Delmaine Donson

Verizon Communications Inc. (NYSE:VZ) was a hot topic today at our investing service. The just-reported earnings were mixed, and the outlook was modest. Period. End of article. Perhaps more attention-grabbing for our members was the stock being up 8% and halted this morning. Turns out there was a technical glitch impacting the prints of a dozen or so stocks. The issue was quickly corrected. At the time of this column, Verizon is now down 2%, but we see the stock as a good buy in the mid and high $30s. In this column, we outline our trade, but think the stock is great for long-term income and/or compounding in a tax-favored account.

The play

Target entry 1: $38.50-$38.75 (30% of position)

Target entry 2: $37.65-$37.80 (30% of position)

Target entry 3: $36.00-$36.25 (40% of position)

Target trading exit: $43

Traders can set a stop around 34, but the yield would be tremendous at this level.

We also love a buy write strategy especially if volatility picks up and sends this stock to the third target entry.

Discussion

Verizon Communications Inc. stock is a few points off of a 13-year low. While earnings left something to be desired, as we will discuss, the dividend looks secure, and that is why we bought the stock.

Verizon Q4 results in context

The market has certainly been nervous about this earnings season. There remain concerns over guidance and concerns over the health of the consumer. We believe this recent huge rally in stocks is way overdone and we will be pulling back to (SP500) 3750 in the next two months. We do not believe earnings weakness is priced in yet, but as we saw with Verizon and many other companies, the outlook is not great.

This is the first real week of Q4 earnings reports aside from the banks. Verizon surpassed expectations on the top line and was in line on the line, but the outlook was a very visible miss. Management continues to battle churn, but met operational targets.

We delivered on the operational expectations and financial targets that we set in the second half of 2022

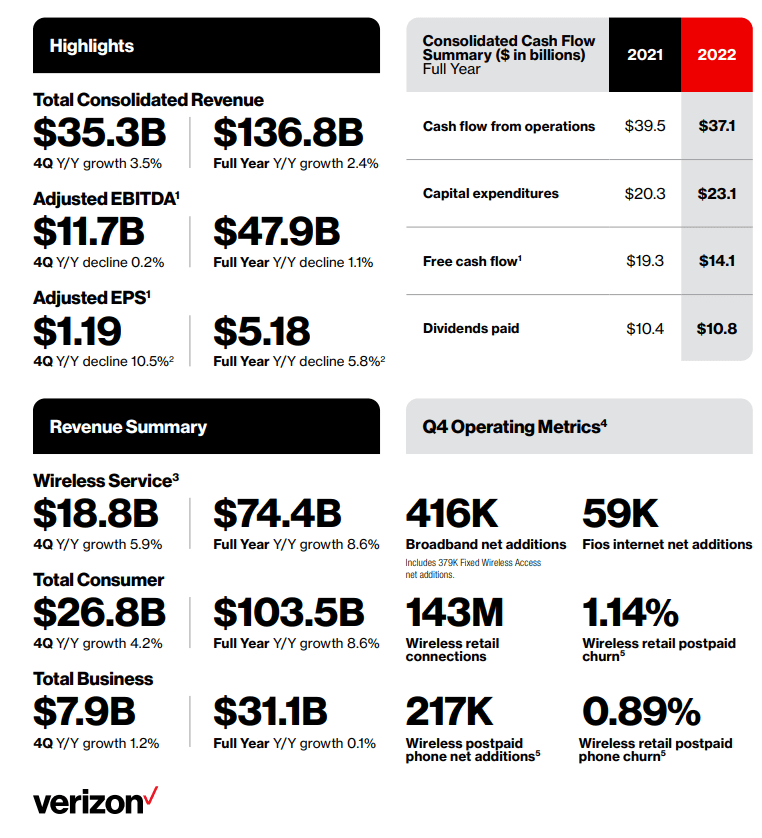

To remain competitive, we thought for the holiday quarter the company would be very promotional given the changes in the economy, and consumer. Last quarter they had taken pricing action to help drive numbers, but we are seeing the impact on margin. Revenue came in at $35.3 billion and was up 2.4% from last year. They beat estimates by $160 million.

