength during a recession. Continual dividend growth, debt repayments and broadband momentum could create up-side potential for FY 2023 while the firm’s strong FCF could help stabilize the stock!

Be the first to comment