Alan_Lagadu

Aircraft play a massive part in the modern world. They are used for the transportation of people for various purposes, including recreation, business, relocation, and more. They are also used for the transportation of goods to places that otherwise may not have access to said items. Add on top of this the fact that aircraft are incredibly large and complex pieces of equipment that require countless parts in order to operate, and it should come as no surprise that there would be a large number of companies dedicated to providing goods and services to make the industry function. One such player is a company called HEICO (NYSE:HEI). Although it’s far from the largest company in the aerospace market, it does claim to be the world’s largest producer of FAA-approved jet engine and aircraft component replacement parts if you exclude OEMs and their subcontractors. But just because a company is an industry leader does not mean that it makes for a great prospect to buy into. Admittedly, shares in the company have outperformed the broader market over the past couple of months. But given how pricey shares are, it’s difficult to imagine them moving any higher. While I wouldn’t go so far as to rate the company a ‘sell’, I do think shares are nearing that point.

Too lofty

Back in the middle of October of this year, I wrote a follow-up article discussing the investment worthiness of HEICO. At that time, I talked about how the company had continued to generate strong revenue and profit growth in what is admittedly a difficult environment. My overall conclusion is that the company should continue to fare well in the long run. But performing well from a fundamental perspective does not always translate to performing well from a share price perspective. Given how expensive shares were at the time, I felt as though a more appropriate rating for the company was a ‘hold’ to reflect my view that shares should generate upside or downside that would more or less match with the broader market should achieve. Since then, the company has managed to outperform the market, but only slightly. While the S&P 500 is up 4.4%, shares of HEICO have generated upside of 5.7%.