Verizon Q4 infographic

The comparisons are largely summarized above. What about the revenue drivers?

Verizon’s Q4 revenue drivers

So revenues beat by $160 million versus estimates. What we wanted to see was new customer additions. Wireless postpaid growth saw 217,000 new net adds. There was retail postpaid churn of 1.14%, rather high, but both adds and churn improved from Q3, which was good news. A lot of the new customer adds were driven by 5G availability and promotions, but revenues held up with pricing increases. Over in broadband, the company saw net adds of 416,000, up from Q3’s 377,000, which was positive. Business also reported 455,000 wireless retail postpaid net adds. So this is not all bad here, folks. Verizon Communications also saw 379,000 Fios net adds in the quarter. This was positive and an increase from the 37,000 net adds in Q3. This was impressive in this environment, though reflected some usual holiday quarter strength too.

Verizon Q5 earnings outperformance

New customer additions were decent here, and revenues were modestly better than expected and grew from last year. As far as earnings go, with a nice top line beat we were expecting a decent EPS result. Analysts were looking for $1.19, and the company matched that benchmark. However, EPS is down from $1.33 last year. Adjusted EBITDA was down 0.2% to $11.7 billion.

The cost reduction efforts that are being implemented seem to be having an impact to a degree, but with revenues up, and EPS down, clearly there remains ongoing need to control spending. Regardless of the cause, EPS declines quarter after quarter will not lead to success. We suspect Verizon Communications management continues to lean out spending. But interest expense is up now due to higher rates, and CAPEX is up to $23.1 billion this year, well above 2021 spending.

But what about the main reason to own Verizon Communications Inc. shares, in the dividend? Well it comes down to free cash flow.

Verizon Q4 free cash flow a disappointment

Cash flow is a concern always for big dividend names. It is a metric that is critical for measuring dividend safety or gauging the potential for a dividend cut. Verizon’s performance has the dividend being more than covered, but the payout ratio is creeping higher.

We mentioned higher expensed, and capex was higher year-to-date, and interest expenses are up. While EBITDA was about flat, these higher expenses weigh, as we saw on the bottom line EPS figure. The net result of cash flow from operations which were $37.1 billion, a big drop from $39.5 billion last year. Free cash flow for 2022 was down 26.9% versus 2021, hitting $14.1 billion. This is down from $19.3 billion last year. That is painful, and means free cash flow was only $1.7 billion in Q4. That is a big miss against expectations. We were looking for $2.5 billion. Why is this an issue? Well, the company pays more each year to the dividend. Dividends paid were $10.8 billion versus $10.4 billion year-to-date last year. Doing the math, we see the payout ratio has jumped from 54% in 2021, up to a still safe, but much less comfortable, 77%. This is something to keep a close watch on moving forward.

And on the topic of negatives, the debt burden is huge. This is a risk in a rising-rate environment, as interest expense will continue to climb. The company is trying to chip away at the debt, but the net debt is still massive at $130.6 billion. This results in a debt to adjusted EBITDA ratio of 2.7X.

Forward view

So the Verizon Communications Inc. results were mixed, fair to say. The outlook was a visible miss, however. Revenues in 2023 will be up very low single-digits. Guidance for 2023 earnings was $4.55 to $4.85. But if you are keeping score, this is a decline from the $5.18 in EPS in 2022. That is a noticeable decline. So, at $39 a share here, that means Verizon Communications Inc. stock is 8.3X FWD EPS at the midpoint. That may seem cheap, but is a wider multiple than in much of 2022 due to the decline in EPS outlook.

Verizon Communications Inc. can get cheaper if earnings fall more. Right now, the outlook suggests a minor crisis is brewing, and we expect more pressure on cash flow. We see the dividend as secure, but there is more risk attached to Verizon Communications Inc. stock now.

Be the first to comment