Nastasic

Vericel

Only buy something that you’d be perfectly happy to hold if the market shut down for 10 years. – Warren Buffett

Author’s Note: This is an abbreviated version of an article originally published in advance inside Integrated BioSci Investing for our members.

In biotech investing, you should not be discouraged when seeing your stock decline while the fundamentals are boosted. That is to say, there will be periodic mismatches between the stock’s intrinsic value and its true worth. In that situation, it is best to accumulate more shares rather than sell out. You should focus on the long-term fundamentals because they determine where your stock trade be in the future.

On that note, Vericel Corp. (NASDAQ:VCEL) has been enjoying significant sales growth for its Sports Medicines and Burn franchises. Nonetheless, the market sentiment for this stock is clearly lagging behind due to the previous complete response letter (i.e., non-approval) of NexoBrid. In this research, I’ll feature a fundamental analysis of Vericel while focusing on the latest catalytic developments.

StockCharts

Figure 1: Vericel chart

About The Company

As usual, I’ll deliver a brief overview of the company for new investors. If you are already familiar with the firm, I recommend that you skip to the next section. I noted in the prior research,

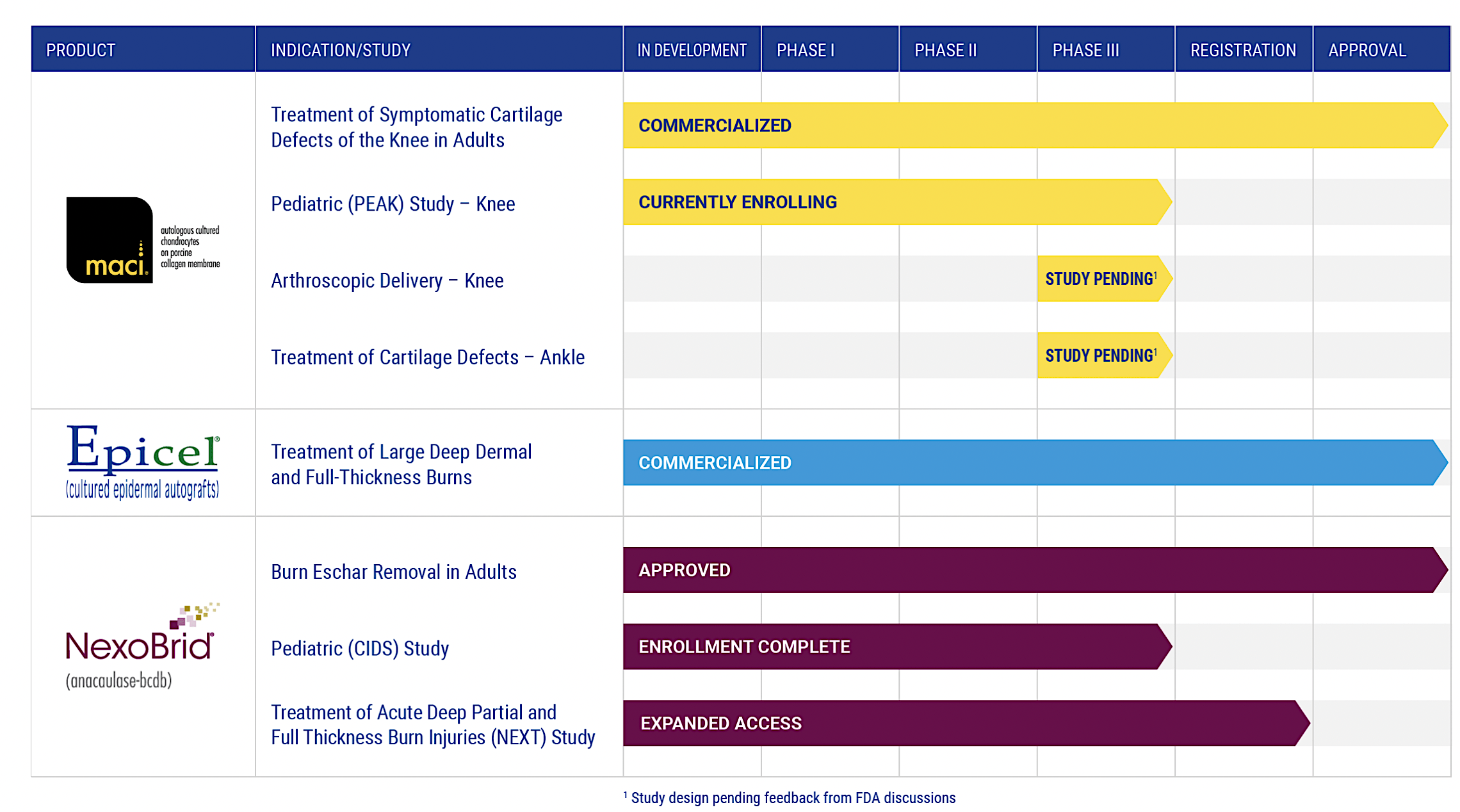

Headquartered in Cambridge, Massachusetts, Vericel is a leader in advanced cellular therapies for regenerative medicine and severe burns. As shown below, the company is brewing a pipeline of autologous cellular therapies – via either the infusion, injection, or transplantation – of the patient’s manufactured whole cells (for damaged tissues and organ regeneration).