Author – SEC EDGAR Data

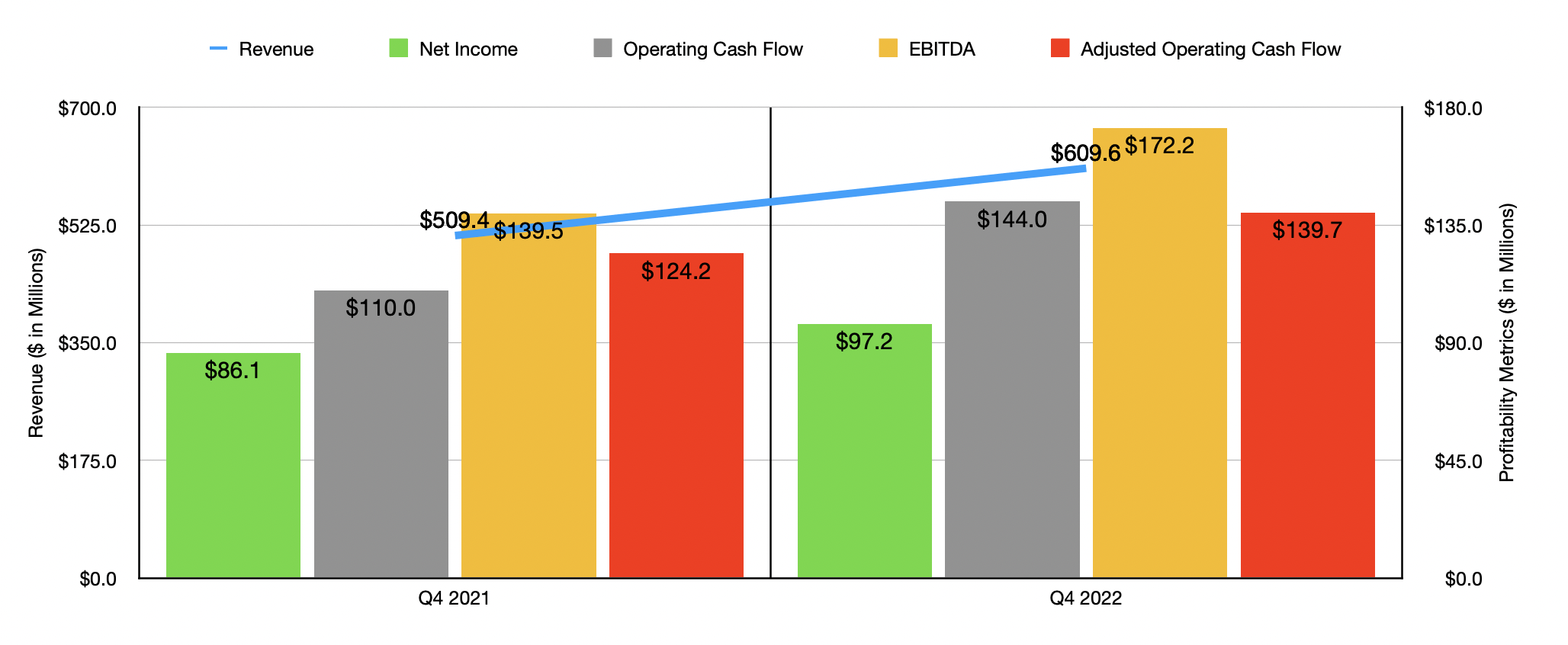

To understand why the company continues to increase in price, we need only touch on its fundamental performance for the final quarter of its 2022 fiscal year. This is the only quarter for which new data is available that was not available when I last wrote about it. During that quarter, revenue totaled $609.6 million. That’s 19.7% higher than the $509.4 million generated at the same time one year earlier. This was not the only quarter for which sales for the company came in strong. According to management, improvement in the commercial aerospace market was instrumental in pushing up sales on a year-over-year basis and pushing up sales, on a sequential basis, for nine consecutive quarters for its Flight Support Group. The company did also have help with other parts of its operations, such as its Electronic Technologies Group, which reported a year-over-year sales increase of 6% thanks largely to acquisitions, some of which was offset by weaker organic revenue.

With this rise in revenue came improved profitability. Net income of $97.2 million in the final quarter of 2022 beat out the $86.1 million reported only one year earlier. Operating cash flow rose from $110 million to $144 million. Though if we adjust for changes in working capital, the increase would have been smaller, with the metric climbing from $124.2 million to $139.7 million. Meanwhile, EBITDA for the business also increased, rising from $139.5 million to $172.2 million.

