sfe-co2

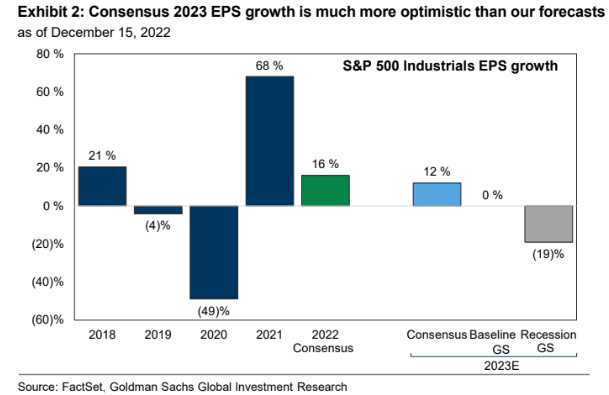

The Industrials sector has outperformed the broad market this year as the value trade continues to hold its own after beginning a bit more than two years ago. Goldman Sachs recently published a note cautious on the cyclical space, though. The bank remarked that Wall Street is much more optimistic than they are regarding 2023 EPS. If consensus is correct, however, Industrials will bolster what could be a tepid year of SPX earnings after a solid 16% earnings advance this year.

Industrials Earnings At Risk In 2023?

Goldman Sachs Investment Research

According to Bank of America Global Research, Veritiv Corporation (NYSE:VRTV) is a business-to-business distributor of print, publishing, packaging, and facility solutions. It has approximately 125 operating distribution centers spread across the US, Canada, and Mexico and was formed in 2014 through the merger of International Paper’s xpedx business and Unisource Worldwide.

The Georgia-based $1.8 billion market cap Trading Companies & Distributors industry company within the Industrials sector trades at a low 6.1 trailing 12-month GAAP price-to-earnings ratio and pays a small 1.9% dividend yield, according to The Wall Street Journal.

The company’s CFO recently announced retirement, but shares did not move much on that news. Shares did rise, however, following Veritiv’s Q3 earnings report that featured a flat year-on-year revenue figure and a 2022 guidance increase. The company appears well-positioned to produce impressive free cash flow despite earnings that are normalizing lower. With total debt that is trending lower and possible shareholder accretive activities, there are some positive aspects investors should take note of. Still, downside risks include a macro slowdown and volatility in commodity prices.

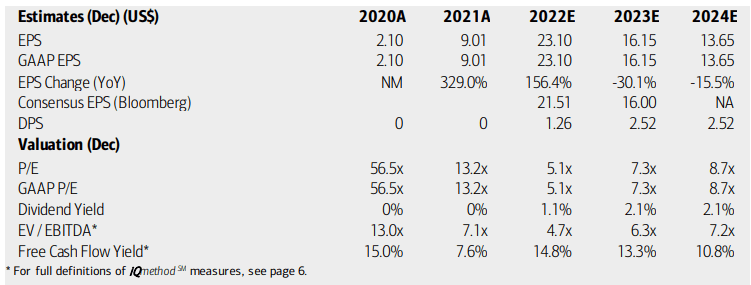

On valuation, analysts at BofA see earnings drifting lower to just under $14 by FY 2024. The Bloomberg consensus forecast is slightly less optimistic than BofA’s outlook for this year and next, however. Dividends are seen as rising in the quarters ahead as the stock’s free cash flow yield is strong in the double digits. With low operating and GAAP P/Es and a below-market EV/EBTIDA ratio, I like the valuation here despite earnings volatility.

Veritiv: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

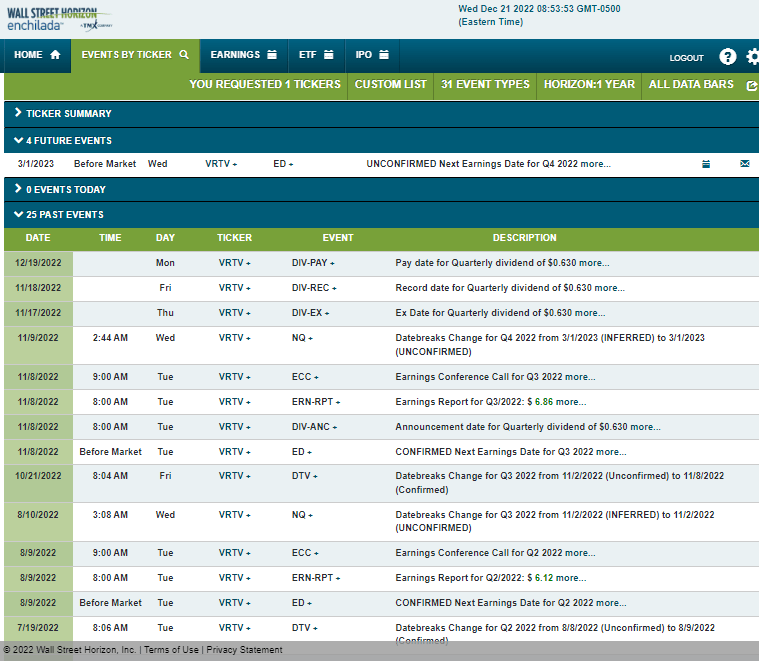

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q4 2022 earnings date of Wednesday, March 1 BMO. The calendar is light aside from that earnings event.