Vericel

Figure 2: Therapeutic pipeline

Latest Operating Results

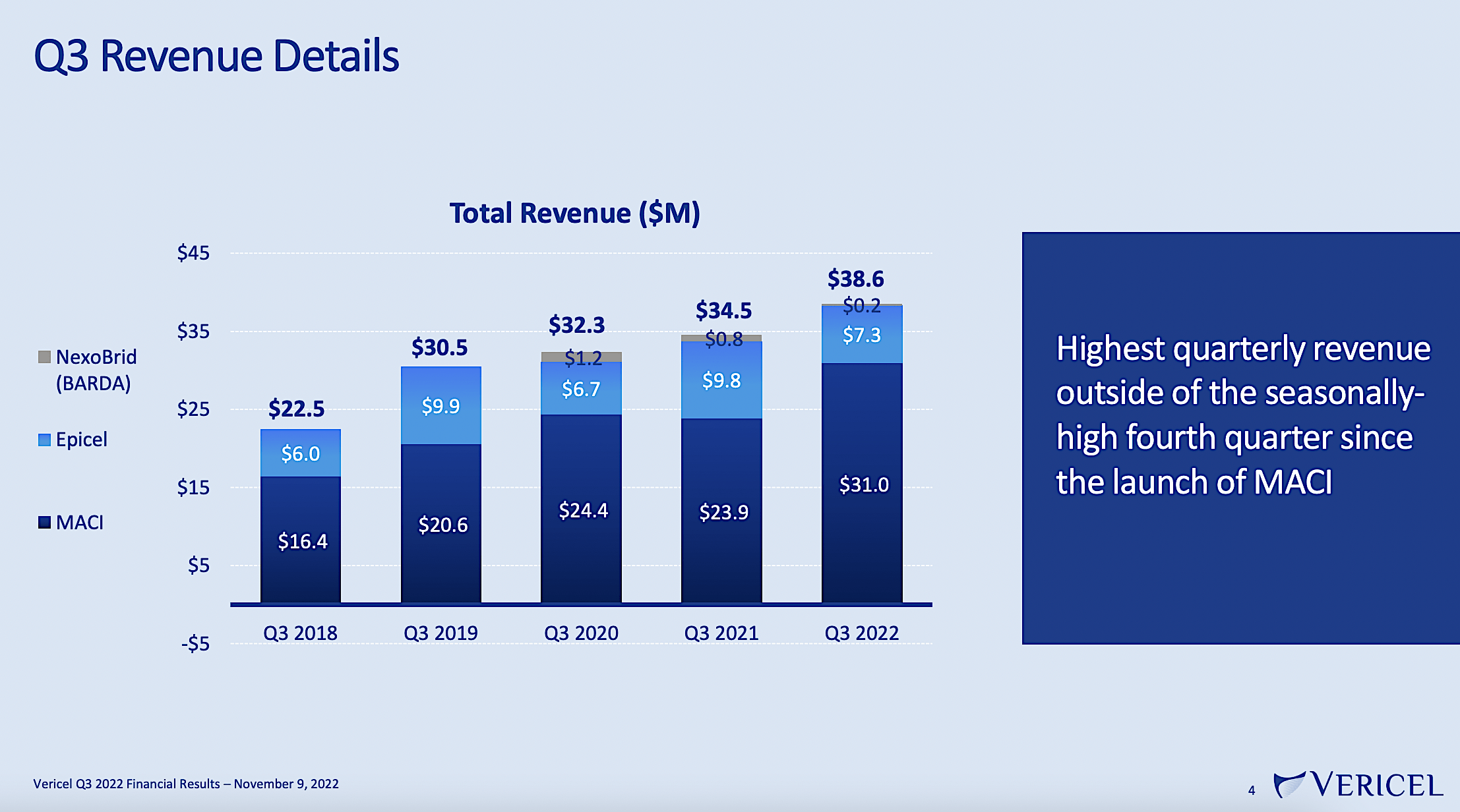

Shifting gears, let us dive into the latest operating results of Vericel. For the latest quarter, the company procured $38.6M in total revenue, which represents a 12% increase from the $34.5M for the same period a year prior. The quarterly Maci sales growth tallied at $31.0M versus $23.8M for the same comparison. As such, this entails a 30% year-over-year (YOY) growth rate for the lead franchise. Whenever the crown jewel therapeutic is enjoying leaping sales increase, that’s a great sign that the growth thesis is working out for you.

Despite the declined (i.e., fluctuating) revenue for Epicel, Vericel finished the quarter with a very strong operating cash flow. Precisely speaking, this is the 9th straight quarter of positive adjusted EBITDA. Simply put, the operating results signaled a healthy business with much upside.