Author – SEC EDGAR Data

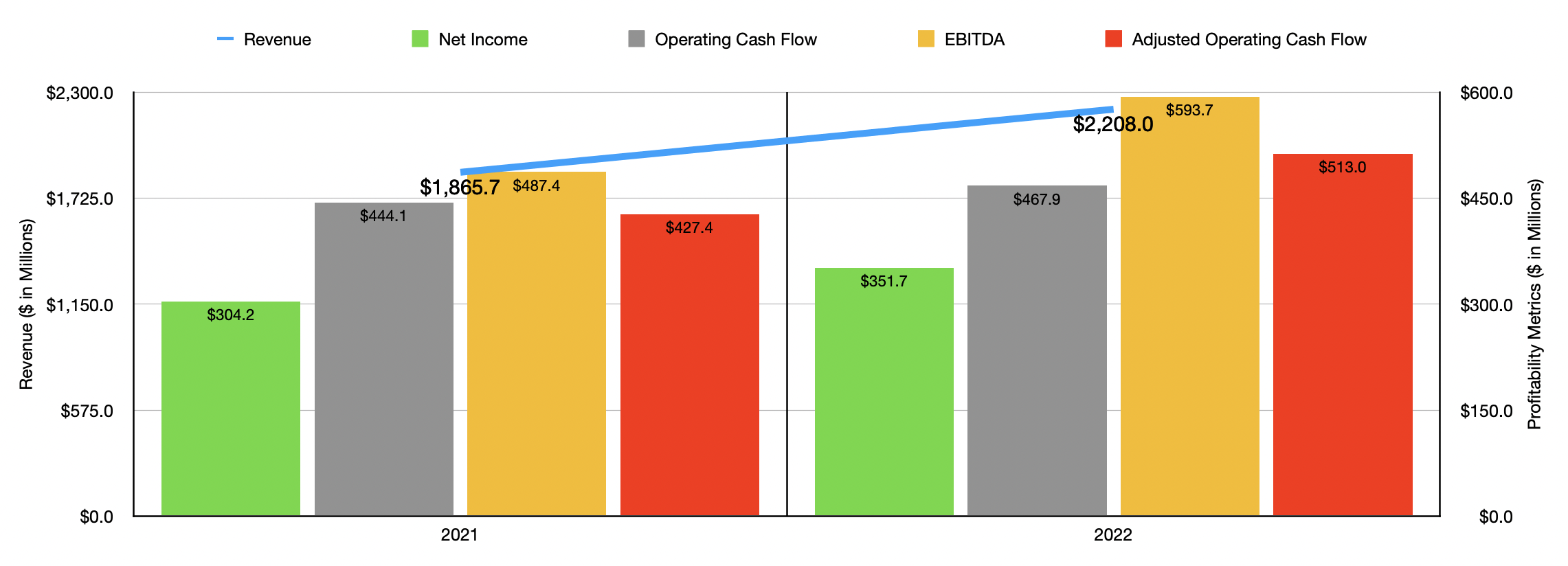

As I alluded to already, this was not the only positive time for the company from a fundamental perspective. For the entirety of the 2022 fiscal year, financial performance had been robust. Sales of $2.21 billion represented a year-over-year improvement of 18.3% compared to the $1.87 billion generated only one year earlier. This brought with it improved profitability as well. Net income rose from $304.2 million to $351.7 million. Operating cash flow rose from $444.1 million to $467.9 million, while the adjusted figure for this increased from $427.5 million to $513 million. Also on the rise was EBITDA, with the metric climbing from $487.4 million to $593.7 million.