Corporate Event Calendar

Wall Street Horizon

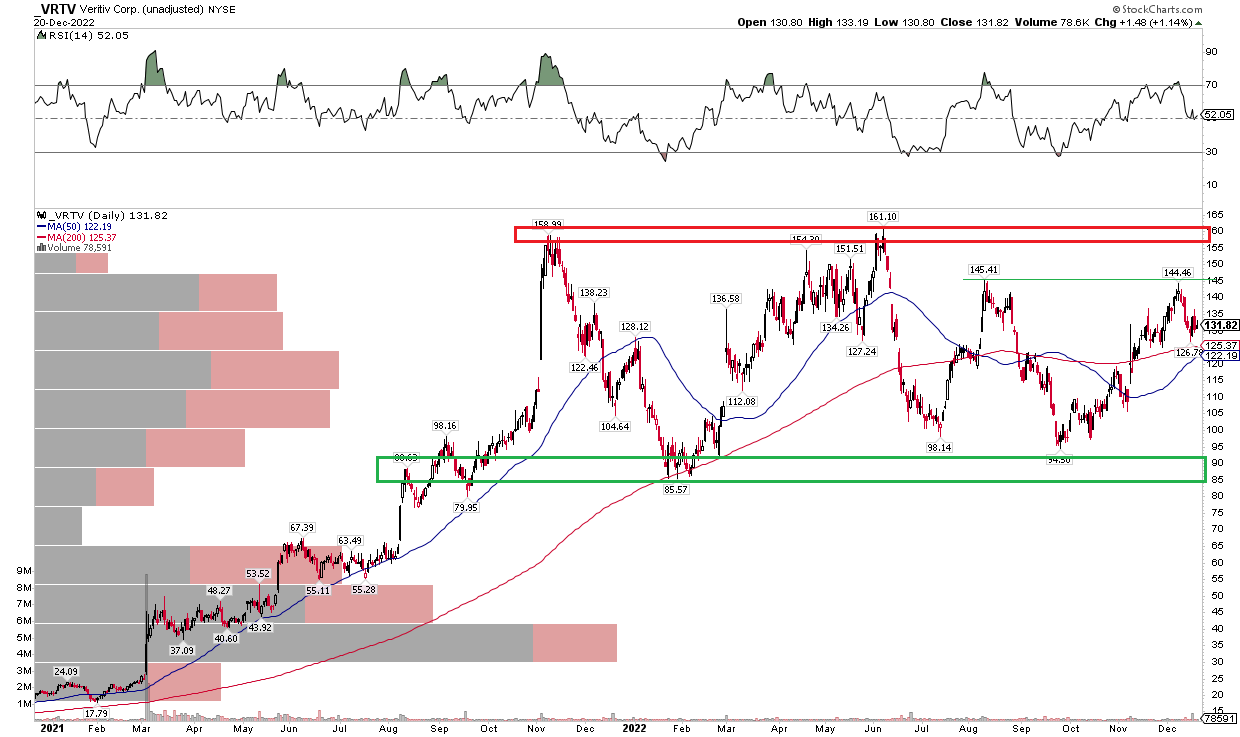

The Technical Take

VRTV sports impressive year-to-date relative strength. Shares are up more than 8% compared to the S&P 500’s 18.6% total return loss through December 20. Relative to the Industrials sector, VRTV also shines, outpacing XLI by more than 14 percentage points on the year. Relative strength sometimes masks absolute weakness, though. Is that the case here? Not so much.

I see VRTV as simply rangebound while so many other stocks are trending lower. The stock has jostled around its 50 and 200-day moving averages throughout 2022. I see key support in the upper $80 to the mid-$90s with more defined resistance near $160. Immediate resistance may be in place at what could be a bearish double-top pattern at $145. If shares breakout above that point, though, a bullish price objective to $195 would trigger.

VRTV: A Stubborn Trading Range Continues

Stockcharts.com

The Bottom Line

With an attractive valuation and solid free cash flow outlook, I am bullish on VRTV. A sideways chart is not too concerning given its relative strength and possible bullish breakout.

Be the first to comment