Figure 3: Robust operating results

Sports Medicine Business

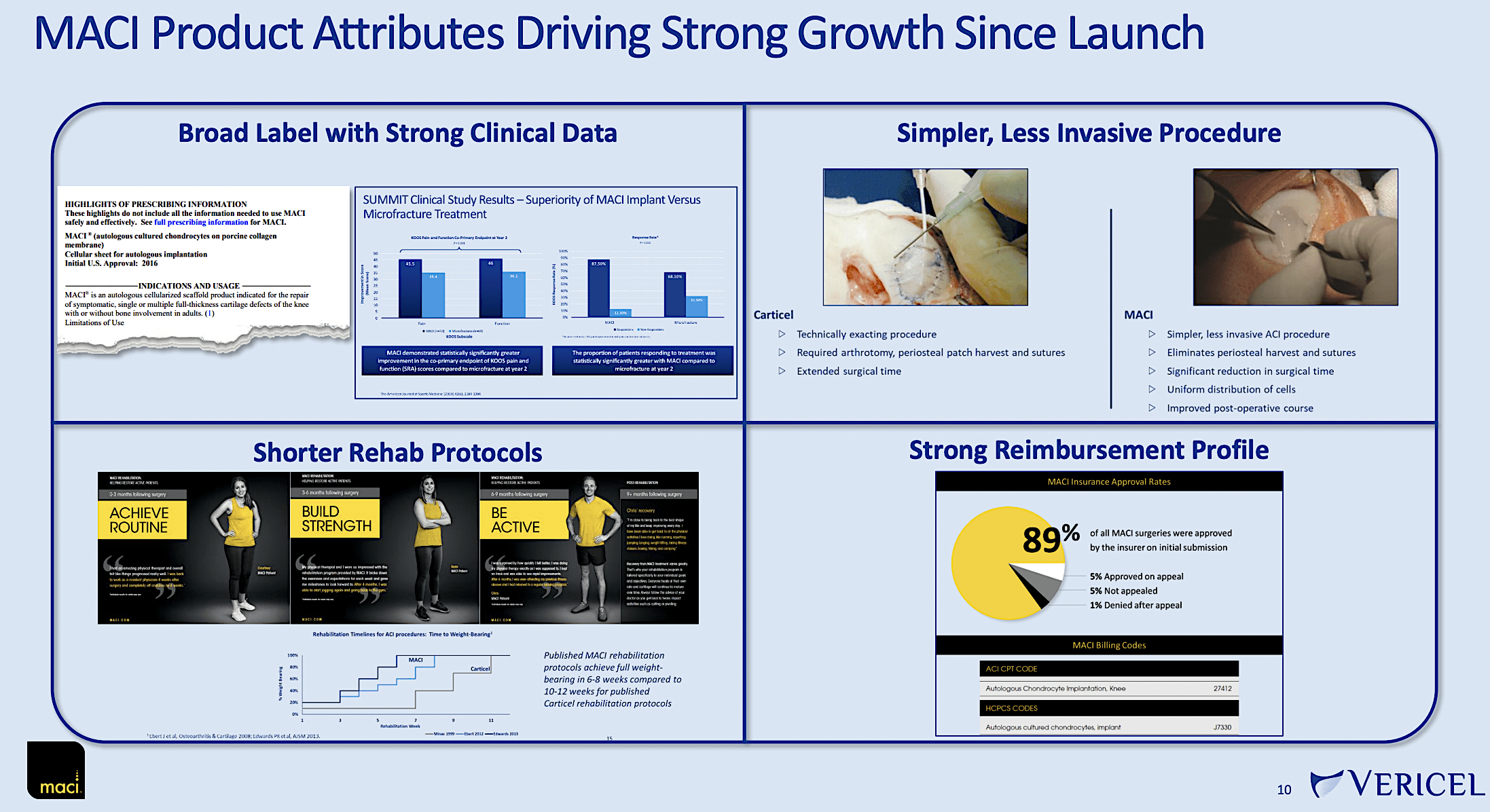

Now, Maci is quite interesting because it’s personalized medicine. That is to say, the docs harvested cells from the patient’s own knees. Doc then amplifies the cells and grows them on a matrix for reintroduction back to the patient. Simply put, it’s an ingenious way to repair articular damage.