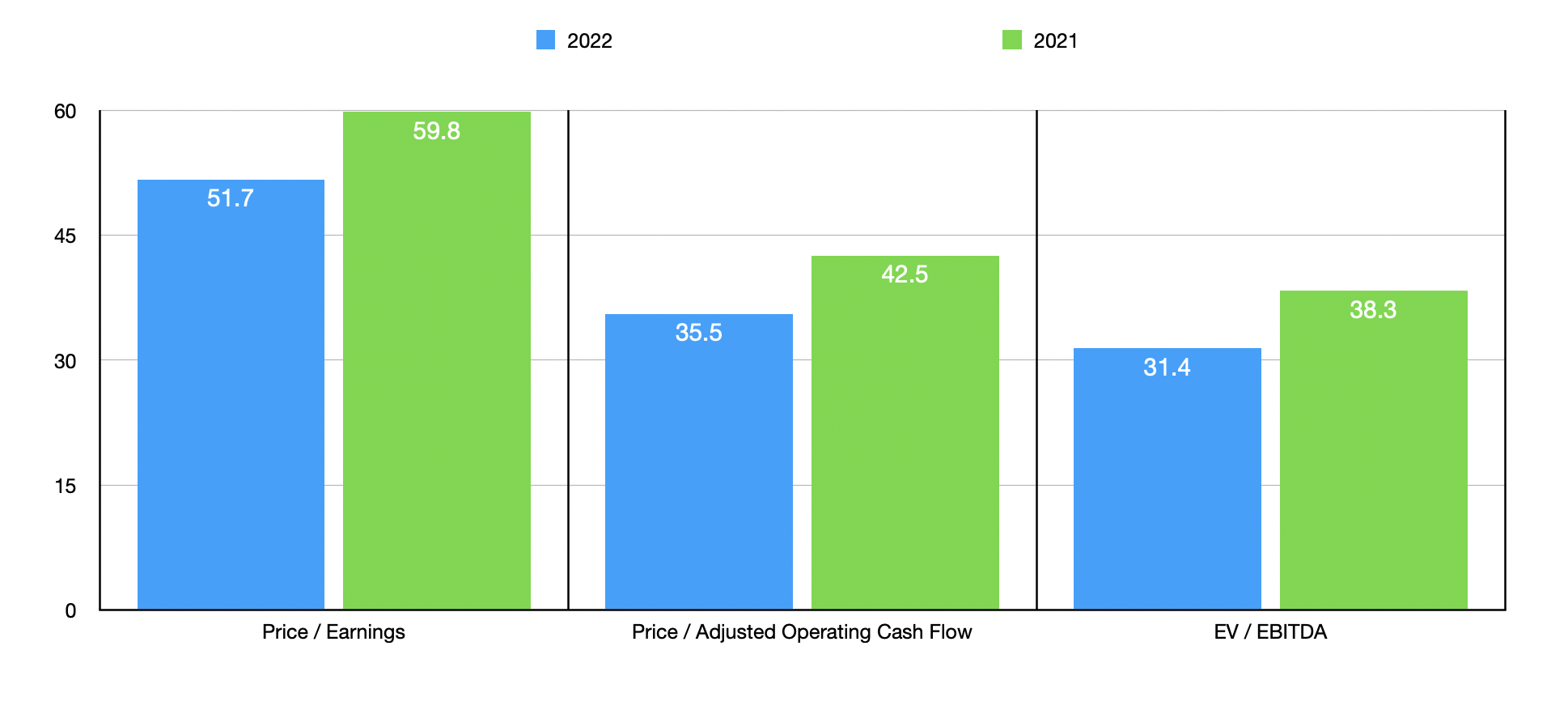

We don’t really have any insight into what 2023 would look like. But using the data from 2022, we can calculate that the company is trading at a price-to-earnings multiple of 51.7. This is significantly higher than what I normally enjoy from a company. For context, it is lower though than the 59.8 reading that we would get using data from the year before. Even though the company is cheaper from a cash flow perspective, the price to operating cash flow multiple is still very high at 35.5. This compares to the 42.5 reading that we get using data from 2021. Meanwhile, the EV to EBITDA multiple for the company comes in at 31.4. That stacks up against the 38.3 reading that we get using data from 2021.

Author – SEC EDGAR Data

As I do in most of my other articles, I decided to compare the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 15.6 to a high of 49.5. Using the price to operating cash flow approach, the range was from 6.8 to 28.8. Meanwhile, the EV to EBITDA multiple for the companies ranged from 8.6 to 19.5. In all three cases, our prospect was the most expensive of the group, with one of those instances resulting in it being substantially more expensive than the next most expensive firm.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| HEICO | 51.7 | 35.5 | 31.4 |

| Howmet Aerospace (HWM) | 38.3 | 28.8 | 19.5 |

| Textron (TXT) | 18.3 | 11.1 | 10.8 |

| Elbit Systems (ESLT) | 15.6 | 23.9 | 8.6 |

| Rolls-Royce Holdings (OTCPK:RYCEY) | 49.5 | 6.8 | 10.2 |

| Huntington Ingalls Industries (HII) | 16.1 | 21.2 | 10.4 |

Takeaway

I understand that this is a space that investors love. In the long run, I have full confidence that the industry will thrive. As the world population grows larger and as trade continues to increase, the need for aircraft will only climb. This likely means that, with good management, HEICO will follow suit. But the fact of the matter is that investors are paying a very high premium for access to this almost guaranteed growth. I don’t mind paying a premium for quality and certainty. But right now, shares are reaching the upper stratosphere and are at risk of becoming overvalued. For now, I have decided to retain my ‘hold’ rating. But I don’t know how much longer that can continue if the stock climbs further from here.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment