-slav-/iStock via Getty Images

Thesis

Veritex Holdings (NASDAQ:VBTX) has successfully grown its top line by around 40% this period compared to a year prior, and also grown its bottom line by 20%, leading to an improvement in the net interest margin. Fortunately for us, this has yet to be reflected in the share price as investors have not considered these financial improvements. Comparing the share price to peers, VBTX has around 66% upside from current prices.

Intro

VBTX is a community bank based in Dallas, Texas, providing relationship-driven banking products to SMEs and consumers. The bank was founded in 2010 in Dallas but has expanded to the Dallas-Fort Worth metroplex as well as Houston and intends to expand further throughout Texas.

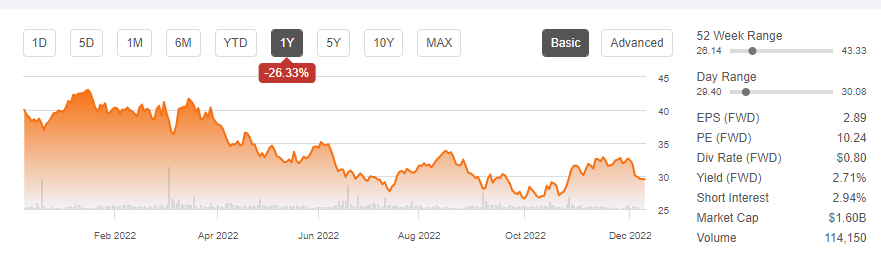

Unfortunately, the bank’s share price has underperformed this year, down around -26% over the past 52 weeks, much steeper than the broader market decline. Stock performance is illustrated below.

Seeking Alpha

Financial Analysis

As it is a community bank, VBTX primarily conducts its business from interest income on loans, service fees, as well as income and sales of securities.

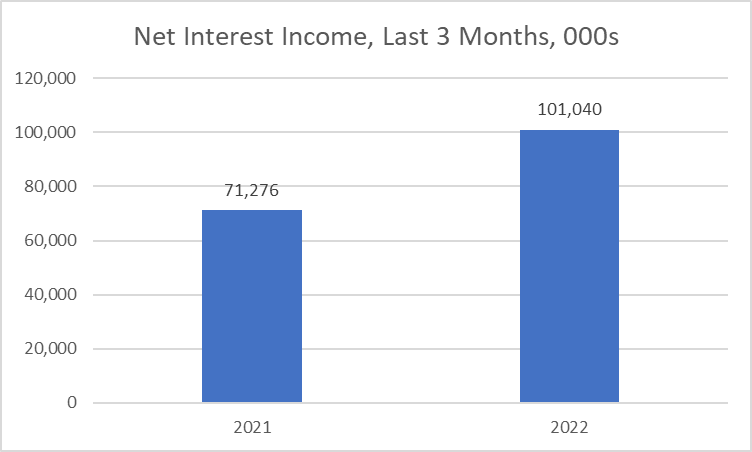

The company have successfully grown their net interest income for the period of the three months that ended September 30, 2022, compared to the same period a year prior. Net interest income reached $101m, achieving a net interest margin of 3.77% and a net interest spread of 3.32%. This is an increase of more than 40% compared to a year prior.

Seeking Alpha

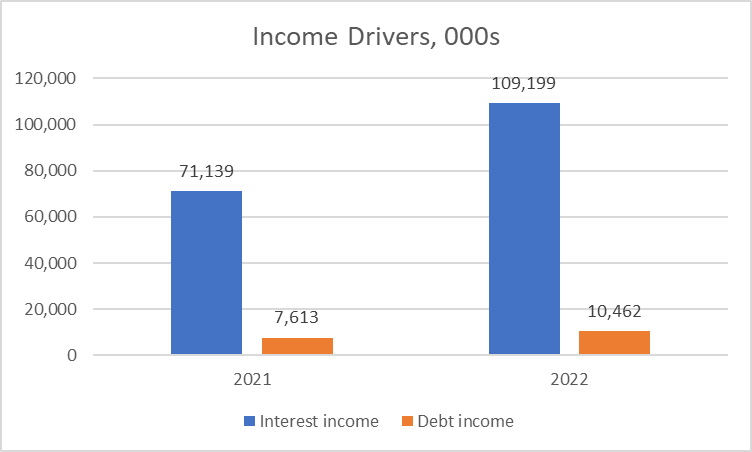

The increase in net interest income was driven by an increase in interest income of 38.1m on loans (a growth rate of over 50% from the year prior) and $2.8m on debt securities (growing 37%).