Figure 4: Strong Maci dynamics

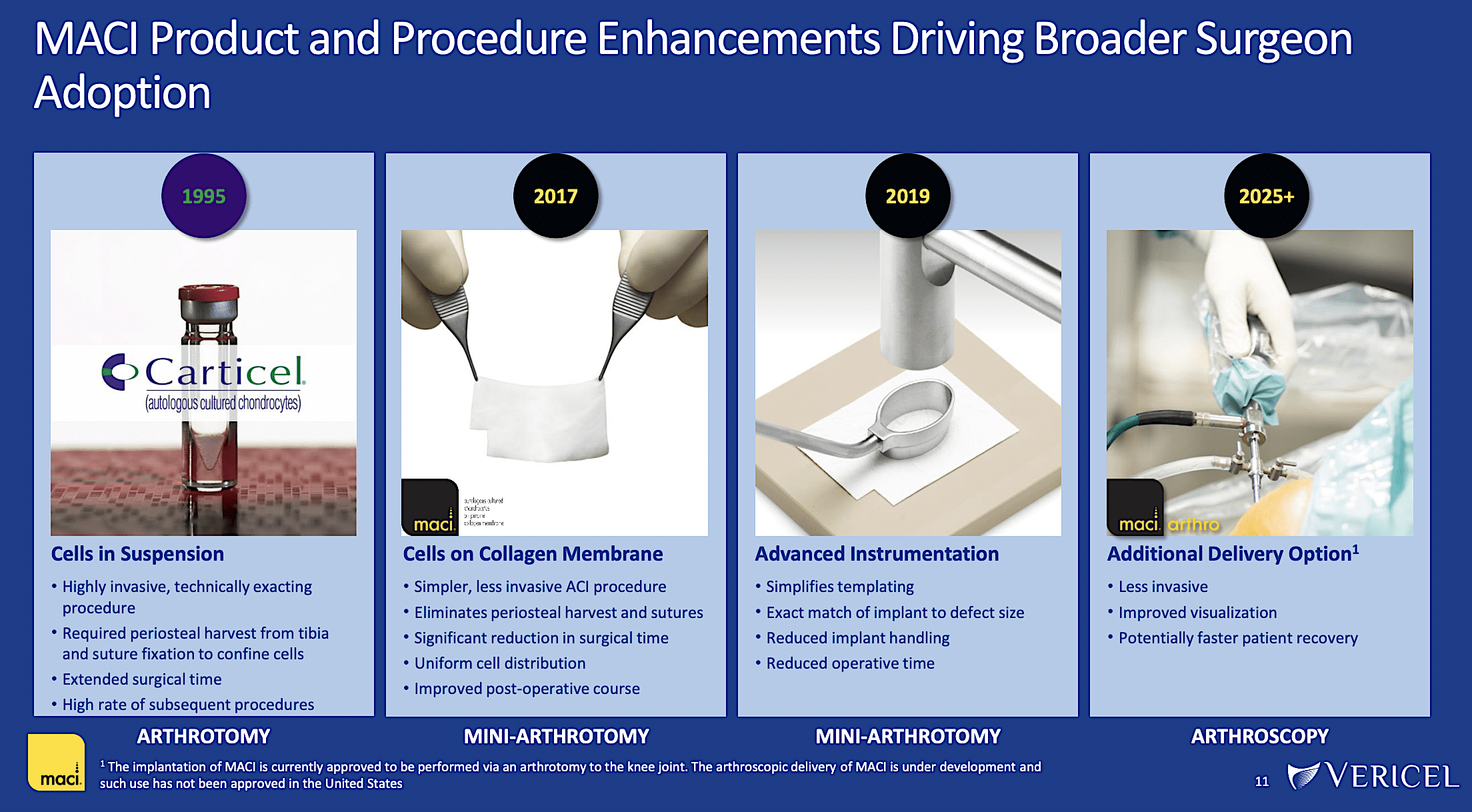

As you know, Maci delivers excellent sales growth for Vericel. And, you can be assured that its advantage (i.e., edge) would boost sales growth in the coming years. First, knee injury is quite common in sports. You can bet that trend isn’t going away anytime soon. So long as there are contact sports, there would be knee injury. Second, Maci has such a broad label that is backed by strong data to warrant a prescription. Third, the procedure is becoming much simpler and less invasive.

Figure 5: Products and procedure enhancement drives Maci growth

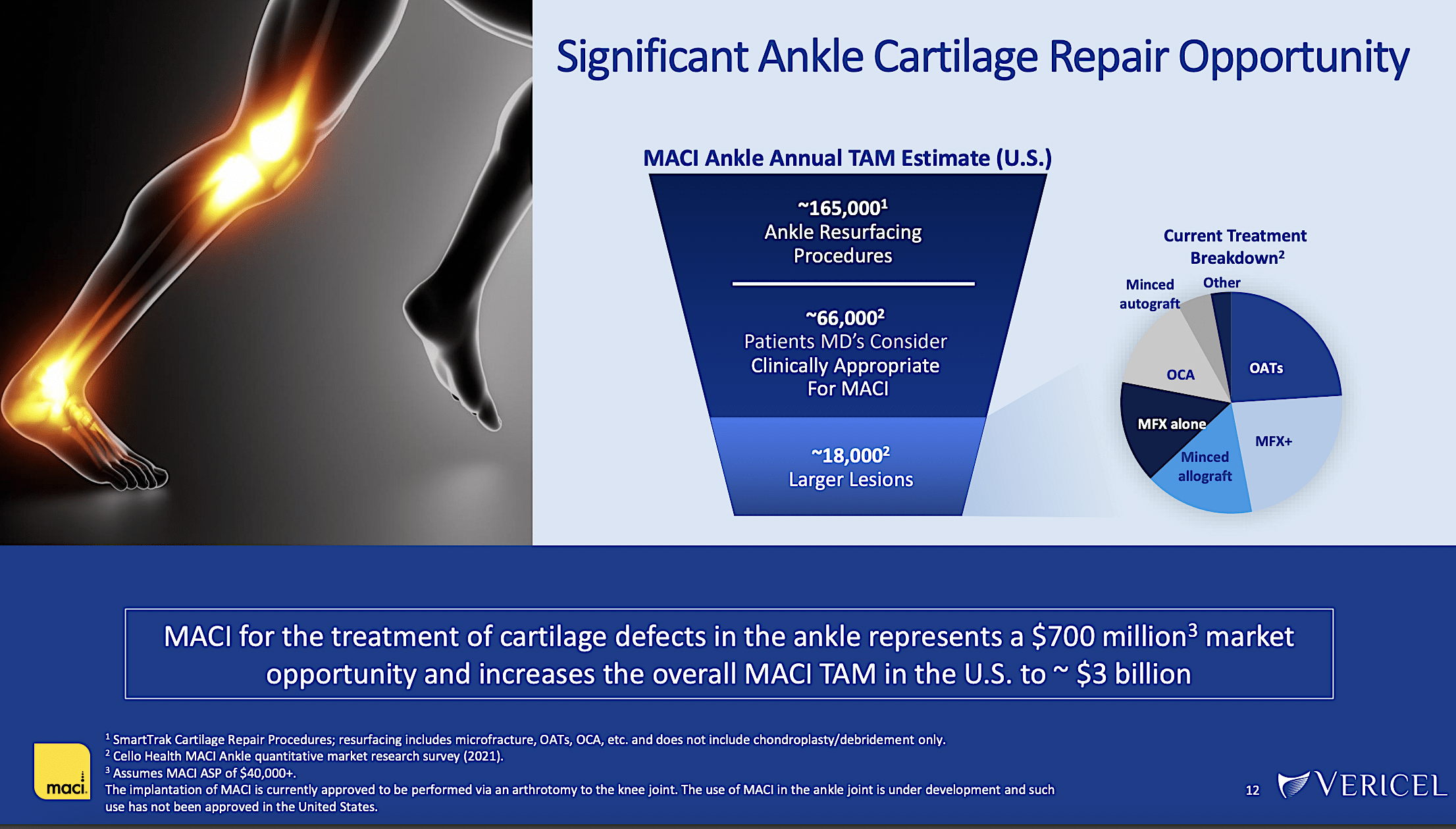

As you can imagine, ankle injury is also quite common in sporting events. In executing the prudent strategy, Vericel is expanding Maci’s label for an ankle injury. In the coming year, if positive data results roll in (and approval is followed by launch), sales growth for Maci should be galvanized by leaps and bounds. And, you can project that this expansion would deliver the most aggressive growth.

Figure 6: Maci’s label expansion for ankle injuries

Burn Franchise

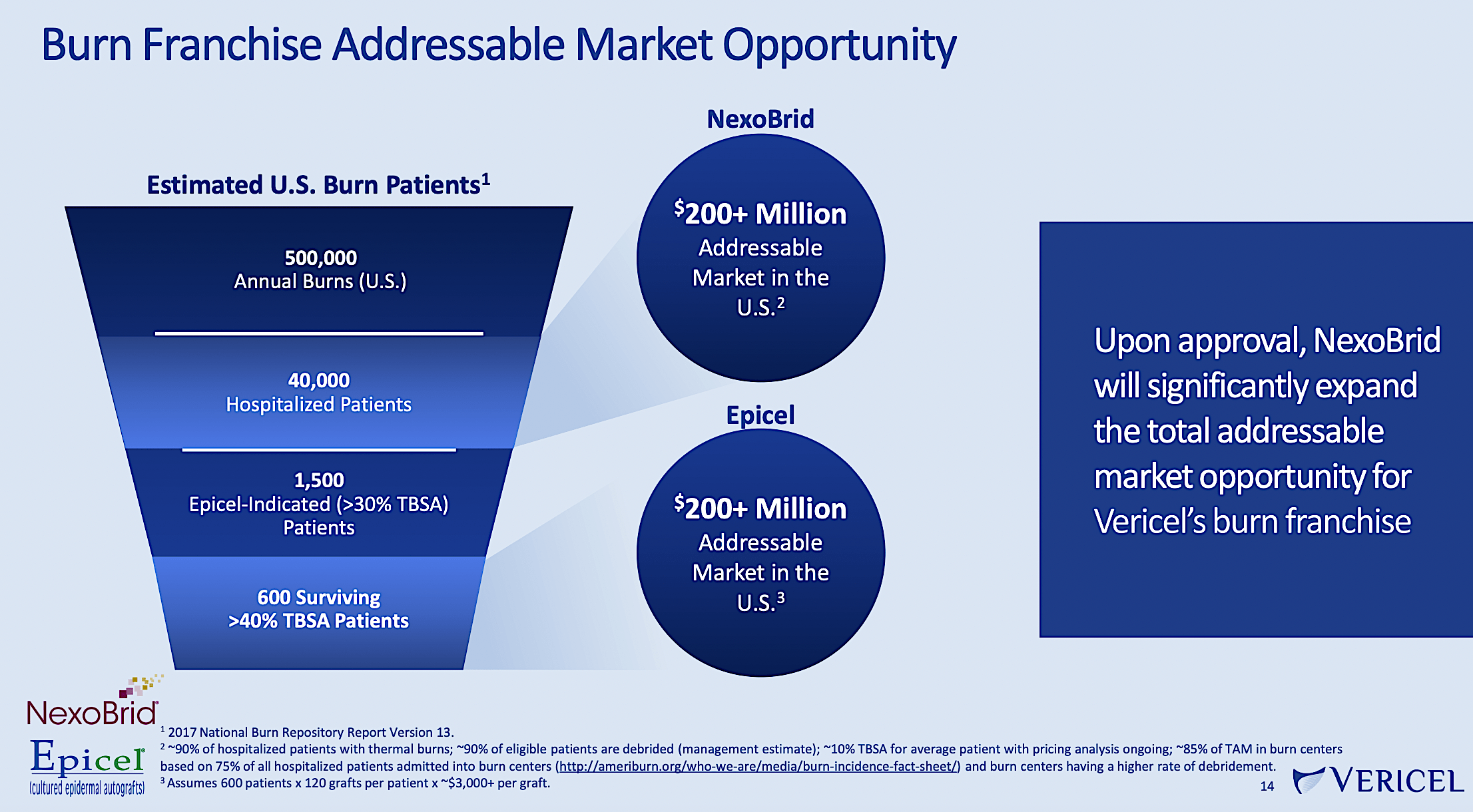

Aside from sports medicine, Vericel is ramping up its burn franchise. As you know, Epicel (a permanent skin replacement for burns) is generating fluctuating sales quarter after quarter. Therefore, you should not set high expectations for this business segment.