Seeking Alpha

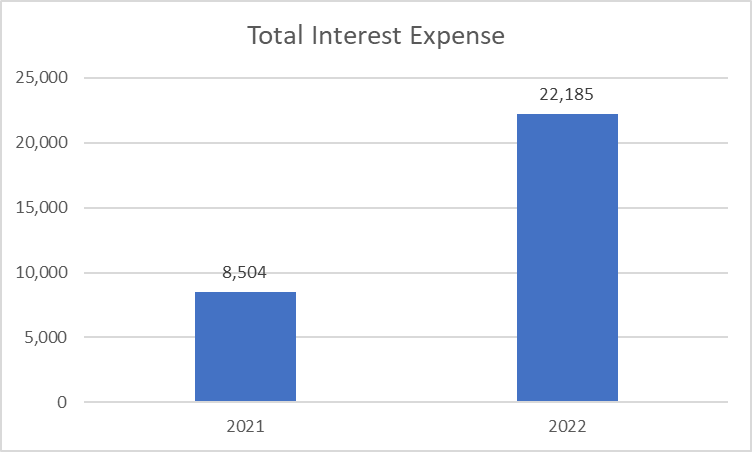

Unfortunately, interest expense grew significantly more than interest income, offsetting all the growth. Total interest expense grew more than 160%, from $8.5m in 2021 to $22m today.

Seeking Alpha

This growth in interest expense was driven by an increase of over $11m in interest-bearing demand and savings deposits (growing by more than 700% compared to the year prior), $2m increase in certificates and other time deposits (growth of more than 100%), as well as an increase in advances from FHLB.

On the other hand, the growth in interest income led to a 51 basis point increase in the net interest margin, from 3.26% in 2021 to 3.77% in 2022, due to an improvement in average balance and loan yields.

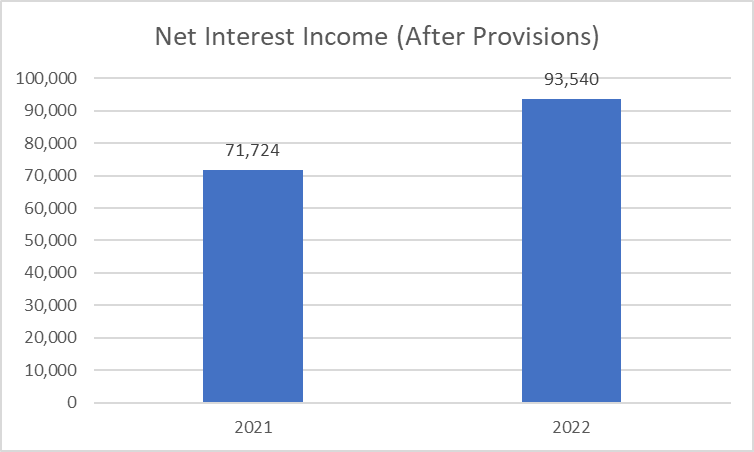

Therefore, this led to an increase in net interest income (after provisions) of 30%, reaching just over $83m for the period.

Seeking Alpha

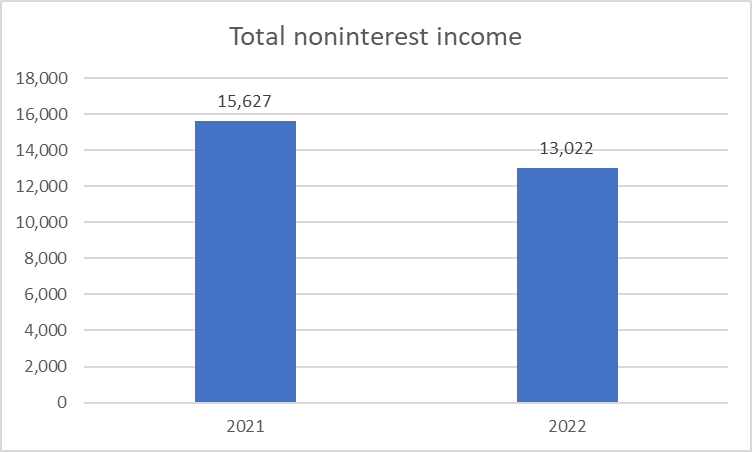

In terms of non-interest income, this primarily consists of service charges and customer swap income, but total non-interest income for the period decreased by $2.6m, or 17%, to $13m (compared to around $16m in 2021 for the same period). The core drivers for this decrease were a large decrease in equity method investment income, as well as a decrease in government-guaranteed loan income. Investment income fell by almost $6m alone. This was fortunately offset by increases in other areas, such as loan fees that increased by around $1m (60%), as well as customer swap income, which increase by over $2m (>200% increase, due to an increase in trade executions).