Figure 7: Burn franchise with Epicel and Nexobrid

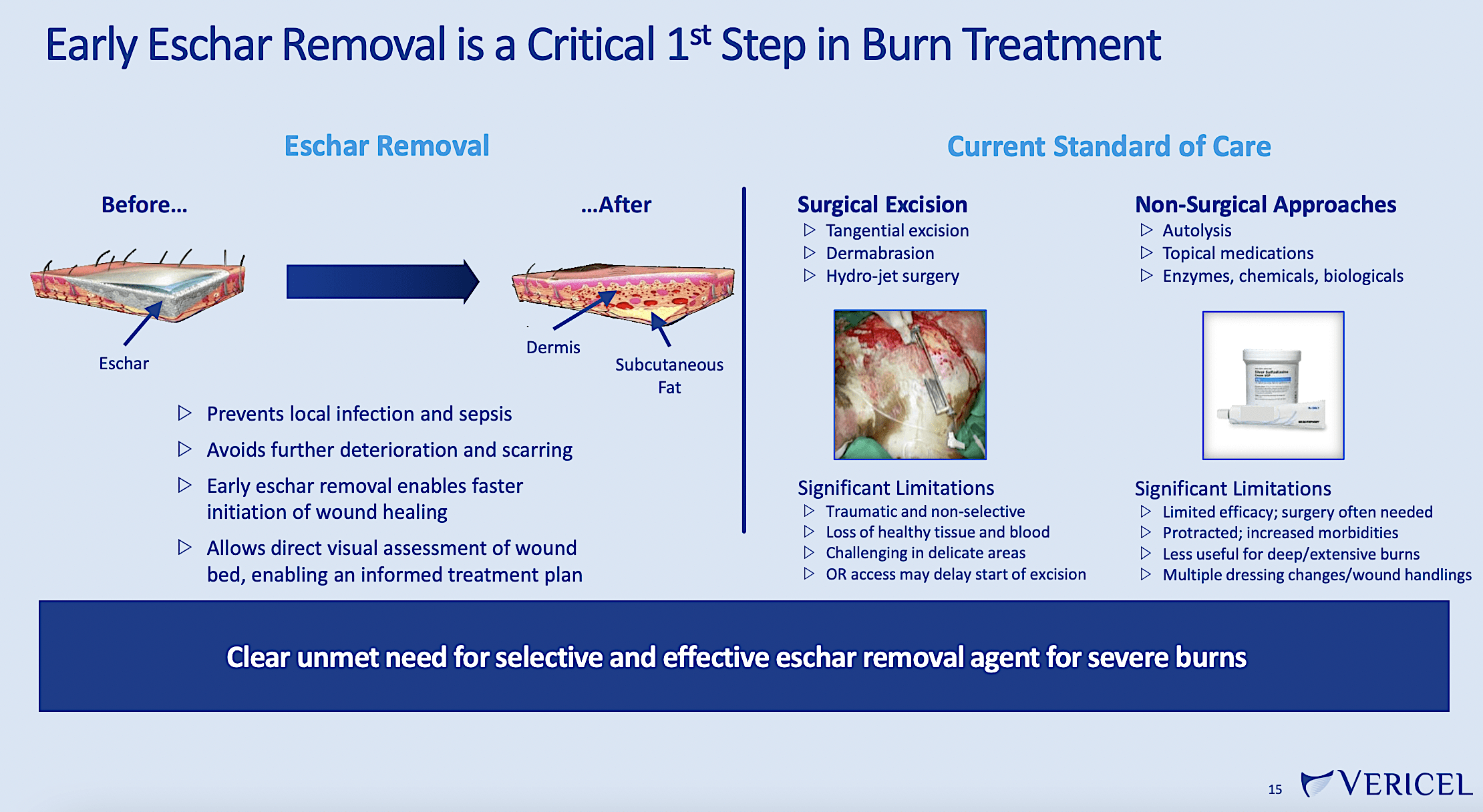

Regardless of its small contribution, Vericel is fostering the burn franchise growth, particularly with NexoBrid. As you can appreciate, NexoBrid is special because it serves as the most critical step in burn management. That is to say, it removes the eschar in the burn which is crucial for healing.

Figure 8: NexoBrid for burns

NexoBrid Approval Catalyst

On December 29, Vericel announced that the FDA approved NexoBrid for the removal of eschar in adults with deep partial-thickness and/or full-thickness burns. Of note, NexoBrid can be applied in two applications for 4 hours each. The first round can take up to 15% of the body. The second application should be applied a day later for 20% of the body’s surface area. Highly enthused, the Principal Investigator of the trial (Dr. Jeremy Goverman) remarked,

When treating partial- and full-thickness burns, a critical first step is the rapid removal of eschar and I believe the approval of NexoBrid provides us with an important non-surgical option to quickly and effectively treat severe thermal burns. As a principal investigator in Phase 3 DETECT clinical trial, I look forward to further incorporating NexoBrid into my practice, as I believe it will lead to improved outcomes for my patients.

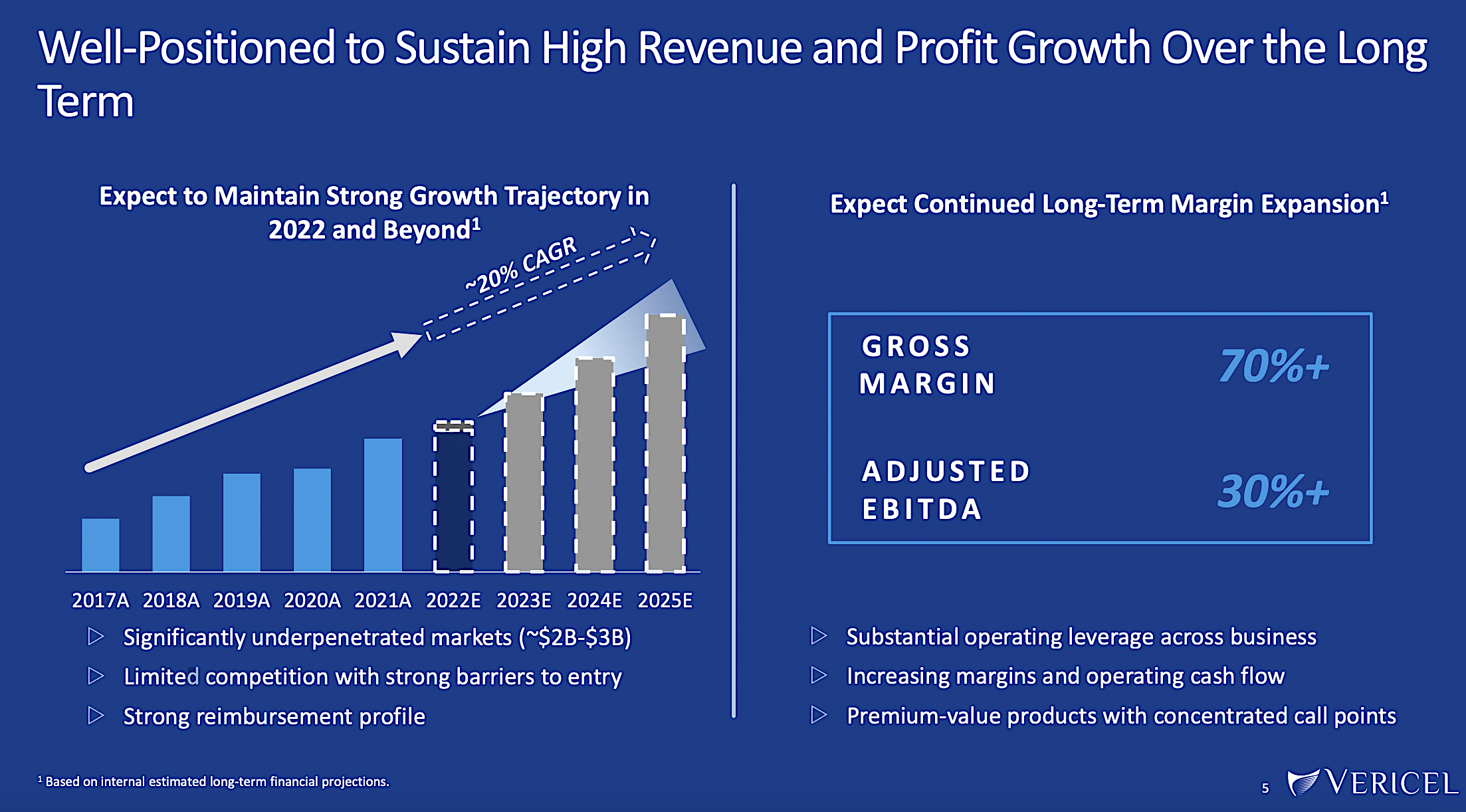

As you can see, this is a major development for patients afflicted by burn wounds. After all, eschar removal delivered improved recovery. Looking ahead, you can expect Vericel to launch NexoBrid in Q2 next year (i.e., just a few months from now). Though it’s not the main franchise, you can expect NexoBrid to deliver an up-gap in revenue. As such, it should contribute significantly to that lofty 20% projected CAGR. According to the President and CEO (Nick Colangelo),

There is a considerable unmet need for non-surgical eschar removal for patients with severe thermal burns, and the FDA’s approval of NexoBrid marks an important advancement in the treatment paradigm for these patients. The addition of NexoBrid to our commercial portfolio significantly expands our target addressable market, and we look forward to executing on our NexoBrid commercial launch plans and establishing NexoBrid as the new standard of care for eschar removal.

Figure 9: Sustained high revenue and growth

Financial Assessment

Just as you would get an annual physical for your well-being, it’s important to check the financial health of your stock. For instance, your health is affected by “blood flow” as your stock’s viability is dependent on the “cash flow.” With that in mind, I’ll analyze the 3Q 2022 earnings report for the period that concluded on September 30.