Seeking Alpha

Non-interest expense, on the other hand, increased. Non-interest expense increased by almost $10m, a 23% increase to $51m, which was primarily driven by a very large increase (almost 30%) in staff costs, which alone now counts for around $30m in costs.

Seeking Alpha

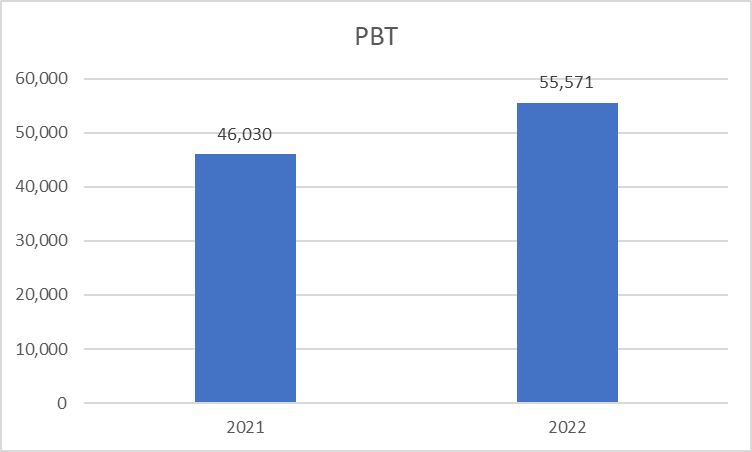

Therefore, taking into account all movements discussed above, income outgrew the increase in expenses, where profit before tax increased by around 20% to reach $55m, leading to an increase in Diluted EPS for the period to increase from $0.73 to $0.79

Seeking Alpha

Valuation

If we collate a list of peers, being regional banks, who have similar market caps, we can potentially see if VBTX is overvalued, undervalued, or even fair-valued.

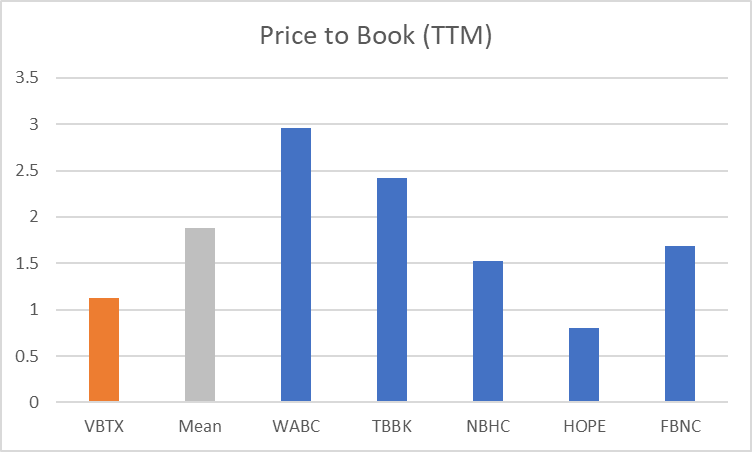

If we look at a P/B valuation compared to peers, VBTX look to be undervalued. VBTX is currently valued at around 1.13x P/B, whereas peers on average are valued at around 1.88x, implying that VBTX stock has around 66% upside from current pricing

Seeking Alpha

Risks

- One risk to this thesis is if salary costs continue increasing. Staff costs were the biggest contributor to growth in operating expenses for VBXT this period, growing by around 30%. This is clearly the impact of the high inflation environment right now. On the other hand, net interest income also grew by around 30%, which offset this increase in staff costs. If net interest income were to continue growing by around 30%, this would cover the increase in staff costs (but then again, other operating expenses may also increase as well, which would lead to lower earnings)

- A second risk is if interest expense continues growing at its current pace of over 100% year-on-year, primarily driven by transaction and savings deposits. If this were to continue, it would knock off some interest margins and lead to lower net interest income and potentially lower the value of the company and share price.

Conclusion

Overall, VBTX has grown both their top line and bottom line. Net interest income grew by around 40%, leading to an increase in earnings before tax by around 20% for the period compared to the same period a year prior. This has led to an increase in Diluted EPS for the period to increase from $0.73 to $0.79 as well as an improvement in net interest margin to 3.77% and net interest spread to 3.32%. However, these improvements have not been taken into account by investors, and therefore have not been reflected in the company’s share price, which is down by more than 25% over the past year. This has led to the company’s share price currently being undervalued compared to peers, with potential upside of around 66% from current prices.

Be the first to comment