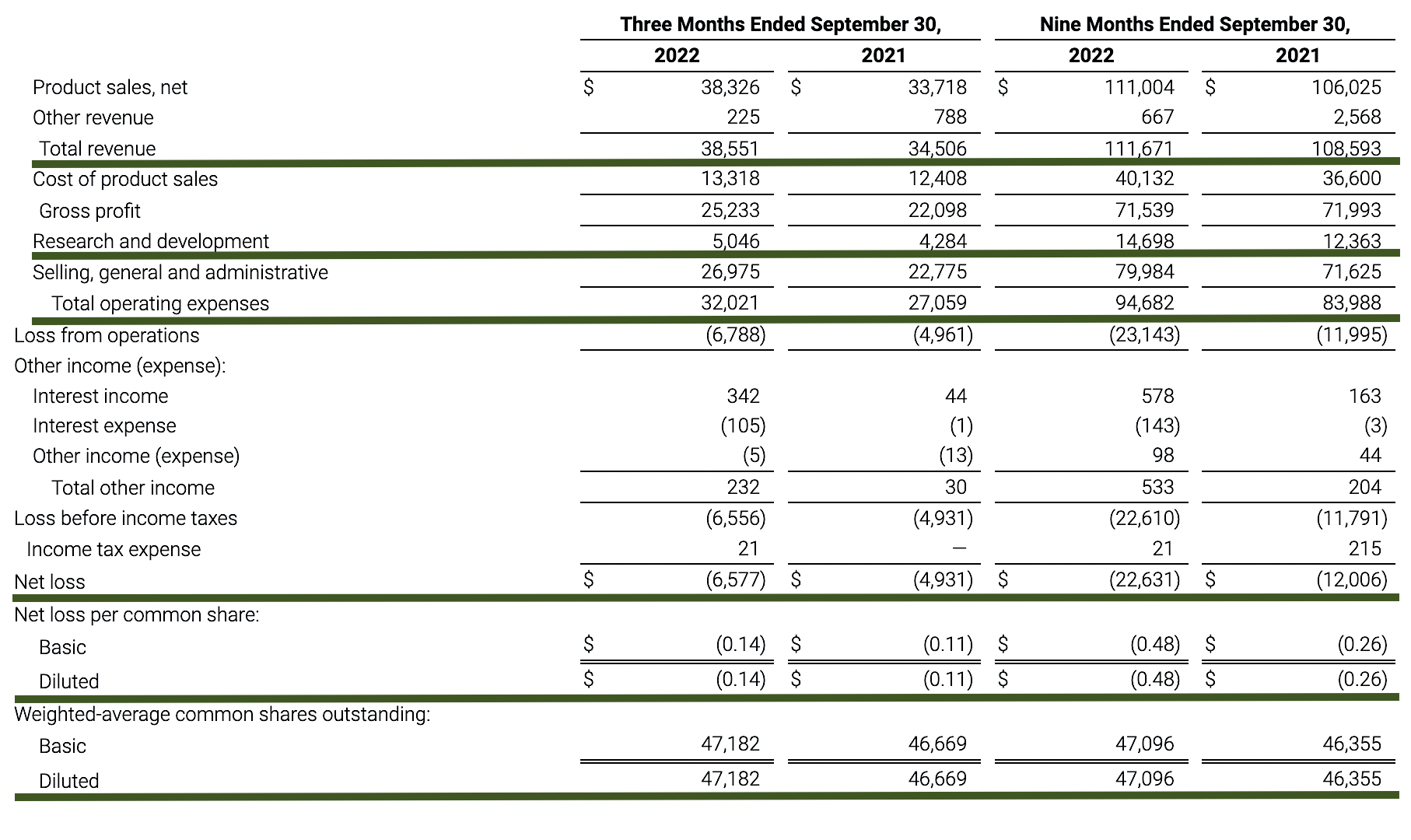

As follows, Vericel procured $38.5M compared to $34.5M for the same period a year prior. The revenue is powered by Maci growth which represents a 30% YOY growth. That aside, the research and development (i.e., R&D) for the respective periods registered at $5.0M and $4.2M. I viewed the 19.0% R&D increase positively. The money invested today can turn into blockbuster profits tomorrow. After all, you have to plant a tree to enjoy its fruits.

Additionally, there were $6.7M ($0.14 per share) net losses compared to $4.9M ($0.11 per share) declines for the same comparison. On a per-share basis, the bottom line depreciation is widened a bit. That made sense due to the increased R&D spending.

Figure 10: Key financial metrics

About the balance sheet, there is $133M in cash, equivalents, and investments. On top of the $38.2M sales (and against the $32.0M quarterly OpEx), there should be adequate capital to fund operations in the coming years without concerns for cash flows. Simply put, the cash position is robust relative to its burn rate and cash flow.

While on the balance sheet, you should check to see if Vericel is a “serial diluter.” After all, a company that is serially diluted will render your investment worthless. Given that the shares outstanding increased from 46.6M to 47.1M, my math reveals a 1.0% annual dilution. At this rate, Vericel easily cleared my dilution cut-off for a profitable investment.

Potential Risks

Since investment research is an imperfect science, there are always risks associated with your stock regardless of its fundamental strength. At this point in its growth cycle, the main concern for Vericel is whether Vericel can continue to ramp up sales for Maci. After all, it is the most important asset. Now, leaping sales growth is highly dependent on additional Maci labels. However, there is the chance that Maci would not be able to gain additional approval (i.e., for ankle repairs). Additionally, the burn franchise might not generate significant sales traction.

Conclusion

All in all, I maintain my strong buy recommendation on Vericel. Not deterred by previous setbacks of Nexobrid, the company finally enjoyed the fruits of FDA approval. Vericel now has two strong franchises to power growth in the coming years. Of those franchises, you can anticipate the most robust expansion to come from Sports Medicine with Maci. Even without the label expansion for ankle injury repairs, Maci is generating stellar sales growth at the 30% YOY clip. As the burn franchises pick up, I believe that Vericel would grow much bigger in the coming years. Next year, you can expect the stock to trade much higher than the current valuation. After all, the share price will catch up to the stock’s true worth in the longer horizon.

Be the first to comment